P8-20. Interpreting beta

LG 5; Basic

Effect of change in market return on asset with beta of 1.20:

a. 1.20 (15%) 18.0% increase

P8-21. Betas

LG 5; Basic

a. and b.

Asset Beta

Increase in

Market Return

Expected Impact

on Asset Return

Decrease in

Market Return

Impact on

Asset Return

A 0.50 0.10 0.05 0.10 0.05

c. Asset B should be chosen because it will have the highest increase in return.

d. Asset C would be the appropriate choice because it is a defensive asset, moving in opposition to the

P8-22. Personal finance: Betas and risk rankings

LG 5; Intermediate

a.

Stock Beta

Most risky B 1.40

b. and c.

Asset Beta

Increase in

Market Return

Expected Impact

on Asset Return

Decrease in

Market Return

Impact on

Asset Return

A 0.80 0.12 0.096 0.05 0.040

d. In a declining market, an investor would choose the defensive stock, Stock C. While the market

e. In a rising market, an investor would choose Stock B, the aggressive stock. As the market rises one

© 2015 Pearson Education, Inc.

P8-23. Personal finance: Portfolio betas: bp

1

n

j j

j

w b

=

´

å

LG 5; Intermediate

a.

Portfolio A Portfolio B

Asset Beta wAwAb

A

wBwBb

B

1 1.30 0.10 0.130 0.30 0.39

b. Portfolio A is slightly less risky than the market (average risk), while Portfolio B is more risky than

P8-24. Capital asset pricing model (CAPM): rj RF [bj(rm RF)]

LG 6; Basic

Case rjRF [bj(rm RF)]

A 8.9% 5% [1.30(8% 5%)]

P8-25. Personal finance: Beta coefficients and the capital asset pricing model

LG 5, 6; Intermediate

To solve this problem you must take the CAPM and solve for beta. The resulting model is

Beta

F

m F

r R

r R

–

=–

a.

10% 5% 5%

Beta 0.4545

16% 5% 11%

–

= = =

–

b.

15% 5% 10%

Beta 0.9091

16% 5% 11%

–

= = =

–

c.

18% 5% 13%

Beta 1.1818

16% 5% 11%

–

= = =

–

d.

20% 5% 15%

Beta 1.3636

16% 5% 11%

–

= = =

–

e. If Katherine is willing to take a maximum of average risk then she will be able to have an expected

P8-26. Manipulating CAPM: rj RF [bj(rm RF)]

LG 6; Intermediate

a. rj8% [0.90(12% 8%)]

b. 15% RF [1.25(14% RF)]

c. 16% 9% [1.10(rm 9%)]

d. 15% 10% [bj(12.5% 10%)

P8-27. Personal finance: Portfolio return and beta

LG 1, 3, 5, 6: Challenge

a. bp (0.20)(0.80) (0.35)(0.95) (0.30)(1.50) (0.15)(1.25)

b. rA

($20,000 $20,000) $1,600 $1,600 8%

$20,000 $20,000

– +

= = =

rB

($36,000 $35,000) $1,400 $2,400 6.86%

$35,000 $35,000

– +

= = =

rC

($34,500 $30,000) 0 $4,500 15%

$30,000 $30,000

– +

= = =

rD

($16,500 $15,000) $375 $1,875 12.5%

$15,000 $15,000

– +

= = =

c. rP

($107,000 $100,000) $3,375 $10,375 10.375%

$100,000 $100,000

– +

= = =

d. rA 4% [0.80(10% 4%)] 8.8%

e. Of the four investments, only C (15% vs. 13%) and D (12.5% vs. 11.5%) had actual returns that

P8-28. Security market line, SML

LG 6; Intermediate

c. rj RF [bj(rm RF)]

Asset A

d. Asset A has a smaller required return than Asset B because it is less risky, based on the beta of 0.80

P8-29. Shifts in the security market line

LG 6; Challenge

a, b, c, d.

b. rj RF [bj(rm RF)]

c. rA 6% [1.1(10% 6%)]

d. rA 8% [1.1(13% 8%)]

e. (1) A decrease in inflationary expectations reduces the required return as shown in the parallel

