P8-10. Assessing return and risk

LG 2; Challenge

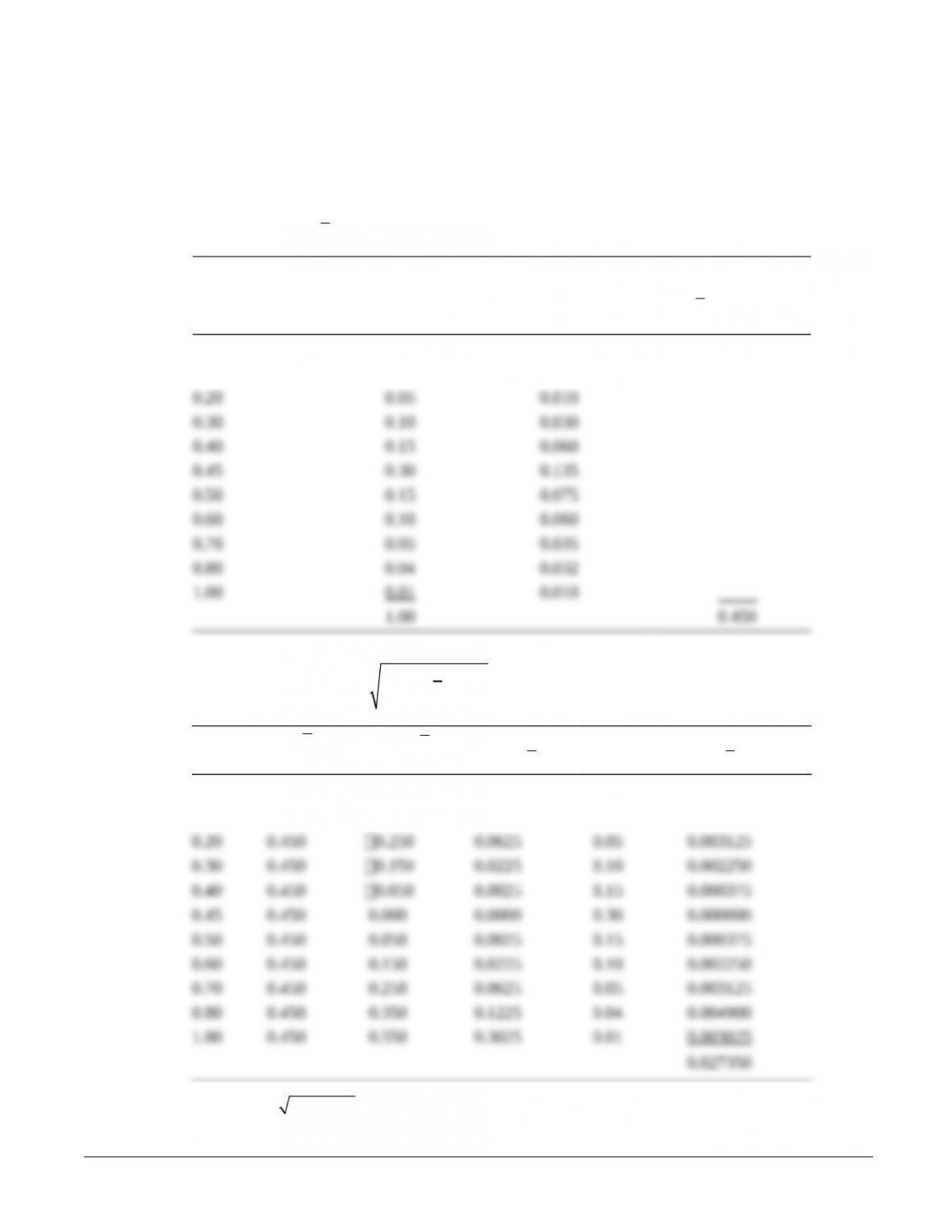

a. Project 257

(1) Range: 1.00 (.10) 1.10

(2) Expected return:

