Answers to Additional Problems and

Applications

Use the following news clip to work Problems 10 to 12.

Money in the Tank

Two gas stations stand on opposite sides of the road: Rutter’s Farm Store and

Sheetz gas station. Rutter’s doesn’t even have to look across the highway to know

when Sheetz changes its price for a gallon of gas. When Sheetz raises the price,

Rutter’s pumps are busy. When Sheetz lowers prices, there’s not a car in sight.

Both gas stations survive but each has no control over the price.

Source: The Mining Journal, May 24, 2008

10. In what type of market do these gas stations operate? What determines the

price of gasoline and the marginal revenue from gasoline?

These stations operate in a perfectly competitive market. The equilibrium price is

11. Describe the elasticity of demand that each of these gas stations faces.

Each station’s elasticity of demand is very high. When one station raises its price

12. Why does each of these gas stations have so little control over the price of

the gasoline they sell?

These stations face a large amount of competition, not only from each other but

also from all nearby gas stations. If a 1rm raises its price it loses a vast number of

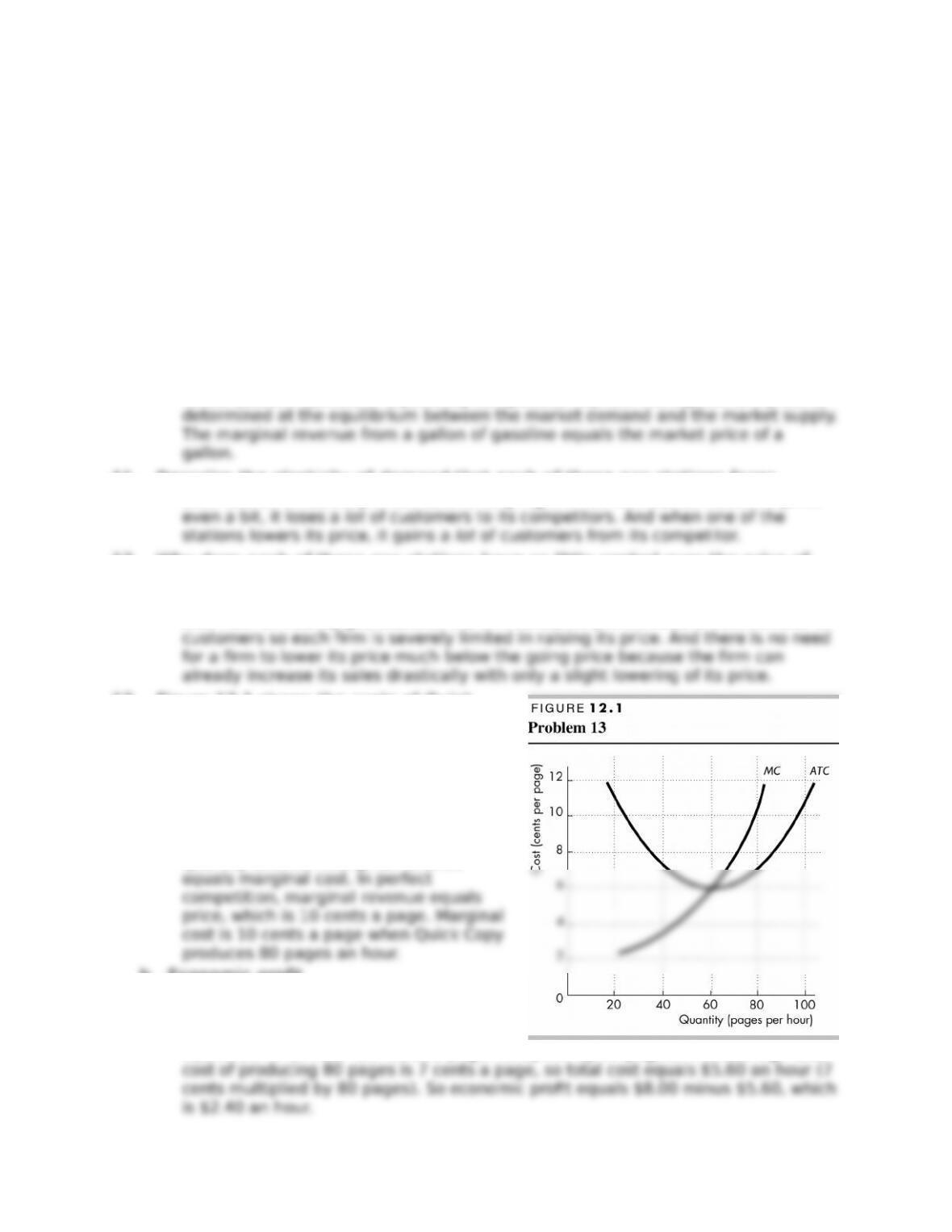

13. Figure 12.1 shows the costs of Quick

Copy, one of many copy shops near

campus. If the market price of copying is

10¢ a page, calculate Quick Copy’s

a. Pro1t-maximizing output.

Quick Copy’s pro1t-maximizing quantity

is 80 pages an hour. Quick Copy

maximizes its pro1t by producing the

quantity at which marginal revenue

b. Economic pro1t.

Quick Copy’s economic pro1t is $2.40 an

hour. Economic pro1t equals total

