Chapter 3. The Goods Market

I. MOTIVATING QUESTION

How is output determined in the short run?

Output is determined by equilibrium in the goods market, i.e., by the condition that supply (production of

goods) equals demand. This condition always determines output, but in the short run, we assume that

production adjusts automatically to output without changes in price. Thus, in the short run, output is

effectively determined by demand. Moreover, in this chapter, investment is exogenous (and therefore

independent of the interest rate), so there is no need to consider simultaneous equilibrium in the goods

and financial markets.

II. WHY THE ANSWER MATTERS

The determination of output is the fundamental issue of macroeconomics. This chapter introduces the

topic through the Keynesian cross model, which considers the goods market in isolation. The Keynesian

cross provides basic intuition about the building and solving of models, the determination of output, and

the role of fiscal policy. The short-run, qualitative results generally survive in more complicated models.

Chapter 4 examines the financial markets in isolation, and Chapter 5 combines the goods and financial

markets to construct the demand side of the economy.

III. KEY TOOLS, CONCEPTS, AND ASSUMPTIONS

1. Tools and Concepts

i. The chapter introduces functional notation.

ii. The chapter introduces modeling terminology: exogenous and endogenous variables, behavioral

equations, identities, and equilibrium conditions.

iii. The chapter describes the Keynesian cross model (although it does not use this expression), and

associated terms, such as the (marginal) propensity to consume, disposable income, and autonomous

spending.

iv. The chapter introduces fiscal policy.

2. Assumptions

i. The text assumes that the economy produces a single good. This assumption is maintained

throughout most of the formal work in the book.

©2017 Pearson Education, Inc. Publishing as Prentice Hall

3-14

ii. After introducing the national income identity, the text assumes a closed economy. This assumption

is maintained until Chapter 17.

iii. For short-run analysis, the text assumes that production adjusts automatically to output without

changes in price. This assumption implies that the price level is fixed. Instructors may wish to clarify

this assumption before the price level is introduced in the discussion of the money market and the LM

curve in Chapters 4 and 5. The assumption that the price level is fixed is maintained until Chapter 7.

iv. Within the short-run context, the critical assumption of this chapter is that investment does not

respond to the interest rate. This isolates the goods market from the financial market. This assumption

will be relaxed in Chapter 5.

v. The chapter, in fact, goes further, and assumes that investment is exogenous. It does not depend on

output, nor is there inventory investment, either planned or unplanned. Chapter 5 introduces the

dependence of investment on output. This chapter discusses in words the dynamic implications of

allowing unplanned inventory adjustment, although it does not stress this point.

IV. SUMMARY OF THE MATERIAL

1. The Composition of GDP

On the expenditure side, GDP can be decomposed into consumption (C), government spending (G), fixed

investment (I), net exports (X-IM), and inventory investment.

2. The Demand for Goods

Assume there is only one good, and use the decomposition of GDP to think about demand for that good.

Assume the economy is closed, so that net exports are zero, and ignore inventory investment, which is

typically a small part of GDP. Then, demand (Z) can be written as

Z = C + I + G.

Write consumption as a linear function of disposable income (YD)

C = C(YD) (3.1)

(+)

The function C = C(YD) is called the consumption function. The positive sign below it indicates that

consumption increases as disposable income increases. However, there is some level of consumption that

would occur even if disposable income were zero. This consumption is called autonomous consumption

and is represented by c0. The parameter c1, which represents the increase in consumption for every extra

unit of disposable income, is called the (marginal) propensity to consume. Assume that households do not

consume every dollar of additional income, but save some, so that 0< c1<1.

Given this new information we can expand the consumption function to the following linear function;

C = c0+c1(YD) (3.2)

©2017 Pearson Education, Inc. Publishing as Prentice Hall

3-15

When we add the government sector and taxation to the model we see that consumers pay taxes (T) on

income (Y). This addition expands the linear expression of the model to;

C = c0+c1(Y – T ) (3.3)

The two remaining components of consumption are government spending (G) and business investment (I)

which in the next section we will hold constant.

