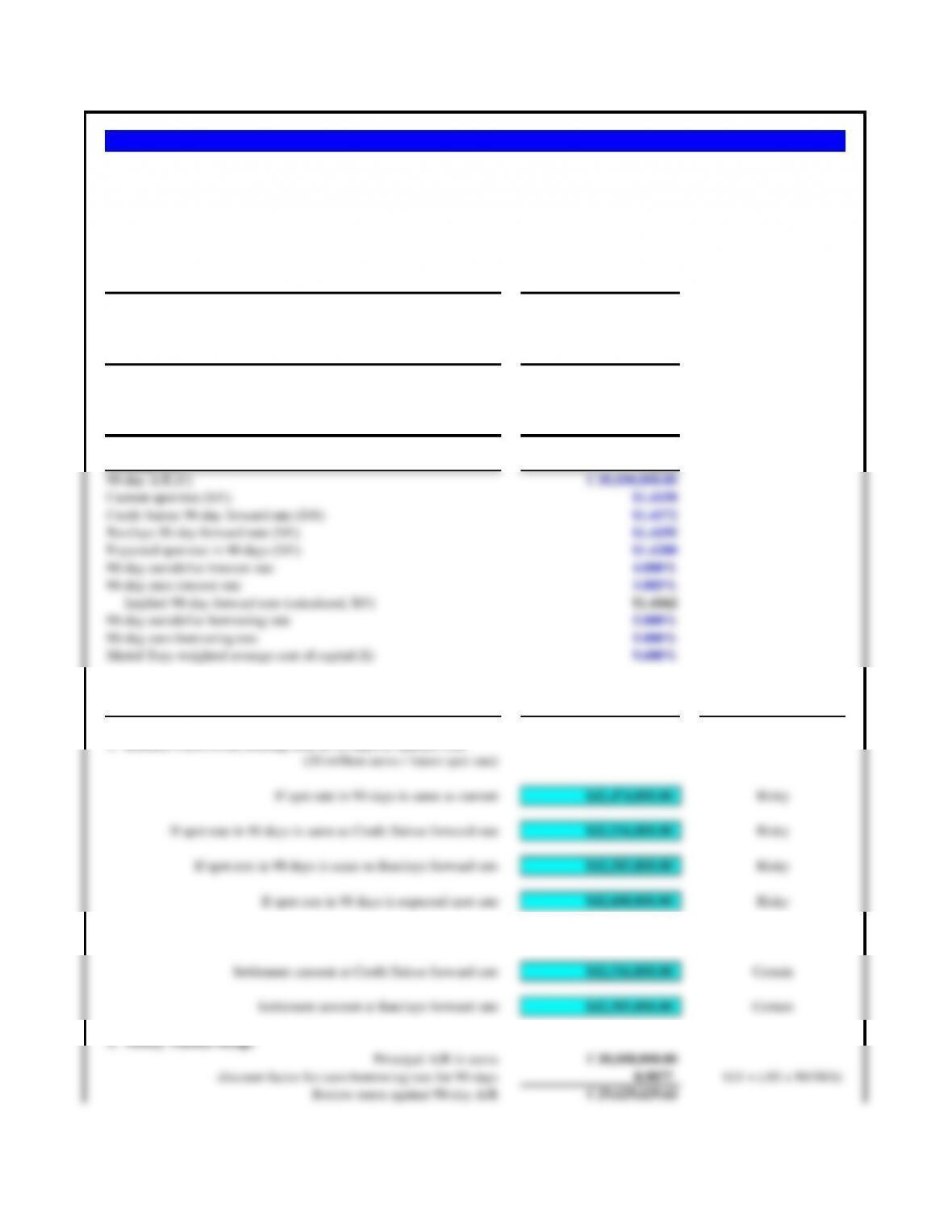

Current spot rate ($/€) $1.4158

Credit Suisse 90-day forward rate ($/€) $1.4172

Barclays 90-day forward rate ($/€) $1.4195

Mattel Toys WACC ($) 9.600%

90-day eurodollar interest rate 4.000%

90-day euro interest rate 3.885%

90-day eurodollar borrowing rate 5.000%

90-day euro borrowing rate 5.000%

Assumptions Values

90-day A/R (€) € 30,000,000.00

Current spot rate ($/€) $1.4158

Credit Suisse 90-day forward rate ($/€) $1.4172

Barclays 90-day forward rate ($/€) $1.4195

Expected spot rate in 90 days ($/€)$1.4200

90-day eurodollar interest rate 4.000%

90-day euro interest rate 3.885%

Implied 90-day forward rate (calculated, $/€)$1.4162

If spot rate in 90 days is same as current $42,474,000.00 Risky

If spot rate in 90 days is same as Credit Suisse forward rate $42,516,000.00 Risky

If spot rate in 90 days is same as Barclays forward rate $42,585,000.00 Risky

3. Money Market Hedge

Principal A/R in euros € 30,000,000.00

discount factor for euro borrowing rate for 90 days 0.9877 1/(1 + (.05 x 90/360))

Borrow euros against 90-day A/R € 29,629,629.63

Problem 10.10 Mattel Toys

Mattel is a U.S.-based company whose sales are roughly two-thirds in dollars (Asia and the Americas) and one-third in euros

(Europe). In September Mattel delivers a large shipment of toys (primarily Barbies and Hot Wheels) to a major distributor in

Antwerp. The receivable, €30 million, is due in 90 days, standard terms for the toy industry in Europe. Mattel’s treasury team has

collected the following currency and market quotes. The company’s foreign exchange advisors believe the euro will be at about

$1.4200/€ in 90 days. Mattel’s management does not use currency options in currency risk management activities. Advise Mattel on

which hedging alternative is probably preferable.

