W H AT I S E C O N O M I C S ? 1 9 7

T h e B i g P i c t u r e

Where we have been:

Chapter 18 uses the productivity and cost denitions and concepts introduced

in Chapter 10 and the conditions for maximum prot introduced in Chapter 11.

It builds on these concepts to explain value of marginal product and to show

how factor markets work.

Where we are going:

Chapter 18 explores the workings of factor markets and the resulting

distribution of income. The labor, capital, and natural resource markets are

introduced here and Chapter 19 studies the implications of factor market

equilibrium for the distribution of income and trends in the distribution.

N e w i n t h e Tw e l f t h E d i t i o n

The material in the chapter is largely unchanged from the previous edition. The

focus remains on the job market and the case studies and applications have been

updated. A new Worked Problem section has been added. The Worked Problem

shows the students how to calculate the marginal product of labor and the value

of marginal product. It then demonstrates how to use the results to maximize

prot and how the prot-maximizing quantity of labor changes when the age rate

changes. To include the new Worked Problem without lengthening the chapter,

some problems have been removed from the Study Plan Problem and

Applications. These problems are in the MyEconLab and are called Extra Problems.

18MARKETS FOR

FACTORS OF

PRODUCTION

C h a p t e r

197

L e c t u r e N o t e s

Markets for Factors of Production

Firms choose the quantities of factors they demand in order to maximize their prot.

Households choose the quantities of factors they supply.

The interaction of demand and supply determines factor prices.

I. The Anatomy of Factor Markets

The four factors of production are labor, capital, land (natural resources), and

entrepreneurship.

Labor services are traded in the labor market. The price of labor is the wage rate.

Most labor services are traded on a job contract.

Capital goods are traded in goods markets. Capital services are traded in rental

markets. The services of capital that a rm owns have an implicit price that arises

from depreciation and interest costs. Firms that buy capital and use it themselves

are implicitly renting the capital to themselves.

The price of the services of land is a rental rate. Nonrenewable natural

resources are resources that can be used only once.

Entrepreneurs receive the prot (or loss) that results from their business decisions

and their services are not traded in markets.

Looking back Before you jump into the content of this chapter, provide your students with

some context and perspective.

1. Recall the big issues of microeconomics discussed in Chapter 1. Point out that the

course so far has addressed the rst two questions: “What?” and “How?” and that

you’re now going to address how markets determine the answer to the third question:

“For whom?”

2. Spend a minute or two reviewing the course so far. Point out that Chapters 3–7,

demand and supply and its extensions and applications studied the @ows of goods and

services from rms to households. Chapters 8 and 9 studied the choices of households.

Chapters 10–15 studied the choices of rms. Now, we’re going to study the @ow of

goods and services from rms to consumer households in the product market and the

@ow of factors of production from households to rms in the factor markets.

3. Understanding choices at the margin, demand and supply, and market forces that

bring equilibrium and coordinate activity to produce eCciency are all used in this

chapter. Emphasize the power of the economic tools that the students already know

and the payoD from keeping on top of the entire course.

II. The Demand for a Factor of Production

The Value of Marginal Product

The demand for a factor of production

is called a derived demand because

it is derived from the demand for the

goods and services produced by the

factor.

The value to the rm of hiring one

more unit of a factor of production is

called the factor’s value of marginal

© 2016 Pearson Education, Inc.

Labor

(hours

per

day)

Output

(units

per

day)

Marginal

product

of labor

(units per

day)

Value of

margina

l

product

(dollars)

200 1,000

20 140

300 3,000

10 70

400 4,000

5 35

500 4,500

W H A T I S E C O N O M I C S ? 1 9 9

product. It is equal to the price of a unit of output multiplied by the marginal

product of the factor of production:

VMP = P MP

The table shows the calculation of the VMP for a rm whose output has a price of $7

per unit.