3. The Determination of Equilibrium Output

Output is determined by equilibrium in the goods market. The equilibrium condition is that production

equals demand. Assume for now that production simply increases or decreases with demand without any

change in price. Thus, in the short run, output is fully determined by demand. Then, we can write the

equilibrium condition, Y=Z, as

Y = c0 + c1(Y – T) + +G. (3.5)

The variable Y appears on both sides of this equation. On the LHS, Y represents production. On the

RHS, Y represents national income. Chapter 2 explained why these two quantities are equal. The aim of

this model is to determine the value of Y, an endogenous variable. To solve the model, it is necessary to

write Y as a function of the exogenous variables, i.e., those determined outside the model. In other words,

Y= [1/(1-c1)][c0 + +G -c1T]. (3.8)

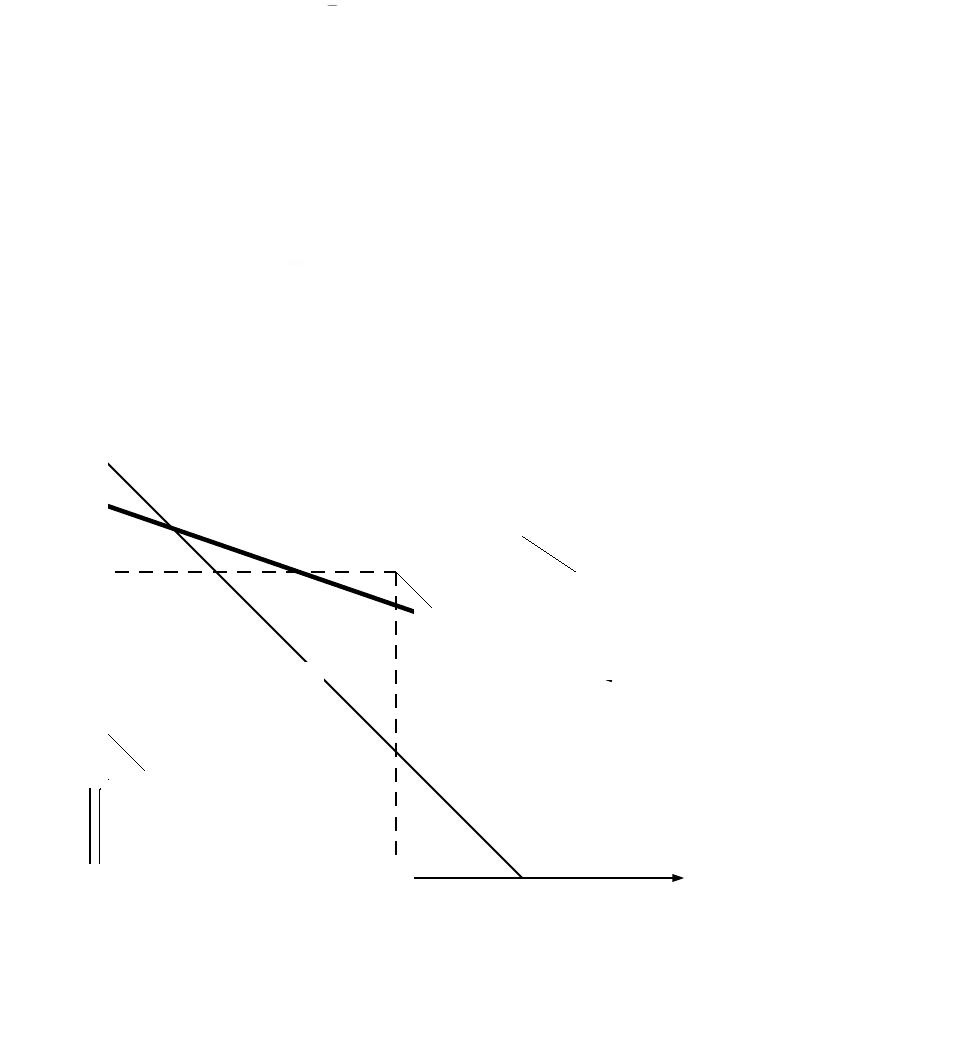

Equation (3.8) shows the algebraic solution and Figure 3-2 the graphical solution. In the graph,

equilibrium occurs where demand (the ZZ curve) crosses the 45 line (i.e., the line along which Y=Z).

Figure 3-2: Equilibrium in the Goods Market

©2017 Pearson Education, Inc. Publishing as Prentice Hall

Demand (Z), Production (Y)

Autonomous

Spending

Equilibrium Point

Slope = c1

ZZ

Demand

Y = Z

45

3-16

Equilibrium income is the product of two factors: autonomous spending (the second term in brackets in

equation (3.8)) and a “multiplier” (the first term in brackets). Assume that autonomous spending is

positive,1 which (given that c1<1) will be true unless the budget surplus, T-G, is very large. The

multiplier, which depends on the value of the propensity to consume, arises because consumption is

affected by income. Suppose there is an increase in autonomous consumption—say, because of an

increase in consumer confidence. The initial increase in consumption because of the rise in c0 leads to an

increase in income. The increase in income leads to a further increase in consumption, which leads to a

further increase in income, and so on. Thus, the effect of the initial increase in consumer confidence is

“multiplied.” The multiplier captures this effect. More formally, the multiplier can be described as the

limit of a geometric series of fractional increases in consumption. A focus box on page 59 discusses the

impact of the early stages of the financial crisis and consumer concerns over their future disposable

income.

