W H AT I S E C O N O M I C S ? 7 7

A n s w e r s t o t h e R e v i e w Q u i z z e s

Page 472

1. What is the distinction between expected wealth and expected utility?

Expected wealth is the money value of what a person expects to own at a point in

time. Expected utility is the utility value of what a person expects to own at a point

2. How does the concept of utility of wealth capture the idea that pain of loss

exceeds the pleasure of gain?

The utility of wealth has diminishing marginal utility. Diminishing marginal utility

3. What do people try to achieve when they make a decision under uncertainty?

4. How is the cost of risk calculated when making a decision with an uncertain

outcome?

A decision made with uncertainty has an expected wealth and an expected utility

that depend on the probability, wealth, and utility associated with the di%erent

outcomes. Because people are risk averse, the amount of certain wealth that

Page 475

1. How does insurance reduce risk?

Insurance reduces the risk any individual faces because insurance pools risks.

Everyone pays into the pool but only the small fraction of people who su%er a loss

2. How do we determine the value (willingness to pay) for insurance?

2

0

UNCERTAINTY

AND

INFORMATION

77

7 8

The amount that someone would be willing to pay to avoid risk is measured using

Suppose a person faces the risky situation of receiving wealth of

W

1

(with utility

of

U1

) or a smaller amount,

W2

(with utility of

U2

). The expected wealth from

this situation is EW, and the expected utility is EU. This risky situation has the

3. How can an insurance company o%er people a deal worth taking? Why do

both the buyers and the sellers of insurance gain?

Insurance companies work by pooling risks so that everyone pays into the pool but

only the (small) fraction of people who su%er a loss are paid from the pool.

Although the likelihood of a bad occurrence is small for each individual, for a large

4. What kinds of risks can’t be insured?

Insurance works because the risks of adverse outcomes are independent, that is,

Page 480

1. How does private information create adverse selection and moral hazard?

Both moral hazard and adverse selection are the result of private information.

Moral hazard occurs when, after an agreement has been reached, one of the

parties to the agreement has the incentive to gain additional bene0ts at the

2. How do markets for cars use warranties to cope with private information?

78

W H A T I S E C O N O M I C S ? 7 9

Warranties serve to limit the adverse selection and moral hazard problems in the

market for cars. Essentially, warranties (and guarantees in general) are signals

3. How do markets for loans use signaling and screening to cope with private

information?

Lenders in the loans market want to separate high-risk borrowers from low-risk

borrowers so that they can charge high-risk borrowers a high interest rate and

low-risk borrowers a low interest rate. They use signals and screens to help them

4. How do markets for insurance use no-claim bonuses to cope with private

information?

“No-claim” bonuses are commonly used in auto insurance. One of the most

important pieces of information a person can give an auto insurance company is

his or her propensity to drive safely and avoid accidents. However, this information

is only believable to the extent that driving records really do di%erentiate good

Page 481

1. Thinking about information as a good, what determines the information

people are willing to pay for?

People are willing to pay for information so long as the marginal cost is less than or

equal to its marginal bene0t. For instance, consumers are willing to purchase

information that has a marginal bene0t to them that exceeds the price they must

2. Why is it ine>cient to be overinformed?

Information is costly to obtain. If the marginal cost of obtaining the information

3. Why are some of the markets that provide information likely to be dominated

by monopolies?