A Firm’s Demand for Labor

The rm hires the quantity of labor that maximizes its prot by comparing the value

of one more worker (the VMP) to the cost of employing one more worker, the wage

rate.

As more labor is employed, the MP diminishes (as shown in the table above). So as

more labor is employed, the VMP diminishes.

If VMP of labor exceeds the wage rate, the rm increases its prot by employing one

more worker; if VMP is less than the wage rate, the rm increases its prot by

employing one less worker; and, if VMP equals the wage rate, the rm is employing

the prot-maximizing quantity of labor.

A Firm’s Demand for Labor Curve

The value of marginal product curve is the rm’s labor demand curve.

Because the VMP of labor diminishes as the quantity of labor employed increases,

the demand curve for labor is downward sloping.

The prot-maximizing level of inputs implies the prot-maximizing level of

output. If you wish to go beyond the analysis in the book, you can take a bit of time to

show your students the basic math of the equivalence of the two conditions for maximum

prot—MR = MC and W = VMP—and give them a good intuitive grasp of what is going on.

There are six steps:

1. The cost of producing one more unit, MC, equals the cost of one more worker, W,

divided by that worker’s marginal product, MP. That is: MC = W/MP.

2. The revenue from selling one more unit, MR, equals the revenue from hiring one more

worker, VMP, divided by that worker’s marginal product, MP. That is: MR = VMP/MP.

3. Setting these two equations side by side: MC = W/MP and MR = VMP/MP is a tiny step to

see that MC = MR implies W = VMP.

4. Just write MC = MR implies W/MP = VMP/MP; multiply by MP and W = VMP.

5. Now put in some numbers to make the student who freezes on symbols more

comfortable.

6. Finally, just talk about what the equations mean. Explain that the marginal worker

costs $x and generates a revenue of $x, so that worker is just worth hiring. Hiring one

more worker costs $x but generates less than $x in revenue, so is not worth hiring.

Hiring one fewer worker saves $x but forgoes more than $x in revenue, so prot falls.

Go on to point out that one unit of output produced by the marginal worker sells for $p

and it costs $x/MP, which equals marginal cost.

Changes in a Firm’s Demand for Labor

Three factors can change the demand for labor and shift the labor demand curve:

If the price of the rm’s output changes, the VMP changes, which changes the

demand for labor. An increase in the price of the output increases the demand for

labor and shifts the demand curve rightward.

If the prices of other factors of production change, in the long run the demand for

labor changes. An increase in the price of a substitute factor leads the rm to

increase the demand for labor.

199

If a change in technology increases the productivity of one type of labor, the demand

for this labor increases and the demand curve shifts rightward.

III. Labor Markets

A Competitive Labor Market

The market demand for labor is determined by adding together the quantities of

labor demanded by all the rms in the market at each wage.

The market supply of labor is derived from the supply of labor decisions made by

individual households.

Aren’t households demanders? Point out that in the labor market, the tables have been

turned compared to the goods and services market. The household that is on the demand

side of the markets for consumer of goods and services is now on the supply side of the

market.

A person’s reservation wage is the lowest wage rate for which the person is willing to

supply labor. As the wage rate rises above the reservation wage, there is a

substitution eDect and an income eDect. The substitution eDect occurs because a

higher wage rate increases the opportunity cost of leisure, which increases the

quantity of labor supplied. The income eDect occurs because an increase in the

wage rate increases the person’s income and so increases the demand for leisure,

which decreases the quantity of labor supplied.

At lower wage rates, the substitution eDect dominates the income eDect, so a rise in

the wage rate increases the quantity of labor supplied. At higher wage rates, the

income eDect dominates the substitution eDect, so a rise in the wage rate decreases

the quantity of labor supplied and the supply of labor curve bends backward.

