T h e B i g P i c t u r e

Where we have been:

Chapter 12 on perfect competition has shown the student how rms make

output and pricing decisions under competitive market assumptions. Chapter

13 explains how a rm with monopoly power makes those same decisions.

Chapter 13 evaluates the eciency of monopoly relative to perfect

competition. It also covers regulation of a natural monopoly.

Where we are going:

Chapter 14 describes rms and industries in monopolistic competition.

Chapter 15 lls in the middle of the spectrum with a study of oligopoly. The

material discussing a monopoly’s downward-sloping demand curve and

resulting downward sloping marginal revenue curve is used in the next

chapter in the context of a rm in monopolistic competition. The result that a

monopoly can earn an economic prot is used in Chapter 15 as the

explanation why oligopolistic rms want to collude to raise their prices and

decrease the quantity they produce.

N e w i n t h e Tw e l f t h E d i t i o n

The chapter opening and a new Economics in the News case at the end of the

chapter look at Google’s success in the market. Is its dominance in search serving

the market and social interests or violating anti-trust law? A new Worked Problem

section has been added. The Worked Problem gives the students the demand and

cost schedule for a monopoly. It then shows the students how to calculate the

prot-maximizing price, quantity, economic prot, and producer surplus if the rm

is a single-price monopoly. Then it demonstrates to the students the

prot-maximizing quantity, economic prot, and producer surplus if the rm can

perfectly price discriminate. To include the new Worked Problem without

lengthening the chapter, some problems have been removed from the Study Plan

Problem and Applications. These problems are in the MyEconLab and are called

Extra Problems.

© 2016 Pearson Education, Inc

13 MONOPOLY

C h a p t e r

M O N O P O LY 143

L e c t u r e N o t e s

Monopoly

A monopoly is a market with a single rm that is protected by barriers to entry.

A monopoly maximizes its prot by producing where MR = MC and then using its

demand curve to set its price.

Price-discriminating monopolies charge a higher price to customers with a higher

willingness to pay.

Compared to a competitive market, a monopoly sets a higher price, produces a

smaller quantity, and converts consumer surplus into economic prot.

Natural monopolies can be regulated by the government.

I. Monopoly and How It Arises

A monopoly is a rm that produces a good or service for which no close substitute exists

and which is protected by a barrier that prevents other rms from selling that good or

service.

How a Monopoly Arises

A monopoly has two key features:

No Close Substitutes: There are no close substitutes for the good or service.

Barriers to Entry: A constraint that protects a rm from potential competition is

called a barrier to entry. There are three types of entry barriers:

Natural barriers to entry create a natural monopoly, which is an industry in

which economies of scale enable one rm to supply the entire market at the

lowest possible cost.

An ownership barrier to entry occurs if one rm owns a signicant portion of a

key resource.

Legal barriers to entry create a legal monopoly, which is a market in which

competition and entry are restricted by the granting of a public franchise (an

exclusive right is granted to a rm to supply a good or service—the U.S. Postal

Service has a public franchise to deliver rst-class mail), a government license

(when the government controls entry into particular occupations, professions and

industries—a license is required to practice law), a patent (an exclusive right

granted to the inventor of a product or service) or a copyright (exclusive right

granted to the author or composer of a literary, musical, dramatic, or artistic

work). In the U.S., patents last twenty years, encouraging innovation and

stimulating invention.

Who has to have a license to produce? There are many examples of government

licensing. Licensing can protect consumers from fraud and abuse, but it can also hurt

consumers by preventing competition from producing an ecient allocation of resources.

Have the students debate the merits of the following licensing arrangements: 1) Doctors

can receive a medical license to practice medicine only by graduating from an

AMA-approved medical program; 2) Lawyers can practice law only after passing an

extensive Bar Exam; 3) Cab drivers in New York City can operate a taxi only if they have

purchased a medallion from the city, of which there are a nite number; 4) Beauticians in

many states cannot operate a beauty parlor without a state certication that requires

training in sanitary practices as well as other courses completely unrelated to their

profession (such as civics and history courses).

