Chapter 10

ANSWERS TO QUESTIONS

1. Why are deposit insurance and other types of government safety nets important to the health

of the economy?

2. If casualty insurance companies provided fire insurance without any restrictions, what kind

of adverse selection and moral hazard problems might result?

3. Do you think that eliminating or limiting the amount of deposit insurance would be a good

idea? Explain your answer.

4. How could higher deposit insurance premiums for banks with riskier assets benefit the

economy?

5. What are the costs and benefits of a too-big-to-fail policy?

6. What types of bank regulations are designed to reduce moral hazard problems? Will they

completely eliminate moral hazard problems?

7. Why does imposing bank capital requirements on banks help limit risk taking?

8. At the height of the global financial crisis in October 2008, the U.S. Treasury forced nine of

the largest U.S. banks to accept capital injections in exchange for nonvoting ownership

stock, even though some of the banks did not need the capital and did not want to participate.

What could be the Treasury’s rationale for doing this?

9. What special problem do off-balance-sheet activities present to bank regulators, and what

have they done about it?

10. What are some of the limitations to the Basel and Basel 2 Accords? How does the Basel 3

Accord attempt to address these limitations?

11. How does bank chartering reduce adverse selection problems? Does it always work?

12. Why has the trend in bank supervision moved away from a focus on capital requirements to a

focus on risk management?

make sure that banks are not taking on too much risk, bank supervisors now are focusing

more on whether the risk-management procedures in banks keep them from excessive risk

13. How do disclosure requirements help limit excessive risk taking by banks?

14. Suppose Universal Bank holds $100 million in assets, which are composed of the following:

Required reserves: $10 million

a. Do you think it is a good idea for Universal Bank to hold stocks, corporate bonds, and

commodities as assets? Why or why not?

c. If the price of commodities suddenly increased sharply, would Universal Bank be better

off using a mark-to-market accounting system or the historical-cost system?

d. What do your answers to parts (b) and (c) tell you about the tradeoffs between the two

accounting systems?

15. Why might more competition in financial markets be a bad idea? Would restrictions on

competition be a better idea? Why or why not?

ANSWERS TO APPLIED PROBLEMS

16. Consider a failing bank. How much is a deposit of $350,000 worth if the FDIC uses the

payoff method? The purchase and assumption method? Which method is more costly to

taxpayers?

$350,000 is worth better than $350,000 purchase and

assumption policy, the bank is completely absorbed, and all accounts are worth their full

value. Upfront, the first method will have a lower cost to the insurance fund. However, if

17. Consider a bank with the following balance sheet:

Assets

Liabilities

Required Reserves

$8 million

Checkable deposits

$100 million

Excess reserves

$3 million

Bank capital

$6 million

T-bills

$45 million

Commercial loans

$50 million

e the loan commitment is

not an accounting transaction yet, the capital ratio is the same after.

Before, the loan commitment, for risk-weighted assets:

18. Oldhat Financial starts its first day of operations with $9 million in capital. A total of $130

million in checkable deposits is received. The bank makes a $25 million commercial loan and

another $50 million in mortgages with the following terms: 200 standard, 30-year, fixed-rate

mortgages with a nominal annual rate of 5.25%, each for $250,000. Assume that required

reserves are 8%.

a. What does the bank balance sheet look like?

Assets

Liabilities

Required Reserves

$10.4 million

Checkable Deposits

$130 million

Excess Reserves

$53.6 million

Bank Capital

$ 9 million

Loans

$75 million

b. How well capitalized is the bank?

c. Calculate the risk-weighted assets and risk-weighted capital ratio after Oldhat’s first

day.

Reserves have a zero weight. So, $64 million has zero weight. Residential mortgages

19. Early the next day, the bank invests $50 million of its excess reserves in commercial loans.

Later that day, terrible news hits the mortgage markets, and mortgage rates jump to 13%,

implying a present value of Oldhat’s current mortgage holdings of $124,798 per mortgage.

Bank regulators force Oldhat to sell its mortgages to recognize the fair market value. What

does Oldhat’s balance sheet look like? How do these events affect its capital position?

The sale of each mortgage would be recorded as:

Debit

Credit

Cash

$124,798

Mortgages

$250,000

Loss

$125,202

Assets

Liabilities

Required Reserves

$10.4 million

Checkable Deposits

$130 million

Excess Reserves

$28.6 million

Bank Capital

Loans

$75 million

20. To avoid insolvency, regulators decide to provide the bank with $25 million in bank capital.

However, the bad news about the mortgages is featured in the local newspaper, causing a

bank run. As a result, $30 million in deposits is withdrawn. Show the effects of the capital

injection and the bank run on the balance sheet. Was the capital injection enough to stabilize

the bank? If the bank regulators decide that the bank needs a capital ratio of 10% to prevent

further runs on the bank, how much of an additional capital injection is required to reach a

10% capital ratio?

Assets

Liabilities

Required Reserves

$ 8 million

Checkable Deposits

$100 million

Excess Reserves

$26 million

Bank Capital

$ 9 million

Loans

$75 million

ratio.