revenue minus total cost. Total revenue

equals $8.00 an hour (10 cents a page multiplied by 80 pages). The average total

14. The market for smoothies is

perfectly competitive and the

market demand schedule is in the

1rst table. Each of the 100

producers of smoothies has the

quantity supplied. The 1rm’s supply

curve is the same as its marginal cost curve at prices above minimum average

variable cost. Average

variable cost is a minimum

when marginal cost equals

average variable cost.

b. What is the market quantity of smoothies?

c. How many smoothies does each 1rm sell?

d. What is the economic pro1t made or economic loss incurred by each 1rm?

Each 1rm incurs an economic loss. Each 1rm produces 7 smoothies at an average

15. Chevy Volt Production Temporarily Shut Down

GM will temporarily lay oA 1,300 employees as the company stops production

of the electric car, Chevy Volt, for 1ve weeks. GM had hoped to sell 10,000

Volts last year, but ended up selling just 7,671. It plans to maintain inventory

levels by adjusting production to match demand.

Source: Politico, March 2, 2012

a. Explain how the shutdown decision will aAect GM Chevy Volt’s TFC, TVC, and

TC.

Price

(dollars per

smoothie)

Quantity

demanded

(smoothies per

hour)

Output

(smooth

ies

Marginal cost

(dollars per

additional

Average

variable

cost

Averag

e total

cost

b. Under what conditions would this shutdown decision maximize Chevy Volt’s

economic pro1t (or minimize its loss)? Explain your answer.

GM will shut down its plant when the price of a Volt is less than its average

c. Under what conditions will GM start producing the Chevy Volt again? Explain

your answer.