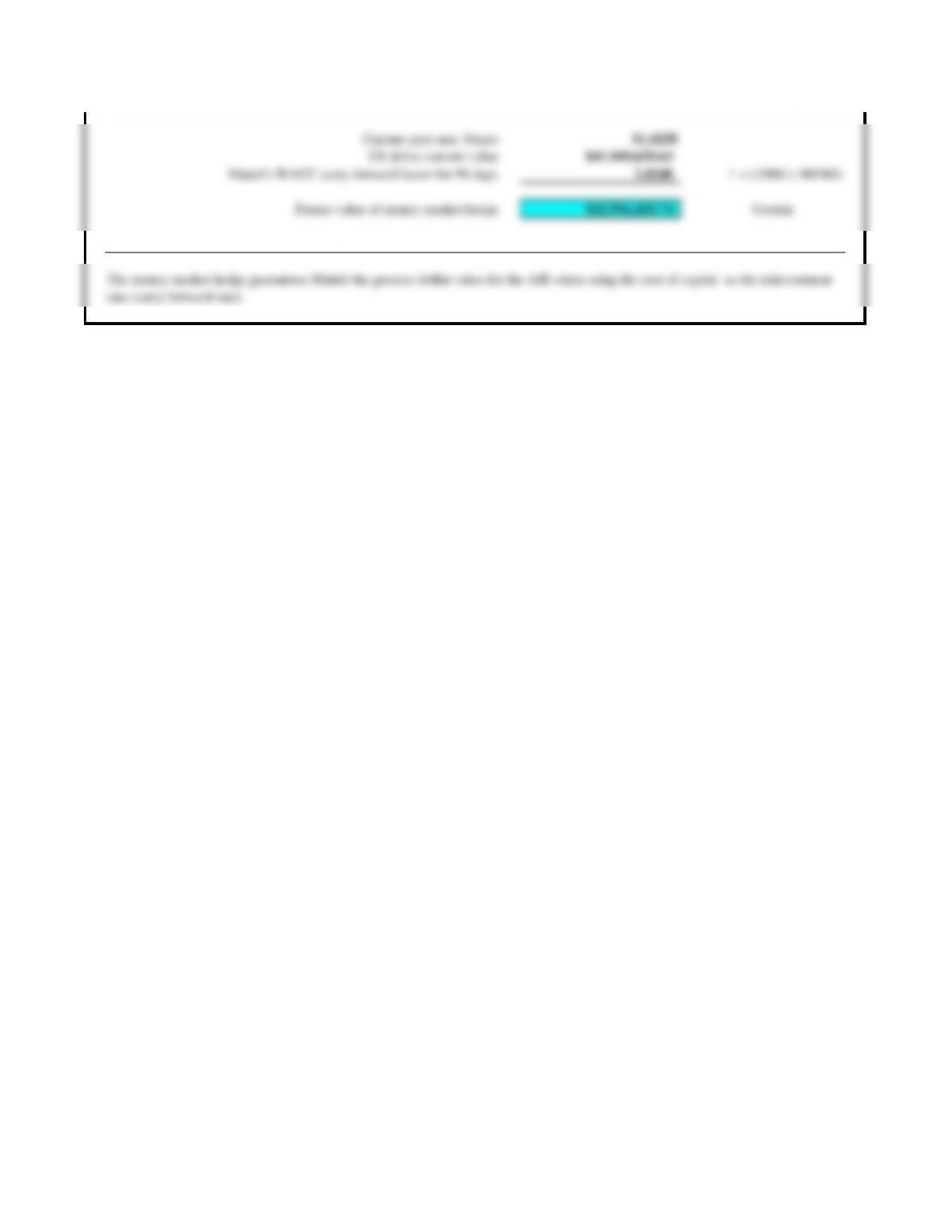

Current spot rate, $/euro $1.4158

US dollar current value $41,949,629.63

Mattel’s WACC carry-forward factor for 90 days 1.0240 1 + (.0960 x 90/360)

Future value of money market hedge $42,956,420.74 Certain

Evaluation of Alternatives

The money market hedge guarantees Mattel the greatest dollar value for the A/R when using the cost of capital as the reinvestment

rate (carry-forward rate).