79

8 0

Objective information about, say, the quality of a good or service or the risk

80

A n s w e r s t o t h e S t u d y P l a n P r o b l e m s a n d

A p p l i c a t i o n s

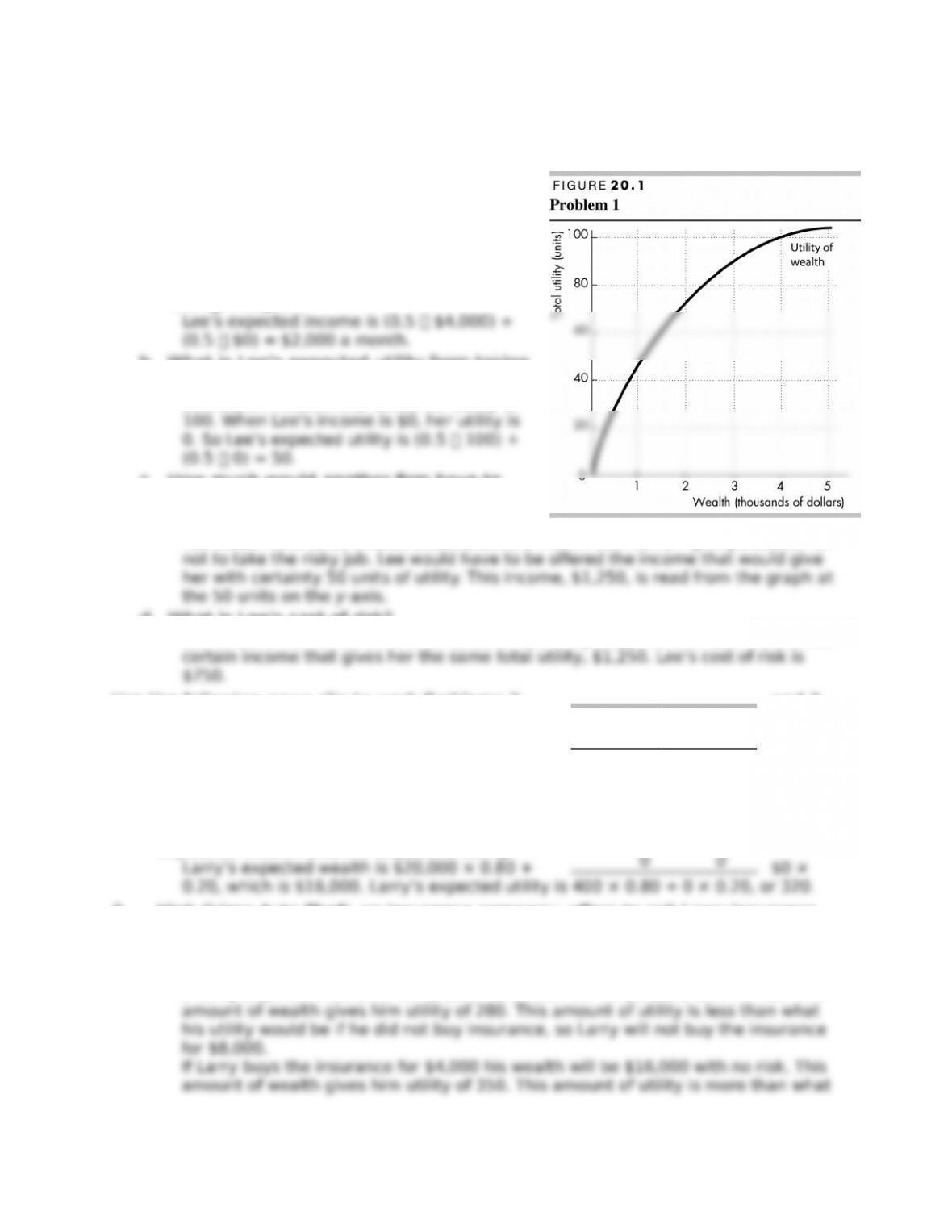

1. The 0gure shows Lee’s utility of wealth

curve. Lee is o%ered a job as a salesperson

in which there is a 50 percent chance that

she will make $4,000 a month and a 50

percent chance that she will make nothing.

a. What is Lee’s expected income from

taking this job?

b. What is Lee’s expected utility from taking

this job?

When Lee’s income is $4,000, her utility is

c. How much would another 0rm have to

o%er Lee with certainty to persuade her

not to take the risky sales job?

Lee would have to be o%ered about $1,250 a month with certainty to persuade her

d. What is Lee’s cost of risk?

Lee’s cost of risk is the di%erence between Lee’s expected income, $2,000, and the

Use the following news clip to work Problems 2 and 3.

Larry lives in a neighborhood in which 20 percent of the

cars are stolen every year. Larry’s car, which he parks

on the street overnight, is worth $20,000. (This is Larry’s

only wealth.) The table shows Larry’s utility of wealth

schedule.

2. If Larry cannot buy auto theft insurance, what is his

expected wealth and his expected utility?

3. High-Crime Auto Theft, an insurance company, o%ers to sell Larry insurance

at $8,000 a year and promises to provide Larry with a replacement car worth

$20,000 if his car is stolen. Is Larry willing to buy this insurance? If not, is he

willing to pay $4,000 a year for such insurance?

If Larry buys the insurance for $8,000 his wealth will be $12,000 with no risk. This

Wealth

(dollars)

Utility

(units)

20,000 400

16,000 350

12,000 280

8,000 200

4,000 110

0 0

4. Suppose that there are three national soccer leagues: Time League, Goal

Di%erence League, and Bonus for Win League. The leagues are of equal

quality, but the players are paid di%erently. Players in the Time League are

paid by the hour for time spent practicing and playing. Players in the Goal

Di%erence league are paid an amount that depends on the goals scored by

the team minus the goals scored against it. Players in the Bonus for Win

League are paid one wage for a loss, a higher wage for a tie, and the highest

wage of all for a win.

a. Describe the predicted di%erences in the quality of the games played by

each of the leagues.