© 2016 Pearson Education, Inc

What’s the advantage of patents? Granting an innovator a monopoly to the innovation

increases the incentives to innovate. But the evidence whether monopoly leads to greater

innovation is mixed. Consider the struggle for developing countries with populations

dealing with epidemics such as AIDS. In the developed countries in which they operate,

pharmaceutical companies are granted legal barriers (patents) on their drugs, granting

them a legal monopoly and enabling them to earn a high economic prot once they bring a

new and successful medicine to market. The anticipation of this prot provides the

incentive for these rms to undertake the expensive (currently estimated at approximately

$900 million per approved drug) and risky development of innovative cures for the terrible

diseases aDicting mankind, such as AIDS. However, once the new medicines are made

available, the absence of competition means the price is high, which decreases the use of

these new medicines, especially among the population of the poorer, developing nations

that have been hit the hardest by these diseases. So, once the drug is discovered, the

monopoly creates a deadweight loss but without the economic prot the monopoly brings,

the drug might not have been discovered. There is a tradeoE between current suEerers,

who want a low price, and suEerers in the future, who want new and better medicines

developed.

The Economics in Action case considers how the information age has led to the creation of

new natural monopolies. These rms have high xed costs but almost zero marginal costs.

The rms cited include Google, Microsoft, and Facebook. These same information age

technological changes have hurt other monopolies such as the U.S. Postal Service, with

competition from FedEx, UPS, email, and online payments systems. Local cable television

providers now face competition from satellite and phone companies.

Monopoly Price-Setting Strategies

A single-price monopoly is a rm that sells each unit of its output for the same

price to all its customers.

Price discrimination is the practice of selling diEerent units of a good or service

for diEerent prices. Many rms price discriminate, but not all of them are monopoly

rms.

