Chapter 4. Financial Markets

I. MOTIVATING QUESTION

How is the interest rate determined in the short run?

The interest rate is determined by equilibrium in the money market, i.e., by the condition that money

supply equals money demand. Since the text abstracts from all assets other than bonds and money,

equilibrium in the money market is equivalent to equilibrium in the bond market. In this chapter, nominal

income is taken as given, so there is no need to consider simultaneous equilibrium of goods and financial

markets.

II. WHY THE ANSWER MATTERS

Investment is a function of the interest rate (as will be discussed in Chapter 5), so output is affected by the

interest rate. In addition, the determination of the interest rate is intimately connected with monetary

policy. This chapter introduces the simplest model needed to think about the determination of the interest

rate and the role of the central bank. This chapter takes nominal GDP, which affects money demand, as

given, so the financial markets can be considered in isolation from the goods market. Chapter 5 will

address the joint determination of output and the interest rate in the short run. Chapter 9 will address the

complexity of the financial system in light of the financial crisis.

III. KEY TOOLS, CONCEPTS, AND ASSUMPTIONS

1. Tools and Concepts

i. The chapter defines stock and flow variables and distinguishes wealth (a stock) from income (a

flow).

ii. The chapter introduces monetary policy and describes open market operations.

iii. The chapter makes use of balance sheets for the central bank and private banks.

iv. The chapter introduces various terms and concepts associated with the banking system. These

include currency, checkable deposits, reserves, the reserve ratio, central bank money (high powered

money, the monetary base), the federal funds market and the federal funds rate, and the money

multiplier.

2. Assumptions

i. This chapter assumes that nominal GDP is given. More precisely, the chapter maintains the

previous chapter’s assumption that the price level is fixed, and adds the assumption that real income is

given. Chapter 5 considers the joint determination of the interest rate and real income.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

4-19

ii. For clarity, the chapter assumes that money and bonds are the only assets available and that money

does not pay interest. Money is divided into currency and checkable deposits in the section of the chapter

that describes the banking system. The assumption that money does not pay interest is maintained

throughout the book. Later chapters introduce other financial assets—stocks and bonds of different

maturities—and physical capital

IV. SUMMARY OF THE MATERIAL

1. The Demand for Money

Suppose the financial markets include only two assets: money, which can be used to purchase goods and

services and pays no interest; and bonds, which cannot be used for transactions, but pay a positive interest

rate i. Financial wealth equals the sum of money and bonds.

Financial wealth is a stock variable, i.e., a variable whose value can be measured at any point in time. An

individual’s financial wealth changes over time by saving or dissaving, but at any given moment,

financial wealth is fixed. Saving is a flow variable, i.e., a variable whose value is meaningful only when

expressed in terms of a time period. Income is also a flow variable, as is recognized in ordinary speech.

People speak of annual income or monthly income.

At every moment, households must decide how to allocate their given financial wealth between money

and bonds. Since financial wealth is fixed, the demand for bonds is known once the demand for money is

known, and vice-versa. Accordingly, the chapter restricts attention to the demand for money.

By assumption, money is needed for transactions. Although it is hard to measure the overall level of

transactions in the economy, it seems reasonable to assume that the level of transactions is proportional to

nominal income, denoted $Y. So, money demand should be proportional to $Y. On the other hand,

allocating wealth to money comes at the cost of forgone interest on bonds. So, money demand should

decrease with the interest rate. Putting these observations together, the chapter specifies money demand

as

Md=$YL(i), (4.1)

where the function L decreases as the interest rate increases.

A box in the text notes that most U.S. currency is held abroad by foreigners, so that factors beyond U.S.

economic variables affect U.S. money demand. Nevertheless, the text does not include foreign variables

in the specification of U.S. money demand.

2. The Determination of the Interest Rate, I

Assume all money is currency, so there are no checking accounts or banks. Consider the supply of money

to be fully in the control of the central bank, and take nominal income as given. Then, equilibrium in the

money market occurs when the supply of money (M) equals the demand for money (Md) given in equation

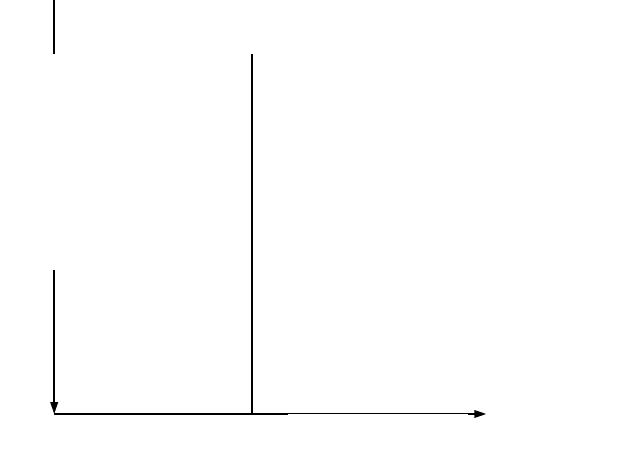

(4.1). Figure 4-2 illustrates this equilibrium point.

