Chapter 19

ANSWERS TO QUESTIONS

1. How would you expect velocity to typically behave over the course of the business cycle?

2. If velocity and aggregate output are reasonably constant (as the classical economists

believed), what will happen to the price level when the money supply increases from $1

trillion to $4 trillion?

3. If credit cards were made illegal by congressional legislation, what would happen to

velocity? Explain your answer.

4. “If nominal GDP rises, velocity must rise.” Is this statement true, false, or uncertain?

Explain your answer.

5. Why would a central bank be concerned about persistent, long-term budget deficits?

6. “Persistent budget deficits always lead to higher inflation.” Is this statement true, false, or

uncertain? Explain your answer.

7. Suppose a new “payment technology” allows individuals to make payments using U.S.

8. Some payment technologies require infrastructure (e.g., merchants need to have access to

credit card swiping machines). In most developing countries, this infrastructure is either

nonexistent or very costly. Everything else being equal, would you expect the transaction

component of the demand for money to be greater or smaller in a developing country than in

a rich country?

9. What three motives for holding money did Keynes consider in his liquidity preference theory of

the demand for real money balances? On the basis of these motives, what variables did he

think determined the demand for money?

The three motives are: precautionary, speculative, and transactions motives. From these three

10. In many countries, people hold money as a cushion against unexpected needs arising from a

variety of potential scenarios (e.g., banking crises, natural disasters, health problems,

unemployment, etc.) that are not usually covered by insurance markets. Explain the effect of

such behavior on the precautionary component of the demand for money.

11. In Keynes’s analysis of the speculative demand for money, what will happen to money

demand if people suddenly decide that the normal level of the interest rate has fallen? Why?

12. Why is Keynes’s analysis of the speculative demand for money important to his view that

velocity will undergo substantial fluctuations and thus cannot be treated as constant?

13. According to the portfolio theories of money demand, what are the four factors that

determine money demand? What changes in these factors can increase the demand for

money?

The four factors determining money demand under portfolio theory are: interest rates

14. Explain how the following events will affect the demand for money according to the portfolio

theories of money demand:

a. The economy experiences a business cycle contraction.

b. Brokerage fees decline, making bond transactions cheaper.

c. The stock market crashes. (Hint: Consider both the increase in stock price volatility

following a market crash and the decrease in wealth of stockholders.)

15. Suppose a given country experienced low and stable inflation rates for quite some time, but

then inflation picked up and over the past decade has been relatively high and quite

unpredictable. Explain how this new inflationary environment would affect the demand for

money according to portfolio theories of money demand. What would happen if the

government decided to issue inflation-protected securities?

16. Consider the portfolio choice theory of money demand. How do you think the demand for

money would be affected during a hyperinflation (i.e., monthly inflation rates in excess of

50%)?

The demand for money would decrease, similar to problem 15 above, but much more

17. Both the portfolio choice and Keynes’s theories of the demand for money suggest that as the

relative expected return on money falls, demand for it will fall. Why does the portfolio choice

approach predict that money demand is affected by changes in interest rates? Why did

Keynes think that money demand is affected by changes in interest rates?

18. Why does the Keynesian view of the demand for money suggest that velocity is unpredictable?

19. What evidence is used to assess the stability of the money demand function? What does the

evidence suggest about the stability of money demand, and how has this conclusion affected

monetary policymaking?

20. Suppose that a plot of the values of M2 and nominal GDP for a given country over 40 years

shows that these two variables are very closely related. In particular, a plot of their ratio

(nominal GDP/M2) yields very stable and easy-to-predict values. On the basis of this

evidence, would you recommend that the monetary authorities of this country conduct

monetary policy by focusing mostly on the money supply rather than on setting interest

rates? Explain.

ANSWERS TO APPLIED PROBLEMS

21. Suppose the money supply M has been growing at 10% per year, and nominal GDP, PY, has

been growing at 20% per year. The data are as follows (in billions of dollars):

2015

2016

2017

M

100

110

12

PY

1,000

1,200

1,440

Calculate the velocity for each year. At what rate is the velocity growing?