=1

n

i ri

i

r r P= ´

å

Rate of Return

ri

Probability

Pr i

Weighted Value

ri Pr i

Expected Return

å

1=

= ´

n

i ri

i

r r P

.10 0.01 0.001

0.10 0.04 0.004

(3) Standard deviation:

2

1

( )

n

i ri

i

r r Ps

=

= – ´

å

ri

r

–

i

r r

( )–

i

r r

2Pr i

( )–

i

r r

2Pr i

0.10 0.450 0.550 0.3025 0.01 0.003025

0.10 0.450 0.350 0.1225 0.04 0.004900

Project 257

0.027350 0.165378s= =

© 2015 Pearson Education, Inc.

(4)

0.165378 0.3675

0.450

CV = =

Project 432

(2) Expected return:

1

n

i ri

i

r r P

=

= ´

å

Rate of Return

ri

Probability

Pr i

Weighted Value

riPri

Expected Return

å

=1

= ´

n

i ri

i

r r P

0.10 0.05 0.0050

0.15 0.10 0.0150

(3) Standard deviation:

2

1

( )

n

i ri

i

r r Ps

=

= – ´

å

ri

r

–

i

r r

2

( )

i

r r–

Pri

P

2

( )

i ri

r r– ´

0.10 0.300 0.20 0.0400 0.05 0.002000

0.15 0.300 0.15 0.0225 0.10 0.002250

Project 432

0.011250

0.106066

(4)