Assumptions Values

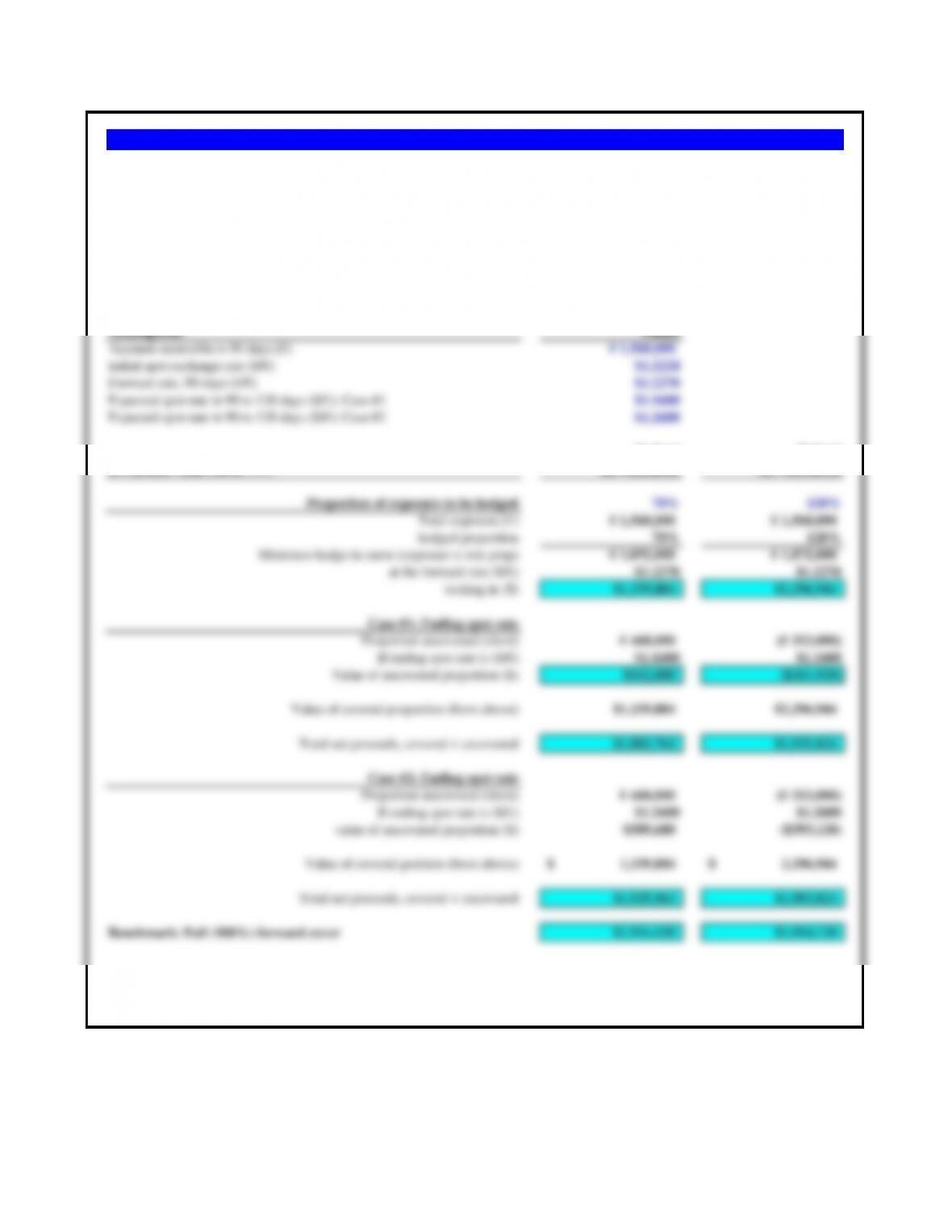

Account recievable in 90 days (€) € 1,560,000

Initial spot exchange rate ($/€)$1.2224

Forward rate, 90 days ($/€)$1.2270

Expected spot rate in 90 to 120 days ($/€): Case #1 $1.1600

Expected spot rate in 90 to 120 days ($/€): Case #2 $1.2600

Hedged Hedged

If Chronos Time Pieces …… the Minimum the Maximum

Proportion of exposure to be hedged 70% 120%

Total exposure (€)€ 1,560,000 € 1,560,000

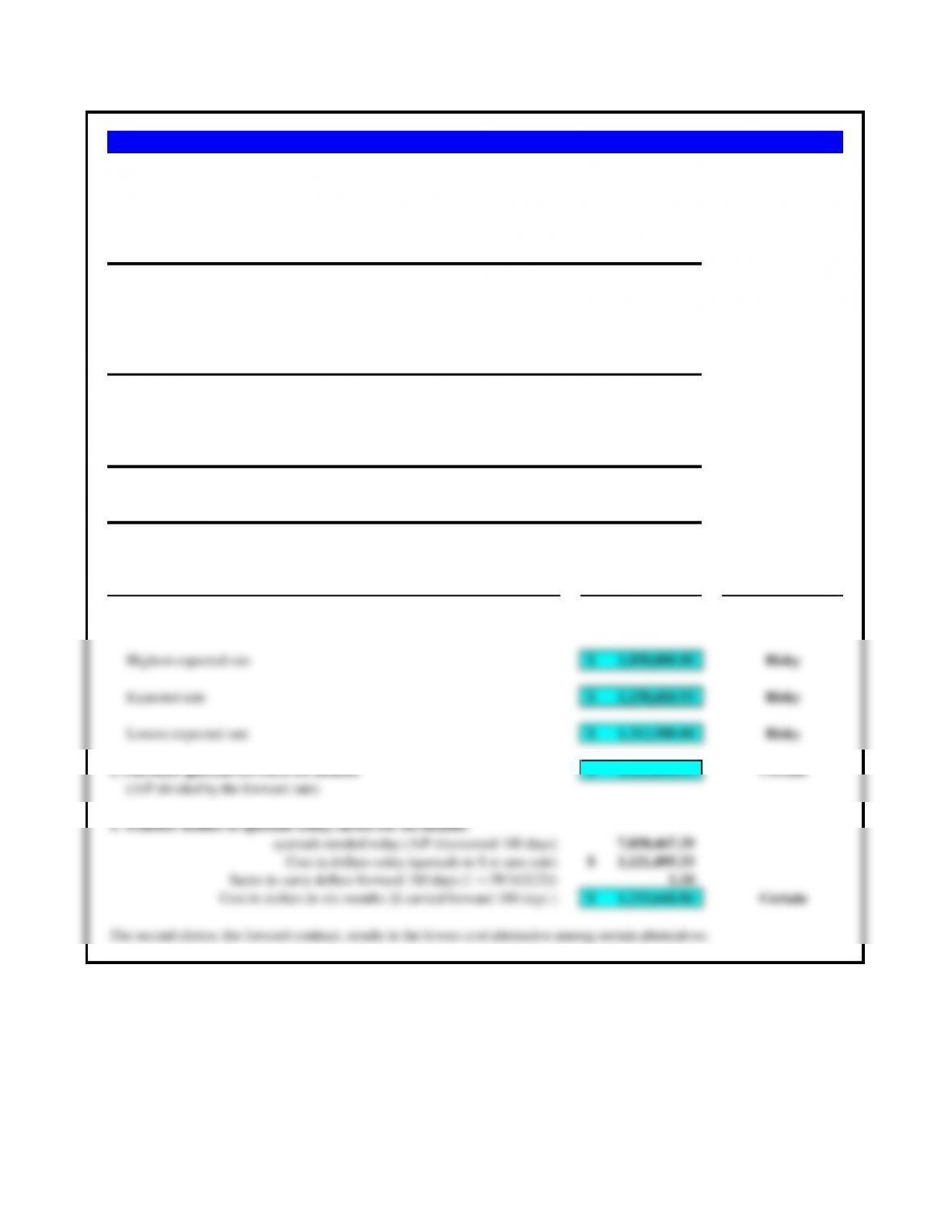

Problem 10.11 Chronos Time Pieces

Chronos Time Pieces of Boston exports wrist watches to many countries, selling in local currencies to watch stores and distributors.

Chronos prides itself on being financially conservative. At least 70% of each individual transaction exposure is hedged, mostly in the

forward market, but occasionally with options. Chronos’s foreign exchange policy is such that the 70% hedge may be increased up to a

120% hedge if devaluation or depreciation appears imminent. Chronos has just shipped to its major North American distributor. It has

issued a 90-day invoice to its buyer for €1,560,000. The current spot rate is $1.2224/€, the 90-day forward rate is $1.2270/€.

Chronos’s treasurer, Manny Hernandez, has a very good track record in predicting exchange rate movements. He currently believes the

euro will weaken against the dollar in the coming 90 to 120 days, possibly to around $1.16/€.

Construction payment due in six-months (A/P, quetzals) 8,400,000

Present spot rate (quetzals/$) 7.0000

Six-month forward rate (quetzals/$) 7.1000

Guatemalan six-month interest rate (per annum) 14.000%

U.S. dollar six-month interest rate (per annum) 6.000%

Farah’s weighted average cost of capital (WACC)

20.000%

Expected spot rate in six-months (quetzals/$):

Highest expected rate (reflecting a significant devaluation) 8.0000

Expected rate 7.3000

Lowest expected rate (reflecting a strengthening of the quetzal)

6.4000

What realistic alternatives are available to Farah for making payments? Which method would you select and why?