Velocity is approximately 10 in 2015, 10.9 in 2016, and 11.9 in 2017. The rate of velocity

growth is approximately 9% per year.

22. Calculate what happens to nominal GDP if velocity remains constant at 5 and the money

supply increases from $200 billion to $300 billion.

23. What happens to nominal GDP if the money supply grows by 20% but velocity declines by

30%?

24. If velocity and aggregate output remain constant at 5 and $1,000 billion, respectively, what

happens to the price level if the money supply declines from $400 billion to $300 billion?

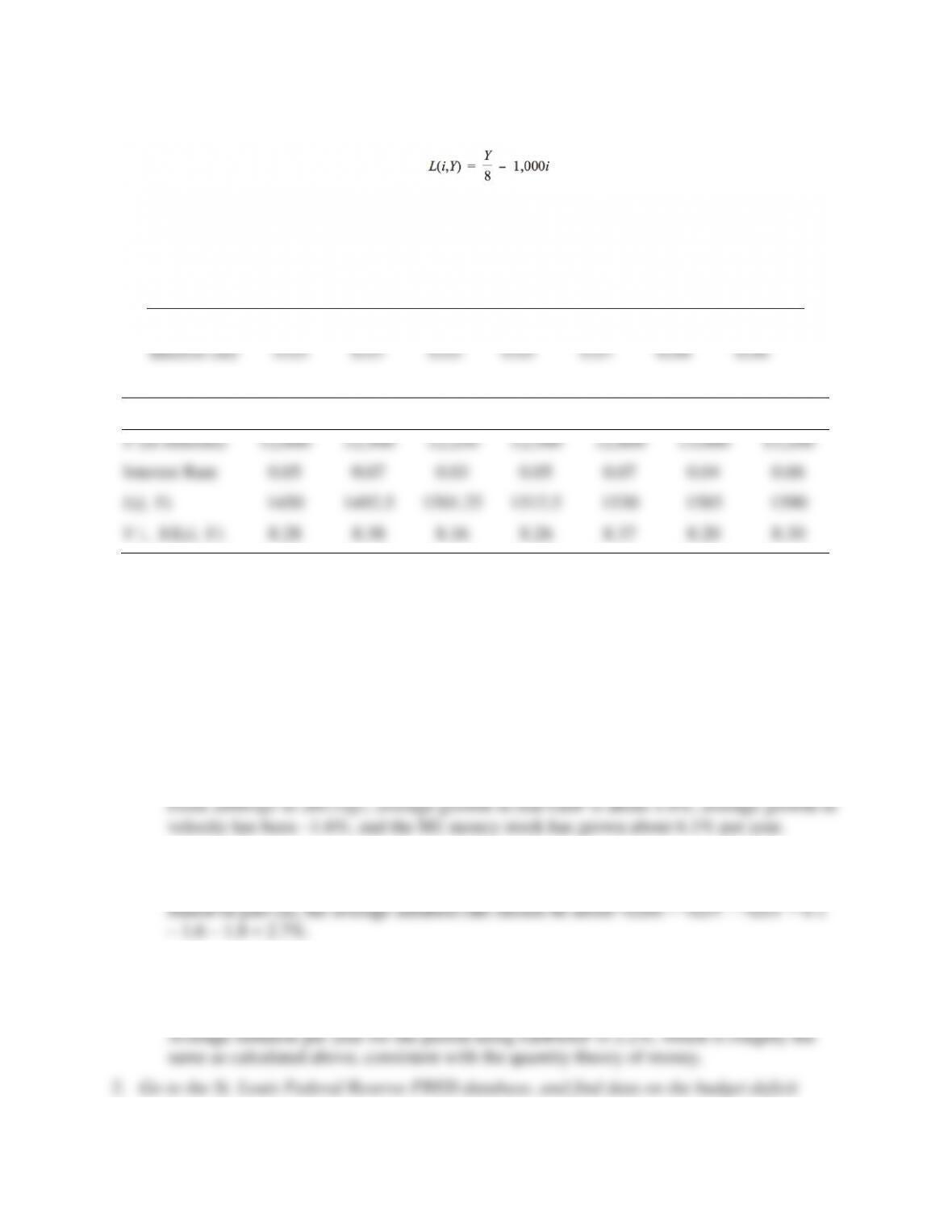

25. Suppose the liquidity preference function is given by

Use the money demand equation, along with the following table of values, to calculate the

velocity for each period.

Period

1

Period

2

Period

3

Period

4

Period

5

Period

6

Period

7

Y (in billions)

12,000

12,500

12,250

12,500

12,800

13,000

13,200

Interest rate

0.05

0.07

0.03

0.05

0.07

0.04

0.06

Period 1

Period 2

Period 3

Period 4

Period 5

Period 6

Period 7

Y (in billions)

12,000

12,500

12,250

12,500

12,800

13,000

13,200

Interest Rate

0.05

0.07

0.03

0.05

0.07

0.04

0.06

L(i, Y)

1450

1492.5

1501.25

1512.5

1530

1585

1590

V Y/L(i, Y)

8.28

8.38

8.16

8.26

8.37

8.20

8.30

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database, and find data on the M1 Money Stock

(M1SL), M1 Money Velocity (M1V), and Real GDP (GDPC1). Convert the M1SL data series

to “quarterly” using the frequency setting, and for all three series, use the “Percent Change

from Year Ago” setting for units.

a. Calculate the average percentage change in real GDP, the M1 money stock, and velocity

since 2000:Q1.

b. Based on your answer to part (a), calculate the average inflation rate since 2000 as

predicted by the quantity theory of money.

c. Next, find the data on the GDP deflator price index (GDPDEF), download the data using

the ‘Percent Change from Year Ago’ setting, and calculate the average inflation rate

since 2000:Q1. Comment on the value relative to your answer in part (b).