0.106066 0.3536

0.300

CV = =

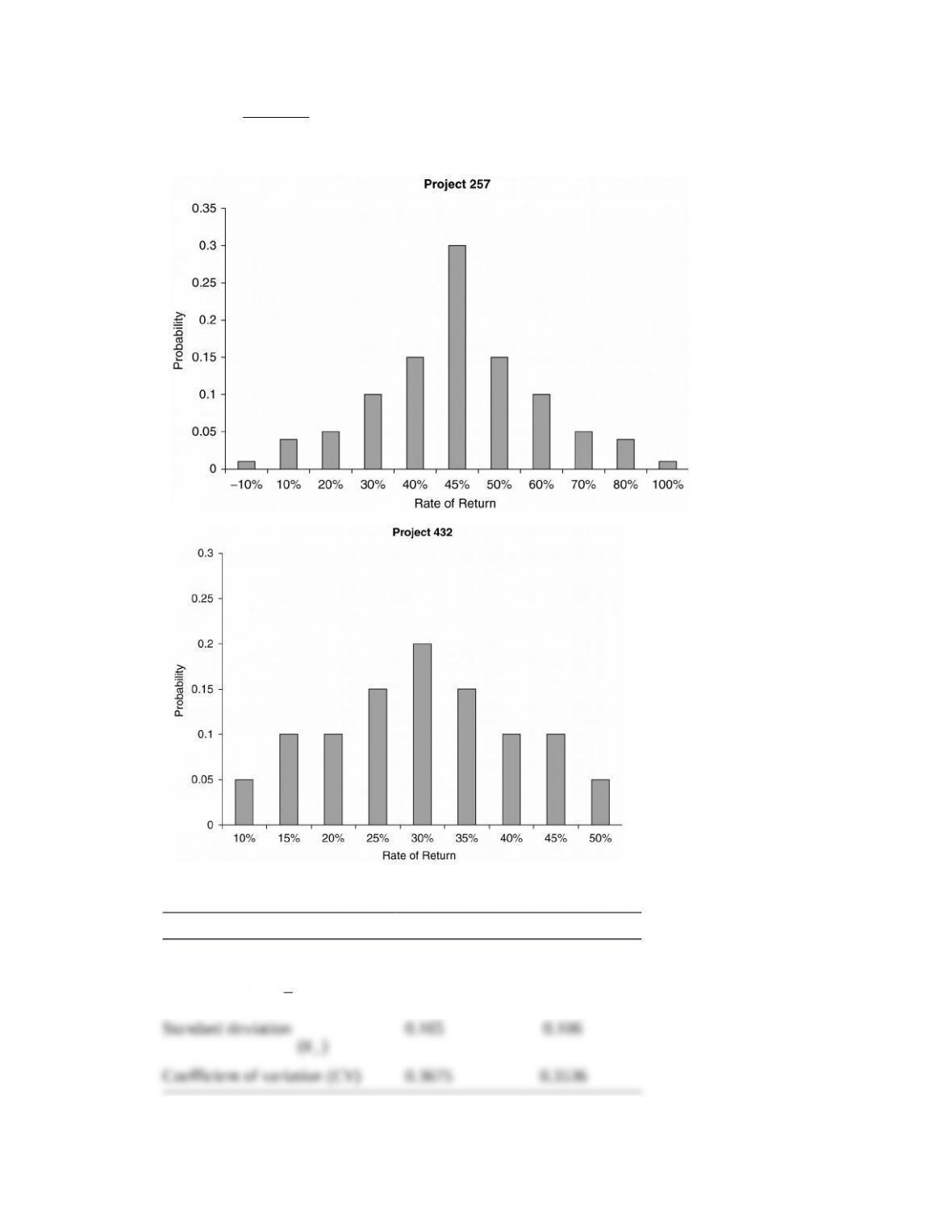

b. Bar Charts

c. Summary statistics

Project 257 Project 432

Range 1.100 0.400

Expected return

( )r

0.450 0.300

Standard deviation

( )

r

s

0.165 0.106

Coefficient of variation (CV) 0.3675 0.3536

P8-11. Integrative—expected return, standard deviation, and coefficient of variation

LG 2; Challenge

a. Expected return:

1

n

i ri

i

r r P

=

= ´

å

Rate of Return

ri

Probability

Pr i

Weighted Value

riPri

Expected Return

å

1=

= ´

n

i ri

i

r r P

Asset F 0.40 0.10 0.04

0.04

Asset G 0.35 0.40 0.14

0.11

Asset H 0.40 0.10 0.04

0.10

Asset G provides the largest expected return.

b. Standard deviation:

2

1

( )

n

i ri

i

r r xPs

=

= –

å

–

i

r r

( )–

i

r r

2Pr i 2r

Asset F 0.40 0.04 0.36 0.1296 0.10 0.01296

Asset G 0.35 0.11 .24 0.0576 0.40 0.02304

Asset H 0.40 0.10 .30 0.0900 0.10 0.009

c.

standard deviation ( )

