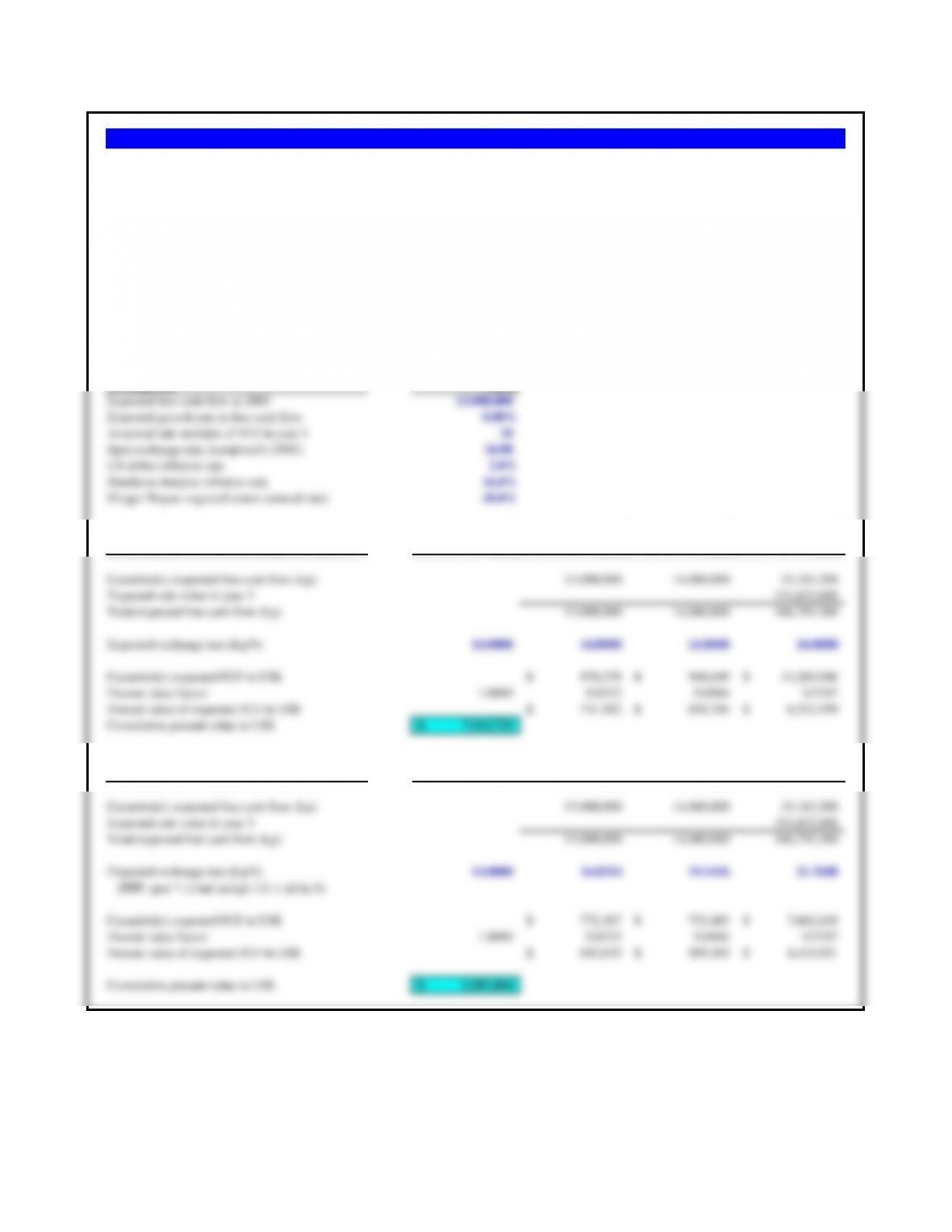

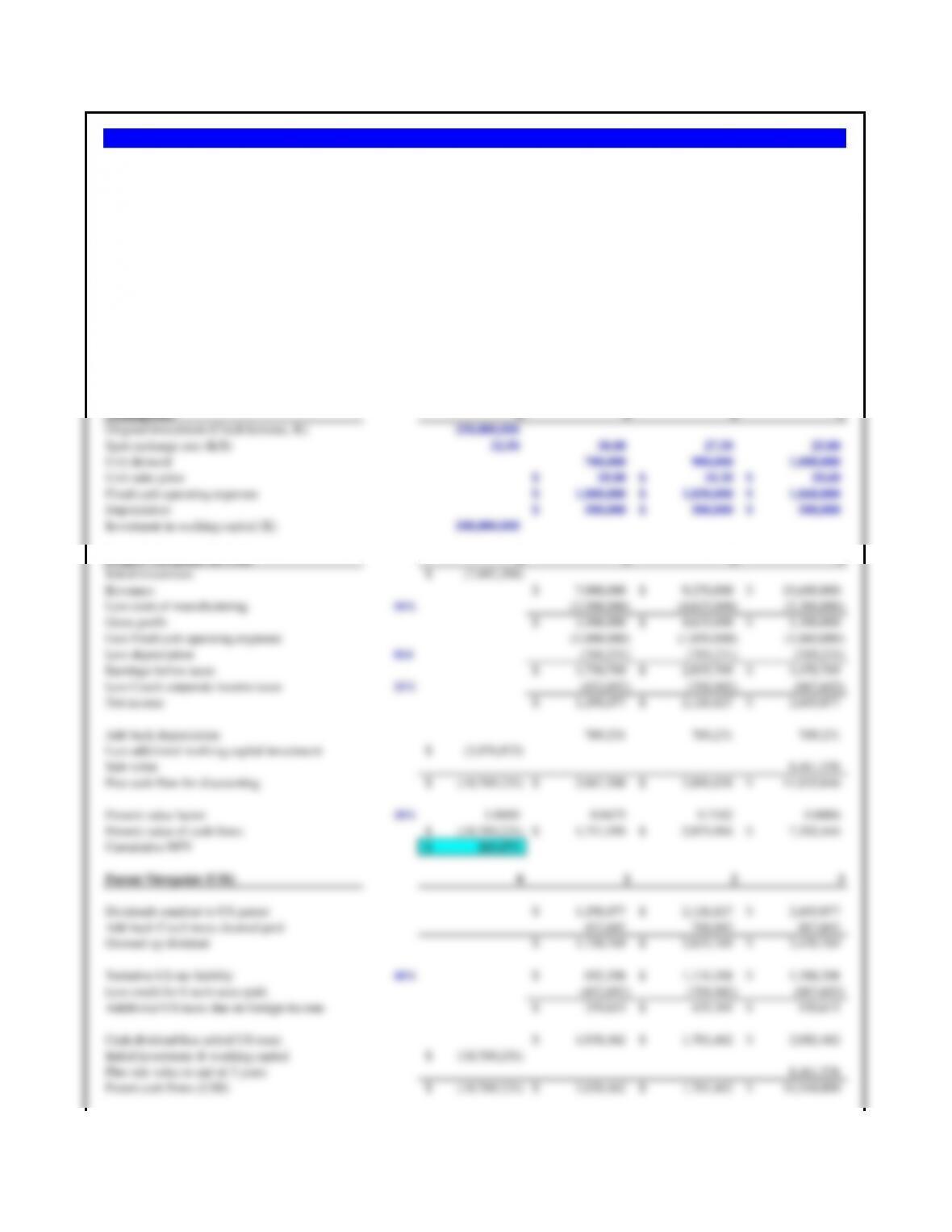

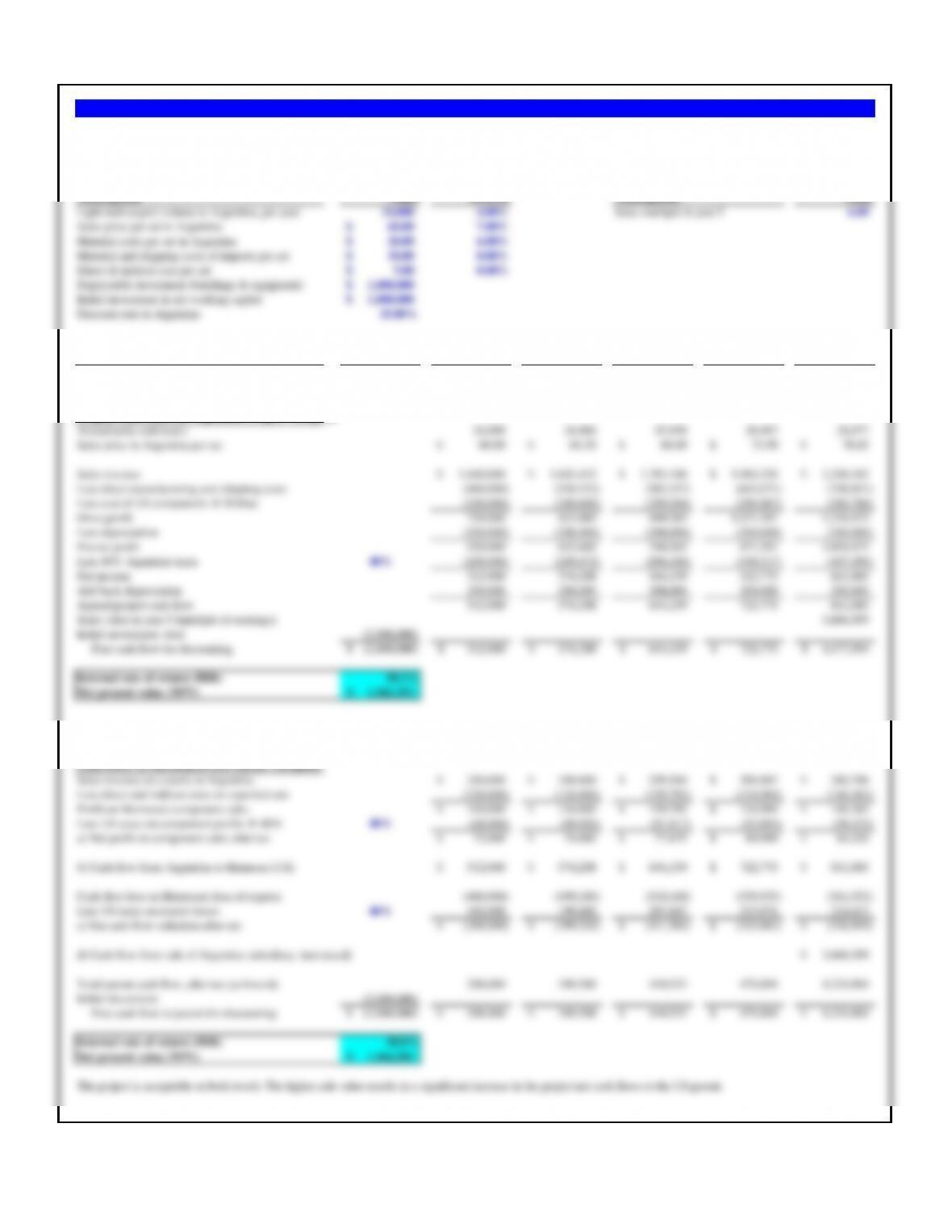

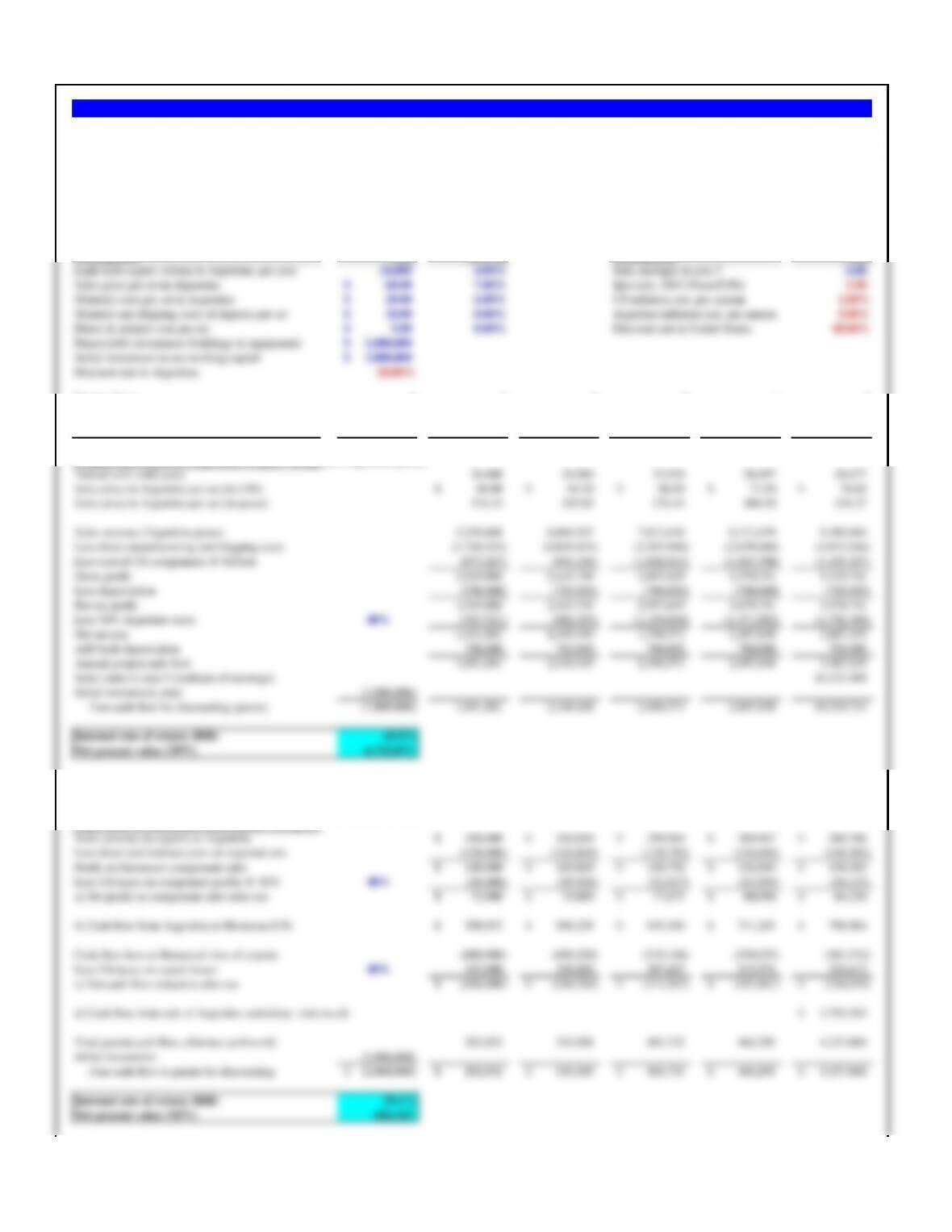

Assumptions Values

Expected free cash flow in 2003 13,000,000

Expected growth rate in free cash flow 8.00%

Assumed sale multiple of FCF in year 3 10

Spot exchange rate, Lempiras/$ (2002) 14.80

US dollar inflation rate 2.0%

Honduran lempira inflation rate 16.0%

Slinger Wayne required return (annual rate) 20.0%

0 1 2 3

a) Carambola’s value if exchange rate fixed 2012 2013 2014 2015

Carambola’s expected free cash flow (Lp) 13,000,000 14,040,000 15,163,200

Expected sale value in year 3 151,632,000

Total expected free cash flow (Lp) 13,000,000 14,040,000 166,795,200

Cumulative present value in US$ 7,912,725$

0 1 2 3

b) Carambola’s value assuming PPP 2012 2013 2014 2015

Present value of expected FCF in US$ 643,639$ 509,363$ 4,434,091$

Cumulative present value in US$ 5,587,094$

a. What is Carambola worth if the Honduran lempira were to remain fixed over the three year investment period?