GM will start producing the Chevy Volt again when the price of Volt exceeds its

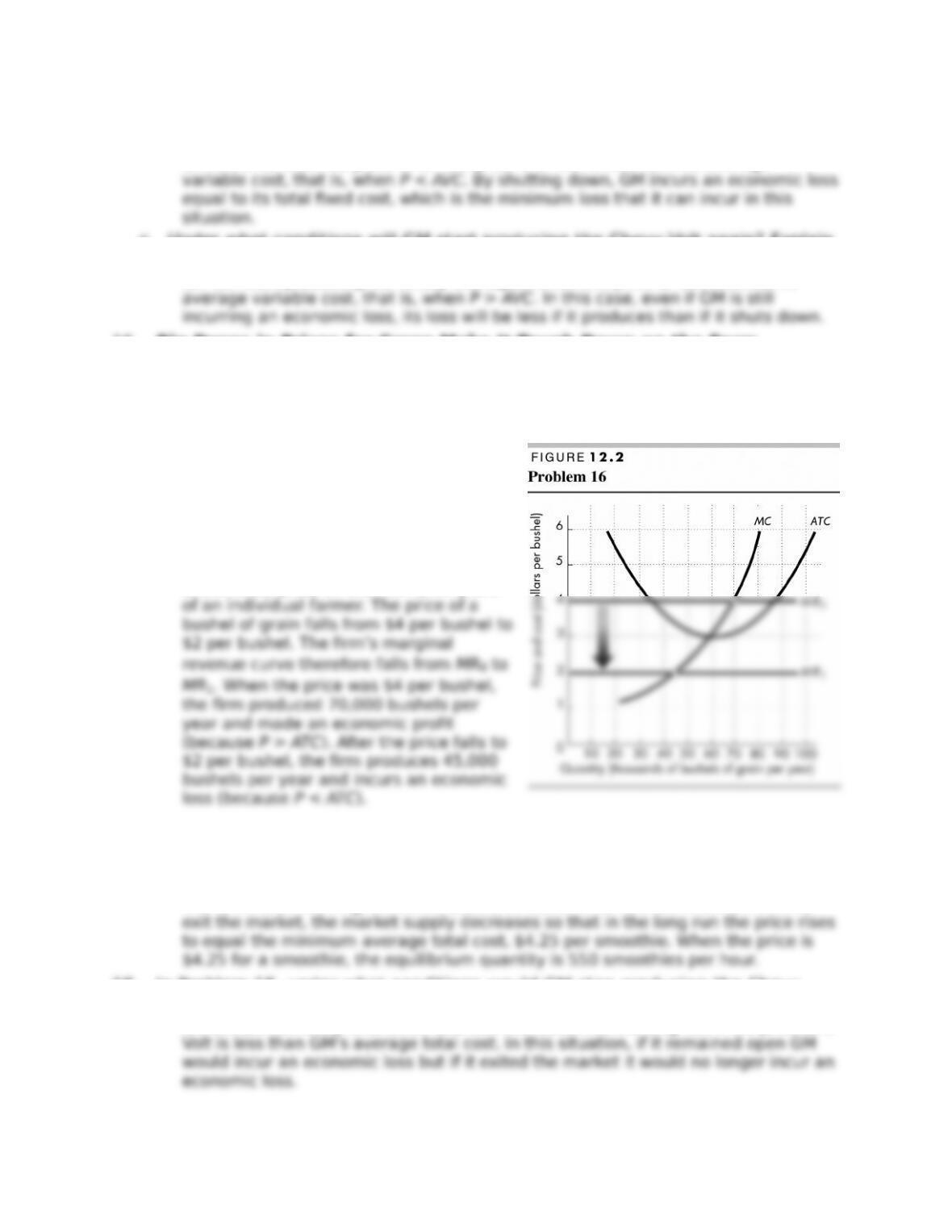

16. Big Drops in Prices for Crops Make It Tough Down on the Farm

Grain prices have fallen roughly 50 percent from earlier this year. With

better-than-expected crop yields, world grain production this year will rise

nearly 5 percent from 2007 to a record high.

Source: USA Today, October 23, 2008

Why did grain prices fall in 2008? Draw a

graph to show that short-run eAect on

an individual farmer’s economic pro1t.

Grain prices fell in 2008 because the

supply of grain increased. The increase in

the supply of grain drives the prices of

grain lower. Figure 12.2 shows the eAect

of the lower price on the economic pro1t

17. In Problem 14, do 1rms enter or exit the market in the long run? What is the

market price and the equilibrium quantity in the long run?

The 1rms are incurring economic losses, so some 1rms exit the market. As 1rms

18. In Problem 15, under what conditions would GM stop producing the Chevy

Volt and exit the market for electric cars. Explain your answer.