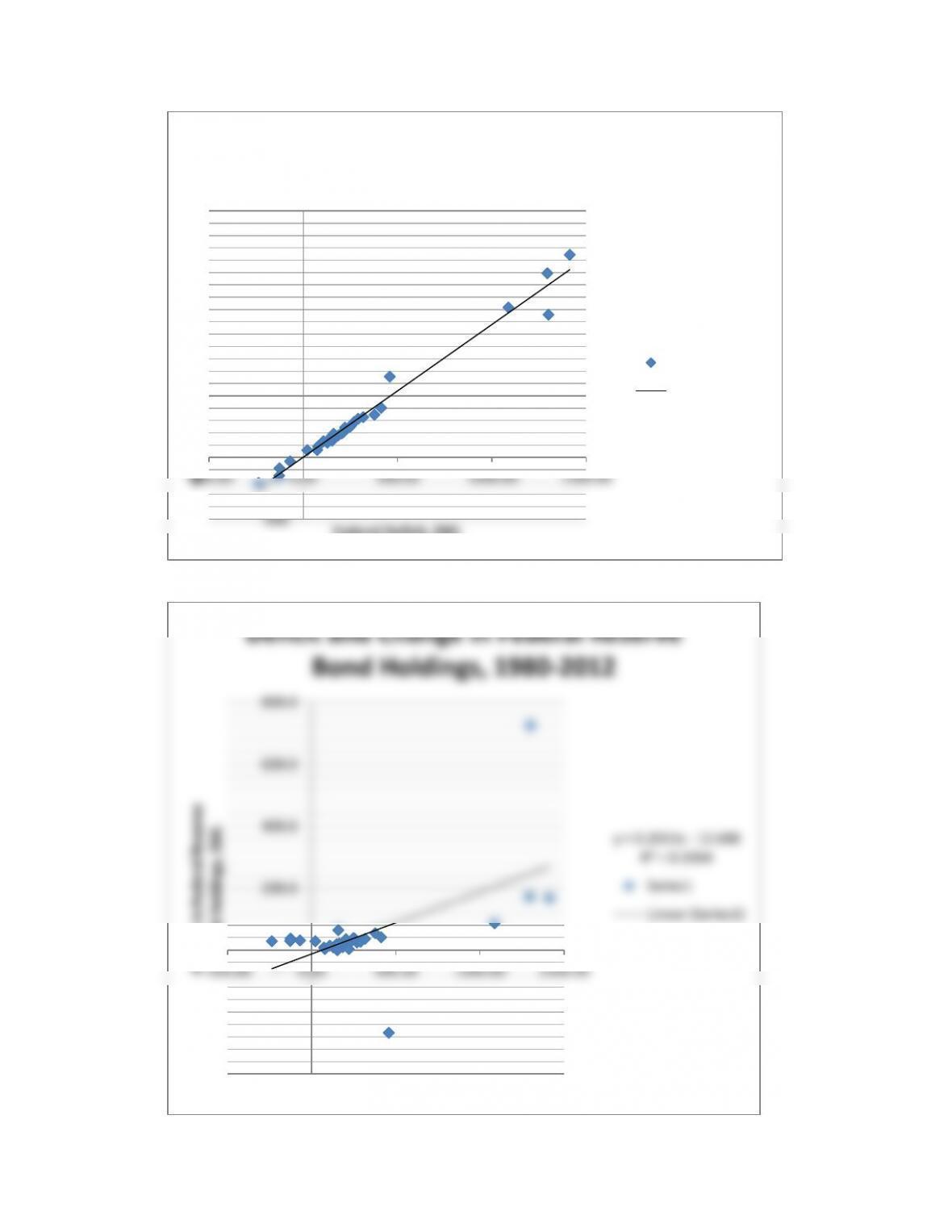

(FYFSD), the amount of federal debt held by the public (FYGFDPUN), and the amount of

federal debt held by the Federal Reserve (FDHBFRBN). Convert the two “debt held” series

a. Create a scatter plot showing the deficit on the horizontal axis and the change in bond

holdings by the public on the vertical axis, using the data from 1980 through the most

recent period of data available. Insert a fitted line into the scatter plot, and comment on

the relationship between the deficit and the change in public bond holdings.

b. Create a scatter plot showing the deficit on the horizontal axis and the change in bond

the most recent period of data available. Insert a fitted line into the scatter plot, and

comment on the relationship between the deficit and the change in Federal Reserve bond

holdings.