b. What is Carambola worth if the Honduran lempira were to change in value over time according to purchasing power parity?

Problem 18.1 Carambola de Honduras

A private equity firm like Slinger Wayne, however, is not interested in owning a company for long, and plans to sell Carambola at the end of

three years for approximately 10 times Carambola’s free cash flow in that year. The current spot exchange rate is Lp14.80/$, but the Honduran

inflation rate is expected to remain at a relatively high rate of 16.0% per annum compared to the U.S. dollar inflation rate of only 2.0% per

annum. Slinger Wayne expects to earn at least a 20% annual rate of return on international investments like Carambola.

Slinger Wayne, a U.S.-based private equity firm, is trying to determine what it should pay for a tool manufacturing firm in Honduras named

Carambola. Slinger Wayne estimates that Carambola will generate a free cash flow of 13 million Honduran lempiras (Lp) next year (2012), and

that this free cash flow will continue to grow at a constant rate of 8.0% per annum indefinitely

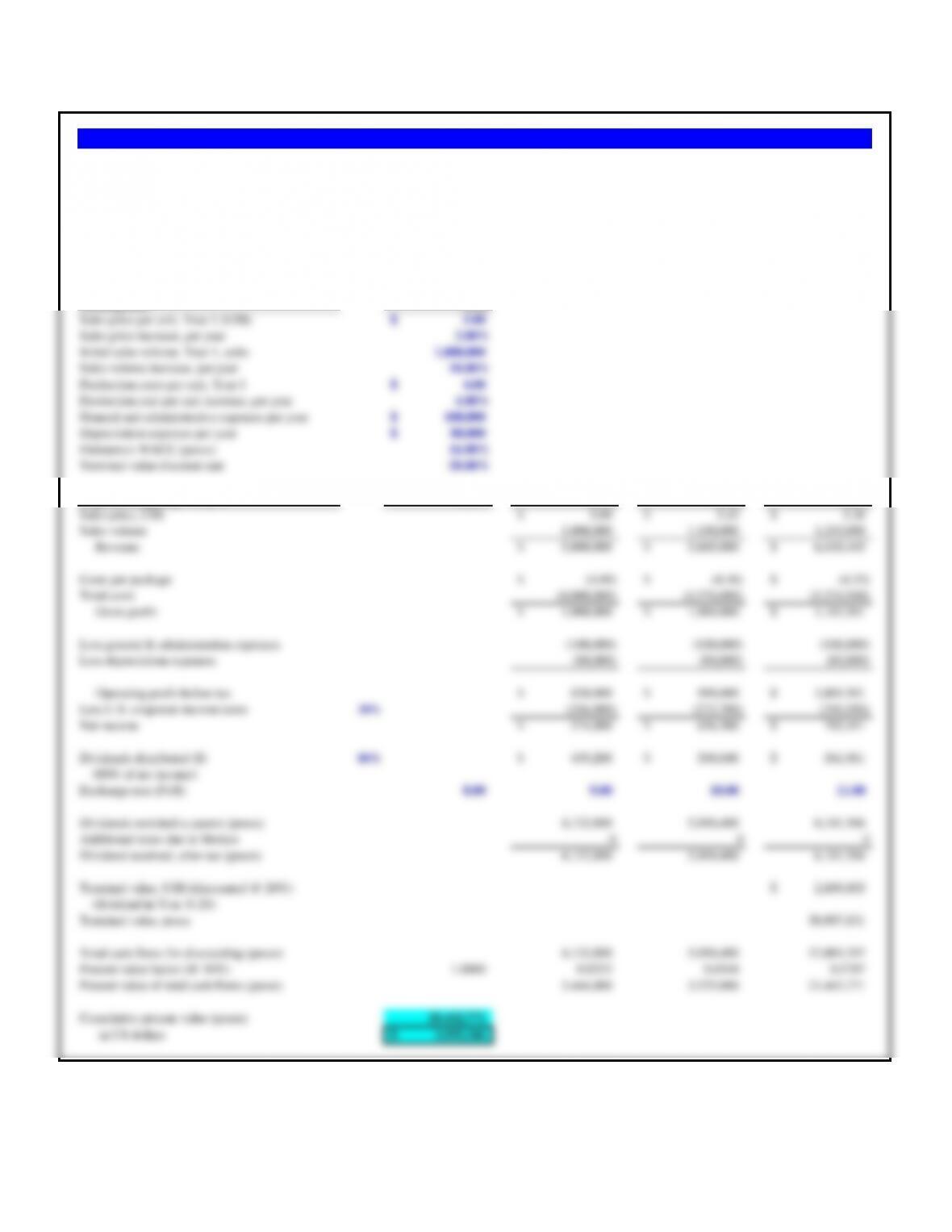

Assumptions Value

Sales price per unit, Year 1 (US$) 5.00$

Sales price increase, per year 3.00%

Initial sales volume, Year 1, units 1,000,000

Sales volume increase, per year 10.00%

Production costs per unit, Year 1 4.00$

Production cost per unit increase, per year 4.00%

General and administrative expenses per year 100,000$

Depreciation expenses per year 80,000$

Finisterra’s WACC (pesos) 16.00%

Terminal value discount rate 20.00%

Less general & administration expenses (100,000) (100,000) (100,000)

Less depreciation expenses (80,000) (80,000) (80,000)

Problem 18.2 Finisterra, S.A.

Finisterra, S.A., located in the state of Baja California, Mexico, manufactures frozen Mexican food which enjoys a large following in the U.S. states of

California and Arizona to the north. In order to be closer to its U.S. market, Finisterra is considering moving some of its manufacturing operations to

southern California. Operations in California would begin in Year 1 and have the following attributes.

The operations in California will pay 80% of its accounting profit to Finisterra as an annual cash dividend. Mexican taxes are calculated on grossed up

dividends from foreign countries, with a credit for host country taxes already paid. What is the maximum U.S. dollar price Finisterra should offer in Year 1

for the investment?