What’s your reservation wage? Ask the students if they would be willing to work 40

hours each week at a wage rate of $20 per hour (which is about $40,000 per year). Next,

ask them whether they would increase their labor supplied to 48 hours per week if they

could earn $40 per hour (about $80,000 per year, if working 40 hours per week). Most

students would be willing to work more hours per week at this wage rate. Then ask them

how many hours per week they would work if they were paid $10,000 per hour. In this

case, working only one day per week would garner them about $8 million per year, leaving

the remaining six days of each week to enjoy their high income. Many would not be willing

to continue working 48 hours a week, thereby creating a backward-bending supply of labor

curve.

The supply of labor increases (shifts rightward) when the adult population increases

and when capital and technology used in the home increase.

Labor market equilibrium determines the wage rate and employment.

Comparing competitive output markets with competitive input markets. Just as

the perfectly competitive rm in the market for a good or service is a price taker in that

market, so the individual household in a perfectly competitive factor market is a price

taker. Also, the rm that buys the services of the factor of production is a price taker in a

perfectly competitive factor market. Even in the market for land, which is in perfectly

inelastic supply, the individual landowner faces a perfectly elastic demand for his or her

land.

W H A T I S E C O N O M I C S ? 2 0 1

Di%erences and Trends in Wage Rates

DiDerences in demand and supply across labor markets make wage rates unequal.

The highest wage rates are earned in markets where the value of marginal product

is high and where few people have the ability and training for the job.

Because the value of marginal product increases over time as new capital and new

technologies increase labor productivity, wage rates also increase over time.

Wage inequality has increased recently with high wage rates increasing more

rapidly than low wage rates. Some low wage rates have stagnated or fallen. The

new information technologies increased the productivity and wage rates of already

high-paid workers. Globalization has brought increased competition for low-skilled

workers and lowered the wages of already low-paid workers.

An Economics in Action case has been updated with current Bureau of Labor Statistics data

on U.S. wages. The diDerence between median and mean income is highlighted as more

Americans earn less than the average income. The application also notes that higher than

average wage jobs typically require college and post graduate degrees.

An Economics in the News case considers how college majors aDect job prospects.

Biomedical engineering earns the top rating for starting median salary combined with

anticipated job growth. With both demand and supply increasing, the number of

biomedical engineers is expected to grow 60 percent between now and 2020. The case

takes students through the analysis of the changes in demand and supply and helps them

understand why both the number of jobs and salaries are expected to increase.

A Labor Market with a Union

A labor union is an organized group of workers that aims to increase the wage rate and

in@uence other job conditions. The text analyzes how unions impact the labor market

equilibrium for union workers and how this impacts nonunion workers.

To reach their goals, unions attempt to restrict the quantity of labor available for the

rm to employ (shifting the labor supply curve leftward).

Unions also attempt to in@uence the demand for labor and to increase the demand

for labor (shifting the labor demand curve rightward) with the following strategies:

Increase the marginal product of union members to increase the demand for

their labor.

Encourage import restrictions to increase the demand for union-made U.S.

products.

Support minimum wage laws to raise the cost of non-union low-skilled labor.

Support immigration restrictions to decrease the supply of competitive labor.

In equilibrium, if a union decreases the supply of labor, there will be fewer jobs at

higher wages. If it is able to also increase the demand for union labor, this will

further increase wages and oDset some of the decrease in employment. The market

for nonunion labor will also be eDected workers unable to get union jobs increase the

supply.

Monopsony in the Labor Market

A monopsony is a market in which there is a single buyer.

For a monopsony, the marginal cost of labor exceeds the wage rate because the

monopsony faces an upward-sloping labor supply curve. To attract one more worker,

the monopsony must oDer a higher wage rate, and it must pay this higher wage rate

to all its workers.

