Chapter 10 Fixed-Income Securities 183

Suggested Answers to Discussion Questions

10.1 a. On average, total returns on bonds were much higher in the 1980s than in the 1970s. Interest

rates in the bond market (i.e., bond yields) generally rose in the 1970s, which kept total bond

b. During the 1990s, interest rates continued to fall, reaching levels not seen in over 30 years. By

c. Table 10.1 shows that by 2014, bond yields were very low, suggesting that there may be little

room for additional interest rate declines, and hence little room for more capital gains on bonds.

d. Answers will vary with the student’s degree of risk aversion. When students first graduate, they

are 40 years from retirement. Over this time period, extremely good years in the stock market

10.2 a. Agency bonds: bonds issued by government agencies that are high–quality securities. They

b. Municipal bonds: bonds that are the issues of states, counties, cities, and other political

c. Zero-coupon bonds: bonds that make no payments until maturity. Zero coupon bonds are useful

d. Junk bonds: high-yield bonds that have received low, sub-investment-grade ratings (below

e. Foreign bonds: bonds that are issued in a foreign country and priced in that country’s currency.

f. Collateralized mortgage obligations: payments are based on tranches that are short, medium, or

©2017 Pearson Education, Inc.

184 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

10.3 There are no investment products in the world that are purely risk-free, yet the markets like to think

of a risk-free asset for comparison purposes, especially to determine the risk premium for risky

assets. The closest thing the markets have to a purely risk-free asset are the debt securities of the

10.5 Convertible securities start out as bonds (or even preferred stock) and may end up as shares of

common stock if the conversion value at some point exceeds the bond value. Before conversion, the

bonds are usually unsecured debt obligations and subordinated to other forms of debt. Corporations

10.6 LYONs, or liquid yield option notes, add a conversion feature and put option to a zero coupon. Like

a traditional convertible bond, investors can convert the bonds for shares through the conversion

10.7 Answers will depend on the debentures and preferred stock chosen. It may be advantageous for the

instructor to select securities and to use this question as part of a lecture. Convertible issues are not

Solutions to Problems

10.1 Current yield

Annual interest income

Current market price of bond

10.2 Current yield = coupon / market price

©2017 Pearson Education, Inc.

Chapter 10 Fixed-Income Securities 185

10.3 Interest .075 $1,000 $75

10.4 An investor, comparing municipals to corporates, must convert the municipal yield to its fully

taxable equivalent (FTEY):

Since the fully taxable equivalent yield of 7.3% is less than the 7.5% return on the corporate bond,

Yes, the decision very likely would change if this was an “in-state” bond and the investor lived in a

10.5 After-tax yield Before-tax yield [1 {FTR STR (1 FTR)}]

Where: FTR federal tax rate and STR state tax rate.

10.6 Bond A: AA-rated, in-state muni with 6.375% coupon; exempt from both federal and state income

taxes

a. Calculations for fully taxable equivalent yields (FTEY):

Bond A:

Bond yield

FTEY 1 [Federal tax rate State tax rate (1 FTR)]

6.375 6.375

1 [0.35 0.115(1 0.35)] 1 (0.35 0.0748)

11.08%

=– – –

= =

– + – – +

=

Bond B:

Bond yield 7.125

FTEY 10.96%

1 (Federal tax rate) 1 0.35

= = =

– –

186 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Note: Because the Treasury bond is exempt from state taxes only, the yield is adjusted to

b. Ranking on the basis of fully taxable equivalent yield, best to worst:

Bond Coupon FTEY

10.7 Treasury taxable equivalent yield Treasury yield/(1 State tax rate(1-FTR))

Municipal taxable equivalent yield Muni rate/[1 (FTR STR (1 FTR))]

Sara should purchase the municipal bond, as the tax-adjusted yield is 6.49%, which is better than the

tax-adjusted yield of 5.3% on the Treasury bond.

10.8 Current yield

Annual interest income

Current market price of bond

=

Coupon Interest Market Price Current Yield

95

540

All of the above bonds have a current yield of 9.72% and, as such, are identical.

10.9 a.

Coupon Interest Market Price Current Yield

$75

$962.50

As the price of the bond went up, the current yield dropped to 7.79%.

b. HPR

Annual interest income Capital gains

Purchase price

+

=

©2017 Pearson Education, Inc.