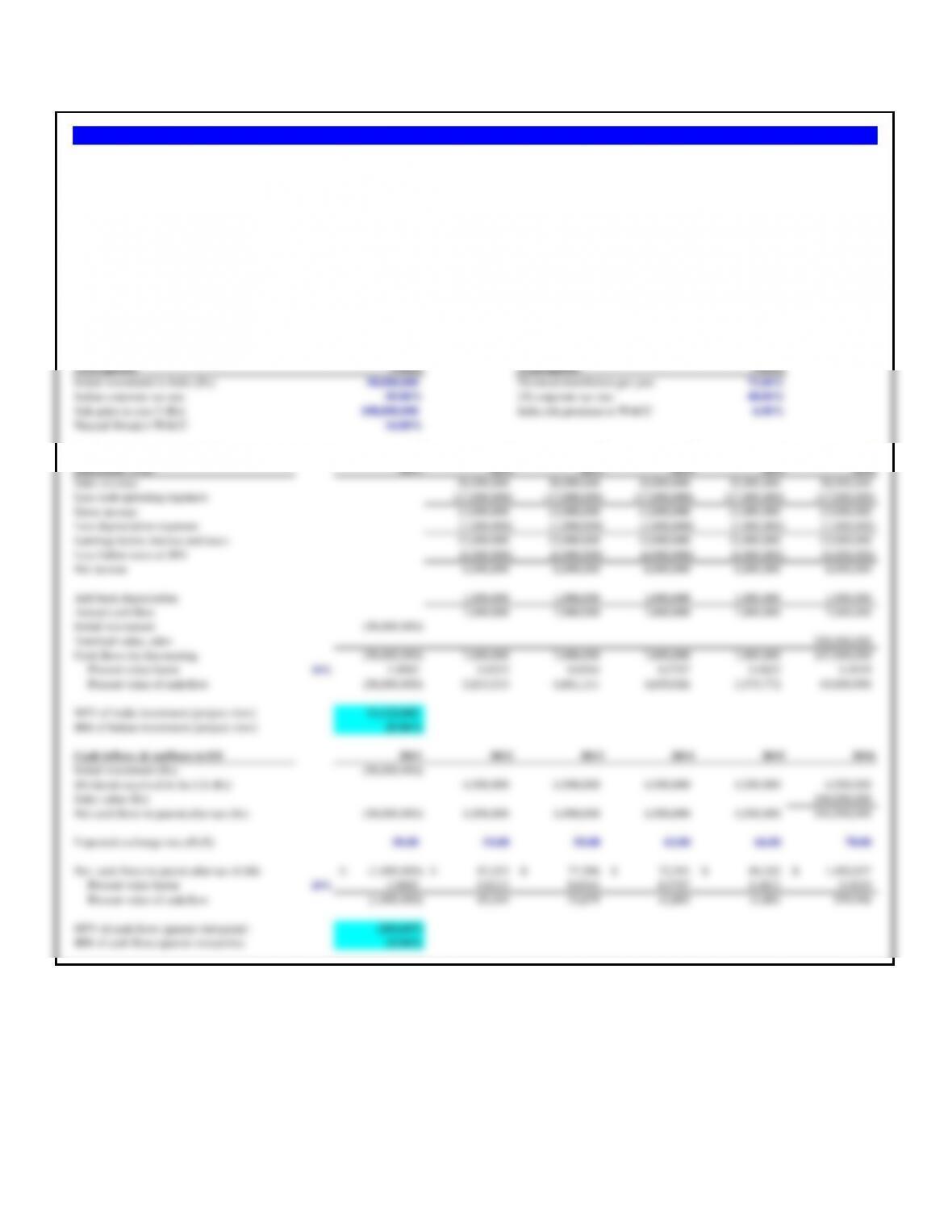

Assumptions Values

Cash dividends to be received (euros) € 720,000

Expected dividend growth rate per year 10.0%

Current spot exchange rate ($/euro) 1.3603$

Grenouille’s weighted average cost of capital 12.0%

a) PV of dividend stream if euro appreciates 4% 0 1 2 3

Dividend stream expected from investment, in euros € 720,000 € 792,000 € 871,200

Current and expected spot rate ($/euro) : spot x ( 1 + .04) 4.0% 1.3603$ 1.4147$ 1.4713$ 1.5302$

Dividends, in US dollars 1,018,593$ 1,165,270$ 1,333,069$

Present value factor 1.0000 0.8929 0.7972 0.7118

Present value of dividends, in US dollars 909,458$ 928,946$ 948,852$

Cumulative NPV

2,787,256$

b) PV of dividend stream if euro depreciates 3% 0 1 2 3

Dividend stream expected from investment, in euros € 720,000 € 792,000 € 871,200

Current and expected spot rate ($/euro) : spot x ( 1 – .03) -3.0% 1.3603$ 1.3195$ 1.2799$ 1.2415$

Dividends, in US dollars 950,034$ 1,013,686$ 1,081,603$

Present value factor 1.0000 0.8929 0.7972 0.7118

Present value of dividends in US dollars 848,244$ 808,104$ 769,863$

Cumulative NPV

2,426,212$

b. What is the present value of the expected dividend stream if the euro were to depreciate 3.00% per annum against the dollar?

Problem 18.3 Grenouille Properties

Grenouille Properties (U.S.) expects to receive cash dividends from a French joint venture over the coming three years. The first dividend , to

be paid December 31, 2011, is expected to be €720,000. The dividend is then expected to grow 10.0% per year over the following two years.

The current exchange rate (December 30, 2010) is $1.3603/€. Grenouille’s weighted average cost of capital is 12%.

a. What is the present value of the expected euro dividend stream if the euro is expected to appreciate 4.00% per annum against the dollar?