201

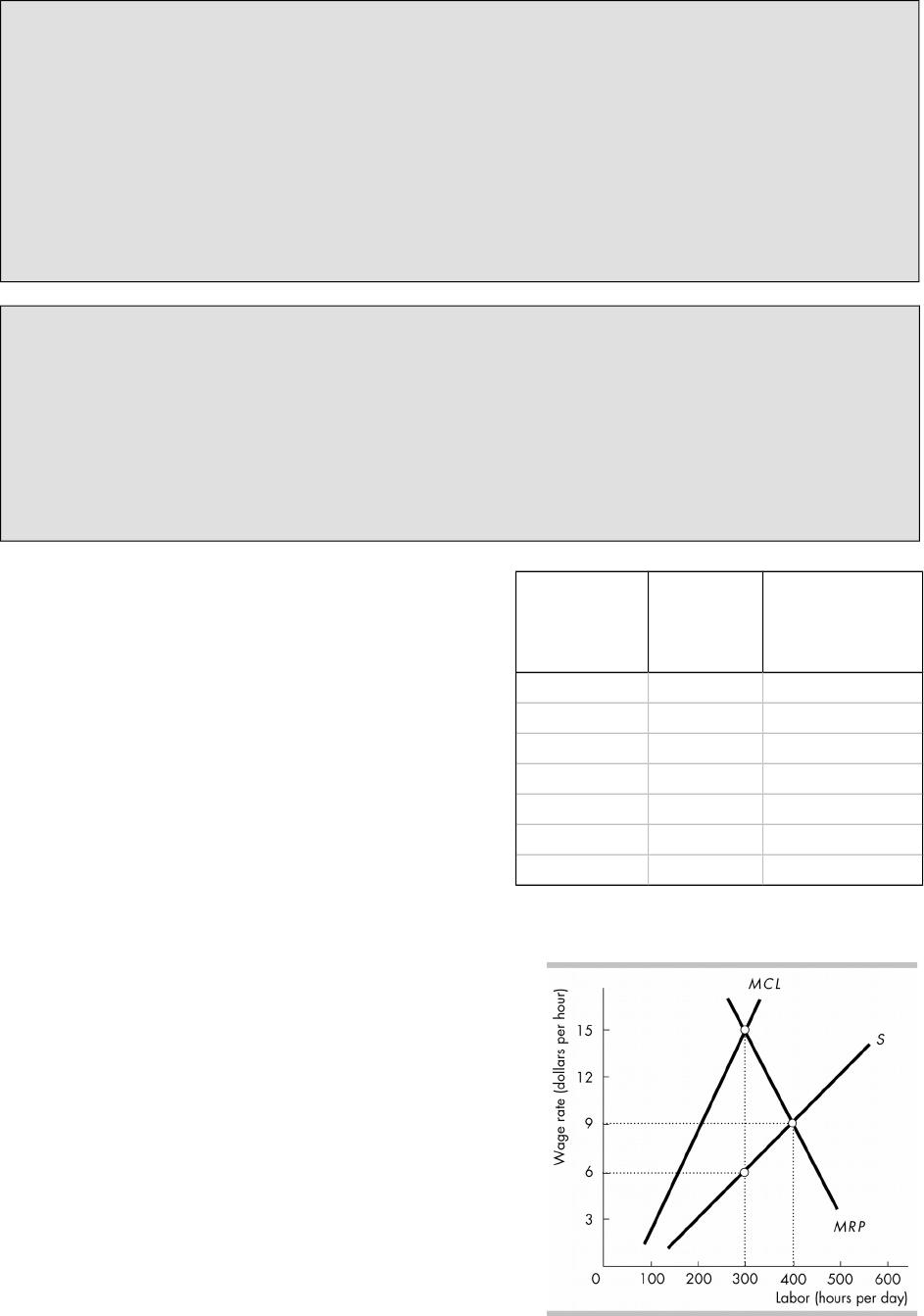

Example: The idea that the marginal cost of labor is somehow diDerent from the wage

rate is often confusing for students. Be sure to go through the intuition and the math

calculations for the marginal cost of labor several times. As in the table below, if

employment rises from 200 to 300 hours per day, the wage rate will rise from $3 to $6. The