GM will permanently shut down and exit the market in the long run if the price of a

19. Exxon Mobil Selling All Its Retail Gas Stations

Exxon Mobil is not alone among Big Oil exiting the retail gas business, a

market where pro1ts have gotten tougher as crude oil prices have risen. Gas

station owners say they’re struggling to turn a pro1t because while wholesale

gasoline prices have risen sharply, they’ve been unable to raise pump prices

fast enough to keep pace.

Source: Houston Chronicle, June 12, 2008

a. Is Exxon Mobil making a shutdown or exit decision in the retail gasoline

market?

b. Under what conditions will this decision maximize Exxon Mobil’s economic

pro1t?

This decision maximizes Exxon Mobil’s economic pro1t if Exxon Mobil’s retail

c. How might Exxon Mobil’s decision aAect the economic pro1t of other

gasoline retailers?

Exxon Mobil’s exit will decrease the number of retail 1rms selling gasoline. The

20. Another DVD Format, but It’s Cheaper

New Medium Enterprises claims the quality of its new system, HD VMD, is

equal to Blu-ray’s but at $199 it’s cheaper than the $300 Blu-ray player. The

Blu-ray Disc Association says New Medium will fail because it believes that

Blu-ray technology will always be more expensive. But mass production will

cut the cost of a Blu-ray player to $90.

Source: The New York Times, March 10, 2008

a. Explain how technological change in Blu-ray production might support the

prediction of lower prices in the long run. Illustrate your explanation with a

graph.

Technological change will decrease the

1rm’s average total cost and marginal

cost. As more 1rms adopt the new

technology, the market supply will

increase, which drives down the price.

b. Even if Blu-ray prices do drop to $90 in the long run, why might the HD VMD

still end up being less expensive at that time?

Quite likely there will be technological advances in the HD VMD laser player which

decrease its costs of production, increase its market supply, and lower its price.

21. In a perfectly competitive market, each 1rm maximizes its pro1t by choosing

only the quantity to produce. Regardless of whether the 1rm makes an

economic pro1t or incurs an economic loss, the short-run equilibrium is

eIcient. Is the statement true? Explain why or why not.

The statement is true. A perfectly competitive 1rm is a price taker and so it has no

choice about what price it will charge. If there are no external bene1ts or external