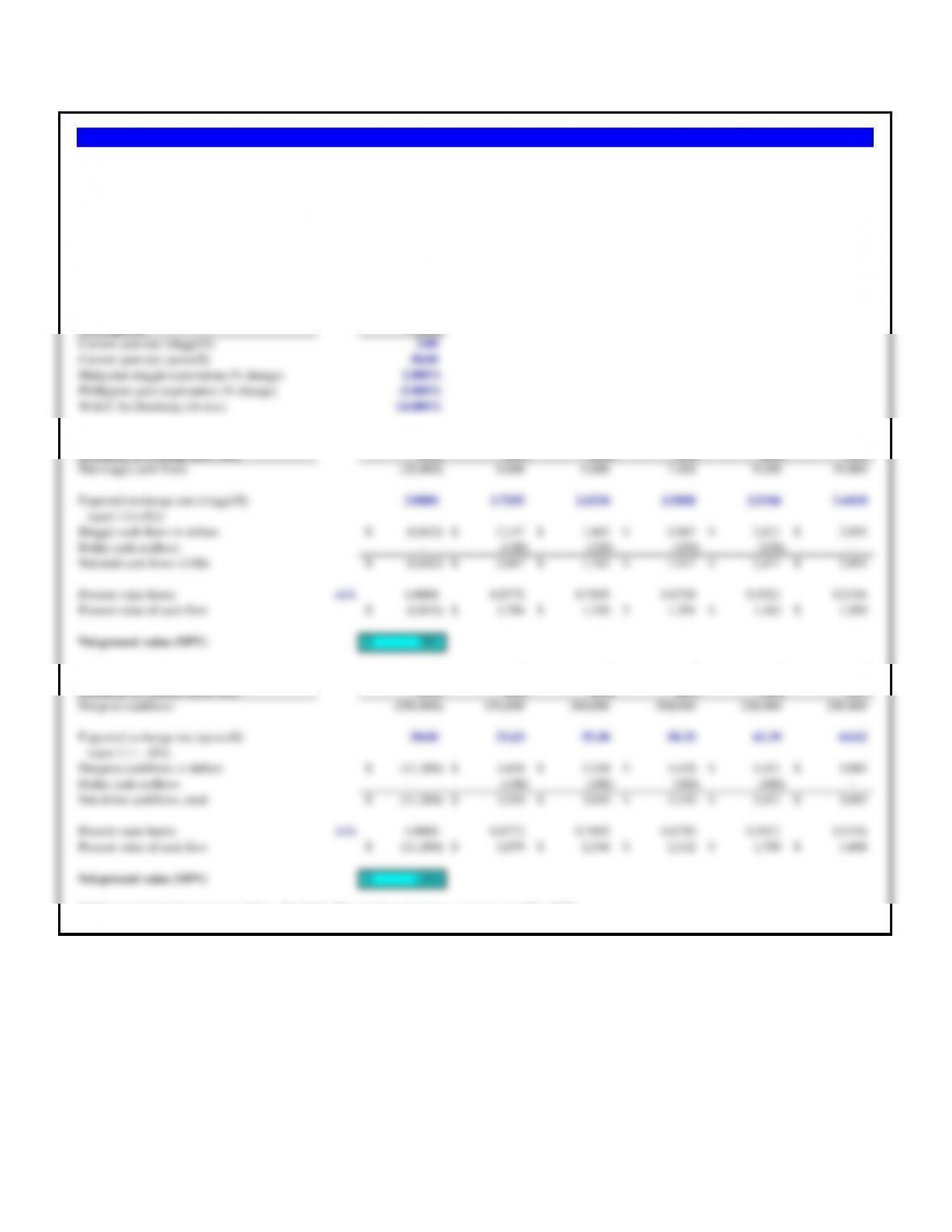

Assumptions Values Assumptions Values

Initial investment in India (Rs) 50,000,000 Dividend distribution per year 75.00%

Indian corporate tax rate 50.00% US corporate tax rate 40.00%

Sale price in year 5 (Rs) 100,000,000 India risk premium to WACC 6.00%

Natural Mosaic’s WACC 14.00%

Pro forma income and cash flow 0 1 2 3 4 5

(December 31st) 2011 2012 2013 2014 2015 2016

Sales revenue 30,000,000 30,000,000 30,000,000 30,000,000 30,000,000

Less cash operating expenses (17,000,000) (17,000,000) (17,000,000) (17,000,000) (17,000,000)

Gross income 13,000,000 13,000,000 13,000,000 13,000,000 13,000,000

Less depreciation expenses (1,000,000) (1,000,000) (1,000,000) (1,000,000) (1,000,000)

Earnings before interest and taxes 12,000,000 12,000,000 12,000,000 12,000,000 12,000,000

Less Indian taxes at 50% (6,000,000) (6,000,000) (6,000,000) (6,000,000) (6,000,000)

Net income 6,000,000 6,000,000 6,000,000 6,000,000 6,000,000

Add back depreciation 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000

Annual cash flow 7,000,000 7,000,000 7,000,000 7,000,000 7,000,000

Initial investment (50,000,000)

NPV of India investment (project view) 11,122,042

IRR of Indian investment (project view) 25.96%

The U.S. corporate tax rate is 40% and the Indian corporate tax rate is 50%. Because the Indian tax rate is greater than the U.S. tax rate, annual dividends paid to Natural

Mosaic will not be subject to additional taxes in the United States. There are no capital gains taxes on the final sale. Natural Mosaic uses a weighted average cost of capital of

14% on domestic investments, but will add 6 percentage points for the Indian investment because of perceived greater risk. Natural Mosaic forecasts the rupee/dollar exchange

rate for December 31st on the next six years are listed below.

What is the net present value and internal rate of return on this investment?

Problem 18.4 Natural Mosaic

Natural Mosaic Company (U.S.) is considering investing Rs50,000,000 in India to create a wholly owned tile manufacturing plant to export to the European market. After five

years the subsidiary would be sold to Indian investors for Rs100,000,000. A pro forma income statement for the Indian operation predicts the generation of Rs7,000,000 of

annual cash flow, is listed below.

The initial investment will be made on December 31, 2011, and cash flows will occur on December 31st of each succeeding year. Annual cash dividends to Philadelphia

Composite from India will equal 75% of accounting income.

Assumptions Values

Current spot rate (ringgit/$) 3.80

Current spot rate (pesos/$) 50.00

Malaysian ringgit expectation (% change) 2.000%

Phillippine peso expectation (% change) -5.000%

WACC for Doohicky Devices 14.000%

0 1 2 3 4 5

Doohicky in Penang (after-tax) 2012 2013 2014 2015 2016 2017

Net ringgit cash flows (26,000) 8,000 6,800 7,400 9,200 10,000

Expected exchange rate (ringgit/$) 3.8000 3.7255 3.6524 3.5808 3.5106 3.4418

(spot / (1+.02))

Ringgit cash flows in dollars (6,842)$ 2,147$ 1,862$ 2,067$ 2,621$ 2,905$

Dollar cash outflows – (100) (120) (150) (150) –

Net total cash flows (US$) (6,842)$ 2,047$ 1,742$ 1,917$ 2,471$ 2,905$

Present value factor 14% 1.0000 0.8772 0.7695 0.6750 0.5921 0.5194

Present value of cash flow (6,842)$ 1,796$ 1,340$ 1,294$ 1,463$ 1,509$

Expected exchange rate (pesos/$) 50.00 52.63 55.40 58.32 61.39 64.62

(spot / ( 1 – .05))

The Malaysia ringgit currently trades at RM3.80/$ and the Philippine peso trades at Ps50.00/$. Doohicky expects the Malaysian ringgit to appreciate 2.0% per

year against the dollar, and the Philippine peso to depreciate 5.0% per year against the dollar. If the weighted average cost of capital for Doohicky Devices is

14.0%, which project looks most promising?

Problem 18.5 Doohicky Devices

Doohickey Devices, Inc., manufactures design components for personal computers. Until the present, manufacturing has been subcontracted to other companies,

but for reasons of quality control Doohicky has decided to manufacture itself in Asia. Analysis has narrowed the choice to two possibilities, Penang, Malaysia,

and Manila, the Philippines. At the moment only the following summary of expected, after tax, cash flows is available. Although most operating outflows would

be in Malaysian ringgit or Philippine pesos, some additional U.S. dollar cash outflows would be necessary, as shown in the table below.

Assumptions 0 1 2 3

Original investment (Czech korunas, K) 250,000,000

Spot exchange rate (K/$) 32.50 30.00 27.50 25.00

Unit demand 700,000 900,000 1,000,000

Unit sales price 10.00$ 10.30$ 10.60$

Fixed cash operating expenses 1,000,000$ 1,030,000$ 1,060,000$

Depreciation 500,000$ 500,000$ 500,000$

Investment in working capital (K) 100,000,000

Less depreciation 10.0 (769,231) (769,231) (769,231)

Earnings before taxes 1,730,769$ 2,835,769$ 3,470,769$

Less Czech corporate income taxes 25% (432,692) (708,942) (867,692)

Variable manufacturing costs are expected to be 50% of sales. No additional funds need be invested in the U.S. subsidiary during the period

under consideration. The Czech Republic imposes no restrictions on repatriation of any funds of any sort. The Czech corporate tax rate is 25%

and the United States rate is 40%. Both countries allow a tax credit for taxes paid in other countries. Wenceslas uses 18% as its weighted average

cost of capital, and its objective is to maximize present value. Is the investment attractive to Wenceslas Refining?