II. A Single-Price Monopoly’s Output and Price Decision

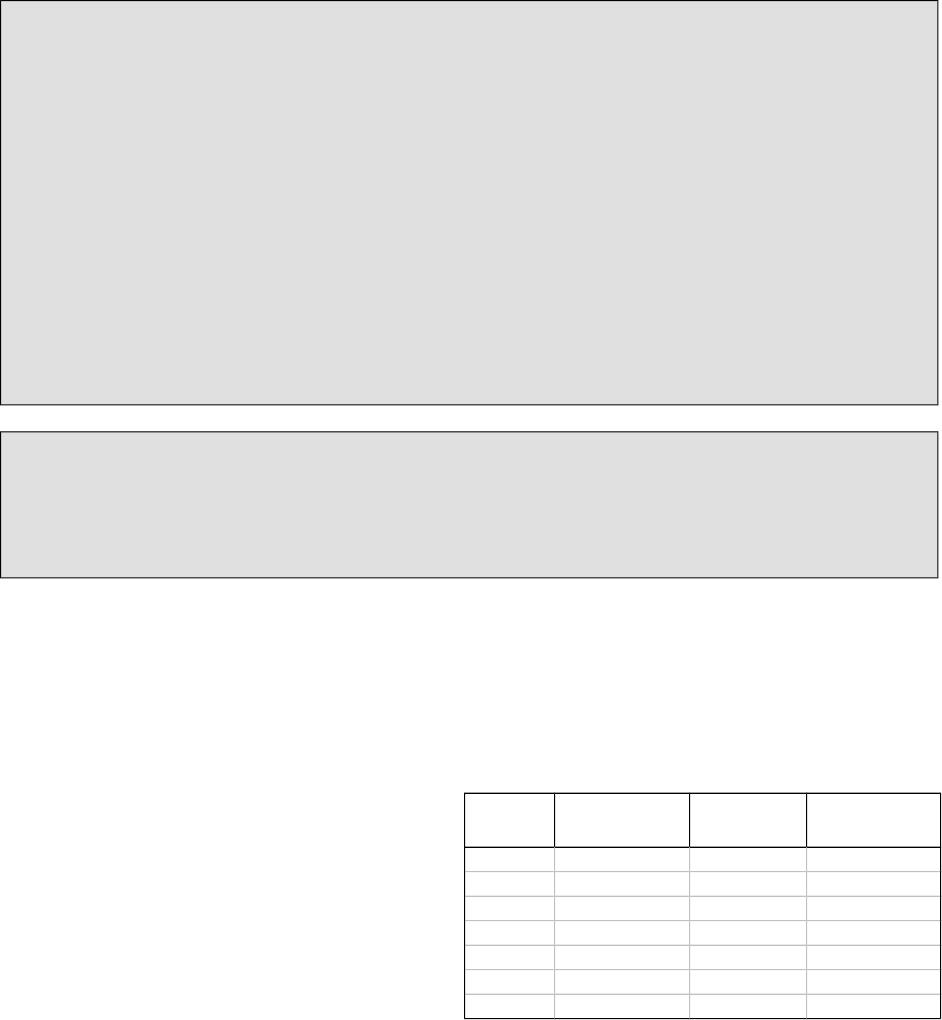

Price and Marginal Revenue

The demand curve facing a

monopoly rm is the market

demand curve. Total revenue (TR)

is the price (P) multiplied by the

quantity sold (Q). Marginal revenue

(MR) is the change in total revenue

resulting from a one-unit increase

in the quantity sold.

The table shows the calculation of

TR and MR.

A key feature of a single-price monopoly is that MR < P at each quantity so the MR

curve lies below the demand curve. MR < P because a single–price monopoly must

lower its price on all units sold to sell an additional unit of output.

© 2016 Pearson Education, Inc

Price

Quantity

demanded

Total

revenue

Marginal

revenue

$4 0 $0

$3

$3 20 $60

$1

$2 40 $80

$1

$1 60 $60

M O N O P O LY 1 4 5

Why is MR below the price? While the formula isn’t dicult, students often have trouble

understanding this concept intuitively. If a rm sells output for $2, why aren’t they getting

$2 of revenue for each unit of output they sell so that marginal revenue is $2? Remind

students that we are assuming that the monopoly charges the same price to all

consumers. As in the table above, if on any given day, every consumer is paying $2 for

output, 40 units are demanded and total revenue is $80. If the monopoly decides it wants

to sell more than 40 units the next day, it must lower the price to do so. The monopoly is

NOT simply lowering the price to $1 for units 41 through 60. Rather, the monopoly lowers

the price on ALL units it will sell the next day. As a result, units 1 through 40 that

customers used to pay $2 for will now be sold for only $1. That’s a loss of $1 on each of

those 40 units for a revenue loss of $40. Part of that revenue loss is oEset by the sales of

units 41 through 60. Since the rm gains $1 in revenue from the sale of each of those

units, there is a revenue gain of $20. A revenue loss of $40 (from lowering prices)

compared with a revenue gain of $20 (from selling more output) generates a net revenue

loss of $20, and (when divided by the change in output from 40 to 60) a marginal revenue

of negative $1. For visual learners, showing these areas of revenue gain and revenue loss

should also help (similar to Figure 13.2 in the text).

Marginal Revenue and Elasticity

If demand is elastic, the MR is positive. A decrease in the price will result in a

proportionately greater increase in quantity, generating an increase in revenue.

If demand is unit elastic (as it is at the midpoint of a linear demand curve), the MR

equals zero. A change in the price will result in a proportionate change in quantity,

generating no change in revenue. If further increase in revenue is not possible from

changing price, this is also the point where revenue is maximized.

If demand is inelastic, MR is negative. A decrease in price will result in a

proportionately smaller increase in quantity, generating a decrease in revenue.

A single-price monopoly never produces in the inelastic part of its demand because

if it did, the rm could increase its total prot by decreasing its output, which would

raise its total revenue and decrease its total cost.

