W H AT I S E C O N O M I C S ? 2 2 1

T h e B i g P i c t u r e

Where we have been:

Chapter 20 uses the general economic reasoning featured in many of the

previous chapters. For instance, Chapter 20 uses the concepts of marginal

utility &rst covered in Chapter 8. It concludes with a general discussion of

e)ciency in information markets, which draws upon material &rst covered in

Chapter 2 and expanded upon in Chapter 5.

Where we are going:

Chapter 20 is the &nal chapter in the microeconomics section. This chapter is

important because it relaxes many of the implicit assumptions concerning

information that bother students about the e)ciency of the market. Chapter

20 provides some interesting, real-life examples of market processes in an

uncertain world.

N e w i n t h e Tw e l f t h E d i t i o n

The chapter has been lightly revised to help enhance students’ understanding. An

application on sub-prime loans is incorporated. A new Worked Problem section has

been added. The Worked Problem shows how to calculate expected wealth and

utility. It also demonstrates how to compare a risky choice to a no-risk opportunity

and how to calculate the cost of risk. To include the new Worked Problem without

lengthening the chapter, some problems have been removed from the Study Plan

Problem and Applications. These problems are in the MyEconLab and are called

Extra Problems.

20

UNCERTAINTY

AND

INFORMATION

C h a p t e r

221

L e c t u r e N o t e s

Uncertainty and Information

People need to make decisions in the face of uncertainty and risk.

Markets allow people to buy and sell risk.

Some people may have private information.

Markets must cope with incomplete information, which can lead to moral hazard and

adverse selection.

I. Decisions in the Face of Uncertainty

Expected wealth

Expected wealth is the money value of what a person expects to own at a given

point in time.

An expectation is an average calculated by using a formula that weights each

possible outcome with a probability (chance) that it will occur.

Risk aversion

Risk aversion is the dislike of risk. Most people are risk averse.

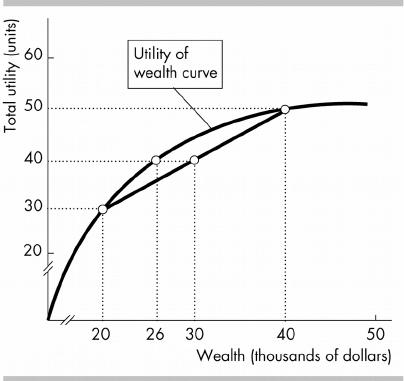

Utility of Wealth

Wealth yields utility, but the marginal

utility of wealth diminishes as wealth

increases, as shown in the &gure. Because

the slope of the utility of wealth curve

diminishes as wealth increases, the utility

gained from a $1 increase in wealth is less

than the utility lost from a $1 decrease in

wealth.

Expected utility

This is the utility value of what a person

expects to own at a given point in time. It is

calculated by using a formula that weights

each possible outcome with the probability

that it will occur.

In the &gure, suppose a person is faced

with two investments: One o;ers wealth

of $26,000 with no uncertainty and so has utility of 40 units with no uncertainty.

The other option has, with a 0.50 probability, wealth equal to $40,000 and utility

of 50 units; or, with another 0.50 probability, it has wealth of $20,000 and utility

of 30 units. Expected utility from this second option is 0.50 50 units + 0.50 30

units = 40 units. If given the choice between $26,000 with certainty and a 50:50

chance of having $40,000 or $20,000, the person is indi;erent between the two

choices because both have the same (expected) utility, 40 units.

The expected wealth from the second option is 0.50 $40,000 + 0.50 $20,000

= $30,000, which is $4,000 more than the certain wealth of $26,000 from the

&rst option. The $4,000 di;erence is called the cost of risk.

Making a Choice with Uncertainty

Faced with uncertainty, people choose the option with the highest expected utility.

By comparing the expected utility from a risky prospect with the expected utility

from a safe prospect, you can choose the one that maximizes expected utility.

