Chapter 7. The Labor Market

I. MOTIVATING QUESTION

How is the unemployment rate determined in the medium run?

In the medium run, the unemployment rate tends to return to the so-called natural rate, determined by

equilibrium in the labor market when the expected price level equals the actual price level. Conditional

on price level expectations, equilibrium in the labor market occurs when the real wage implied by

wage-setting behavior (influenced by the relative bargaining power of workers and firms) equals the real

wage implied by price-setting behavior (influenced by the degree of competition in the goods market).

II. WHY THE ANSWER MATTERS

The analytical framework in the text is built around equilibrium in three markets: goods, financial, and

labor. Following the approach of Chapters 3 and 4, this chapter begins the discussion of the labor market

by considering it in isolation. The assumption that isolates the labor market from the other markets is that

the expected price level equals the actual price level. In these circumstances, the framework presented in

the book produces an equilibrium rate of unemployment and an equilibrium real wage, independent of the

goods and financial markets. Unlike the other markets, however, the labor market considered in isolation

is relevant not to the short run but to the medium run, a time frame over which it is reasonable to assume

that price expectations are correct.

III. KEY TOOLS, CONCEPTS, AND ASSUMPTIONS

1. Tools and Concepts

i. The chapter reviews the definition of key labor market terms introduced in Chapter 2 and

introduces several new ones, including the participation rate, discouraged workers, separations,

layoffs, and quits.

ii. The chapter makes use of a production function.

iii. The chapter introduces wage-setting and price-setting relations.

iv. The chapter defines analytically the natural rate of unemployment and the natural level of

output.

v. The chapter introduces the concept of an expected price level, the first expectation seen in the

book.

2. Assumptions

©2017 Pearson Education, Inc. Publishing as Prentice Hall

7-36

i. The chapter assumes that labor is the only factor of production. The text maintains this assumption

until Chapter 10, which introduces growth.

ii. The chapter assumes a constant returns to scale (CRS) production function with fixed technology.

This specification of the production function (labor only, CRS, and fixed technology) implies that

the real wage is constant.

IV. SUMMARY OF THE MATERIAL

1. A Tour of the Labor Market

The U.S. labor market is characterized by large flows between the three states of labor market activity:

employed, unemployed, and out of the labor force. The text provides data on the size of these flows. The

fact that large numbers of people move from out of the labor force into employment suggests that some

individuals classified as out of the labor force may be discouraged workers, i.e., people who have given

up looking for work, but who would take work if they were offered it. If this is the case, the

unemployment rate underestimates the number of people available for work. Some economists prefer to

use the nonemployment rate as a measure of the state of the labor market.

2. Movements in Unemployment

The chapter develops four facts about the U.S. unemployment rate. First, after World War II, there was an

upward trend in the unemployment rate until the mid-1980s; since then, the unemployment rate has

declined. Second, year-to-year fluctuations in the unemployment rate are associated with recessions and

expansions. Third, when the unemployment rate is high, the proportion of unemployed workers finding

jobs is low. Finally, when the unemployment rate is high, the proportion of employed workers losing

their jobs is high.1

3. Wage Determination

The text considers wage determination from two perspectives: bargaining and efficiency wages. Wage

bargaining between employers and employees takes many forms. In some occupations, wages are

determined by collective bargaining between unions and firms. In the United States, slightly more than

10% of workers are covered by collective bargaining agreements. Highly or uniquely skilled workers

(e.g., athletes, entertainers) engage in individual bargaining with their employers. For jobs that require

little skill, employers may make take-it-or-leave-it wage offers.

Efficiency wage theories are motivated by the idea that labor productivity is related to the wage. Paying a

high wage may improve employee morale. Alternatively, a high wage may reduce turnover, which can be

advantageous to the firm if it takes time to train new workers. From this perspective, firms have an

incentive to offer a wage above the reservation wage—the wage at which a worker is indifferent between

working or becoming unemployed.