Problem 18.6 Wenceslas Refining Company

Privately owned Wenceslas Refining Company is considering investing in the Czech Republic so as to have a refinery source closer to its

European customers. The original investment in Czech korunas would amount to K250 million, or $5,000,000 at the current spot rate of K32.50/$,

all in fixed assets, which will be depreciated over ten years by the straight-line method. An additional K100,000,000 will be needed for working

capital.

For capital budgeting purposes Wenceslas assumes sale as a going concern at the end of the third year at a price, after all taxes, equal to the net

book value of fixed assets alone (not including working capital). All free cash flow will be repatriated to the United States as soon as possible. In

evaluating the venture, the U.S. dollar forecasts are shown in the table below.

Present value factor 18% 1.0000 0.8475 0.7182 0.6086

Present value of cash flow (10,769,231)$ 880,052$ 1,221,963$ 6,417,404$

Cumulative NPV (2,249,812)$

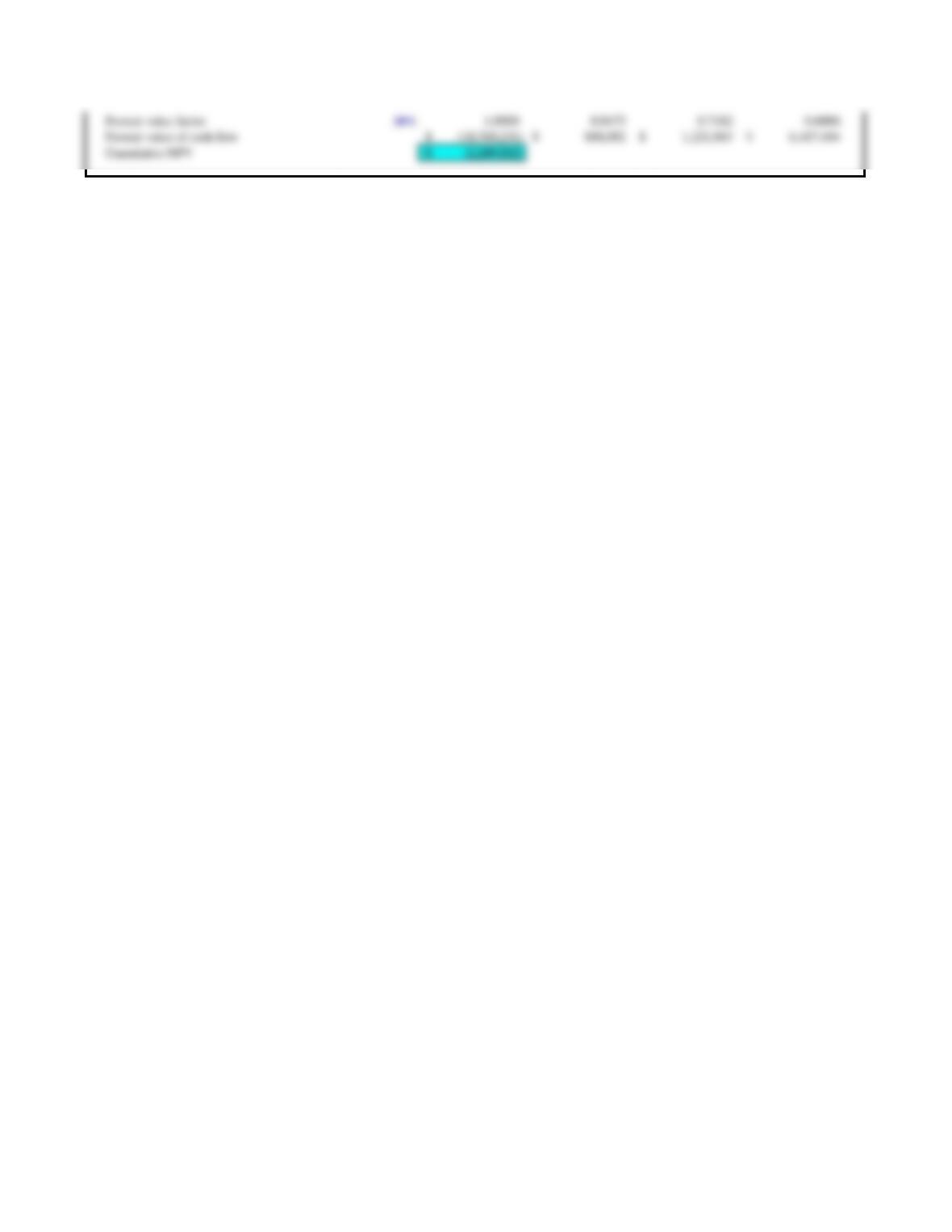

Assumptions Value Growth

Light bulb export volume to Argentina, per year 24,000 0.00%

Sales price per set in Argentina 60.00$ 0.00%

Material costs per set in Argentina 20.00$ 0.00%

Material and shipping costs of imports per set 10.00$ 0.00%

Direct & indirect cost per set 5.00$ 0.00%

Depreciable investment (buildings & equipment) 1,000,000$

Initial investment in net working capital 1,000,000$

Project Cash Flows in Argentina: Project Viewpoint

Annual units sold (sets) 24,000 24,000 24,000 24,000 24,000

Sales price in Argentina per set 60.00$ 60.00$ 60.00$ 60.00$ 60.00$

Sales revenue 1,440,000$ 1,440,000$ 1,440,000$ 1,440,000$ 1,440,000$

Less direct and indirect costs on exported sets (120,000) (120,000) (120,000) (120,000) (120,000)

Profit on Hermosa’s component sales 120,000$ 120,000$ 120,000$ 120,000$ 120,000$

Less US taxes on component profits @ 40% 40% (48,000) (48,000) (48,000) (48,000) (48,000)

a) Net profit on component sales after-tax 72,000$ 72,000$ 72,000$ 72,000$ 72,000$

b) Cash flow from Argentina to Hermosa (US) 512,000 512,000 512,000 512,000 512,000

Evaluate the proposed investment in Argentina by Hermosa Components (US). Hermosa’s management wishes the baseline analysis to be performed in U.S. dollars

(and implicitly also assumes the exchange rate remains fixed throughout the life of the project). Create a project viewpoint capital budget and a parent viewpoint capital

budget. What do you conclude from your analysis?

Problem 18.7 Hermosa Components: Baseline Analysis

Hermosa Beach Components, Inc., of California exports 24,000 sets of low-density light bulbs per year to Argentina under an import license that expires in five years. In

Argentina the bulbs are sold for the Argentine peso equivalent of $60 per set. Direct manufacturing costs in the United States and shipping together amount to $40 per set.

The market for this type of bulb in Argentina is stable, neither growing nor shrinking, and Hermosa holds the major portion of the market.

The Argentine government has invited Hermosa to open a manufacturing plant so imported bulbs can be replaced by local production. If Hermosa makes the

investment, it will operate the plant for five years and then sell the building and equipment to Argentine investors at net book value at the time of sale plus the value of any

net working capital. (Net working capital is the amount of current assets less any portion financed by local debt.) Hermosa will be allowed to repatriate all net income and

depreciation funds to the United States each year. Hermosa traditionally evaluates all foreign investments in U.S. dollar terms.

Total parent cash flow, after-tax (a+b+c+d) 296,000 296,000 296,000 296,000 1,296,000

Initial investment (2,000,000)

Free cash flow to parent for discounting (2,000,000)$ 296,000$ 296,000$ 296,000$ 296,000$ 1,296,000$

Internal rate of return (IRR) 5.9%

Net present value (NPV) (510,585)$

Although the investment has a positive NPV on the project level, the prospective investment from the parent’s viewpoint is negative.