Economics in the News

22. After you have studied Economics in the News on pp. 290–291, answer the

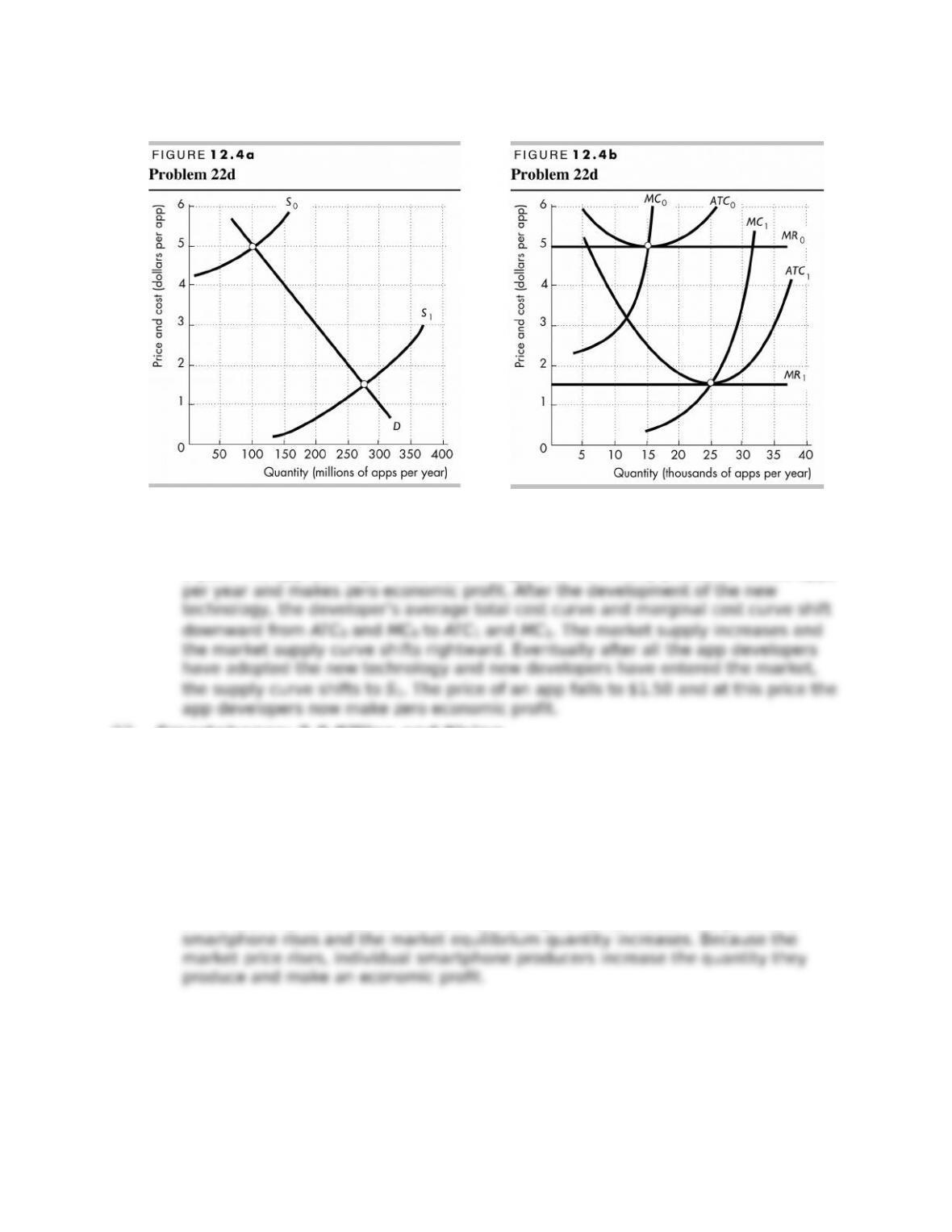

following questions.

a. What are the features of the market for apps that make it competitive?

The market for apps is highly competitive because there are many producers and

b. Does the information provided in the news article suggest that the app

market is in long-run equilibrium? Explain why or why not.

c. How would an advance in development technology that lowered a

developer’s costs change the market supply and the developer’s marginal

revenue, marginal cost, average total cost, and economic pro1t?

An advance in development technology that lowers developers’ costs increases the

market supply, which lowers the market price. Developers’ marginal revenue is

equal to the market price, so the fall in the price lowers the marginal revenue. The

new technology lowers developers’ marginal cost and average total cost and the

d. Illustrate your answer to part (c) with an appropriate graphical analysis.

Figure 12.4a shows the market for apps; Figure 12.4b shows an individual app

developer. Before the advancement in development technology, the market supply

curve is S0 and the price is $5 per app and 100 million apps are bought and sold in

a year. The app developer illustrated in Figure 12.4b initially produces 15,000 apps

