IV. Output, Price, and Prot in the Long Run

In the short run, a rm might break even, earn an economic prot or incur a loss. Because

of entry and exit, in the long run a rm can only break even.

Entry

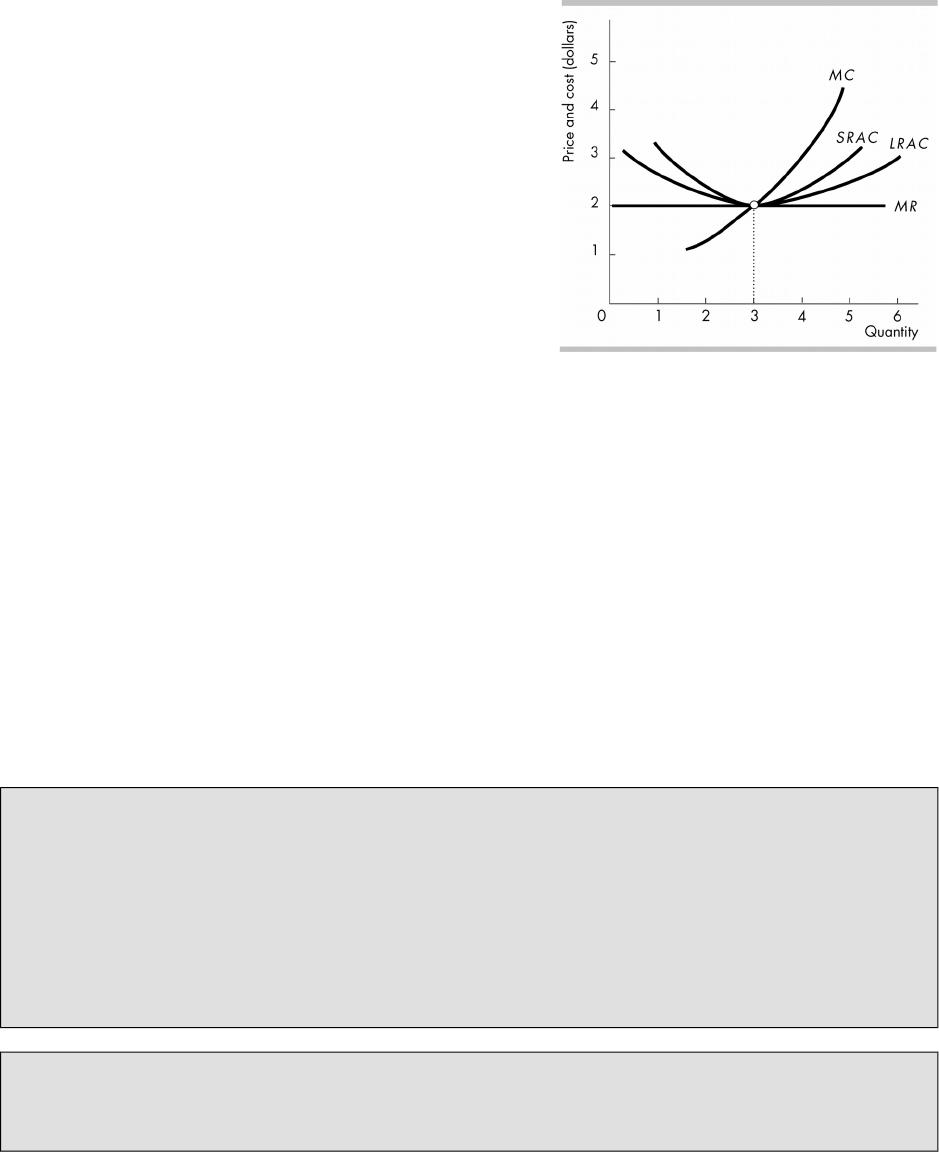

Economic prot motivates rms to enter the

industry, thereby increasing the market

supply.