The project as described should be rejected.

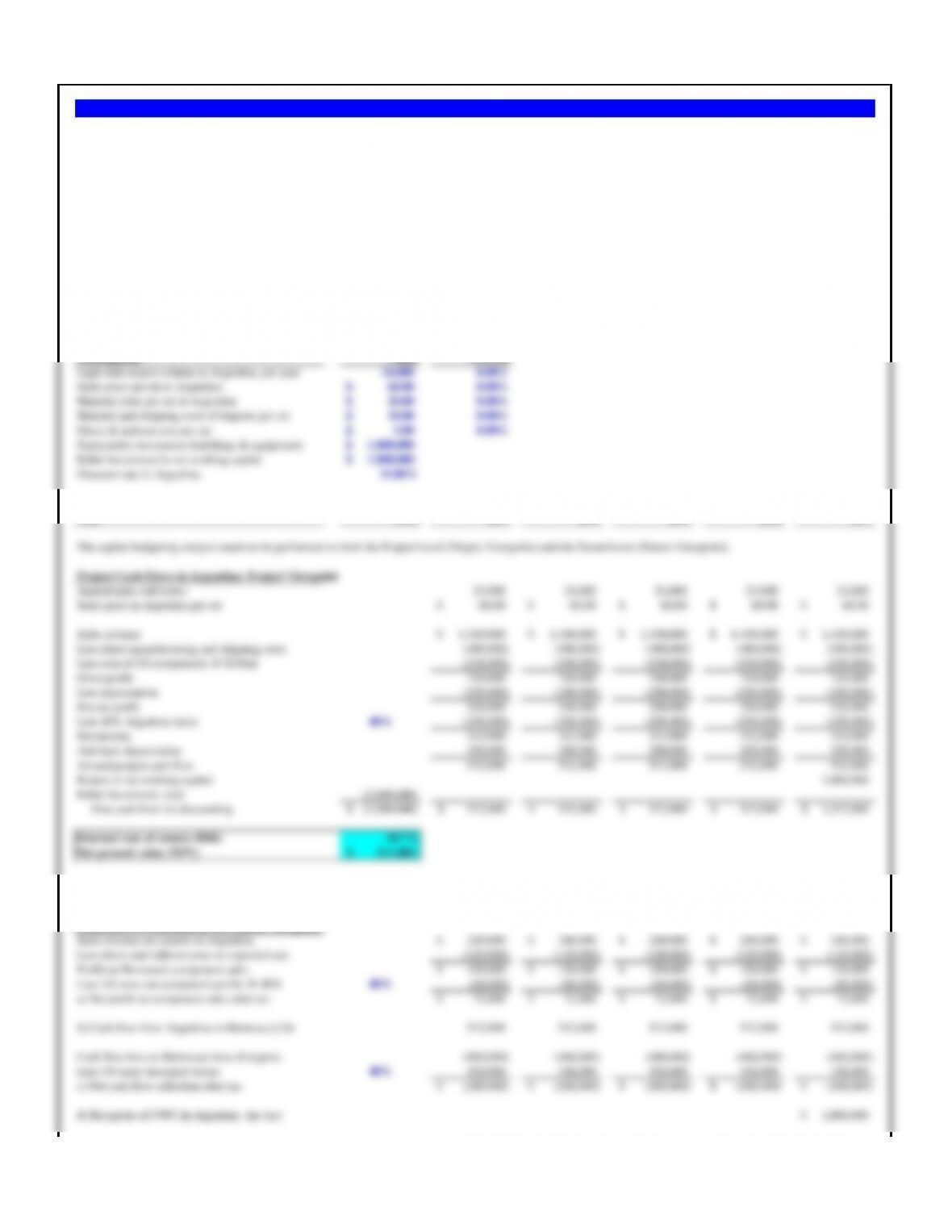

Assumptions Value Growth

Light bulb export volume to Argentina, per year 24,000 4.00%

Sales price per set in Argentina 60.00$ 7.00%

Material costs per set in Argentina 20.00$ 6.00%

Material and shipping costs of imports per set 10.00$ 0.00%

Direct & indirect cost per set 5.00$ 0.00%

Depreciable investment (buildings & equipment) 1,000,000$

Initial investment in net working capital 1,000,000$

Project Cash Flows in Argentina: Project Viewpoint

Annual units sold (sets) 24,000 24,960 25,958 26,997 28,077

Sales price in Argentina per set 60.00$ 64.20$ 68.69$ 73.50$ 78.65$

Sales revenue 1,440,000$ 1,602,432$ 1,783,186$ 1,984,330$ 2,208,162$

Less direct manufacturing and shipping costs (480,000) (529,152) (583,337) (643,071) (708,921)

Less cost of US components @ $10/set (240,000) (249,600) (259,584) (269,967) (280,766)

Gross profit 720,000 823,680 940,265 1,071,291 1,218,475

Less direct and indirect costs on exported sets (120,000) (124,800) (129,792) (134,984) (140,383)

Profit on Hermosa’s component sales 120,000$ 124,800$ 129,792$ 134,984$ 140,383$

Less US taxes on component profits @ 40% 40% (48,000) (49,920) (51,917) (53,993) (56,153)

a) Net profit on component sales after-tax 72,000$ 74,880$ 77,875$ 80,990$ 84,230$

Problem 18.8 Hermosa Components: Revenue Growth Scenario

As a result of their analysis in the previous question, Hermosa wishes to explore the implications of being able to grow sales volume by 4% per year. Argentine inflation is

expected to average 5% per year, so sales price and material cost increases of 7% and 6% per year, respectively, are thought reasonable. Although material costs in

Argentina are expected to rise, US-based costs are not expected to change over the five year period. Evaluate this scenario for both the project and parent viewpoints. Is the

project under this revenue growth scenario acceptable?