4. Investment Equals Saving: An Alternative Way of Thinking About Goods

Market Equilibrium

Private saving is defined as disposable income minus consumption, or

S=Y-T-C.

Using this definition, the equilibrium output condition (Y=C+I+G) can be expressed as

I=S+(T-G). (3.10)

In a closed economy, investment equals private (consumer) saving (S) plus government saving (T-G).

The quantity T-G is called the budget surplus. The quantity G-T is called the budget deficit.

5. Is the Government Really Omnipotent? A Warning

The equilibrium output condition (3.8) seems to imply that the government, by choosing G and T, has

absolute control over the level of output. The text stresses that this chapter provides only a first pass at

the analysis of fiscal policy. Later chapters will make clear the many limitations on the ability of the

government to control output through spending and taxation.

V. PEDAGOGY

1. Points of Clarification

i. The Definition of Goods. The chapter assumes that the economy produces only one item and calls

this item a good. However, the model is not meant to be limited to physical goods as opposed to services.

“Goods” is generally used to refer to both physical goods and services.

1

©2017 Pearson Education, Inc. Publishing as Prentice Hall

Income, Y

3-17

ii. The Definitions of G and T. Government spending includes the purchase of newly produced

goods and services, not total government outlays. In particular, transfers—such as Social Security

payments, veterans’ benefits, and interest on the government debt—are excluded. Note also that

government spending includes spending by all levels of government (federal, state, and local) and that

some government spending pays for capital goods. The variable T is defined as taxes minus transfers and

includes taxes minus transfers at all levels of government.

iii. Exports and Imports in GDP. Imports are subtracted from GDP on the expenditure side because

the domestic spending categories C, I, and G include spending on foreign goods and services. To isolate

spending on domestically produced goods and services, imports must be subtracted. Likewise, exports

are added because they represent foreign spending on domestically produced goods and services.

2. Alternative Sequencing

©2017 Pearson Education, Inc. Publishing as Prentice Hall

3-18

For simplicity, investment is taken as exogenous. Chapter 5 describes the effects of output and the

interest rate on investment in the course of developing the IS-LM model. An alternative would be to

introduce the dependence of investment on the interest rate in this chapter, and then assume a fixed

interest rate. Since assuming a fixed interest rate is essentially equivalent to assuming exogenous

investment, this approach removes an (arguably) unnecessary step in the development of the IS-LM

framework. It also allows for early experiments with the effects of changes in the interest rate on output

as precursors to the derivation of the IS curve. On the other hand, introducing the interest rate at this

stage complicates the simple Keynesian cross story.

3. Enlivening the Lecture

The chapter does not cover explicitly fiscal policy experiments. Explaining these in lecture reinforces

concepts and provides an opportunity to link the model to current policy debates. For example, with

respect to fiscal stimulus packages, instructors could entertain the notion that the propensity to consume

might vary with income (or more accurately, wealth) and discuss how different distributions of tax

benefits might have different quantitative effects on consumption. The focus box on page 63 introduces

the “Paradox of Saving” which is also an interesting way to stimulate class discussion.

VI. EXTENSIONS

1. Macroeconomic Models

Some instructors may wish to supplement the discussion of model building in the text by distinguishing a

model’s structural form from its reduced form and by explaining the requirement that the number of

equations equal the number of exogenous variables. A model’s structural form sets out the model’s

postulates about behavior, definitions, and equilibrium conditions. A model’s reduced form expresses the

endogenous variables in terms of the exogenous ones. The number of equations must equal the number of

unknowns if the model is to provide a complete (not underdetermined) and coherent (not overdetermined)

explanation of the phenomenon of interest.

2. Inventory Investment

As noted above in Part III, apart from a few words in the text, the formal model of this chapter abstracts

from inventory investment. This simplifies the presentation and allows the identification of aggregate

demand with final sales. As an alternative, instructors could introduce and distinguish planned and

unplanned inventory investment and characterize goods-market equilibrium by the condition that

unplanned inventory investment equals zero. In this approach, aggregate demand does not, in general,

equal final sales.

3. Fiscal Policy

The discussion in the text omits several familiar fiscal policy issues, including the balanced budget

multiplier and the role of income taxes as automatic stabilizers. These issues are examined in problems at

the end of the chapter (see the solutions for a discussion). However, instructors may wish to consider

these issues in class

©2017 Pearson Education, Inc. Publishing as Prentice Hall

3-19