Chapter 10 Fixed-Income Securities 187

$75 $962.50 $850 $75 $112.50

$850.00 $850.00

$187.50 22.06%

$850.00

+ – +

= =

= =

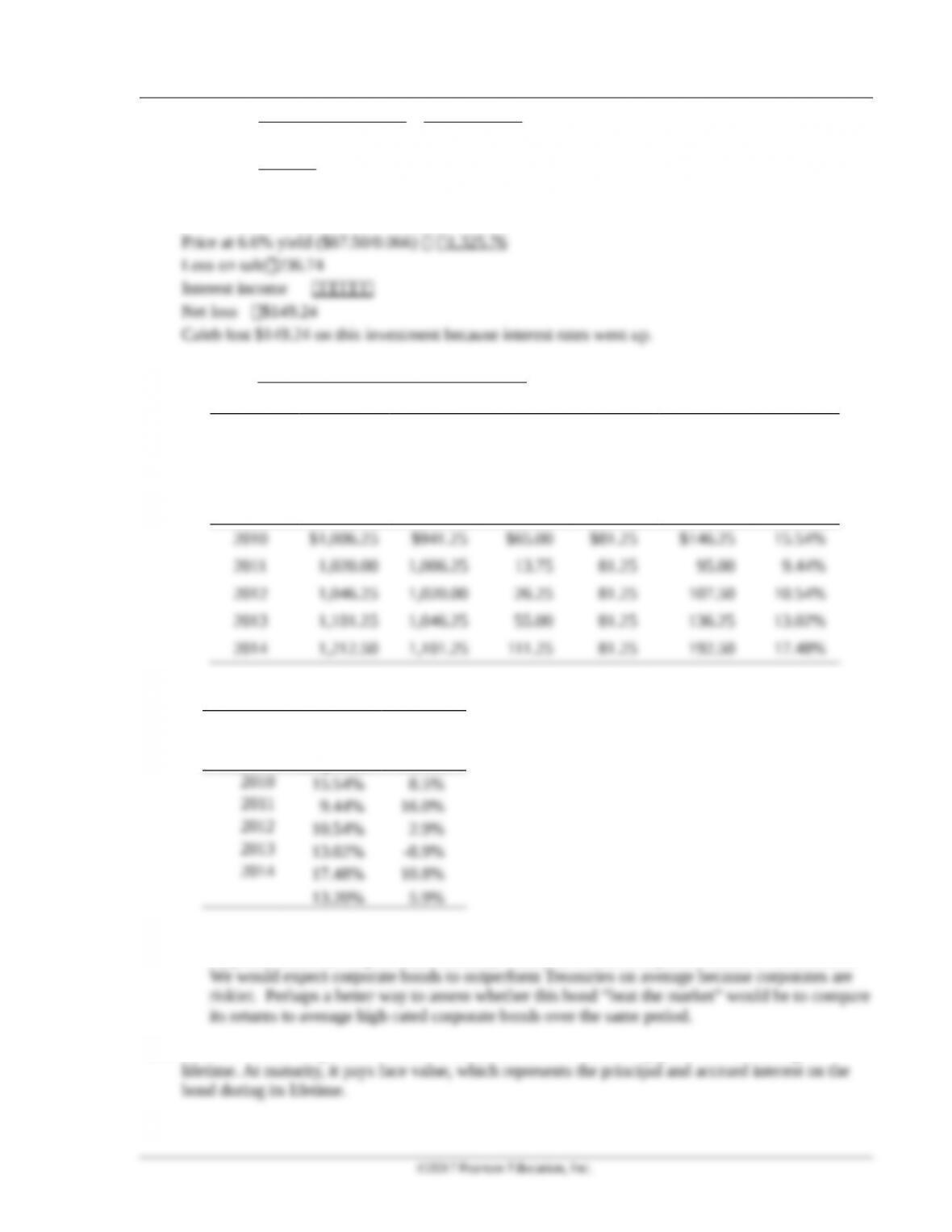

10.10 Price at 5.6% yield ($87.50//0.056) $1,562.50

Price at 6.6% yield ($87.50/0.066) 1,325.76

Loss on sale236.74

Interest income

Net loss $149.24

Caleb lost $149.24 on this investment because interest rates went up.

10.11 a.

Annual interest income + Capital gains

HPR Price at beginning of year

=

(1) (2) (3) (4) (5) (6)

Ending Beginning Capital Annual Total

Year Price Price Gain Income Return HPR

(1) – (2) (3) + (4) (5)

¸

(2)

b. Evaluation of return performance:

Year

High-Rate

d

Corporate T-Bond

Looking at the average HPRs over the five-year period, we can conclude that the high-rated

corporate bond has outperformed Treasury bonds, as would be expected: 13.20% versus 5.9%.

10.12 $20,000. A zero-coupon bond trades at a discount to face value and pays no interest during its

©2017 Pearson Education, Inc.

188 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

10.13 Nate probably purchased an asset-backed security. These securities pay a portion of principal with

10.14 a. Total return in Swiss francs:

Ending value of bond in CHF + Interest in CHF

Total return 1

Beginning value of bond in CHF

11,750 CHF + 950 CHF 1

11,000 CHF

15.45%

= –

= –

=

b. Total return in U.S. dollars:

Ending value of bond in CHF + Interest in CHF

Total return Beginning value of bond in CHF

Exchange rate at end of holding period 1

Exchange rate at beginning of period

(11,750 CHF + 950

r

Total eturn

= ´

–

=CHF) 0.8000 1

11,000 CHF 0.6329

1.4594 1

45.94%

´–

´

= –

=

(Students sometimes ask why CHF is used for Swiss currency. Actually, Fr and SFr are also

commonly used, but CHF is used by financial institutions. Because French, German, Italian and

Romansh are all official languages in Switzerland, the Latin for Swiss Republic Confoederatio

Helevetica skirts the problem of choosing one of the spoken languages.)