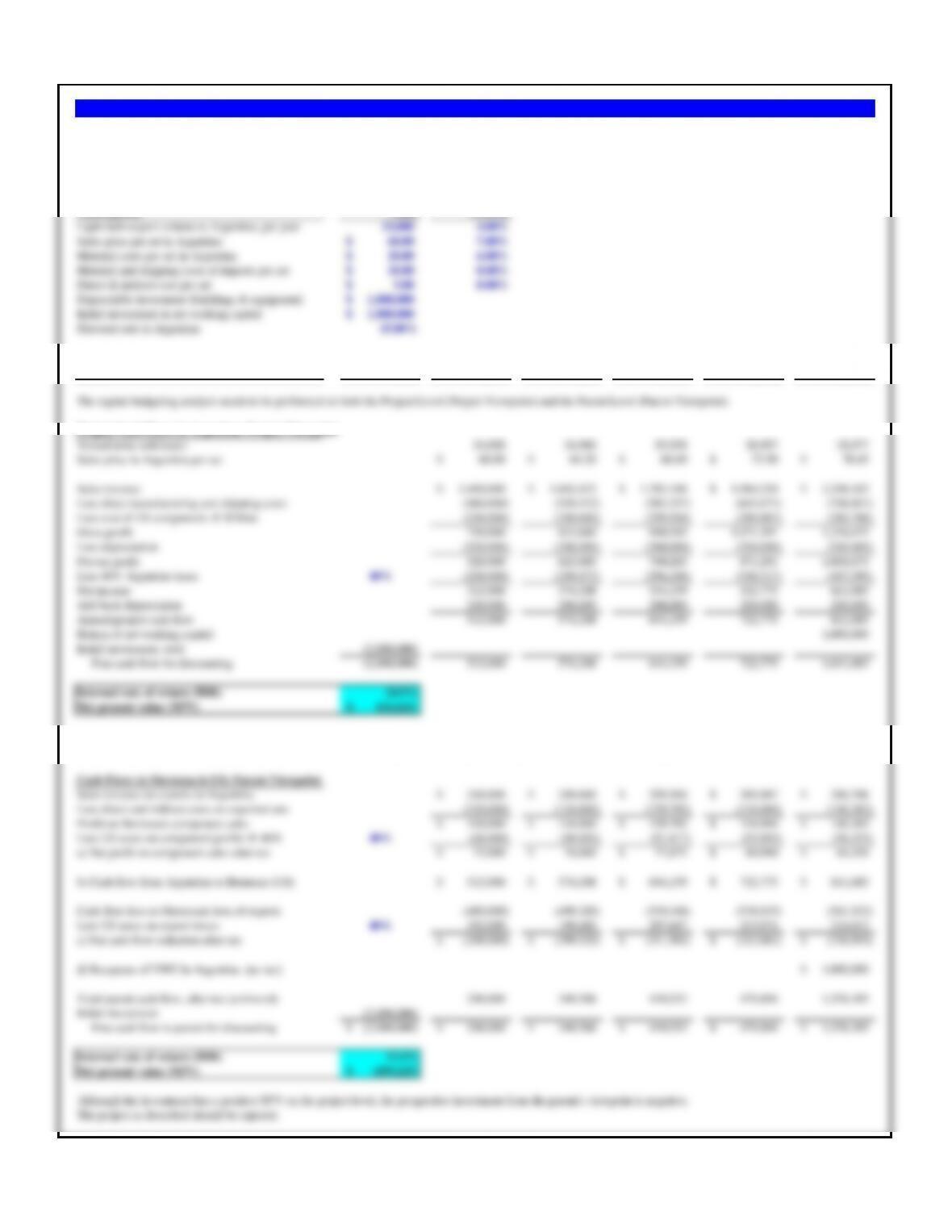

Assumptions Value Growth Assumptions Value

Light bulb export volume to Argentina, per year 24,000 4.00% Sales multiple in year 5 6.00

Sales price per set in Argentina 60.00$ 7.00%

Material costs per set in Argentina 20.00$ 6.00%

Material and shipping costs of imports per set 10.00$ 0.00%

Direct & indirect cost per set 5.00$ 0.00%

Depreciable investment (buildings & equipment) 1,000,000$

Initial investment in net working capital 1,000,000$

Discount rate in Argentina 15.00%

Annual units sold (sets) 24,000 24,960 25,958 26,997 28,077

Sales price in Argentina per set 60.00$ 64.20$ 68.69$ 73.50$ 78.65$

Sales revenue 1,440,000$ 1,602,432$ 1,783,186$ 1,984,330$ 2,208,162$

Less direct manufacturing and shipping costs (480,000) (529,152) (583,337) (643,071) (708,921)

Less cost of US components @ $10/set (240,000) (249,600) (259,584) (269,967) (280,766)

Gross profit 720,000 823,680 940,265 1,071,291 1,218,475

Less depreciation (200,000) (200,000) (200,000) (200,000) (200,000)

Profit on Hermosa’s component sales 120,000$ 124,800$ 129,792$ 134,984$ 140,383$

Less US taxes on component profits @ 40% 40% (48,000) (49,920) (51,917) (53,993) (56,153)

a) Net profit on component sales after-tax 72,000$ 74,880$ 77,875$ 80,990$ 84,230$

b) Cash flow from Argentina to Hermosa (US) 512,000$ 574,208$ 644,159$ 722,775$ 811,085$

Problem 18.9 Hermosa Components: Revenue Growth and Sales Price Scenario

In addition to the assumptions employed in problem 8, Hermosa now wishes to evaluate the prospect of being able to sell the Argentine subsidiary at the end of year 5 at a

multiple of the business’s earnings in that year. Hermosa believes that a multiple of 6 is a conservative estimate of the market value of the firm at that time. Evaluate the

project and parent viewpoint capital budgets.

Assumptions Value Growth Assumptions Value

Light bulb export volume to Argentina, per year 24,000 4.00% Sales multiple in year 5 6.00

Sales price per set in Argentina 60.00$ 7.00% Spot rate, 2003 (Pesos/US$) 3.50

Material costs per set in Argentina 20.00$ 6.00% US inflation rate, per annum 1.00%

Material and shipping costs of imports per set 10.00$ 0.00% Argentine inflation rate, per annum 5.00%

Direct & indirect cost per set 5.00$ 0.00% Discount rate in United States 18.00%

Depreciable investment (buildings & equipment) 1,000,000$

Initial investment in net working capital 1,000,000$

Annual units sold (sets) 24,000 24,960 25,958 26,997 28,077

Sales price in Argentina per set (in US$) 60.00$ 64.20$ 68.69$ 73.50$ 78.65$

Sales price in Argentine per set (in pesos) 218.32 242.85 270.14 300.50 334.27

Sales revenue (Argentine pesos) 5,239,604 6,061,547 7,012,430 8,112,479 9,385,094

Less direct manufacturing and shipping costs (1,746,535) (2,001,632) (2,293,990) (2,629,048) (3,013,046)

Less cost of US components @ $10/set (873,267) (944,166) (1,020,821) (1,103,700) (1,193,307)

Less direct and indirect costs on exported sets (120,000) (124,800) (129,792) (134,984) (140,383)

Profit on Hermosa’s component sales 120,000$ 124,800$ 129,792$ 134,984$ 140,383$

Less US taxes on component profits @ 40% 40% (48,000) (49,920) (51,917) (53,993) (56,153)

a) Net profit on component sales after-tax 72,000$ 74,880$ 77,875$ 80,990$ 84,230$

b) Cash flow from Argentina to Hermosa (US) 508,952$ 568,229$ 635,360$ 711,263$ 796,964$

Problem 18.10 Hermosa Components: Revenue Growth, Sales Price and Currency Risk Scenario

Melinda Deane, a new analysts at Hermosa and a recent MBA graduate, believes that it is a fundamental error to evaluate the Argentine project’s prospective earnings and

cash flows in dollars, rather than first estimating their Argentine peso (Ps) value and then converting cash flow returns to the U.S. in dollars. She believes the correct

method is to use the end-of-year spot rate in 2012 of Ps3.50/$ and assume it will change in relation to purchasing power. (She is assuming U.S. inflation to be 1% per

annum, Argentine inflation to be 5% per annum). She also believes that Hermosa should use a risk-adjusted discount rate in Argentina which reflects Argentine capital

costs (20% is her estimate) and a risk-adjusted discount rate for the parent viewpoint capital budget (18%) on the assumption that international projects in a risky currency

environment should require a higher expected return than other lower risk projects. How do these assumptions and changes alter Hermosa’s perspective on the proposed

investment?

The project is acceptable on both levels, despite the deteriorating peso scenario and the higher discount rates.

Note: One way of checking the accuracy of your spreadsheet solution is to assume that the initial spot rate is Ps1.00/$, and the inflation rates

in both countries are zero. The results should be identical to those in the previous problem.