When the market supply curve shifts

rightward, the market price falls. Eventually

the price falls to equal the minimum ATC for

each rm in the industry and rms have

adjusted their plant size so they are

producing at the minimum long-run average

cost. At this price, rms in the industry no

longer make an economic prot and so rms

no longer enter the industry. The gure

illustrates this long-run equilibrium. In the

gure, LRAC is the long-run average cost

curve and SRAC is the short-run average

cost curve.

One di(erence between the old and new market equilibriums is that the number of

rms in the industry has risen and total quantity produced in the industry has

increased.

Exit

The e(ects of a decrease in market demand are the opposite of those outlined

above.

In the long run, competitive rms make zero economic prot (price = average total

cost) so that their owners make a normal prot.

Long Run Equilibrium

Long run equilibrium in a competitive market occurs when there is zero economic

prot and entry and exit have stopped.

Because markets are constantly experiencing new changes and shocks, it is rare to

see one in a state of long-run equilibrium, but each competitive markets reacts to

any new changes by pushing toward it.

Prot as a “signal”: When demand for a good increases so that the existing rms in an

industry make an economic prot, the economic prot indicates that consumers are willing

to pay a higher price for the good than they were willing to pay before the demand

increased. The economic prot for the rms is a signal from the consumers to the owners

of rms in other industries that society now values the availability of the good more highly

than the availability of goods from those other industries. These self-interested rm owners

choose to enter the industry in order to make an economic prot. Their self-interested

decisions promote the social interest by using more resources to produce those goods that

are more highly valued by society. The dynamic behavior of a perfectly competitive market

characterizes the “invisible hand” coined by Adam Smith.

Why would a rm stay in business if prot is zero? It is likely that you will hear this

question from at least one of your students. Remind them that the prot we’re measuring

is economic prot. Zero economic prot doesn’t necessarily mean that the rm isn’t

making any money. Rather, zero economic prot means that the prots the accountant is

© 2016 Pearson Education, Inc.

P E R F E C T C O M P E T I T I O N 1 2 3

reporting is exactly the same as the value of the rm’s best alternative. If the rm were to

move to its best alternative, it would make the same amount of prot. If a rm is making

zero economic prot, there isn’t any incentive to go anywhere else as there isn’t any place

that would generate a higher return for the rm. You may need to continue reminding your

students of this throughout this chapter.

An Economics in Action feature examines entry and exit using the personal computer

market and the farm equipment market.

V. Changes in Demand and Supply as Technology Advances

Change in Demand

Technological change can increase demand if it creates new applications for a

product or new products. Technological change can also decrease demand if new

ways of doing things or new products displace previous ones.

If demand increases, the price and economic prot rise. The economic prot

leads to entry, which increases market supply and causes the price to fall so that

eventually rms again make zero economic prot. The number of rms is greater

than before the increase in demand.

If demand decreases, the price falls and economic losses are created. Firms exit

the market, which raises the price and decreases the remaining rms’ economic

losses. Eventually the price rises so that the surviving rms make zero economic

prot. The number of rms is less than before the decrease in demand.

An Economics in the News case explores the e(ects of a decrease in demand for records

and taped music

Change in Supply

New, cost-saving technologies typically require new plant and equipment.

Consequently it takes time for new technology to spread throughout an industry.

Firms that adopt the new technology lower their costs and their supply curves shift

rightward. The price of the good falls but the rms with the new technology make an

economic prot.

Firms using the old technology incur economic losses. These rms either adopt the

new technology or else exit the industry. In the long run, all the rms use the new

technology and make zero economic prot.

Changes in technology brings only temporary economic prot to producers, but the

lower prices and better products that technological advances bring are permanent

gains for consumers.

An Economics in the News case explores the implications of technological changes that

have created falling costs to sequence DNA.