But if a monopoly is the only producer so there are no substitutes, isn’t demand

always inelastic? This question is common. As the only producer of a good, a monopoly

does have some control over the price it charges for output, and students understand that

conceptually. For example, when you go to the movie theater, you know you’re likely to pay

$5 or more for a tub of popcorn, even though you could buy the same amount of popcorn

at the grocery store for $1 or less. Because you’re stuck at the movie theater with

whatever options they oEer, consumers end up paying a higher price. In other words,

because there are fewer substitutes at the theater, demand for popcorn is less elastic.

However, that fact does NOT mean that the demand for popcorn at a movie theater

universally has an elasticity of demand that’s less than one. Even if demand for a

monopoly’s product is fairly inelastic, the demand still has some ranges where elasticity is

greater than one (anywhere above the midpoint on a linear demand curve, for example).

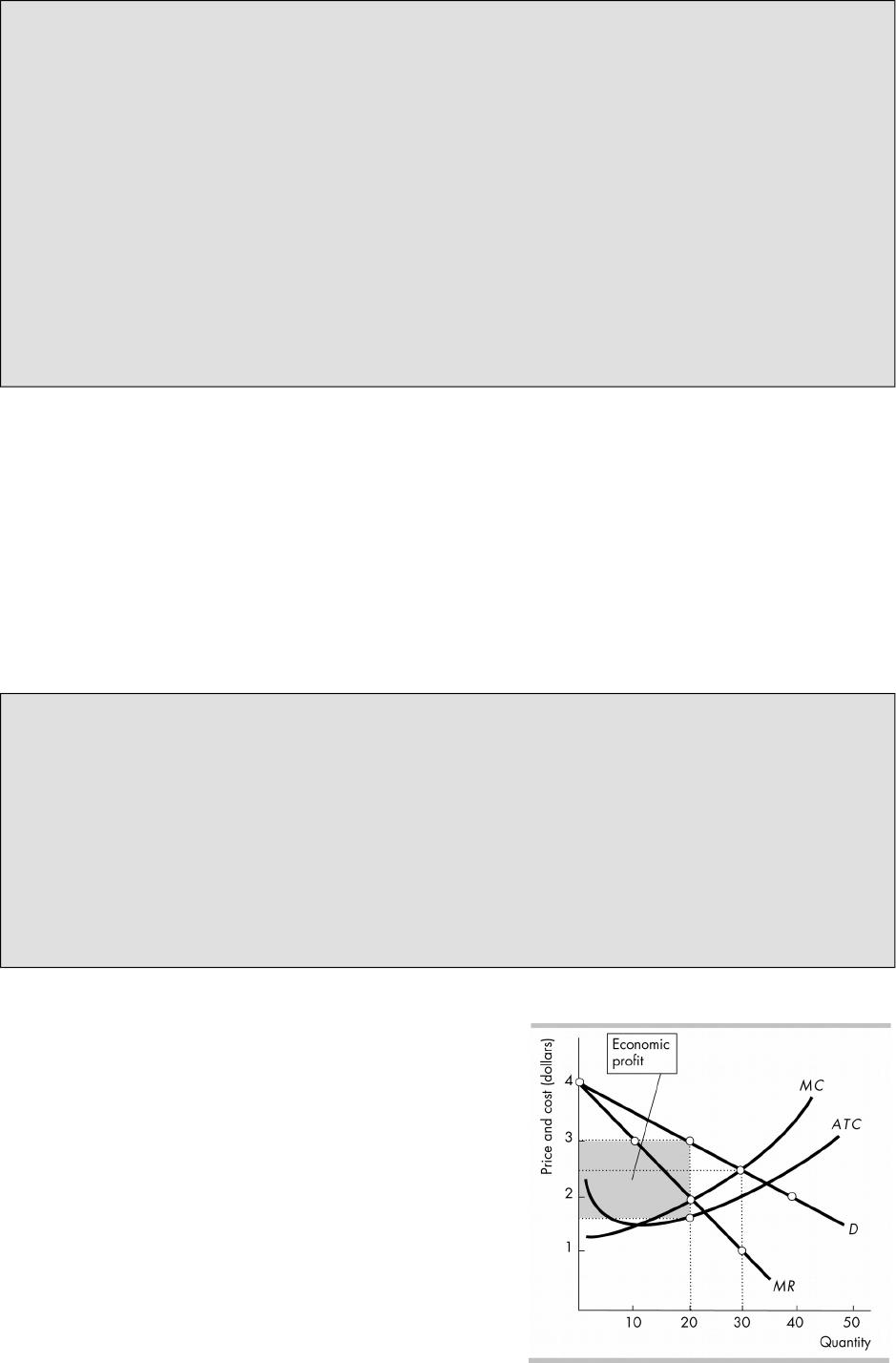

Price and Output Decision

To maximize its prot, a monopoly produces

the level of output where MR = MC. The

monopoly then uses its demand curve to set

the price at the highest price for which it will

be able to sell the quantity it produces. In

the gure, which uses the demand and MR

schedules from the table above, the rm produces 20 units of output and sets a price

of $3 per unit.

The rm makes an economic prot if P > ATC, which is the case for the rm in the

gure. The monopoly can make an economic prot even in the long run because the

barriers to entry protect the rm from competition. However, a monopoly rm is not

guaranteed an economic prot. In the short run and/or long run, it might make zero

economic prot, (P = ATC) or in the short run, it might incur an economic loss

(P < ATC).

Joan Robinson and Paul Samuelson: The classic monopoly diagram provides a good

opportunity to tell your students about the contribution of one of the most brilliant

economists of the 20th century, Joan Robinson. This diagram rst appeared in her book,

The Economics of Imperfect Competition, published in 1933 when she was just 30 years

old.

Women are still not attracted to economics on the scale that they’re attracted to most

other disciplines, so the opportunity to talk about an outstanding female economist

shouldn’t be lost. Joan Robinson was a formidable debater and reveled in verbal battles, a