Coefficient of variation = expected value

s

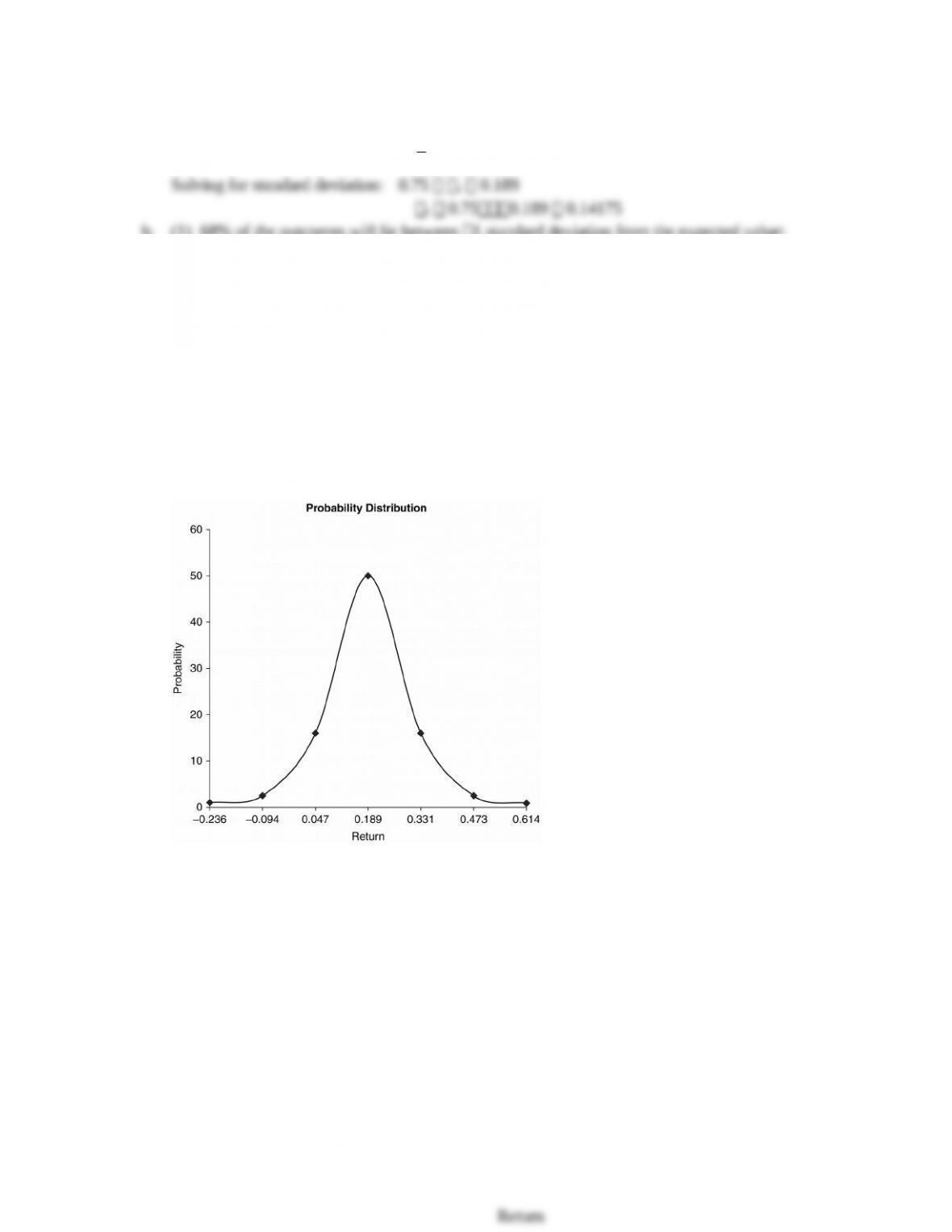

P8-12. Normal probability distribution

LG 2; Challenge

a. Coefficient of variation: CV

r

rs¸

Solving for standard deviation: 0.75 r 0.189

r 0.750.189 0.14175

b. (1) 68% of the outcomes will lie between 1 standard deviation from the expected value:

1 0.189 0.14175 0.33075

1 0.189 0.14175 0.04725

s

s

+ = + =

– = – =

(2) 95% of the outcomes will lie between 2 standard deviations from the expected value:

2 0.189 (2 0.14175) 0.4725

2 0.189 (2 0.14175) 0.0945

s

s

+ = + ´ =

– = – ´ =–

(3) 99% of the outcomes will lie between 3 standard deviations from the expected value:

3 0.189 (3 0.14175) 0.61425

3 0.189 (3 0.14175) 0.23625

s

s

+ = + ´ =

– = – ´ =–

c.

P8-13. Personal finance: Portfolio return and standard deviation

LG 3; Challenge

a. Expected portfolio return for each year: rp (wLrL) (wMrM)

Year

Asset L

(wLrL)

Asset M

(wMrM)

Expected

Portfolio Return

rp

2015 (14% 0.40 5.6%) (20%0.60

12.0%)

17.6%

6.0%)

b. Portfolio return:

1

n

j j

j

p

w r

rn

=

´

=

å

17.6 16.4 16.0 15.2 14.0 13.6 15.467 15.5%

6

p

r+ + + + +

= = =

c. Standard deviation:

2

1

( )