Do rms in perfectly competitive markets advertise? Firms in perfectly competitive

markets have no incentive to advertise because their product is indistinguishable from the

output of rival rms. Industry associations will sometimes advertize to increase demand for

the product as a whole. Brainstorming all the ads for agricultural products such as “Pork:

the other white meat,” and all the varieties of milk ads can be fun, but the point is that it

isn’t a pork producer or a dairy farmer creating the ad, but all of the pork producers or

dairy farmers paying dues to an industrial organization that then creates the ads.

Successful advertisements might lead to an economic prot in the short run, but in the

long run entry will force the rms back to zero economic prot.

© 2016 Pearson Education, Inc.

1 2 4 C H A P T E R 1 2

VI. Competition and E’ciency

Ecient Use of Resources

Resource allocation in a market is eAcient when society values no other use of the

resources more highly. Resource use is eAcient when production is such that the

marginal social benet of the good equals the marginal social cost of the good.

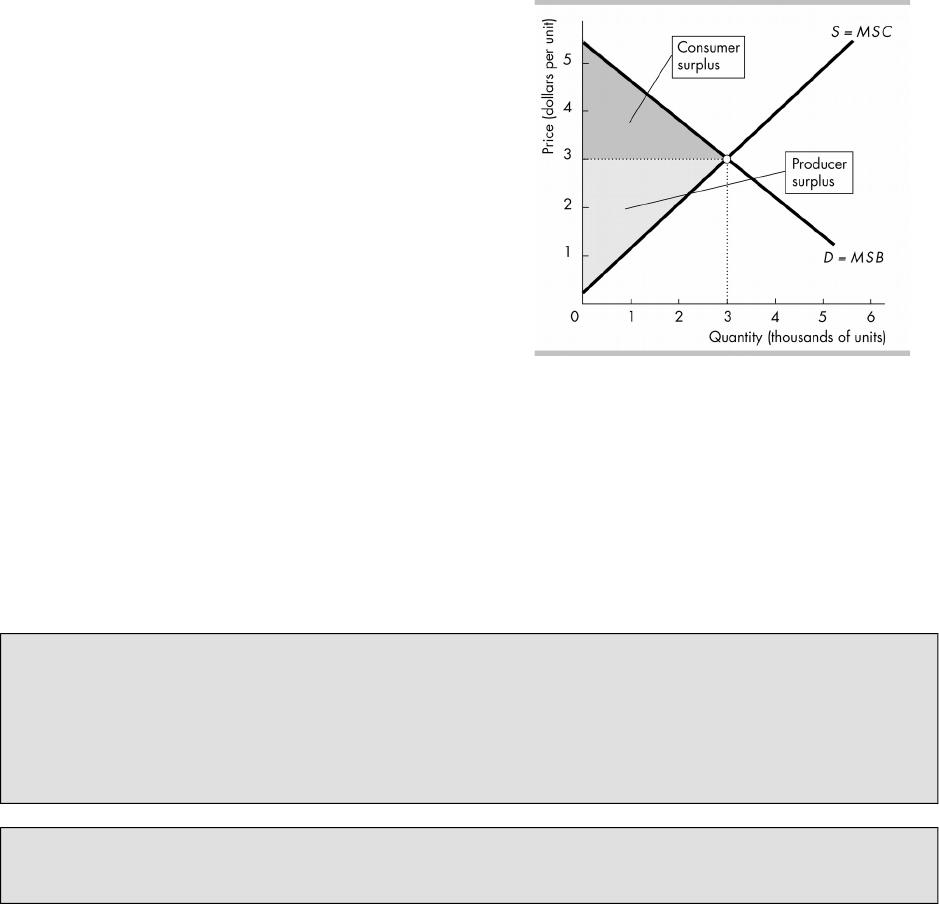

Choices, Equilibrium, and Eciency

Consumers allocate their budgets to get

the most value out of them. Because

consumers get the most value out of their

budget, a consumer’s individual demand

curve for a good is the consumer’s

marginal benet curve for the good. If no

one else benets from the good other than

the consumers, then, as shown on the

gure, the market demand curve for a

good is the marginal social benet curve.