What realistic alternatives are available to Farah Jeans? Cost Certainty

1. Wait six months and make payment at spot rate

Highest expected rate 1,050,000.00$ Risky

Expected rate 1,150,684.93$ Risky

Lowest expected rate 1,312,500.00$ Risky

2. Purchase quetzals forward six-months 1,183,098.59$ Certain

(A/P divided by the forward rate)

3. Transfer dollars to quetzals today, invest for six-months

quetzals needed today (A/P discounted 180 days) 7,850,467.29

Cost in dollars today (quetzals to $ at spot rate) 1,121,495.33$

factor to carry dollars forward 180 days (1 + (WACC/2)) 1.10

Cost in dollars in six-months ($ carried forward 180 days ) 1,233,644.86$ Certain

Problem 10.12 Farah Jeans

Farah’s treasury manager, concerned about the Guatemalan economy, wonders if Farah should be hedging its foreign exchange

risk. The manager’s own forecast is as follows:

Farah Jeans of San Antonio, Texas, is completing a new assembly plant near Guatemala City. A final construction payment of

Q8,400,000 is due in six months. (“Q” is the symbol for Guatemalan quetzals.) Farah Jeans uses 20% per annum as its

weighted average cost of capital. Today’s foreign exchange and interest rate quotations are:

a. What will be the amount of foreign exchange gain (loss) upon settlement?

b. If Jason hedges the exposure with a forward contract, what will be the net foreign exchange gain (loss) on settlement?

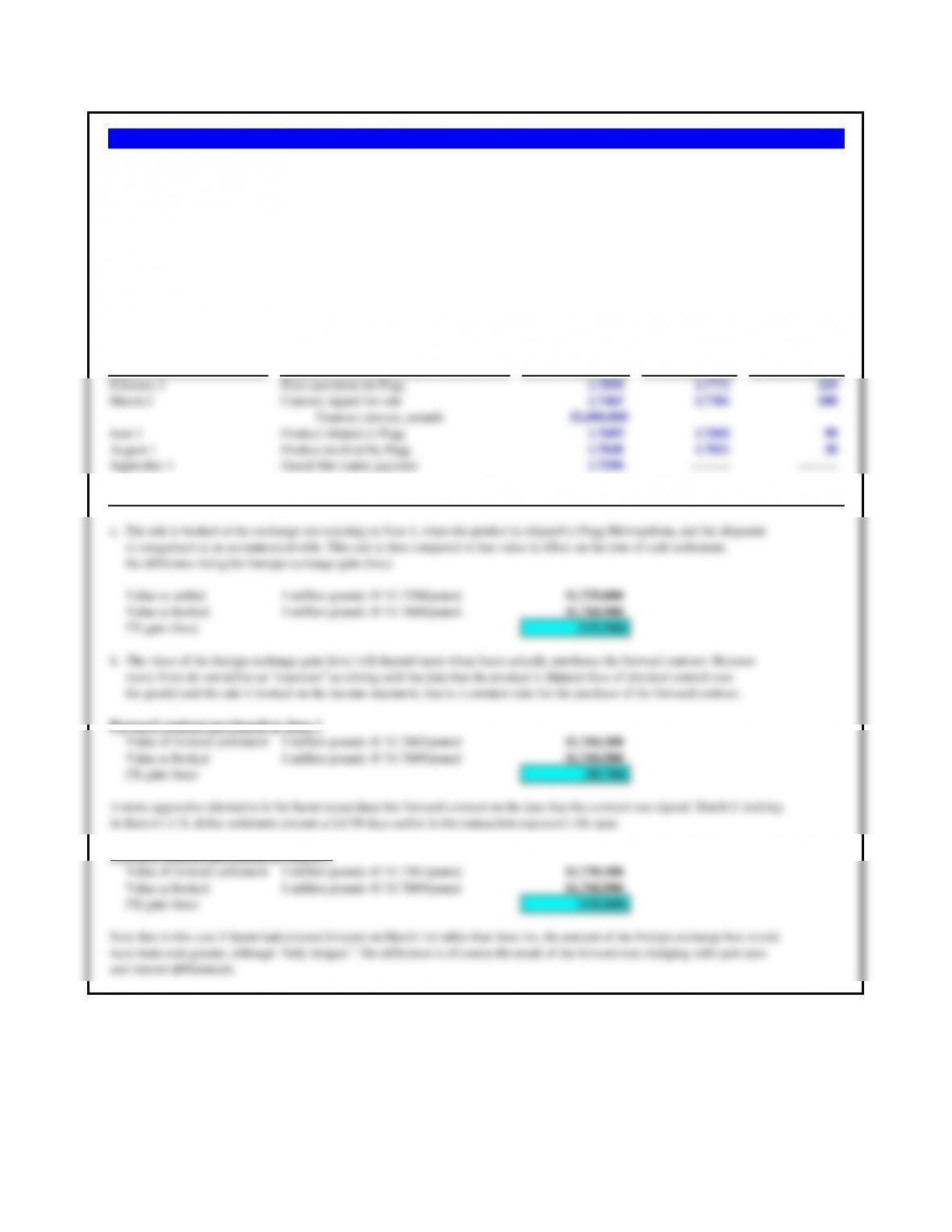

Spot Rate Forward Rate Days Forward

Date Event ($/£) ($/£) of Forward Rate

February 1 Price quotation for Pegg 1.7850 1.7771 210

March 1 Contract signed for sale 1.7465 1.7381 180

Contract amount, pounds £1,000,000

June 1 Product shipped to Pegg 1.7689 1.7602 90

August 1 Product received by Pegg 1.7840 1.7811 30

September 1 Grand Met makes payment 1.7290 ——— ———

Analysis

a. The sale is booked at the exchange rate existing on June 1, when the product is shipped to Pegg Metropolitan, and the shipment

is categorized as an account receivable. This sale is then compared to that value in effect on the date of cash settlement,

the difference being the foreign exchange gain (loss).