ANSWERS TO DATA ANALYSIS PROBLEMS

1. Go to the St. Louis Federal Reserve FRED database, and find data on the number of

commercial banks in the U.S. in each of the following categories: average assets less than

$100 million (US100NUM), average assets between $100 million and $300 million

(US13NUM), average assets between $300 million and $1 billion (US31NUM), average

assets between $1 billion and $15 billion (US115NUM), and average assets greater than $15

billion (USG15NUM). Download the data into a spreadsheet. Calculate the percentage of

banks in the smallest (less than $100 million) and largest (greater than $15 billion)

categories, as a percentage of the total number of banks, for the most recent quarter of data

available and for 1990:Q1. What has happened to the proportion of very large banks? What

has happened to the proportion of very small banks? What does this say about the “too-big-

to–fail” problem and moral hazard?

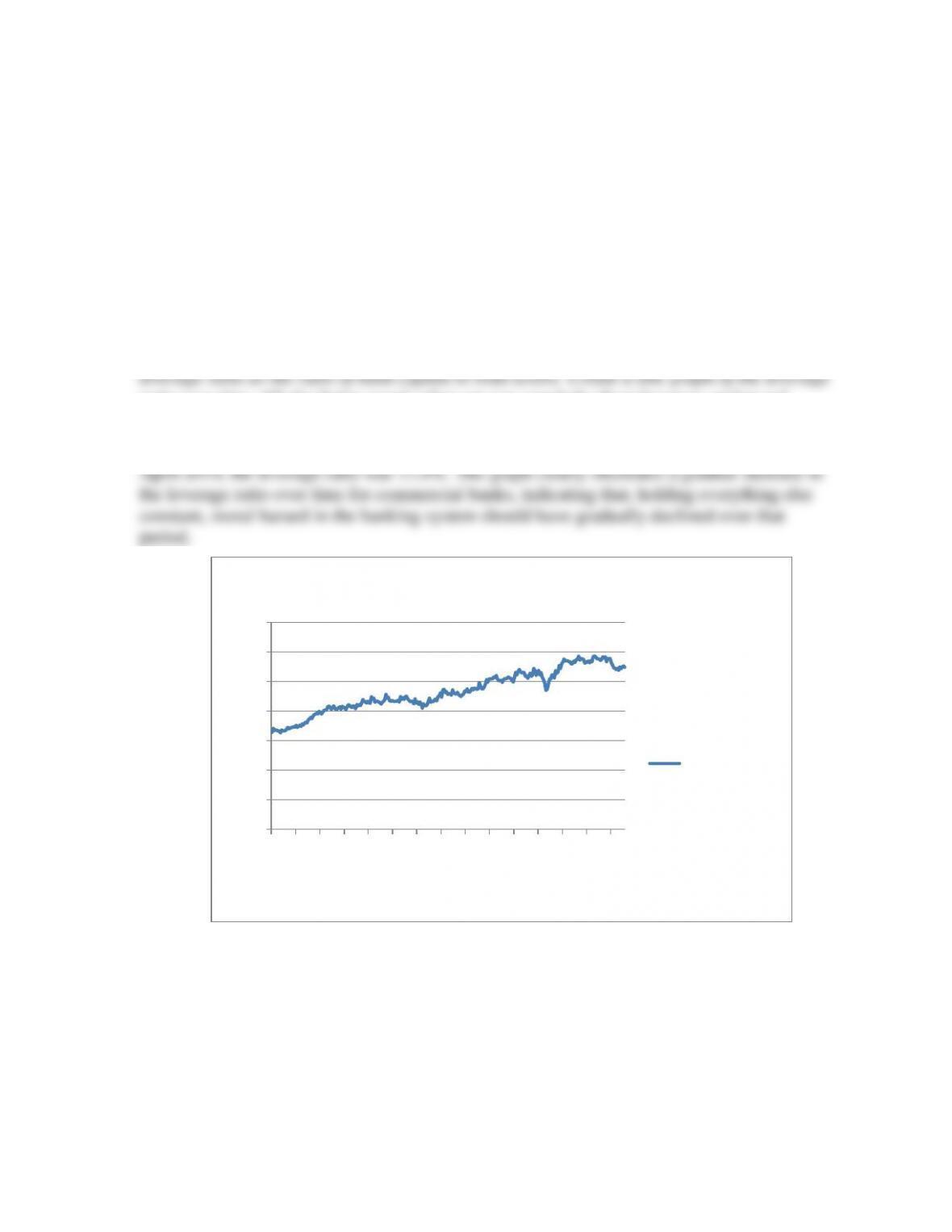

2. Go to the St. Louis Federal Reserve FRED database, and find data on the residual of assets

less liabilities, or bank capital (RALACBM027SBOG), and total assets of commercial banks

(TLAACBM027SBOG). Download the data from January 1990 through the most recent

month available into a spreadsheet. For each monthly observation, calculate the bank

ratio over time. All else being equal, what can you conclude about leverage and moral

hazard in commercial banks over time?

See graph below. In January 1990, the leverage ratio was 6.6%, and the most recent month of

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1990-01-01

1991-09-01

1993-05-01

1995-01-01

1996-09-01

1998-05-01

2000-01-01

2001-09-01

2003-05-01

2005-01-01

2006-09-01

2008-05-01

2010-01-01

2011-09-01

2013-05-01

Leverage Ratio

Leverage Ratio