An increase in the money supply shifts the vertical line to the right, resulting in a new equilibrium with a

lower interest rate. In order to induce the private sector to hold more money, bonds must become less

©2017 Pearson Education, Inc. Publishing as Prentice Hall

4-20

attractive (the interest rate must fall). An increase in nominal income (for a given money supply) shifts

the money demand curve to the right and generates a new equilibrium with a higher interest rate. The

increase in nominal income leads to an increase in the quantity of money demanded at the original interest

rate. Since the supply of money has not changed, the interest rate must rise to reduce the quantity of

money demanded and thereby offset the effect of the increase in income.

How does the central bank control the money supply? Consider the central bank’s balance sheet.

Currency held by the public constitutes the central bank’s liabilities. The central bank’s assets are any

bonds that it owns. To increase the money supply, the central bank creates currency to purchase bonds,

thus increasing assets (through the additional bonds) and liabilities (through the new currency created and

exchanged for bonds). To reduce the money supply, the central bank sells bonds for existing currency,

thus reducing assets (through the sale of bonds) and liabilities (through the reduction of currency held by

the general public). Purchases and sales of bonds by the central bank are called open market operations.

Figure 4-2: Equilibrium in the Money Market

The text also shows how bond prices and interest rates are related. Suppose a bond promises a payment

of $F one year in the future. Call the current price of the bond $PB. Then, the interest rate (or rate of

return) on this bond is given by

i=($F-$PB)/$PB.

We can solve this equation for the bond price:

$PB=$F/(1+i).

Given fixed nominal bond payments, we show that the nominal interest rate and the bond prices are

inversely related. For example, when the central bank purchases bonds through open market operations it

increases the demand for bonds and tends to increase their price which, in turn, reduces the interest rate.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

Interest Rate, i

Money, M

Ms

Md=$YL(i)

4-21

3. The Determination of the Interest Rate, II

Now introduce banks into the model. Banks receive funds from depositors (individuals and firms) and

allow their depositors to write checks against (or withdraw) their account balances. These checkable

deposits are liabilities of banks. On the asset side, banks hold bonds, loans (which are claims against

borrowers), and reserves of some of their deposits. Some bank reserves are held in cash and the rest in

accounts at the central bank. Banks hold reserves in part to protect against daily excesses of withdrawals

(in currency or check form) over deposits and in part because they are required to do so by the central

bank. In the United States, the Federal Reserve sets the required reserve ratio for checkable deposits.

The actual reserve ratio in the United States is currently a minimum of 10%.

Adding banks to the economy alters the central bank balance sheet only on the liabilities side. Central

bank liabilities now consist of currency held by the public plus reserves held by banks. Central bank

liabilities—the money the central bank has created—are called central bank money.

Now reconsider money market equilibrium in terms of central bank money (Hd). The demand for central

bank money arises from two sources: currency held by the public and reserves held by banks. Since bank

reserves depend on the amount of checkable deposits we can model this relationship by letting the θ

(Greek lowercase letter theta) represent the reserve ratio. Recall from our original equation 4.1 that

money demand is given by;

Md=$YL(i),

(4.3)

The second component of money demand, bank reserve demand, can be modeled with the equation;

Hd = θMd = θ$Y L(i) (4.4)

Equilibrium in the money market can now be depicted as the point where the money supply controlled by

the Federal Reserve (H) is equal to the money demand (Hd).

We can rewrite this equation in the following manner;

H = θ$Y L(i) (4.6)

Graphically this equilibrium is presented in Figure 4-7. Now you can see that an increase or decrease in

the money supply impacts the price of money (i.e. the interest rate). The specific interest rate targeted by

the Fed is the federal funds rate.