Value as settled 1 million pounds @ $1.7290/pound $1,729,000

Value as booked 1 million pounds @ $1.7689/pound $1,768,900

Forward contract purchased on June 1

Value of forward settlement 1 million pounds @ $1.7602/pound $1,760,200

Value as booked 1 million pounds @ $1.7689/pound $1,768,900

Note that in this case if Jason had covered forward on March 1st rather than June 1st, the amount of the foreign exchange loss would

have been even greater, although “fully hedged.” The difference is of course the result of the forward rate changing with spot rates

and interest differentials.

Problem 10.13 Burton Manufacturing

Jason Stedman is the director of finance for Burton Manufacturing, a U.S.-based manufacturer of hand-held computer systems for inventory

management. Burton’s system combines a low-cost active tag that is attached to inventory items (the tag emits a low-grade radio frequency) with

custom-designed hardware and software that tracks the low-grade emissions for inventory control. Burton has completed the sale of a inventory

management system to a British firm, Pegg Metropolitan (UK), for a total payment of £1,000,000. The exchange rates shown were available to

Burton on the following dates corresponding to the events of this specific export sale. Assume each month is 30 days.

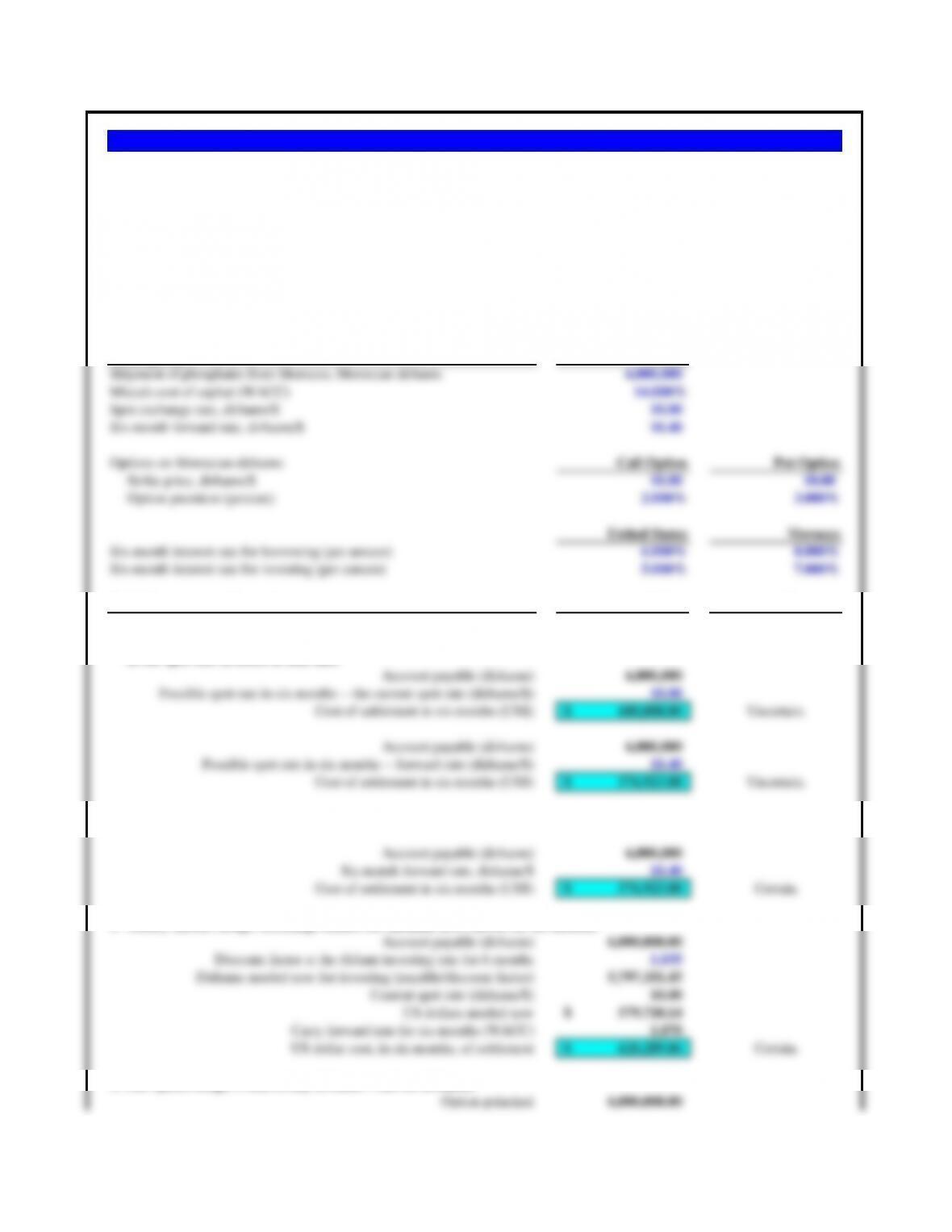

Assumptions Values

Shipment of phosphates from Morocco, Moroccan dirhams 6,000,000

Micca’s cost of capital (WACC) 14.000%

Spot exchange rate, dirhams/$ 10.00

Six-month forward rate, dirhams/$ 10.40

Options on Moroccan dirhams: Call Option Put Option

Strike price, dirhams/$ 10.00 10.00

Cost of settlement in six months (US$) 600,000.00$ Uncertain.

Account payable (dirhams) 6,000,000

Possible spot rate in six months — forward rate (dirhams/$) 10.40

Cost of settlement in six months (US$) 576,923.08$ Uncertain.

3. Money market hedge. Exchange dollars for dirhams now, invest for six months.

Account payable (dirhams) 6,000,000.00

Discount factor at the dirham investing rate for 6 months 1.035

Carry forward rate for six months (WACC) 1.070

US dollar cost, in six months, of settlement 620,289.86$ Certain.

Problem 10.14 Micca Metals, Inc.

Six-month call options on 6,000,000 dirhams at an exercise price of 10.00 dirhams per dollar are available from Bank Al-

Maghrub at a premium of 2%. Six-month put options on 6,000,000 dirhams at an exercise price of 10.00 dirhams per dollar are

available at a premium of 3%. Compare and contrast alternative ways that Micca might hedge its foreign exchange transaction

exposure. What is your recommendation?

Micca Metals, Inc. is a specialty materials and metals company located in Detroit, Michigan. The company specializes in specific

precious metals and materials which are used in a variety of pigment applications in many other industries including cosmetics,

appliances, and a variety of high tinsel metal fabricating equipment. Micca just purchased a shipment of phosphates from

Morocco for 6,000,000, dirhams, payable in six months.