In the Time League, players have no incentive to play hard or to win the game. In

this league the games are likely to be dull, drawn out, low quality a%airs with

players not playing particularly hard. In the Goal Di%erence League, the players

b. Which league is the most attractive to players?

c. Which league will generate the largest pro0ts?

If fans like action packed games and if the average salary is the same in all

5. You can’t buy insurance against the risk of being sold a lemon. Why isn’t

there such a market? How does the market provide a buyer with some

protection against being sold a lemon? What are the main ways in which

markets overcome the lemons problem?

There is not a market for “lemon insurance” for several reasons. De0ning a

“lemon” is far from clear cut. The de0nition would need to be speci0ed in the

contract. But that leads to a moral hazard problem because a buyer with a car

Even without insurance, the market does give protection against lemons.

Warranties are designed to help cope with the moral hazard and adverse selection

© 2016 Pearson Education, Inc.

8C H A P T E R 2 0

6. Show Us Our Money

I have no clue what my colleagues make and I consider my salary my own business. It

Source: Time, May 12, 2008

Explain why a worker might be willing to pay for the salary information of

other workers.

A worker could demand a higher salary by comparing his or her pay with that of a

Answers to Additional Problems and Applications

Use the table, which shows Jimmy’s and Zenda’s

utility of wealth schedules, to work Problems 7

to 9.

8. a. Calculate Jimmy’s and

Zenda’s marginal utility of

wealth schedules.

The table to the right sets

b. Who is more risk averse,

Jimmy or Zenda? How do

© 2016 Pearson Education, Inc.

Wealth

Jimmy’s

utility

Zenda’s

utility

Wealth

Jimmy’s

utility

Jimmy’s

margin

al utility

Zenda

’s

utility

Zenda

’s

margi

nal

0 0 0

2.00 5.12

U N C E RTA I N T Y A N D I N F O R M AT I O N 9

9. Suppose that Jimmy and Zenda each have $400 and are o%ered a business

investment opportunity that involves committing the entire $400 to the

project. The project could return $600 (a pro0t of $200) with a probability of

0.85 or $200 (a loss of $200) with a probability of 0.15. Who goes for the

project and who hangs on to the initial $400?

Jimmy puts his money into the project, but Zenda does not. Jimmy maximizes his

expected utility. If Jimmy puts his money into the project and it makes a pro0t, his

utility is 393; if Jimmy puts his money into the project and it fails, his utility is 300.

So Jimmy’s expected utility from the project is (0.85 393) + (0.15 300), which

© 2016 Pearson Education, Inc.

1 0 C H A P T E R 2 0

Use the following information to work Problems 10 to 12.

Two students, Jim and Kim, are o%ered summer jobs managing a student

house-painting business.

There is a 50 percent chance that either of them

will be successful and end up with $21,000 of

wealth to get them through the next school

10. Does anyone take the painting job? If so,

who takes it and why? Does anyone take the job picking fruit? If so, who takes

it and why?

Jim will take the painting job. If Jim takes the job managing the house painters, his

Kim will take the fruit-picking job. If Kim takes the job managing the house

11. In Problem 10, what is each student’s maximized expected utility? Who has

the larger expected wealth? Who ends up with the larger wealth at the end of

the summer?

Jim’s expected utility is 380; Kim’s expected utility is 475. Jim has higher expected

12. In Problem 10, if one of the students takes the risky job, how much more

would the fruit-picking job have needed to pay to attract that student?

Jim takes the risky job. His expected utility with the risky job is 380. The fruit

Use the table, which shows Chris’s utility of wealth

schedule, to work Problems 13 and 14.

Chris’s wealth is $5,000 and it consists entirely of her share

© 2016 Pearson Education, Inc.

Wealth Jim’s

utility

Kim’s

utility

Wealth

(dollars)

Utility

(units)

U N C E RTA I N T Y A N D I N F O R M AT I O N 1 1

13. If Chris cannot buy cold-summer insurance, what is her expected wealth and

what is her expected utility?

14. Business Loss Recovery, an insurance company, is willing to sell Chris cold-summer

If Chris buys the insurance for $3,000 her wealth will be $2,000 with no risk. This

amount of wealth gives her utility of 90, which is more than what her utility would

Use the following information to work Problems 15 to 17.

Larry has a good car that he wants to sell; Harry has a lemon that he wants to sell.

Each knows what type of car he is selling. You are looking at used cars and plan to

buy one.

15. If both Larry and Harry are o%ering their cars for sale at the same price, from

whom would you most want to buy, Larry or Harry, and why?