4. The Liquidity Trap

The central bank can choose a desired interest rate by changing the money supply. However, the central

bank can push interest rates to zero which would limit further monetary stimulus. This condition is known

as a zero lower bound. When the economy is in this position and monetary policy is no longer effective

the economy is said to be in a liquidity trap. Increasing the money supply beyond this point has no impact

on interest rates. Both households and banks absorb increases in the money supply when interest rates are

zero so monetary policy loses its effectiveness. The Focus box on page 81 addresses the “Liquidity Trap

in Action” as a result of central bank policy following the financial crisis.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

4-22

V. PEDAGOGY

1. Points of Clarification

i. The Definition of Money Demand. Money demand refers to a portfolio decision, the amount of

fixed wealth that the nonbank public desires to hold in money as opposed to bonds. Money demand does

not refer to the demand for income or wealth.

ii. Comparative Statics with Bond Prices. It may be useful to reconsider comparative statics in the

money market in terms of bond prices. The text carries out this exercise for open market operations, but

instructors could also do the analysis for an exogenous increase in national income. An increase in

income shifts the money demand curve to the right, which leads to an increase in the equilibrium interest

rate, as is evident from the graph. To tell the bond market story, note that at the initial interest rate, the

quantity of money demanded exceeds the quantity supplied. In other words, households are attempting to

sell bonds to acquire money. The pressure to sell bonds (effectively a shift to the left of the bond demand

curve) reduces the bond price and hence increases the interest rate.

iii. The Central Bank Balance Sheet. It is probably wise to assume that many undergraduates have

never seen a balance sheet of any kind. A few words of explanation would be useful. In addition, as a

memory aid for students, it may be useful to simplify the discussion of open market operations by noting

that when the central bank increases its assets, it increases the money supply. Thus, when the central bank

buys bonds, it increases the money supply.

iv. Currency, Government Bonds, and the Central Bank. The model without banks implies that

the central bank creates currency when conducting an open market purchase. Although this notion has

some intuitive appeal, and can be useful as a pedagogical step, it is worth clarifying that in fact the central

bank creates reserves, not currency.

Moreover, the central bank does not create government bonds, but conducts open market operations with

government bonds. The stock of government bonds outstanding is the government (in popular usage,

national) debt, which is the product of past fiscal deficits. Open market operations apportion this debt

between the central bank and the private sector.

2. Alternative Sequencing

Instructors have several options for presenting money market equilibrium. The most straightforward

presentation would rely on Section 4.2 for the cash economy and progress to Section 4.3 if banks and

checkable deposits are introduced. Section 4.3 equates the demand and supply for central bank money.

Alternatively, to emphasize the federal funds market, instructors could present equilibrium with banks in

terms of the supply and demand for reserves.

The interest rate was not introduced in the discussion of the goods market in Chapter 3. Thus, at this

point in the text, the determination of the interest rate seems to stand apart from the determination of real

output. As discussed in Part V of Chapter 3 of the Instructor’s Manual, an alternative is to introduce the

dependence of investment on the interest rate in Chapter 3 and to assume a fixed interest rate.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

4-23

Another option is to introduce some of the material in Chapter 23, devoted to monetary policy, in the

discussion of the current chapter. Some of the basic facts about the structure of Monetary Policy and the

crisis may be helpful to orient students and to help facilitate discussion of current Fed policy.

3. Enlivening the Lecture

Casual empiricism suggests that undergraduates have more immediate interest in material related to

financial markets than in almost any other topic. A discussion relating the material of the chapter to

current Federal Reserve policy (perhaps with a few words about the stock market’s response to Fed

policy) would probably be interesting to students. In addition there is a current debate about negative

interest rates and whether or not central banks can use negative rates effectively.

Another suggestion is to look at the interest rate section of the financial pages of a major newspaper

during the lecture. Besides making the financial pages a bit more accessible to students, this strategy

might also provide an opportunity to discuss the inverse relationship between prices and interest rates.

VI. EXTENSIONS

1. The Balance Sheet Constraint

To clarify the relationship between bond market and money market equilibrium, it may be useful to be

more explicit about the implications of the balance sheet constraint. The constraint implies

Md+Bd=Financial Wealth=M+B,

or

(Md – M)=(B – Bd).

In other words, the excess demand for money must equal the excess supply of bonds. When one market

clears, the other must clear as well.

2. The Money Demand Function

This chapter assumes a money demand function of the form Md=$YL(i)=PYL(i). A more general

alternative would be Md=L($Y,i). The functional form assumed in the chapter allows for an easy

conversion to real money demand by dividing through by the price level. Introducing the more general

form requires explaining to students that money demand should be homogeneous of degree one in P. On

the other hand, this exercise does make clear what is assumed.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

4-24