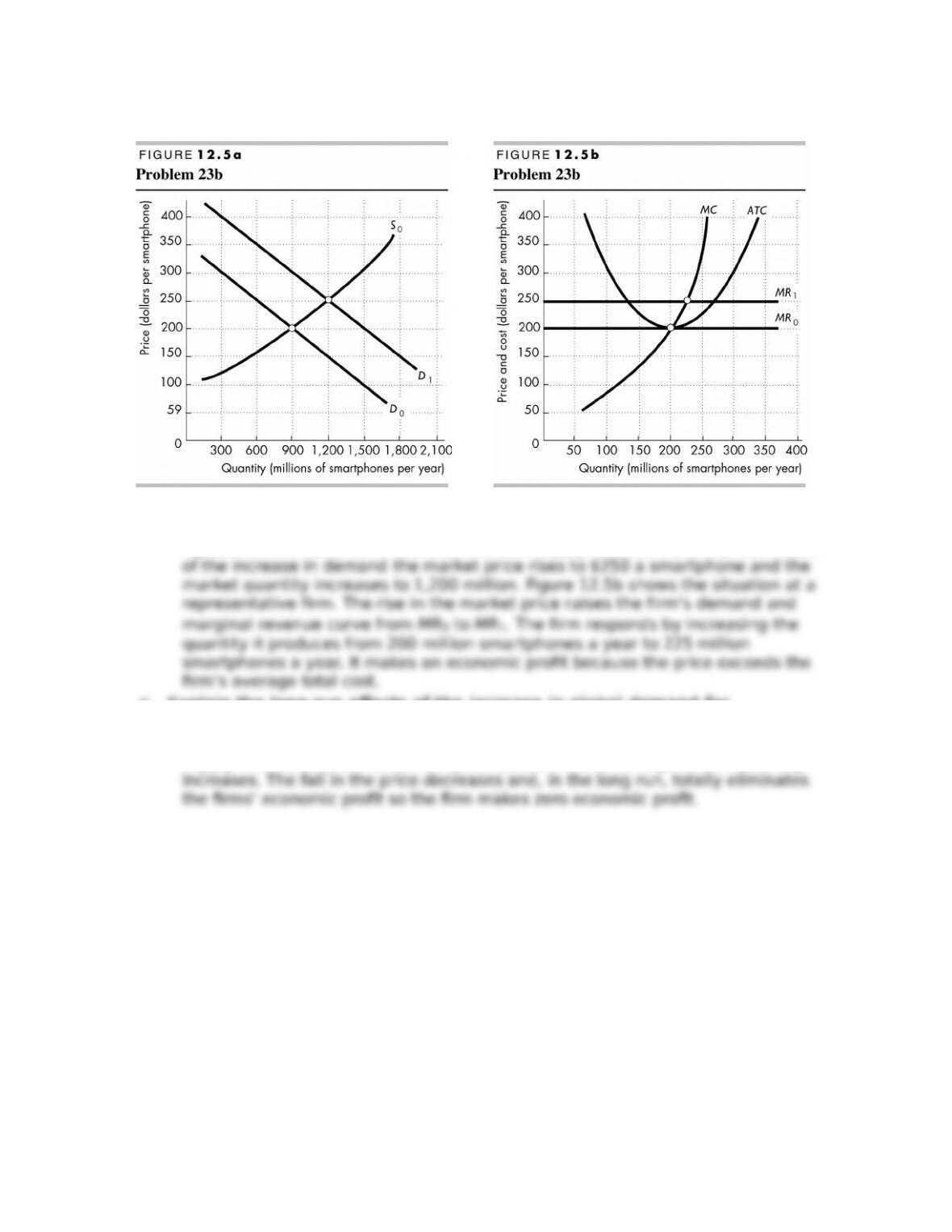

23. Smartphones: 2.6 Billion and Rising

Smartphone subscriptions increased by 40 percent in 2013 to reach 2.6

billion. This number is expected to rise to 5.6 billion by 2019. Emerging

markets, especially China and India, provide most of the growth as many

people buy their 1rst smartphone.

Source: CNET News, November 11, 2013

a. Explain the eAects of the increase in global demand for smartphones on the

market for smartphones and on an individual smartphone producer in the

short run.

In the short run the market demand for smartphones increases. The price of a

b. Draw a graph to illustrate your explanation in part (a).

Figure 12.5 shows the short-run outcome. Figure 12.5a shows the market

equilibrium. In the market, demand increases and the demand curve shifts

rightward from D0 to D1. In the short run the supply curve remains S0. As a result

c. Explain the long-run eAects of the increase in global demand for

smartphones on the market for smartphones.

In the long run the economic pro1t attracts entry into the market. The market

supply increases which drives the price down. The market equilibrium quantity