If you know that Larry’s car is a good car and Harry’s car is a lemon, you most

16. If you made an o%er of the same price to Larry and Harry, who would sell to

you and why? Describe the adverse selection problem that arises if you o%er

the same price to Larry and Harry.

The price o%ered will be the price for which a lemon sells. Harry, who has a lemon,

will be willing to sell at that price; Larry, who has a good car, will not be willing to

17. How can Larry signal that he is selling a good car so that you are willing to

pay Larry the price that he knows his car is worth, and a higher price than

what you are willing to o%er Harry?

18. Pam is a safe driver and Fran is a reckless driver. Each knows what type of

driver she is, but no one else knows. What might an automobile insurance

company do to get Pam to signal that she is a safe driver so that it can o%er

her insurance at a lower premium than it o%ers to Fran?

One possibility is to o%er insurance with a higher deductible at a lower cost. Pam

knows that she is less likely to need the insurance, so she is willing to accept the

© 2016 Pearson Education, Inc.

1 2 C H A P T E R 2 0

19. Why do you think it is not possible to buy insurance against having to put up

with a low-paying, miserable job? Explain why a market in insurance of this

type would be valuable to workers but unpro0table for an insurance provider

and so would not work.

Insurance against a low-paying job is not available because of moral hazard and

adverse selection. In particular, the moral hazard exists that once someone

purchased this type of insurance, the person could then take a low-paying job that

Use the following news clip to work Problems 20 and 21.

Why We Worry About the Things We Shouldn’t … and Ignore the Things

We Should

We pride ourselves on being the only species that understands the concept of risk,

yet we have a confounding habit of worrying about mere possibilities while

ignoring probabilities, building barricades against perceived dangers while leaving

ourselves exposed to real ones: 20% of all adults still smoke; nearly 20% of drivers

and more than 30% of backseat passengers don’t use seat belts; two thirds of us

are overweight or obese. We dash across the street against the light and build our

homes in hurricane-prone areas—and when they’re demolished by a storm, we

rebuild in the same spot.

Source: Time, December 4, 2006

20. Explain how “worrying about mere possibilities while ignoring probabilities”

can result in people making decisions that not only fail to satisfy social

interest, but also fail to satisfy self-interest.

By “worrying about mere possibilities while ignoring probabilities,” society

sometimes devotes its scarce resources in ways that do not make people as well

o% as possible. In particular resources devoted to preventing mad cow pathogen

21. How can information be used to improve people’s decision making?

Information can improve people’s decision making by providing them with data

about the potential outcomes of their decisions. With this information readily at

Economics in the News

22. After you have studied Economics in the News on pp. 482–483, answer the

following questions.

a. What information do accurate grades provide that grade inUation hides?

Accurate grades provide valuable information about the student’s productivity and

the extent of the student’s skill base. High grades would be correlated with high

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 1 3

b. If grade inUation became widespread in high schools, colleges, and

universities, what new arrangements do you predict would emerge to

provide better information about student ability?

If grade inUation becomes too severe, a student’s class ranking, for instance, 23rd

c. Do you think grade inUation is in anyone’s self-interest? Explain who bene0ts

and how they bene0t from grade inUation.

The people who bene0t from grade inUation are the students who 0rst received

d. How do you think grade inUation might be controlled?

23. Are You Paid What You’re Worth?

How do you know if your pay adequately reUects your contributions to your

employer’s pro0ts? In many instances, you don’t. Your employer has more and

better information than you do about how your salary and bonus compare to

others in your 0eld, to others in your o>ce, and relative to the company’s

pro0ts in any given year. You can narrow the information gap a bit if you’re

willing to buy salary reports from compensation sources. For example, at

$200, a quick-call salary report from Economic Research Institute will o%er

you compensation data for your position based on your years of experience,

your industry and the place where your company is located.

Source: CNN, April 3, 2006

a. Explain the role that asymmetric information can play in worker wages.

Asymmetric information can lead to adverse selection and moral hazard, which

both play a role in determining workers’ wages. For instance, adverse selection

occurs if a 0rm o%ers to pay its salespeople a 0xed wage. The 0rm will attract

b. What adverse selection problem exists if a 0rm o%ers lower wages to

existing workers?

If a 0rm o%ers lower wages to its existing workers, the most productive workers will

c. What will determine how much a worker should actually pay for a detailed

salary report?

The bene0ts the worker expects to receive from the salary report will determine

how much he or she is willing to pay. For instance, if a worker believes that his or

© 2016 Pearson Education, Inc.

1 4 C H A P T E R 2 0

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 1 5