II. Buying and Selling Risk

Both buyers and sellers gain from exchanging risk as they would any product. What they

are trading is avoiding risk. A buyer of risk avoidance is transferring the risk to the seller.

The seller is willing to assume the risk because the costs of risk are lower to the seller than

what the buyer is willing to pay.

Insurance Markets

How insurance reduces risk: People pool and share risk. When people buy insurance

against the risk of an unwanted event, they pay an insurance company a premium.

If the unwanted event occurs, the insurance company pays out the amount to the

insured.

Why people buy insurance: People buy insurance because they are risk averse. If

premiums are not too high, loss of utility from paying the premium for the insurance

is less than the expected utility loss if the adverse event were to occur.

How insurance companies earn a pro&t:

Everyone pays into the insurance pool, but only the small fraction of people who

actually su;er a loss are paid from these funds.

Although the probability of any particular individual su;ering a loss is quite

small, for a large number of people the total number and the total amount of

losses can be estimated very accurately.

Insurance companies earn a pro&t because the insurance company can collect a

premium that is high enough to at least break even, and customers who are risk

averse are willing to pay that premium.

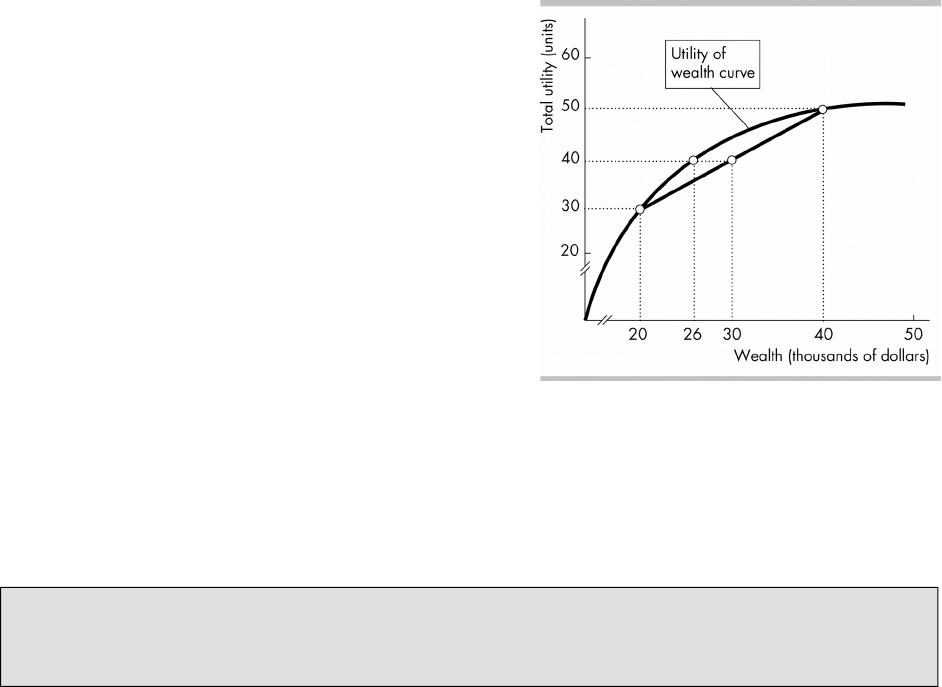

A Graphical Analysis of Insurance

Risk Taking Without Insurance: In the

&gure, suppose the person has a 50

percent chance of keeping $40,000 of

wealth and a 50 percent chance of having

$20,000 of wealth. As seen before, the

expected wealth is $30,000 and the

expected utility is 40. The &gure shows

that the person is willing to accept a lower

wealth with certainty, $26,000, which will

give the same utility, 40, as the risky case.

The Value and Cost of Insurance: The key

point is that the certain wealth with utility

of 40 ($26,000) is less than the expected

wealth with utility of 40 ($30,000). As long

as the person can buy insurance for less

than $14,000, the individual is better o;

(has higher expected utility) from the

purchase of insurance than from the uncertainty of wealth with no insurance.