10.15 a. If you buy each for $10,000 and sell each for $10,000, the profit will be the interest you earn,

b. The original purchase will be $10,000/1.11 9,009 euros

10.16 Conversion equilvalent= Current Market Price of convertible bond/conversion ratio

Chapter 10 Fixed-Income Securities 189

10.17 If you spend $800 by purchasing shares, you will have 32 shares. If those shares increase in value to

$33, you will earn a profit of $8 per share or $256. That represents a 32% return on your $800

investment.

10.18 Convertible bond: $1,000 face value, 6% coupon, 20-year maturity, convertible into 20 shares;

current price of the convertible is $800, current stock price is $35.

c. Conversion value Conversion ratio Market price of the stock

d. Conversion

premium Current market price of convertible Conversion value

e.

Payback period =

Conversion premium (in $)

Annual interest Annual dividend

income from income from

convertible bond underlying CS

–

=

$100 $100

$60 (20 0.75) $60 $15

=

– ´ –

2.2 years

Investment value Value as a straight (nonconvertible) bond

So the convertible is selling near its floor, or its value as a bond.

10.19 Price of convertible in one year will be 10% over the conversion value.

Conversion value (end of year) Price of stock Conversion ratio

©2017 Pearson Education, Inc.

190 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

Now with $5,000, an investor can buy five bonds priced at $1,000 each. Therefore:

One-year holding period return $3,650/$5,000 73%

Given the convertible is selling at a price of $1,000, which includes a 25% conversion premium:

(A factor of 1.25 is used in this formula since, with a 25% conversion premium, the price of the

convertible will be equal to 125% of the conversion value.)

Conversion value

Price of underlying common stock Security‘s conversion ratio

$800/20 $40/share

=

= =

Note: This problem shows that, while the price of the convertible went up by 65% over the course

of the year (from $1,000 to $1,650), the price of the underlying common stock went up even more:

10.20 The investment value of a convertible bond is done by pricing the bond at a rate equal (or close) to

10.21 Conversion value Conversion ratio Price of common stock

Conversion premium Market price Conversion value

So there is a conversion premium of $18 or 25% ($18/$72).

Conversion parity

Market price of convertible

Conversion ratio

$90 $50

1.8 =

Conversion parity is the price the common stock would have to sell for in order to make the

Chapter 10 Fixed-Income Securities 191

Solutions to Case Problems

Case 10.1 Max and Veronica Develop a Bond Investment Program

This simple case requires the student to choose a fixed-income investment strategy for a couple who hope

to invest on a long-term basis. In particular, the student must review and consider the applicability of

several kinds of issues as they relate to the investment needs of this couple.

a.Max and Veronica don’t rely on the income from their investments for their day-to-day needs. They have

an adequate income, and given that they say that the want to achieve some capital appreciation while

b.Max and Veronica could consider a variety of issues. For example, Treasury obligations maturing in 20

years or more would be one option. Treasury obligations have low risk, are noncallable or have very

long call deferment periods, and are exempt from state and local taxes. Agency issues are another

Case 10.2 The Case of the Missing Bond Ratings

In this case, the student relates various financial ratios to bond ratings in order to assign a bond rating to a

particular issue. The student should review the financial ratios presented in Chapter 6 before solving this

case.

a.Bonds issued by Companies 2, 3, and 6 are investment grade issues. The bonds issued by the other three

(1, 4, and 5) are in the junk bond category. Comparing the various financial ratios, we see that

b.AAA is the highest rating for a bond, while B is the one of the lowest rating for speculative

©2017 Pearson Education, Inc.

192 Smart/Gitman/Joehnk • Fundamentals of Investing, Thirteenth Edition

c.Company 6 ranks second in terms of financial ratios; its current ratio is slightly better than

Companies 1 and 5 are fairly similar with respect to the financial ratios. Even though Company 5 has a

Answer to Chapter-Opening Problem

a. Both upgrades and downgrades are generally trending up over time. The main reason for this is that

b. Downgrades outnumber upgrades in most years. In part, this is because firms typically issue debt

when their credit ratings are high rather than low. That is, if a firm is having financial difficulties and

would have to issue a low-rated bond if it borrowed, the firm is less likely to issue the bond. Instead,

c. The ratio of downgrades to upgrades was relatively high in 1990, 1991, 2001, 2002, 2008, and 2009.

©2017 Pearson Education, Inc.