Firms maximize their prots in order to get

the most value out of their resources.

Firms make choices across all possible

allocations of their resources. A rm’s

supply curve for a good is its marginal

cost curve. If all the costs of production of

the good are paid by the producers, then, as shown in the gure, the market supply

curve for a good is the marginal social cost curve.

In a competitive equilibrium, the quantity demanded equals the quantity supplied. If

there are no externalities, the demand curve is the same as the marginal social

benet curve and the supply curve is the same as the marginal social cost curve, so

at the competitive equilibrium, the marginal social benet equals the marginal

social cost. Resource use is eAcient. Because resources are used eAciently, at the

competitive equilibrium there is no other allocation of resources that will generate

greater net benets to society. The gure shows this outcome, where resource use is

eAcient at the equilibrium quantity of 3,000 units.

Watching the work of the invisible hand: The power of the market to make rms

respond to consumers’ changing demands becomes visible to the student in this chapter.

When you teach the dynamics of rm entry and exit, do the analysis with a specic (and

current) example with which the students can identify. Have them pick an industry that has

grown and largely died in their lifetime (for me, VCRs, for them, DVDs at Blockbuster, or

video cameras or lm cameras). What has replaced it and how is society served by failure

as well as success?

Economics in the News analyzes the market for smart phone apps. It explains how the

rapid expansion of smartphones increased the demand for apps, thereby bring economic

prots to app producers.

© 2016 Pearson Education, Inc.

P E R F E C T C O M P E T I T I O N 1 2 5

Additional Problems

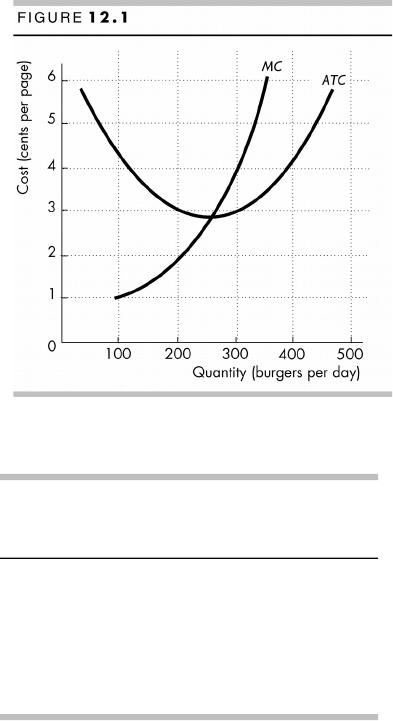

1. Bob’s is one of many burger stands along

the beach. Figure 12.1 shows Bob’s cost

curves.

a. If the market price of a burger is $4, what

is Bob’s prot-maximizing output?

b. Calculate the economic prot that Bob’s

makes.

c. With no change in demand or technology,

how will the price change in the long run?

2. Lucy’s Lasagna is a price taker that has

the costs shown in the table.

a. If lasagna sells for $7.50 a plate, what is

Lucy’s prot-maximizing output?

b. What is Lucy’s shutdown point?

c. Over what price range will Lucy leave the

lasagna industry?

d. Over what price range will other rms

with costs identical to Lucy’s enter the

industry?

e. What is the price of lasagna in the long run?

S o l u t i o n s t o A d d i t i o n a l P r o b l e m s

1. a. Bob’s prot-maximizing quantity is 300 burgers a day. Bob’s maximizes its prot by

producing the quantity at which marginal revenue equals marginal cost. In perfect

competition, marginal revenue equals price, which is $4 a burger. Marginal cost is $4

when 300 burgers a day are produced.

b. Bob’s economic prot is $300 a day. Prot equals total revenue minus total cost.