Ignoring any operating costs, if there are many people in the same situation the

insurance will cost the insurance company $10,000 per person, the expected loss

per person. As long as the company can sell the insurance for more than $10,000,

the insurance company is better o; by selling the insurance.

Gains from Trade: Both the insurance company and the person will be better o; if

insurance can be bought and sold for between $14,000 and $10,000.

Why are men (especially young men) charged more for auto insurance? Have the

students consider the di)culty of providing insurance with a;ordable premiums to

consumers, yet be pro&table enough to encourage producers to accept the risks involved.

For example, car insurance companies charge higher premiums to unmarried young men

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 1 9 9

than they charge unmarried young women, even if two such individuals have the same

driving records. This di;erence is based on statistical probabilities calculated by the

insurance company keeping record of large samples of loss claims. Ask the students if this

di;erence is “fair?” Then ask how a drivers’ risk-taking behavior might change once he or

she is insured. This last question is a good introduction to the following material on private

information and moral hazard.

Risk That Can’t Be Insured

If risks are not independent, they cannot be insured (e.g., private markets will not

insure homeowners in a Kood plain because the occurrence of a Kood negatively

a;ects everyone in that area).

Risks must be observable to both the buyer and the seller in order to be insurable.

Economics in Action considers insurance in the United States, both private and public such

as Medicare, Social Security, and unemployment insurance.

III. Private Information

Asymmetric Information: Examples and Problems

Private information is information about the value of the item being traded that is

possessed by only buyers or sellers. A market in which buyers or sellers have private

information has asymmetric information.

Asymmetric information creates two problems:

Adverse selection is the tendency for people to enter into agreements in which

they can use their private information to their own advantage and to the

disadvantage of the less informed party.

Moral hazard is the tendency for people with private information, after entering

into an agreement, to use that information for their own bene&t and at the cost of

the less-informed party.

The Market for Used Cars

The owner of a used car has private information about the quality of the car. If the

buyer cannot determine the quality of the car before the purchase, moral hazard

occurs when the seller claims that each car is high quality but in truth o;ers

“lemons” for sale.

Because consumers are unable to distinguish between a “lemon” and a good

vehicle, they must assume that all used vehicles for sale are “lemons,” and used car

dealers must price their cars at the highest price that consumers will pay for a

“lemon.”

The problem that in markets in which it is not possible to distinguish reliable

products from lemons, there are too many lemons and too few reliable products

traded is called the lemons problem.

However, used car dealers can overcome the lemon problem by o;ering a warranty

on the vehicle, which is a signal that the car is of high quality. Signaling occurs

when an informed person takes actions that send information to uninformed

persons.

An equilibrium in a market when only one message is available and an

uninformed person cannot determine quality (as with the market for lemons) is

called a pooling equilibrium.

An equilibrium when signaling provides full information to a previously

uninformed person (as in the used car market with warranties) is called a

separating equilibrium.

© 2016 Pearson Education, Inc.

200 C H A P T E R 2 0

The Market for Loans

Some borrowers are low risk, and will likely repay their loans, and others are high

risk, and will likely default on their loans. The risk that a borrower might not repay a

loan is called credit risk or default risk. Banks want to charge low-risk borrowers

a low interest rate and high-risk borrowers a high interest rate, but banks cannot

immediately distinguish between the two classes of borrowers.

If banks cannot charge di;erent interest rates to di;erent individuals with varying

default risks, the result is an ine)cient pooling equilibrium.

Banks use signals, such as length of time on the job, marital status, age, and

other factors correlated with low-risk borrowers to try to determine the risk of

loaning funds to each individual borrower. Borrowers may have an incentive to

mislead lenders, so banks often require that borrowers provide relevant

information about the likelihood the loan will be repaid (salary, wealth, tenure on

the job, for example). Inducing an informed party to reveal private information is

called screening.