notable one of which was with Paul Samuelson on one of her visits to MIT. Anxious to make

and illustrate a point, Samuelson asked Robinson for the chalk. Monopolizing the chalk and

the blackboard, the unyielding Robinson snapped, “Say it in words young man.”

Samuelson meekly obeyed. This story illustrates Joan Robinson’s approach to economics:

work out the answers to economic problems using the appropriate techniques of math and

logic, but then “say it in words.” Don’t be satised with formal argument if you don’t

understand it. Your students will benet from this story if you can work it into your class

time.

III. Single-Price Monopoly and Competition Compared

Comparing Price and Output

Perfect Competition: The market demand curve (D) in perfect competition is the

same demand curve that the rm faces in monopoly. The market supply curve (S) in

perfect competition is the horizontal sum of the individual rm’s marginal cost

curves. This supply curve also is the monopoly’s marginal cost curve, so in the gure

above the supply curve is labeled MC. In a competitive market, equilibrium occurs

where the quantity demanded equals the quantity supplied. In the gure above, the

competitive equilibrium quantity is 30 units and the competitive equilibrium price is

$2.50 per unit.

Monopoly: The monopoly produces where MR = MC and sets its price using its

demand curve. In the gure, the monopoly produces 20 units of output and sets a

price of $3.00 per unit.

Compared to a perfectly competitive industry, a single-price monopoly produces less

output and sets a higher price.

Is the monopolist’s marginal cost curve its supply curve? Although most students

will be satised with the comparison of the monopolist’s marginal cost curve to a

competitive market’s supply curve, some students will mistakenly assume that the

monopolist’s marginal cost curve is also the monopolist’s supply curve. A monopolist

actually has no “supply curve” because there is no single curve that provides information

both on the quantity supplied and the price. If the rm produces 20 units of output when it

is maximizing prot, that output level is determined by the point where MC = MR. However,

the price charged for that output doesn’t come from the MC curve. The price comes from

© 2016 Pearson Education, Inc

M O N O P O LY 147

the market demand curve. As a result, there is no relationship between the quantity

supplied and price that is dened by the marginal cost curve.