Current spot rate, dirhams/$ 10.00

Premium cost of option 2.000%

Option premium (principal/spot rate x % pm) 12,000.00$

If option exercised, dollar cost at strike price of 10.00 dirhams/$ 600,000.00$

Plus premium carried forward six months (pm x 1.07, WACC) 12,840.000

Total net cost of call option hedge if exercised 612,840.00$ Maximum.

The lowest cost certain alternative is the forward. If Micca were to expect the dirham to depreciate significantly over the next six

months, it may choose the call option.

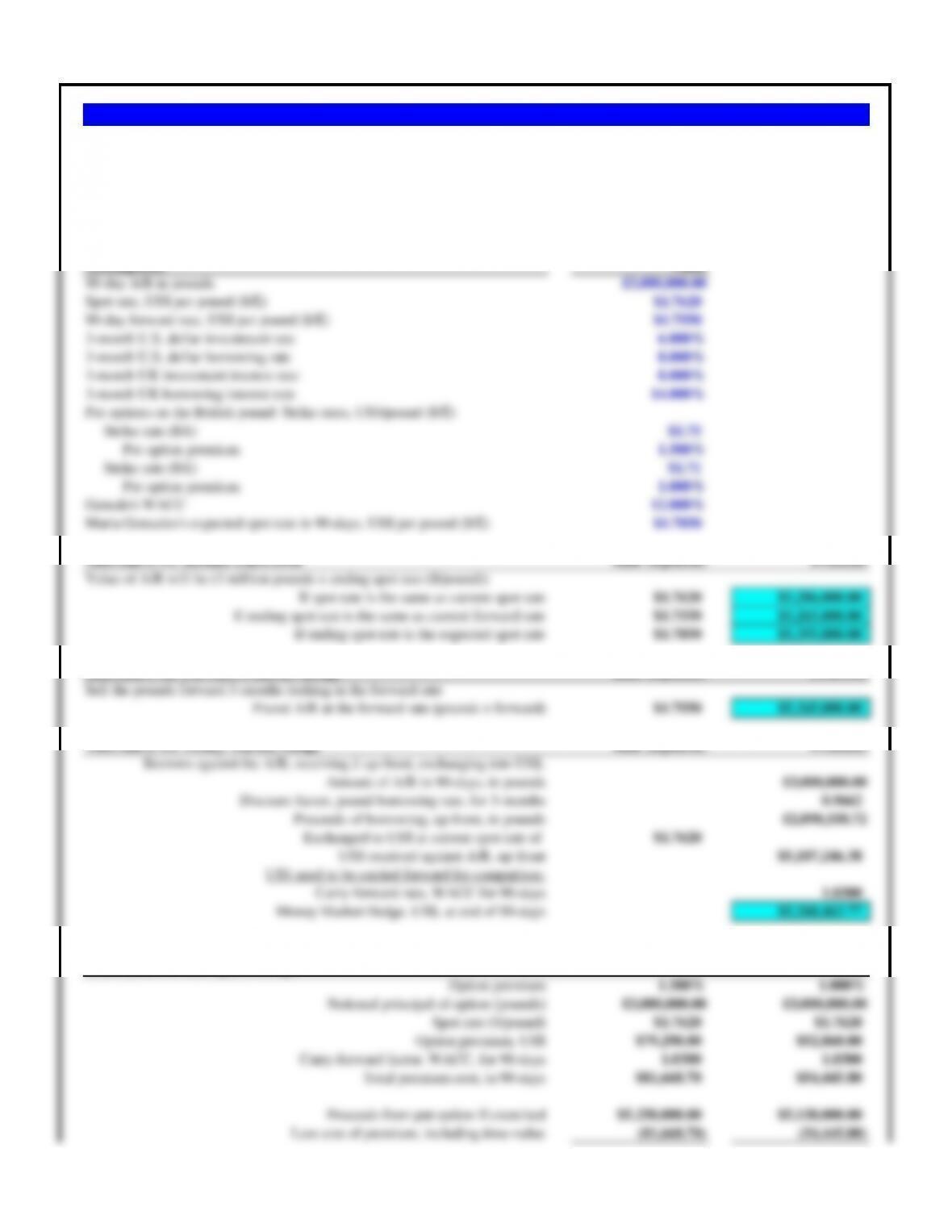

Assumptions Value

90-day A/R in pounds £3,000,000.00

Spot rate, US$ per pound ($/£)$1.7620

90-day forward rate, US$ per pound ($/£)$1.7550

3-month U.S. dollar investment rate 6.000%

3-month U.S. dollar borrowing rate 8.000%

Maria Gonzalez’s expected spot rate in 90-days, US$ per pound ($/£)$1.7850

Alternative #3: Money Market Hedge Rate ($/pound) Proceeds

Borrows against the A/R, receiving £ up-front, exchanging into US$.

Proceeds of borrowing, up-front, in pounds £2,898,550.72

Exchanged to US$ at current spot rate of $1.7620

Spot rate ($/pound) $1.7620 $1.7620

Option premium, US$ $79,290.00 $52,860.00

Carry-forward factor, WACC, for 90-days 1.0300 1.0300

Ganado — the same U.S.-based company as discussed in this chapter, has concluded a second larger sale of telecommunications

equipment to Regency (U.K.). Total payment of £3,000,000 is due in 90 days. Maria Gonzalez has also learned that Ganado will only

be able to borrow in the United Kingdom at 14% per annum (due to credit concerns of the British banks). Given the following

exchange rates and interest rates, what transaction exposure hedge is now in Ganado’s best interest?