An Economics in Action examines the sub-prime credit crisis. Prior to the crisis the supply

of funds to the sub-prime market was much greater than during the crisis.

The Market for Insurance

Moral hazard occurs when insured people have less incentive to be careful and avoid

risky behavior. And adverse selection arises because people who create greater risks

are more likely to buy insurance.

Insurance companies seek out signals (such as an auto insurer looking at an

individual’s driving record) to limit the extent of the adverse selection problem.

Deductibles, where the insured person also must pay part of the expense of an

incident, can reduce the moral hazard problem.

Moral hazard in game shows. The television show, “Who Wants to Be a Millionaire?”

was insured by an insurance company that reimbursed the producers of the show when a

contestant answered all the questions correctly and won a big dollar pay-out. This insurer

had some serious disagreements with the show’s producers after the show ran on national

television for the &rst year, claiming concerns over moral hazard. In particular, the insurer

claimed that the producer eased the questions asked of the contestants in order to

guarantee that some contestants won and thereby boosted the show’s excitement and

ratings. The insurer wanted greater control over the di)culty of the questions being asked

of the contestants.

IV. Uncertainty, Information and the Invisible Hand

Information as a Good

Obtaining more information has increasing opportunity costs and consuming more

information has decreasing marginal bene&ts.

The e)cient amount of information is the amount at which the marginal bene&t from

information equals the marginal cost. It is hard to determine whether a competitive

market for information would produce it at the e)cient level.

Monopoly in Markets that Cope with Uncertainty

Large economies of scale probably exist is providing services to reduce uncertainty

and to provide better information. Therefore insurance markets are highly

concentrated.

Monopoly leads to ine)cient results, even in the absence of uncertainty, so

underproduction of information is thus likely.

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 2 0 1

Economics in the News considers the case of grade inKation. Grade inKation makes it

more di)cult for employers to determine who is outstanding and who is not.

© 2016 Pearson Education, Inc.

2 0 2 C H A P T E R 2 0

A d d i t i o n a l P r o b l e m

1. How might adverse selection discourage &rms from underpaying their

workers?

2. How might moral hazard discourage &rms from o;ering workers a &xed

wage?

3. Baseball players often seek contracts with a “no-trade” clause so that the

player cannot be traded from his current team without his permission.

a. Provide an example of private information that a baseball player who wants

a no-trade clause possesses.

b. Does a baseball player with a no-trade clause present a moral hazard to his

baseball team?

c. Does a baseball player with a no-trade clause present adverse selection

problems to his baseball team?

4. How does health insurance and Kood insurance result in both a moral hazard

and adverse selection problem?

5. How do insurance companies use premiums and deductibles in an attempt to

resolve these problems?

S o l u t i o n s t o A d d i t i o n a l P r o b l e m s

1. If a &rm gets the reputation for underpaying its workers, only low quality workers will

apply to work at the &rm, thereby presenting the &rm with a severe adverse selection

problem.

2. If &rms o;er workers a &xed wage regardless of their e;ort workers have the incentive

to shirk, that is, to work less hard than otherwise.

3. a. A player could know that he was injured or that he had not healed as well as

possible from an injury.

b. A player with a no-trade clause presents a moral hazard problem. The player can

claim to be more badly injured than is truly the case to avoid playing some games.

The player can make this claim knowing that even if he often does so, his team

cannot trade him and must continue to pay his salary.

c. If there are two types of contracts—contracts with the no-trade clause and contracts

without it—then there is a potential adverse selection problem. Players who know

they are more inclined to want to skip a game or two will be eager to sign a no-trade

contract because this contract lessens their cost of feigning injury to take leisure.

4. Health and Kood insurance both present moral hazard and adverse selection

problems. Adverse selection is present because less healthy people will be more likely

to buy health insurance and people living in Kood prone areas will be more likely to

buy Kood insurance. Moral hazard is present because people with health insurance

become more prone to take risks and people with Kood insurance become less prone

to build Kood resistant structures.