E(ciency Comparison and Redistribution of Surpluses

A perfectly competitive industry produces the ecient quantity of output, where

MSB = MSC. Because a single-price monopoly produces less output (where MSB >

MR = MC = MSC), it underproduces and creates a deadweight loss.

Consumer surplus is smaller with a monopoly than with perfect competition. In the

gure above, the consumer surplus under perfect competition is the area under the

demand curve and above the competitive equilibrium price of $2.50 per unit. Under

monopoly the consumer surplus is the area under the demand curve and above the

monopoly price of $3.00.

Though the monopoly creates a deadweight loss, the monopoly’s owners benet

because it earns an economic prot. A monopoly’s owners benets because the

monopoly redistributes some of the consumer surplus away from the consumer and

to the monopoly.

Does ine$ciency imply less pro%t? It is important for students to recognize that the

source of the ineciency of a monopoly rm’s output and pricing decision arises from the

absence of competition in the market, rather than any change in the behavioral

assumptions about the rm owners. All rms maximize prot, but that goal does not imply

eciency when there is less than perfect competition in a market.

Rent Seeking

Any surplus—consumer surplus, producer surplus, and economic prot—is called

economic rent. Rent seeking is the pursuit of wealth by capturing economic rent.

Rent seeking can occur when someone uses resources seeking the opportunity to

buy a monopoly for a price less than the monopoly’s economic prot.

Rent seeking also can occur when someone uses resources lobbying the

government to create a monopoly. Because of rent seeking, the social cost of

monopoly exceeds the deadweight loss it creates.

The resources used in rent seeking are a cost to society that adds to the monopoly’s

deadweight loss. Because there are no barriers to entry in the activity of rent

seeking, the resources used up can equal the monopoly’s potential economic prot,

reducing monopoly prot.

IV. Price Discrimination

Price discrimination is the practice of selling diEerent units of a good or service for

diEerent prices. Price discrimination converts consumer surplus into economic prot.

To be able to price discriminate, a rm must:

Identify and separate diEerent buyer types.

Sell a product that cannot be resold

Two Ways of Price Discriminating

Price discrimination occurs because of people’s diEerent willingness to pay for the

good. A rm can charge the same buyer diEerent prices for diEerent units of a good

or a rm can charge diEerent prices to diEerent groups of buyers.

Discriminating Among Groups of Buyers: A rm can charge diEerent customers

diEerent prices for the product. Groups with a higher willingness to pay are

charged a higher price and groups with a lower willingness to pay are charged a

lower price. For example, business airline travelers who have a high willingness

to pay and often make last-minute reservations are charged a higher price than

leisure travelers, who have a low willingness to pay and often make advance

reservations.

Discriminating Among Units of a Good: A rm can charge a higher price for the

rst units purchased and a lower price for later units purchased. An example is

pizza delivery, where the second pizza is generally cheaper than the rst.

Increasing Pro-t and Producer Surplus

If buyers pay close to the maximum they are willing to pay, a monopoly converts

consumer surplus into producer surplus. More producer surplus means more

economic prot.

Economic prot is TR − TC and Producer Surplus is TR − TVC. Therefore Economic

Prot = Producer Surplus − Total Fixed Costs. Consequently, for a given level of

xed costs, anything that increases producer surplus increases economic prot.

Perfect price discrimination occurs if a rm is able to sell each unit of output for

the highest price anyone is willing to pay for it. In this case, the price of each unit is

the same as the unit’s marginal revenue, so the rm’s (downward sloping) demand

curve becomes the same as its marginal revenue curve. Output increases to the

point where the demand (= marginal revenue) curve intersects the marginal cost

and the ecient quantity is produced. The deadweight loss is eliminated. The rm’s

economic prot is the greatest possible. But consumer surplus equals zero because

the rm captures the entire consumer surplus.