Problem 10.15 Maria Gonzalez and Ganado

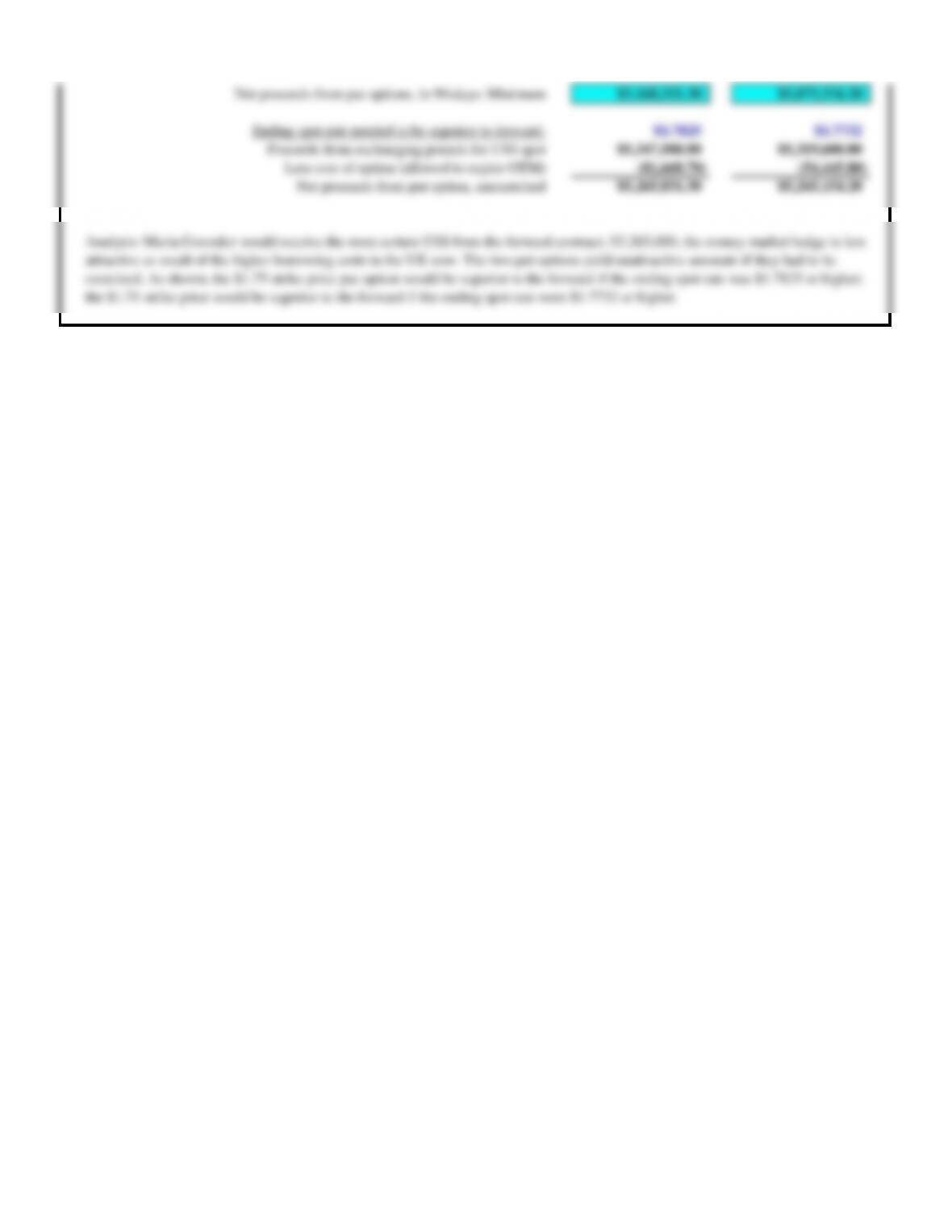

Net proceeds from put options, in 90-days: Minimum $5,168,331.30 $5,075,554.20

Ending spot rate needed to be superior to forward: $1.7825 $1.7732

Proceeds from exchanging pounds for US$ spot $5,347,500.00 $5,319,600.00

Less cost of option (allowed to expire OTM) (81,668.70) (54,445.80)

Net proceeds from put option, unexercised $5,265,831.30 $5,265,154.20

Analysis: Maria Gonzalez would receive the most certain US$ from the forward contract, $5,265,000; the money market hedge is less

attractive as result of the higher borrowing costs in the UK now. The two put options yield unattractive amounts if they had to be

exercised. As shown, the $1.75 strike price put option would be superior to the forward if the ending spot rate was $1.7825 or higher;

the $1.71 strike price would be superior to the forward if the ending spot rate were $1.7732 or higher.

2. Hedge in the money market. Larkin could borrow euros from the Frankfurt branch of its U.S. bank at 8.00% per annum.

Assumptions Values Today is May 1

90-day Forward rate, $/€$1.1060 Exchange Rate

180-day Forward rate, $/€$1.1130 Date ($/€)

US Treasury bill rate 3.600% April 1 $1.0800

Larkin’s borrowing rate, euros, per annum 8.000% May 1 $1.1000

Larkin’s cost of equity 12.000%

Options on euros Strike ($/euro) Call Option Put Option

August maturity options $1.1000 3.0% 2.0%

November maturity options $1.1000 2.6% 1.2%

Valuation of Alternative Hedges August Receivable November Receivable

Amount of receivable, in euros € 2,000,000 € 2,000,000

a. Hedge in the forward market

Amount of receivable, in euros € 2,000,000 € 2,000,000

Respective forward rates ($/€)$1.1060 $1.1130

US dollar proceeds as hedged ($) $2,212,000 $2,226,000

Carry forward to Nov 1st at WACC 1.03 —–

Current proceeds from discounting, euros € 1,960,784 € 1,923,077

Current spot rate ($/€)$1.1000 $1.1000

Carry forward for the period 1.06 1.06

Premium cost carried forward to Nov 1 ($46,640) ($27,984)

3. Hedge with foreign currency options. August put options were available at strike price of $1.1000/€ for a premium of 2.0% per contract, and

November put options were available at $1.1000/€ for a premium of 1.2%. August call options at $1.1000/€ could be purchased for a premium of

4. Do nothing. Larkin could wait until the sales proceeds were received in August and November, hope the recent strengthening of the euro would

continue, and sell the euros received for dollars in the spot market.

Problem 10.16 Larkin Hydraulics

1. Hedge in the forward market. The 3-month forward exchange quote was $1.1060/€ and the 6-month forward quote was $1.1130/€.

By the time the order was received and booked on May 1st, the euro had strengthened to $1.1000/€, so the sale was in fact worth €4,000,000 x

$1.1000/€ = $4,400,000. Larkin had already gained an extra $80,000 from favorable exchange rate movements. Nevertheless Larkin’s director of

finance now wondered if the firm should hedge against a reversal of the recent trend of the euro. Four approaches were possible:

On May 1st, Larkin Hydraulics, a wholly owned subsidiary of Caterpillar (U.S.), sold a 12 megawatt compression turbine to Rebecke-Terwilleger

Company of the Netherlands for €4,000,000, payable €2,000,000 on August 1st and €2,000,000 on November 1st. Larkin derived its price quote

of €4,000,000 on April 1st by dividing its normal U.S. dollar sales price of $4.320,000 by the then current spot rate of $1.0800/€.