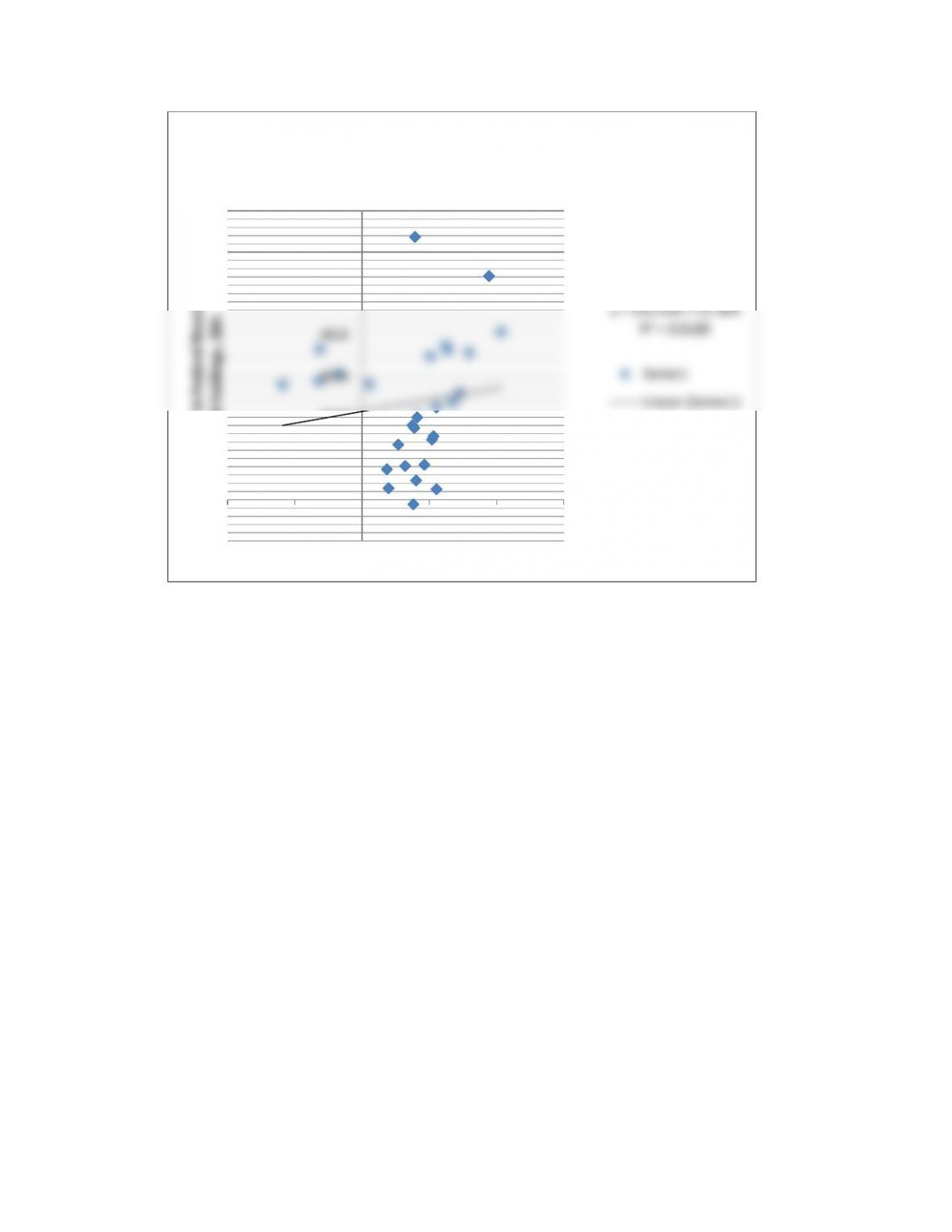

c. Based on your results in parts (a) and (b), comment on how, if at all, the monetizing of

the debt is exhibited in the data. Do you think the relationship between the deficit and the

change in bond holdings of the Federal Reserve has changed since 2008? Why or why

not?

There appears to be some amount of debt monetization in the scatterplot data: in general,

as the deficits get larger, the change in bond holdings by the Fed gets larger, indicating

the central bank is facilitating higher deficits. However, this appears to be driven by the

large outlier deficits in the 2008 – 2012 period. Removing these data show a much

running very large deficits.

y = 1.0767x + 1.8904

R² = 0.9784

-500

0

500

1000

1500

2000

-500.00 0.00 500.00 1000.00 1500.00

Change in Public Bond Holdings, $Bil.

Federal Deficit, $Bil.

Deficit and Change in Public Bond

Holdings, 1980-2012

Series1

Linear (Series1)

-400.0

800.0

Deficit and Change in Federal Reserve

Bond Holdings, 1980-2012

y = 0.0143x + 21.409

R² = 0.0185

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

-400.00 -200.00 0.00 200.00 400.00 600.00

Change in Federal Reserve

Bond Holdings, $Bil.

Federal Deficit, $Bil.

Deficit and Change in Federal Reserve

Bond Holdings, 1980 – 2007

Series1

Linear (Series1)