An Economic in Action feature considers Disney World’s ticket pricing. High prices for the

rst three days seem to extract most of the consumer surplus.

E(ciency and Rent Seeking With Price Discrimination

The more perfectly a monopoly can price discriminate, the greater the amount of its

output and the more ecient the outcome.

Because the producer grabs the entire surplus in perfect price discrimination, rent

seeking becomes protable, and the long-run equilibrium outcome is that rent

seekers use up the entire producer surplus.

Can only monopolies price discriminate? The text uses the example of price

discrimination by an airline. Another easy example of price discrimination is movie

theaters: The price of watching a movie at 8:00 is higher than the price of watching the

same movie at 5:00. But these examples often lead to a very pertinent question from

students: “Neither airlines nor theaters are monopolies. So why can they price

discriminate?” You need to explicitly tell your students that any rm which has some

control over the price it sets has the potential to price discriminate. Monopolies have

control over the price it sets, so we discuss price discrimination in the chapter dealing with

monopoly. But in the “real world,” many rms other than monopolies, such as airlines and

movie theaters, practice price discrimination.

An Economics in the News application describes Microsoft’s launch of Windows 8 and

includes pricing data from various sources for Windows 7 to explore price discrimination.

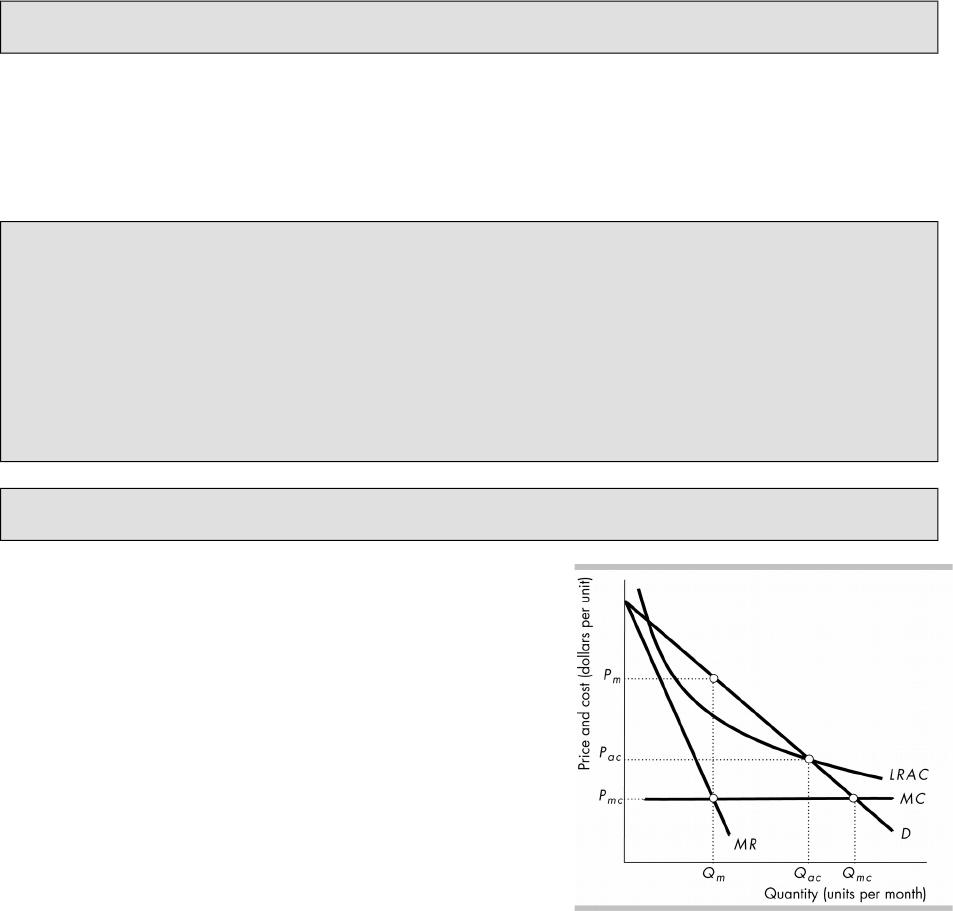

V. Monopoly Regulation

A natural monopoly is an industry in which

one rm can supply the entire market at a

lower cost than can two or more rms. The

denition of a natural monopoly means that

the rm’s LRAC curve falls throughout the

© 2016 Pearson Education, Inc

M O N O P O LY 149

relevant range of production. As a result, the rm’s MC curve is below its LRAC curve

when the MC curve crosses the rm’s demand curve.

The gure shows a natural monopoly with constant marginal costs. A natural

monopoly has large economies of scale so that one rm can supply the entire

market at lower cost than two rms because the LRAC curve is falling even when the

entire market is supplied.

A natural monopoly produces at the lowest possible cost, but as an unregulated

monopoly it will raise the price above the competitive price and produce less than

the ecient quantity. To try to reap the benets of the lower costs while avoiding the

drawback of a monopoly, natural monopolies are typically given a public franchise

(so they are given the right to be a monopoly) but are regulated by a government

agency.

The social interest theory says that political and regulatory processes seek out

ineciency, reduce deadweight loss, and allocate resources eciently. Capture