total cost of labor rises from $600 to $1,800, a diDerence of $1,200. The change in total

cost divided by the change in employment will be $1,200/100 = $12. Intuitively, all 200

hours of labor were earning a wage of $3 per hour until the next 100 hours of labor were

employed. To entice those units of labor to supply their services, the wage rate rose to $6

for all 300 units of labor. As a result, the rm pays $6 for the new 100 hours of labor, and

pays an additional $3 for the 200 hours of labor it was previously employing. That’s $600

for the new 100 units of labor and an additional $600 for the wage increase paid to the

original 200 units of labor, for a marginal cost of labor equal to $1,200/100 = $12 again.

What about “wage discrimination”? Monopolies faced a downward-sloping demand

curve for their output, resulting in a marginal revenue curve that was below the demand

curve. To sell more output, monopolies had to lower the price. The story for monopsony is

similar. Because a monopsony faces an upward-sloping supply curve for labor, to hire more

labor, monopsonies have to raise the wage, resulting in a marginal cost of labor curve that

is above the labor supply curve. Some of your especially attentive students will remember

that marginal revenue and demand were the same when the rm could practice perfect

price discrimination. In the basic model of monopsony, we’re assuming there’s no “wage

discrimination.” Every worker is paid the same wage, just as every customer in a

single-price monopoly is charged the same price.

The rst two columns of the table show

the labor supply schedule and the last

column has the marginal cost of labor,

MCL, schedule. The MCL curve is upward

sloping and lies above the labor supply

curve.

To maximize its prot, a monopsony hires

the quantity of labor where its MCL is

equal to VMP and then pays the wage

rate necessary to attract that quantity of

labor. In the gure, the monopsony

employs 300 hours of labor per day and

pays a wage rate of $6 per hour.

A monopsony hires less labor and pays a

lower wage rate than it would if it were

operating in a competitive labor market. In

the gure, in a competitive labor market 400

hours of labor would be employed and the

wage rate would be $9 per hour.

Labor

(hours per

day)

Wage

rate

(dollars

per hour)

Marginal cost

of labor

(dollars per

hour)

200 3

12

300 6

18

400 9

24

500 12

W H A T I S E C O N O M I C S ? 2 0 3

A Union and a Monopsony

If a union, a monopoly seller of labor services, faces a monopsony buyer of labor

services, the situation is called bilateral monopoly. In a bilateral monopoly, the

wage rate is determined by bargaining and depends on the costs that each party

can in@ict on the other if they fail to agree upon a wage rate.

Examples of bilateral monopoly: Have the students consider the relationship between

professional team owners (NBA, NFL, etc.) and the players who work for these owners.

Such markets are classic examples of bilateral monopoly. Team owners operate a legal

cartel and maintain strict rules for hiring labor (drafting and trading players) that prevent

most of the competition among team owners who might want to sign the same player. So

the owners are close to a monopsony. The best players with uniquely talented skills cannot

be duplicated in the short run, so these players have a monopoly on their skills. The

resulting bilateral monopoly equilibrium is such that player’s wages in general are high

compared to most all other professions. This observation might surprise the students

because it suggests that bargaining position of the players is greater than that of the

owners.

Monopsony and Minimum Wages

The imposition of a minimum wage in a monopsony labor market might increase

both the wage rate and employment. The minimum wage makes the supply of labor

perfectly elastic over some range of employment. Over this range the supply curve

is horizontal and the MCL of an additional employee equals the minimum wage rate.

If this part of the supply curve of labor intersects the monopsony’s VMP curve, the

minimum wage increases both the quantity of labor employed by the monopsony

and the wage rate paid by the monopsony. The wage rate equals the minimum wage

rate.

The At Issue case presents the argument over whether monopolies are always bad,

focusing on the NCAA. Robert Barro argues that the NCAA monopoly hurts the market for

college athletics. Richard McKenzie and Dwight Lee argue that the NCAA monopoly has

helped college athletics.

203