Total revenue equals $1,200 a day ($4 a burger multiplied by 300 burgers). The

average total cost of producing 300 burgers is $3.00 a burger, so total cost equals

$900 a day ($3.00 multiplied by 300 burgers). Prot equals $1,200 minus $900,

which is $300 a day.

c. The price will fall in the long run to $2.80 a burger. At a price of $4 a burger, rms

make economic prot. In the long run, the economic prot will encourage new rms

to enter the burger industry. As they do, the price will fall and economic prot will

decrease. Firms will enter until economic prot is zero, which occurs when the price

is $2.80 a burger (price equals minimum average total cost).

© 2016 Pearson Education, Inc.

Output

(plates per

hour)

Total cost

(dollars per

hour)

0 5

1 20

2 26

3 35

4 46

5 59

1 2 6 C H A P T E R 1 2

2. a. Lucy’s prot-maximizing output is 2 plates an hour. Lucy’s maximizes its prot by

producing the quantity at which marginal revenue equals marginal cost. In perfect

competition, marginal revenue equals price, which is $7.50 a plate. Marginal cost is

the change in total cost when output is increased by 1 plate an hour. The marginal

cost of increasing output from 1 to 2 plates an hour is $6 ($26 minus $20). The

marginal cost of increasing output from 2 to 3 plates an hour is $9 ($35 minus $26).

So the marginal cost of the second plate is half-way between $6 and $9, which is

$7.50. Marginal cost equals marginal revenue when Lucy produces 2 plates an hour.

b. Lucy’s shutdown point is at a price of $10 a plate. The shutdown point is the price

that equals minimum average variable cost. To calculate total variable cost, subtract

total xed cost ($5, which is total cost at zero output) from total cost. Average

variable cost equals total variable cost divided by the quantity produced. For

example, the average variable cost of producing 3 plates is $10 a plate. Average

variable cost is a minimum when marginal cost equals average variable cost. The

marginal cost of producing 3 plates is $10. So the shutdown point is a price of $10 a

plate.

c. Lucy will leave the industry if in the long run the price is less than $11 a plate. Lucy’s

Lasagna will leave the industry if it incurs an economic loss in the long run. To incur

an economic loss, the price will have to be below minimum average total cost.

Average total cost equals total cost divided by the quantity produced. For example,

the average total cost of producing 2 plates is $13 a plate. Average total cost is a

minimum when it equals marginal cost. The average total cost of producing 3 plates

is $11.67, and the average total cost of producing 4 plates is $11.50. Marginal cost

when Lucy’s produces 3 plates is $10 and marginal cost when Lucy’s produces 4

plates is $12. At 3 plates, marginal cost is less than average total cost; at 4 plates,

marginal cost exceeds average total cost. So minimum average total cost occurs

between 3 and 4 plates—$11 at 3.5 plates an hour.

d. Firms with costs identical to Lucy’s will enter at any price above $11 a plate. Firms

will enter an industry when rms currently in the industry are making economic

prot. Firms with costs identical to Lucy’s will make economic prot when the price

exceeds minimum average total cost, which is $11 a plate.

e. The price in the long run is $11 a plate. At $11 a plate, rms in the industry make

zero economic prot.

A d d i t i o n a l D i s c u s s i o n Q u e s t i o n s

1. Why do rms do what they do? Students should see how a clear

understanding of a perfectly competitive market justies rm behavior that

otherwise might appear somewhat peculiar:

Late night TV is full of zany TV commercials with rm owners who claim “I

must be crazy, because I’m losing money on every sale!” Why do they

advertise to increase sales if they’ll cause the owner to lose even more

money? At rst, it appears that these owners must be lying about “losing

money on every sale.” Yet their unlikely claim is potentially true, as the various

rms in their industry may currently face a market price above AVC, but below

ATC in the short run. In this case they would remain in business and continue

advertising, despite “losing money on every sale” because they are earning

revenues above their variable costs to at least help contribute toward paying

their xed cost obligations to their creditors.