theory says regulation serves the interest of producers who capture the regulators to

maximize economic prots.

E(cient Regulation of a Natural Monopoly

An unregulated natural monopoly will produce where MR = MC and use its demand

curve to set the highest price for which this quantity is demanded. In the gure,

when unregulated, the rm produces Qm and sets a price of Pm. There is a

deadweight loss.

A marginal cost pricing rule sets price equal to marginal cost. In the gure, the

rm produces Qmc and sets a price of Pmc. This regulation results in an ecient use

of resources but the rm’s price is less than its average cost, so the monopoly incurs

an economic loss.

If rms are regulated with a marginal cost pricing rule, they incur an economic loss

because the price is less than the average cost. They will have to be paid a subsidy

by the government or allowed to price discriminate in order to avoid the economic

loss.

Second-best Regulation of a Monopoly

An average cost pricing rule sets price equal to average total cost. In the gure,

the rm produces Qac and sets a price of Pac. Because a normal prot is part of the

rm’s costs, the rm earns a normal prot. The amount of output, however, is

inecient, though it is closer to the ecient quantity than when the monopoly is

unregulated. Government subsidies could oEset those losses but would create

deadweight losses from the taxes that would have to be increased to pay the

subsidies.

Because regulators cannot determine a rm’s exact costs, rate of return

regulation is often used.

Rate of return regulation requires a rm to justify its price by showing that

the price enables it to earn a specied target percent return on its capital. When

this policy is used, the managers of the regulated rm have the incentive to

inTate its costs for benecial amenities that do not promote eciency but

instead give the managers more amenities.

Because rate of return regulation does not give the rm the incentive to operate

eciently, price-cap regulation is now used more frequently.

A price–cap regulation is a price ceiling—a rule that species the highest price the

rm is permitted to set. Price cap regulation gives managers an incentive to

minimize costs: if the rm decreases its costs and earns an economic prot, the rm

will be allowed to keep all (or part) of the prot. Typically price cap regulation also

requires earnings sharing regulation, under which prots that rise above a

target level must be shared with the rm’s customers.

Economics in the News: The Economics in the News analyzes whether Google leveraged

its dominant position in search to highlight its own products and services in search results.

It concludes that Google is attempting to perfectly price discriminate and does not appear

to be acting against the social interest.

© 2016 Pearson Education, Inc

M O N O P O LY 1 5 1