( 1)

n

i

rp

i

r r

n

s

=

–

=–

å

222

2 2 2

(17.6% 15.5%) (16.4% 15.5%) (16.0% 15.5%)

(15.2% 15.5%) (14.0% 15.5%) (13.6% 15.5%)

6 1

rp

s

– + – + –

é ù

ê ú

+ – + – + –

ë û

=–

2 2 2

222

(2.1%) (0.9%) (0.5%)

( 0.3%) ( 1.5%) ( 1.9%)

5

rp

s

+ +

é ù

ê ú

+ – + – + –

ë û

=

(.000441 0.000081 0.000025 0.000009 0.000225 0.000361)

5

rp

s+ + + + +

=

0.001142 0.000228% 0.0151 1.51%

5

rp

s= = = =

d. The assets are negatively correlated.

e. Combining these two negatively correlated assets reduces overall portfolio risk.

P8-14. Portfolio analysis

LG 3; Challenge

a. Expected portfolio return:

Alternative 1: 100% Asset F

16% 17% 18% 19% 17.5%

4

p

r+ + +

= =

Alternative 2: 50% Asset F 50% Asset G

Year

Asset F

(wFrF)

Asset G

(wGrG)

Portfolio Return

rp

2016 (16%0.50 8.0%) (17%0.50 8.5%) 16.5%

(2)

2 2 2 2

[(16.5% 16.5%) (16.5% 16.5%) (16.5% 16.5%) (16.5% 16.5%) ]

4 1

FG

s– + – + – + –

=–

2 2 2 2

[(0) (0) (0) (0) ]

3

FG

s+ + +

=

0

FG

s=

(3)

2 2 2 2

[(15.0% 16.5%) (16.0% 16.5%) (17.0% 16.5%) (18.0% 16.5%) ]

4 1

FH

s– + – + – + –

=–

2 2 2 2

[( 1.5%) ( 0.5%) (0.5%) (1.5%) ]

3

FH

s– + – + +

=

[(0.000225 0.000025 0.000025 0.000225)]

3

FH

s+ + +

=

0.0005 0.000167 0.012910 1.291%

3

FH

s= = = =

c. Coefficient of variation: CV

r

rs¸

1.291% 0.0738

17.5%

F

CV = =

00

16.5%

FG

CV = =

1.291% 0.0782

16.5%

FH

CV = =

d. Summary:

rp: Expected Value

of Portfolio rp CVp

Alternative 1 (F) 17.5% 1.291% 0.0738

P8-15. Correlation, risk, and return

LG 4; Intermediate

a. (1) Range of expected return: between 8% and 13%

b. (1) Range of expected return: between 8% and 13%

P8-16. Personal finance: International investment returns

LG 1, 4; Intermediate

a. Returnpesos

24,750 20,500 4,250 0.20732 20.73%

20,500 20,500

–= = =

b.

Price in pesos 20.50

Purchase price= $2.22584 1,000 shares $2,225.84

Pesos per dollar 9.21

= = ´ =

Price in pesos 24.75

Sales price= $2.51269 1,000 shares $2,512.69

Pesos per dollar 9.85

= = ´ =

c. Returnus$

2,512.69 2,225.84 286.85 0.12887 12.89%

2,225.84 2,225.84

–= = =

d. The two returns differ due to the change in the exchange rate between the peso and the dollar. The