1 The text provides evidence about job separations, which include quits as well layoffs. A margin note

argues, however, that quits are lower when the unemployment rate is high – as we would expect from

theory – so that layoffs actually increase by more than separations when the unemployment rate is high.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

7-37

The text summarizes the complex wage determination process by focusing on three factors. First, wage

outcomes depend on labor market conditions, which can be proxied by the unemployment rate (u). When

the unemployment rate is high, it is relatively easy for firms to replace workers and difficult for workers

to find new jobs, so worker bargaining power is low. In addition, workers are highly motivated to work

and are unlikely to quit, so the efficiency wage motive is weaker. Second, given the unemployment rate,

there are institutional and structural factors (summarized by the variable z) that affect the bargaining

power of workers relative to employers. These factors include, among other things, the generosity of

unemployment insurance and the level of the minimum wage. Finally, the nominal wage depends on the

price level, because both workers and firms care about the real wage. However, wages are changed

infrequently, so the price level that matters is the one that prevails over the duration of the wage contract.

Since this future price level is unknown, wage determination depends on the expected price level.

These points suggest an aggregate wage determination equation of the following form:

W=PeF(u, z). (7.1)

– +

4. Price Determination

Assume that labor is the only factor of production and that firms operate under constant returns to scale.

Then, the production function takes the form

Y=N. (7.2)

Since the text assumes that technology is fixed in the medium run, equation (6.2) sets the marginal

productivity of labor equal to one.

Now assume that the goods market is imperfectly competitive, so firms have some market power. This

implies that firms will set price according to

P=(1+m)W. (7.3)

W, the wage, is the marginal cost of production, and m is a markup reflecting the degree of market power

possessed by firms. In a perfectly competitive environment, m =0.

5. The Natural Rate of Unemployment

If nominal wages depend on the price level then:

W =PF(u,z)

And dividing both sides by the price level we get.

W/P= F(u,z) (7.4)

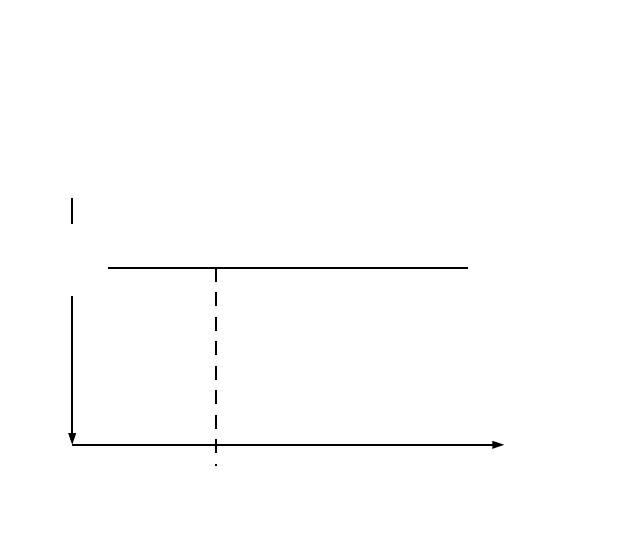

This relationship between the real wage and the rate of unemployment is known as the wage-setting

relation which is shown in Figure 7-6.

The price setting relationship is given by;

P/W = 1 + m (7.5)

©2017 Pearson Education, Inc. Publishing as Prentice Hall

7-38

When we invert this equation we get;

W/P = 1/(1 + m) (7.6)

Labor market equilibrium requires that the real wage implied by WS equal the real wage implied by PS,

or;

F(u,z)=1/(1+m). (7.7)

The value of u that satisfies equation (7.7) is called the natural rate of unemployment. The graphical

solution is given in Figure 7-6. Note that WS slopes down, since an increase in the unemployment rate

tends to reduce the relative power of workers in wage bargaining. The PS curve is flat as a result of the

assumption of constant returns to scale in the production function. If the production function exhibited

decreasing returns to scale, the price-setting relation would be upward sloping.