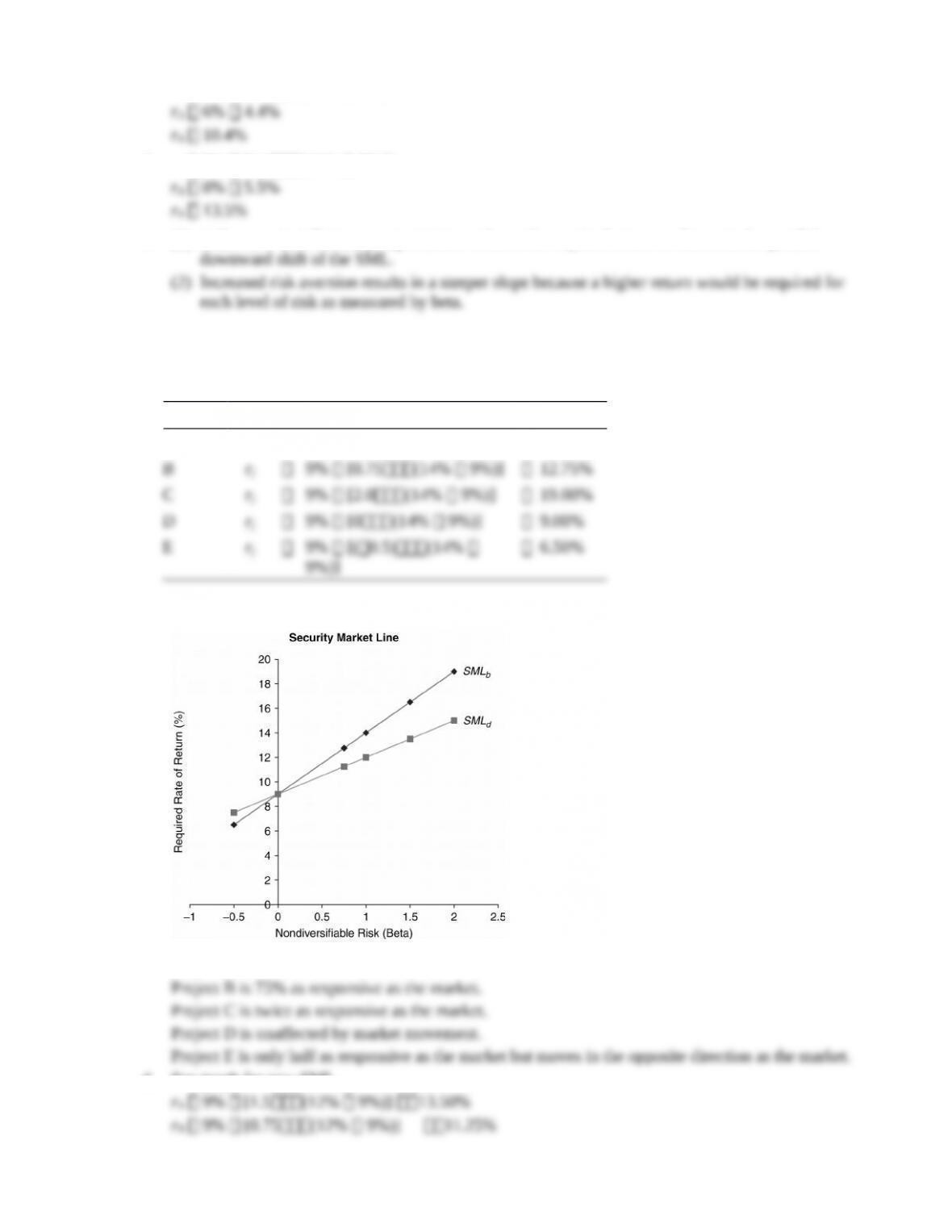

P8-30. Integrative—risk, return, and CAPM

LG 6; Challenge

a.

Project rjRF [bj(rm RF)]

Arj9% [1.5(14% 9%)] 16.50%

b. and d.

c. Project A is 150% as responsive as the market.

d. See graph for new SML.

e. The steeper slope of SMLb indicates a higher risk premium than SMLd for these market conditions.

P8-31. Ethics problem

LG 1; Intermediate

Investors expect managers to take risks with their money, so it is clearly not unethical for managers to

Case

Case studies are available on www.myfinancelab.com.

Analyzing Risk and Return on Chargers Products’ Investments

This case requires students to review and apply the concept of the risk-return tradeoff by analyzing two possible

a. Expected rate of return:

1

1

( )

t t t

t

t

P P C

rP

–

–

– +

=

Asset X:

Year

Cash

Flow (Ct)

Ending

Value (Pt)

Beginning

Value (Pt – 1)

Gain/

Loss

Annual Rate

of Return

2006 $1,000 $22,000 $20,000 $2,000 15.00%

Asset X: (continued)

Year

Cash

Flow (Ct)

Ending

Value (Pt)

Beginning

Value (Pt – 1)

Gain/

Loss

Annual Rate

of Return

2010 1,900 23,000 22,000 1,000 13.18

Average expected return for AssetX 11.74%

Asset Y:

Year

Cash

Flow (Ct)

Ending

Value (Pt)

Beginning

Value (Pt – 1)

Gain/

Loss

Annual Rate

of Return

2006 $1,500 $20,000 $20,000 $ 0 7.50%

Average expected return for Asset Y 11.14%

b. r

2

1

( ) ( 1)

n

i

i

r r n

=

– ¸ –

å

Asset X:

Year

Return

ri

Average

Return, r

( )–

i

r r

( )–

i

r r

2

2006 15.00% 11.74% 3.26% 0.001063

Asset X: (continued)

Year

Return

ri

Average

Return, r

( )–

i

r r

( )–

i

r r

2

2012 2.69 11.74 9.05 0.008190

0.071297 0.07922 0.0890 8.90%

10 1

x

s= = = =

–

8.90% 0.76

11.74%

CV = =

Asset Y:

Year Return

ri

Average

Return, r

( )–

i

r r

( )–

i

r r

2

2006 7.50% 11.14% 3.64% 0.001325

0.006955 0.0773 0.0278 2.78%

10 1

Y

s= = = =

–

2.78% 0.25

11.14%

CV = =

c. Summary statistics:

Asset X Asset Y

Expected return 11.74% 11.14%

d. Using the capital asset pricing model, the required return on each asset is as follows:

Capital asset pricing model: rj RF [bj(rm RF)]

Asset RF [bj(rm RF)] rj

X 7% [1.6(10%

11.8%

e. In part c, we concluded that it would be difficult to make a choice between X and Y because the additional

f. 1. Increase in risk-free rate to 8% and market return to 11%:

Asset RF [bj(rm RF)] rj

X 8% [1.6(11%

12.8%

8%)]

2. Decrease in market return to 9%:

Asset RF [bj(rm RF)] rj

X 7% [1.6(9% 7%)] 10.2%

Spreadsheet Exercise

The answer to Chapter 8’s stock portfolio analysis spreadsheet problem is located on the Instructor’s Resource

Group Exercise

Group exercises are available in www.myfinancelab.com.

This exercise uses current information from several websites regarding the recent performance of each group’s

s