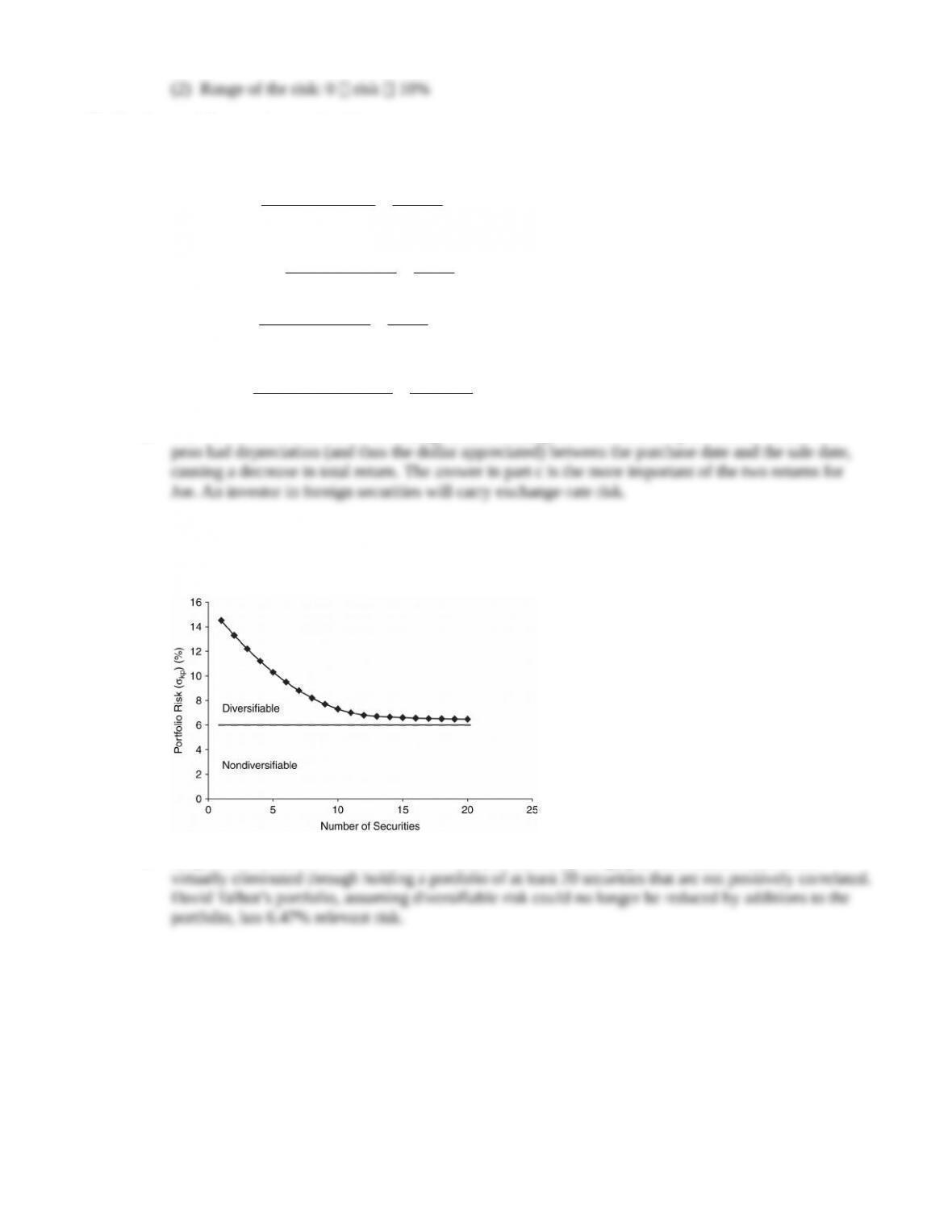

P8-17. Total, nondiversifiable, and diversifiable risk

LG 5; Intermediate

a. and b.

c. Only nondiversifiable risk is relevant because, as shown by the graph, diversifiable risk can be

P8-18. Graphic derivation of beta

LG 5; Intermediate

a.

b. To estimate beta, the “rise over run” method can be used:

Rise

Beta Run

Y

X

D

= =D

c. With a higher beta of 1.33, Asset B is more risky. Its return will move 1.33 times for each one point

P8-19. Graphical derivation and interpretation of beta

LG 5; Intermediate

a. With a return range from 0% to 30%, Biotech Cures, exhibited in Panel B, is the more risky stock.

b. The returns on Cyclical Industries Incorporated’s stock are more closely correlated with the market’s

c. On a standalone basis, Biotech Cures Corporation is riskier. However, if an investor was seeking to