The natural rate of unemployment is the rate of unemployment that makes WS and PS consistent when

P=Pe. It is a medium-run concept, for two reasons. First, prices can adjust over the medium run.

Second, in the absence of economic disturbances, it is unreasonable to assume that workers and firms will

continually hold incorrect price expectations. Eventually, workers and firms will learn from past

experience in forming price expectations. In the short run, there is no presumption that P=Pe, so the

actual unemployment rate need not equal the natural rate of unemployment.

Figure 7-6: The Natural Rate of Unemployment

Moreover, the adjective natural is misleading. The natural rate of unemployment depends on labor

market institutions and market structure. For example, an increase in competition in the goods market (a

decrease in ) would shift the PS line up and reduce the natural rate of unemployment. An increase in the

z index—say, because of an increase in unemployment benefits—would shift the WS curve up and

increase the natural rate of unemployment.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

Real Wage, W/P

Unemployment Rate, u

1

1+m

un

7-39

Note that employment N is given by N=(1-u)L, where L is the labor force. Assuming that L is fixed, the

natural rate of unemployment (un) defines a natural level of employment Nn=(1-un)L, which implies a

natural level of output Yn= Nn. The natural level of output is the level of output that would prevail if

price expectations were correct. Like the natural rate of unemployment, the natural level of output is a

medium-run concept. In the short run, the actual price level can differ from the expected price level, the

actual unemployment rate can differ from the natural rate, and the actual level of output can differ from

the natural level of output.

6. Where We Go from Here

This chapter discusses the determination of the unemployment rate and output in the medium run, a time

frame in which it is reasonable to assume that the price level equals the expected price level. In the short

run, when the expected price level need not equal the actual price level, the demand factors discussed in

the previous chapters affect the unemployment rate. The next two chapters incorporate the labor market

into the model developed in the previous chapters and analyze the determination of output, the

unemployment rate, and the interest rate in the short and medium run.

V. PEDAGOGY

1. Points of Clarification

The introduction of the expected price level, even in the simple fashion of the text, is a big jump for

students. The text quickly removes the expected price level from discussion by equating it with the actual

price level. As a result, students begin to think of the wage-setting and price-setting diagram as the

method to determine unemployment at any time. It is worthwhile to emphasize that the natural rate is a

medium-run concept and that there is no presumption that the price level equals the expected price level,

or that the unemployment rate equals the natural rate, in the short run.

2. Alternative Sequencing

The organization of the text allows instructors to move immediately from the IS-LM framework to

expectations (Chapters 14-16) or the open economy (Chapters 17-19), before consideration of aggregate

demand and aggregate supply. Note, however, that one section of Chapter 20 does use a modified AD-AS

framework to analyze the effects of devaluation.

VI. EXTENSIONS

1. The Concept of the Medium Run

It may be worthwhile to reexamine the concept of the medium run in this chapter. Typically,

disturbances are analyzed in the text as follows. Assume the economy begins in a medium-run

equilibrium. Now consider an economic disturbance. The new medium-run equilibrium describes a point

to which the economy will tend to return in the absence of further disturbances. The new short-run

equilibrium describes the immediate effect of the disturbance. This chapter describes the effects of

disturbances on the unemployment rate and output in the medium run.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

7-40

2. Additional Examples

In Chapter 8, which examines the Phillips curve, boxes in the text examine European unemployment rates

and changes in the U.S. natural rate over time. Although these examples fit naturally into a discussion of

the history of the Phillips curve, instructors could use these examples in this chapter to reinforce the idea

that the natural rate of unemployment depends on structural factors that can change.

VII. OBSERVATIONS

The real wage is unaffected by the business cycle in the model of this chapter. Given the labor only,

constant returns to scale production function, the real wage is always determined by the price-setting

relation, regardless of whether P=Pe. Thus, the real wage is always determined by the degree of

competition in product markets and the marginal product of labor (set equal to one in this chapter).

Assuming that market structure changes relatively slowly, the implication of this model is that the real

wage changes only when labor productivity changes.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

7-41