Why do the same farmers always complain of losing money but never

seem to exit the industry? Point out that agriculture is a collection of highly

competitive markets where farming operations typically have an extremely

© 2016 Pearson Education, Inc.

P E R F E C T C O M P E T I T I O N 1 2 7

high capital-to-labor ratio. This fact makes the typical farm’s ratio of xed

costs to variable costs very high relative to most industries. Also, much of a

farmer’s capital is in the form farmland, which is diAcult to sell during falling

agriculture prices, lengthening the farmer’s short run time frame. In this case,

the dollar di(erence between market price and minimum AVC will be rather

large. As long as market price exceeds AVC, the farmer will minimize losses by

continuing to produce output over an extended short run time frame.

2. What is implied about e$ciency if the average cost of producing a

good exceeds the price people are willing to pay for it? Remind the

students that a rm’s cost curves reOect the opportunity cost to society of the

rm using the resources to make the goods in its market (the resources could

be making goods in some other market that could bring benets to society).

The demand curve reOects the value society places on each quantity of goods

produced. If the price people are willing to pay is determined by the market

supply and demand and the going market price is less than the opportunity

cost of producing the last unit of the good, using more resources to increase

output creates fewer net benets for society than could be generated if the

resources were used elsewhere in other markets.

What happens to the resources that were used by a rm for

production when that rm exits the industry? Point out that when price

falls below ATC, this generates an economic loss for the rm. This is a signal

from a society of consumers to the owner of the resources that he or she will

benet from reallocating the resources to making di(erent goods and services

from the same resources. Society also stands to benet from this switch.

How can an increase in net benets to society be generated from the

systematic destruction of rms leaving the market? A famous economist

named Joseph Schumpeter coined the phrase “creative destruction” to

describe the dynamics of a competitive market. While the productive capacity

of a perfectly competitive industry facing declining consumer demand is

ultimately destroyed, the resources themselves are not destroyed. They are

simply released to rms in other markets to create goods and services that are

relatively more valuable to society. This “destruction” of an industry creates

goods of greater social value in another industry. That is Schumpeter’s

“creative destruction.”

3. What makes all the self-interested rms adopt the latest available

technology for producing at the lowest opportunity cost possible over

time? Emphasize that competitive rms cannot increase their economic

prots by raising their price, so they must search for ways to increase

economic prot through lowering production costs. This means that rms are

constantly seeking out the latest production technologies to nd a cost

advantage over their competitors. If the other rms failed to adopt this

low-cost production technology, they would su(er an economic loss when

those that do adopt the technology lower their prices to increase market share.

Firms that refuse to adopt the technology must then match a lower market

price to retain their market shares, causing them to bear an economic loss and

face an eventual exit from the market.

4. Discuss whether there are economies of scale or diseconomies of

scale in class size at colleges and universities. Does it matter if the

“output” is measured in tuition dollars and costs or in student

success as measured by grades? Does technology impact the answer?

This situation can be fun to explore. Can a great teacher supported by

excellent technology be best used in a huge lecture class? Are there some

© 2016 Pearson Education, Inc.

1 2 8 C H A P T E R 1 2

types of instruction, like experimental labs, where increasing class size might

lead to disaster? Why do colleges advertise their average class size and do

parents and students care? How might the educational “plant” and equipment

di(er to support various choices in class size?

5. Using the global corn market, consider the impact of increasing

demand for ethanol made from corn in the short and long run. The

increase in demand for ethanol raises the price of corn and thereby increases

corn farmers’ economic prot…at least in the short run. But in the long run,

the economic prot leads existing farmers to plant more corn and more corn

farmers to enter the. These long-run changes increase the supply of corn,

thereby lowering the price of corn and decreasing corn farmers’ economic

prot. Entry (and expansion) continues until, in the long run, corn farmers’

economic prot equals zero. At that point entry ceases and the corn market is

back in long-run equilibrium.

© 2016 Pearson Education, Inc.

P E R F E C T C O M P E T I T I O N 1 2 9