5. Insurance companies use premiums and deductibles in an e;ort to create a

separating equilibrium. The companies o;er policies with high deductibles and low

premiums to attract low-risk customers, that is people who are not likely to be

susceptible to diseases or people who have not built in a Kood plain. Simultaneously

the companies also o;er policies with high premiums and low deductibles to appeal to

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 2 0 3

high-risk customers, that is people who are prone to contracting certain ailments or

who have built in a Kood plain.

A d d i t i o n a l D i s c u s s i o n Q u e s t i o n s

11. What does being risk averse mean? Get the students to consider why a

risk premium must be paid to overcome the consumer’s cost of risk.

12. Why do people prefer the utility arising from a level of income known

with certainty more than the utility arising from the same value of

expected income arising from a risky choice? Get the students to

understand that the consumer will never achieve the expected level of income

arising from a risky decision when confronted with a single choice. Expected

income is the value of income that is averaged over numerous outcomes

under the same circumstances. For any one point in time, knowing utility from

a given outcome is preferred to the expected utility of a risky outcome, despite

the two having the same expected level of income.

13. Would insurance companies prefer a higher or lower degree of risk

aversion among consumers? Point out to students that the more concave

the utility of wealth schedule, the higher the cost of risk, and the greater the

risk premium that the consumer is willing to pay to avoid risk.

14. Why will private insurance companies sell health insurance that pays

for unexpected illness but not unemployment insurance that pays for

unexpected unemployment? Explain that adverse selection motivates high

risk workers who know they are likely to be laid o; will be willing to pay a high

risk premium for unemployment insurance, but low risk workers who know

they are unlikely to be laid o; will only pay a low risk premium. By o;ering

insurance premiums that are desirable to the low risk workers, high risk

workers will buy the insurance as well, preventing the insurance companies

from knowing which workers are high risk and which are low risk. This burden

on insurance carriers is not as evident in o;ering health insurance because

the insurers can seek out signals from consumers which reveal who has

low-risk lifestyle and who have a high-risk lifestyle (such as determining

whether the potential health insurance customer is a smoker, or is older, or is

overweight, etc.)

15. What are some examples of goods that require “information” for

consumers to enjoy and goods that require “private information”? All

goods require consumers to have access to price and availability information.

However, private information relates to goods that consumers cannot

completely understand until they commit to purchasing the good. Goods in

this category include used cars, long-wearing and comfortable shoes, high-end

consumer electronics, good homes in pleasant neighborhoods, etc. Markets for

these goods typically create opportunities for middlemen (like realtors,

retailers and car dealers) to supply advice and match consumer tastes with

producer goods.

16. Is the use of signals to discern between high and low risk consumers

“fair”? Ask the students whether charging 17-year-old, unmarried males

higher auto insurance premiums than 35-year–old, unmarried females “fair”?

Is it “fair” for individuals with pre-existing health conditions to pay higher

insurance bills? Is it “fair” for employers to pay women less because women

are (obviously) more likely to give birth? On the other hand, is the use of

signals “e)cient”? Get the students to consider the tradeo; between pooling

© 2016 Pearson Education, Inc.

2 0 4 C H A P T E R 2 0

risk (making avoiding risk a;ordable) and avoiding moral hazard (making

careful, thoughtful consumers pay for the mistakes of careless, thoughtless

consumers).

7. Health care reform uses “pools” of individuals to help to reduce

health care costs for those currently without insurance. How is this

intended to help and why was it designed so people could not “opt

out” of having insurance? The larger the pool, the more risk is spread out. If

younger, healthier workers less likely to have claims can avoid participation,

the expected outlays for the insurance company are spread across a smaller

pool, risk rises for the insurance company, and customers have to pay higher

premiums.

© 2016 Pearson Education, Inc.

U N C E RTA I N T Y A N D I N F O R M AT I O N 2 0 5