Larkin estimates the cost of equity capital to be 12% per annum. As a small firm, Larkin Hydraulics is unable to raise funds with long-term debt.

U.S. T-bills yield 3.6% per annum. What should Larkin do?

Gross proceeds, Nov 1 $2,266,000 $2,200,000

Total net proceeds, after premium deduction, Nov 1

d. Do nothing (remain uncovered)

Amount of receivable, in euros € 2,000,000 € 2,000,000

Ending spot exchange rate ($/€)??? ???

The money market hedge provides the highest certain outcome. If Larkin Hydraulics believes the euro will strengthen versus the dollar over the

coming months, and it is willing to take the currency risk, the put option hedges could be considered.

$4,391,376

US Parent Company Sells Product to a Barcelona Subsidiary

Parameters Value

Sales price 500,000$

Spot rate, day 0 ($/€) 1.0640$

Spot rate, day 90 ($/€) 1.0980$

Forward rate, 90 days ($/€) 1.0615$

a) If the product was invoiced in US dollars, the US parent has no direct exposure, but the Spanish subsidiary in

Problem 10.17 Navarro’s Intra-Company Hedging

Navarro was a U.S.-based multinational company which manufactured and distributed specialty materials for sound-

proofing construction. It had recently established a new European subsidiary in Barcelona, Spain, and was now in the

process of establishing operating rules for transactions between the U.S. parent company and the Barcelona subsidiary.

Ignacio Lopez was International Treasurer for Navarro, and was leading the effort at establishing commercial policies for

the new subsidiary.

Navarro’s first shipment of product to Spain was up-coming. The first shipment would carry an intra-company invoice

amount of $500,000. The company was now trying to decide whether to invoice the Spanish subsidiary in U.S. dollars or

European euros, and in turn, whether the resulting transaction exposure should be hedged. Ignacio’s idea was to take a

recent historical period of exchange rate quotes and movements and simulate the invoicing and hedging alternatives

available to Navarro to try and characterize the choices.

Ignacio looked at the 90-day period which had ended the previous Friday (standard intra-company payment terms for

transcontinental transactions was 90 days). The quarter had opened with a spot rate of $1.0640/€, with the 90-day

forward rate quoted at $1.0615/€ the same day. The quarter had closed with a spot rate of $1.0980/€.

a. Which unit would have suffered the gain (loss) on currency exchange if intra-company sales were invoiced in U.S.

dollars ($), assuming both completely unhedged and fully hedged?

b. Which unit would have suffered the gain (loss) on currency exchange if intra-company sales were invoiced in euros

(€), assuming both completely unhedged and fully hedged?

Barcelona P&L: Forward hedge Rate ($/€) Entry

Receivable in USD 500,000.00$

A/R as invoiced in euros 1.0640 € 469,924.81

A/R as settled at forward rate 1.0615 498,825.19$

FX gain (loss)

(1,174.81)$

Uncovered Forward Cover Money Market Call Option

Payment (exposure) $30,000,000 $30,000,000 $30,000,000 $30,000,000

Effective ending rate (Won/$) 792 794 792 790

Current spot rate (Won/$) 800 800 800 800

Option premium (call) 2.900%

Eurodollar interest 6.000% 6.000%

US dollar interest borrow 9.375% 9.375%

Korean won interest 5.000% 5.000% 5.000% 5.000%

Bank Balance Uncovered Forward Cover Money Market Call Option

Beginning balance 25,000,000,000 25,000,000,000 25,000,000,000 25,000,000,000

Initial deductions 0 0 -23,645,320,197 -696,000,000

balance for interest 25,000,000,000 25,000,000,000 1,354,679,803 24,304,000,000

Interest earnings 312,500,000 312,500,000 16,933,498 303,800,000

Balance at day 89 25,312,500,000 25,312,500,000 1,371,613,300 24,607,800,000

Settlement of payment -23,760,000,000 -23,820,000,000 -23,700,000,000

Final Balance 1,552,500,000 1,492,500,000 1,371,613,300 907,800,000

If exercised.

How should KAL plan to make the payment to Boeing if KAL’s goal is to maximize the amount of won cash left in the bank at the end of the three month

period? Make a recommendation and defend it.

Problem 10.18 Korean Airlines

Korean Airlines (KAL) has just signed a contract with Boeing to purchase two new 747-400’s for a total of $60,000,000, with payment in two equal

tranches. The first tranche of $30,000,000 has just been paid. The next $30,000,000 is due three months from today. KAL currently has excess cash of

25,000,000,000 won in a Seoul bank, and it is from these funds that KAL plans to make its next payment.

The current spot rate is won 800/$, and permission has been obtained for a forward rate (90 days), won 794/$. The 90 day Eurodollar interest rate is

6.000%, while the 90 day Korean won deposit rate (there is no Euro-won rate) is 5.000%. KAL can borrow in Korea at 6.250%, and can probably borrow

in the U.S. dollar market at 9.375%.

A three month call option on dollars in the over-the-counter market, for a strike price of won 790/$ sells at a premium of 2.9%, payable at the time the

option is purchased. A 90 day put option on dollars, also at a strike price of won 790/$, sells at a premium of 1.9% (assuming a 12% volatility). KAL’s

foreign exchange advisory service forecasts the spot rate in three months to be won792/$.

Eurodollar deposit rate

6.000%

US dollars for Payable

29,556,650$ ↔ ↔ 1.0150 ↔ ↔ 30,000,000$

↓

↓

↓

↓

↓

Spot (Won/$) —————> 90 days —————->

800.00

↓

↓

↓

23,645,320,197 Amount to be withdrawn from Korean bank balance

Korean bank balance

25,000,000,000

Korean Airlines Money Market Hedge

The challenge with the Korean Money Market Hedge is that it is a payable — a payable form a Korean won cash balance. A

MM Hedge for a payable is to simply transfer money into the target currency at the start of the period (the front end of the

box), and then to have that money earn interest on deposit for the time period until payment is due.

In this problem, that means transfering enough Korean won at the start to fund a dollar deposit which will yield a total of

$30 million at the end of 90 days. The dollar deposit earns a deposit rate (not a borrowing rate). The won transferred out

of the account at the beginning of the period then reduces the account balance, which then earns the Korean interest rate

for the 90 days to get to an ending cash balance.