Part 4

Risk and the Required Rate of Return

Chapters in this Part

Chapter 8 Risk and Return

Chapter 9 The Cost of Capital

Integrative Case 4: Eco Plastics Company

© 2015 Pearson Education, Inc.

Chapter 8

Risk and Return

Instructor’s Resources

Overview

This chapter focuses on the fundamentals of the risk and return relationship of assets and their valuation. For the

single asset held in isolation, risk is measured with the probability distribution and its associated statistics: the

mean, the standard deviation, and the coefficient of variation. The concept of diversification is examined by

measuring the risk of a portfolio of assets that are perfectly positively correlated, perfectly negatively correlated,

and those that are uncorrelated. Next, the chapter looks at international diversification and its effect on risk. The

Capital Asset Pricing Model (CAPM) is then presented as a valuation tool for securities and as a general

explanation of the risk-return tradeoff involved in all types of financial transactions. Chapter 8 highlights the

importance of understanding the relationship of risk and return when making professional and personal decisions.

Suggested Answer to Opener-in-Review Question

In the chapter opener you learned that Bill Miller’s investment performance was alternating between the

very top and the very bottom of his profession. What aspect of his investment strategy would lead you to

expect that his performance might exhibit greater volatility than that of other mutual funds? In the table

below, we show the annual performance from 2009 to 2012 of Miller’s Opportunity fund and the S&P 500

index.

Opportunity S&P 500

Year Fund Return Return

2009 76.0% 26.5%

2010 16.6% 15.1%

2011 –34.9% 2.11%

2012 39.6% 16.0%

Calculate the average annual return of the Opportunity fund and the S&P 500. Which performed better

over this period? If you had invested $1,000 in each investment at the beginning of 2009, how much money

would you have in each investment at the end of 2012? Calculate the standard deviation of the Opportunity

fund’s return and those of the S&P 500. Which is more volatile?

Average annual return of the Opportunity fund = (76.0% + 16.6% − 34.9% + 39.6%) / 4 = 97.30% / 4 = 24.33%

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 148

Answers to Review Questions

1. Risk is defined as the chance of financial loss, as measured by the variability of expected returns associated

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 149

2. The return on an investment (total gain or loss) is the change in value plus any cash distributions over a

defined time period. It is expressed as a percent of the beginning-of-the-period investment. The formula is:

[(ending value initial value) cash distribution]

Return initial value

– +

=

Realized return requires the asset to be purchased and sold during the time periods the return is measured.

Unrealized return is the return that could have been realized if the asset had been purchased and sold during

the time period the return was measured.

3. a. The risk-averse financial manager requires an increase in return for a given increase in risk.

4. Scenario analysis evaluates asset risk by using more than one possible set of returns to obtain a sense of the

5. The decision maker can get an estimate of project risk by viewing a plot of the probability distribution, which

6. The standard deviation of a distribution of asset returns is an absolute measure of dispersion of risk around

7. The coefficient of variation is another indicator of asset risk; however, this measures relative dispersion. It is

8. An efficient portfolio is one that maximizes return for a given risk level or minimizes risk for a given level of

1

ˆ ˆ

n

p j j

j

r w r

=

= ´

å

where:

j

r

$

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 150

2

1

( )

( 1)

n

i

rp

i

r r

n

s

=

–

=–

å

9. The correlation between asset returns is important when evaluating the effect of a new asset on the portfolio’s

overall risk. Returns on different assets moving in the same direction are positively correlated, while those

10. The inclusion of foreign assets in a domestic company’s portfolio reduces risk for two reasons. When returns

11. The total risk of a security is the combination of nondiversifiable risk and diversifiable risk. Diversifiable risk

refers to the portion of an asset’s risk attributable to firm-specific, random events (strikes, litigation, loss of

12. Beta measures nondiversifiable risk. It is an index of the degree of movement of an asset’s return in response

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 151

13. The equation for the capital asset pricing model is:

rj RF [bj(rm RF)],

where:

14. a. If there is an increase in inflationary expectations, the security market line will show a parallel shift

Suggested Answer to Focus on Ethics Box:

If It Sounds Too Good to Be True, It Probably Is

What are some hazards of allowing investors to pursue claims based on their most recent accounts

statements?

Allowing claims based on fraudulent statements reduces investors’ incentive to perform due diligence. If investors

Suggested Answer to Global Focus Box:

An International Flavor to Risk Reduction

International mutual funds do not include any domestic assets, whereas global mutual funds include both

foreign and domestic assets. How might this difference affect their correlation with U.S. equity mutual

funds?

The difference between global funds and international funds is that global funds can invest in stocks and bonds

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 152

Answers to Warm-Up Exercises

E8-1. Total annual return

E8-2. Expected return

Answer:

Analyst Probability Return Weighted Value

1 0.35 5% 1.75%

E8-3. Comparing the risk of two investments

E8-4. Computing the expected return of a portfolio

E8-5. Calculating a portfolio beta

Answer:

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 153

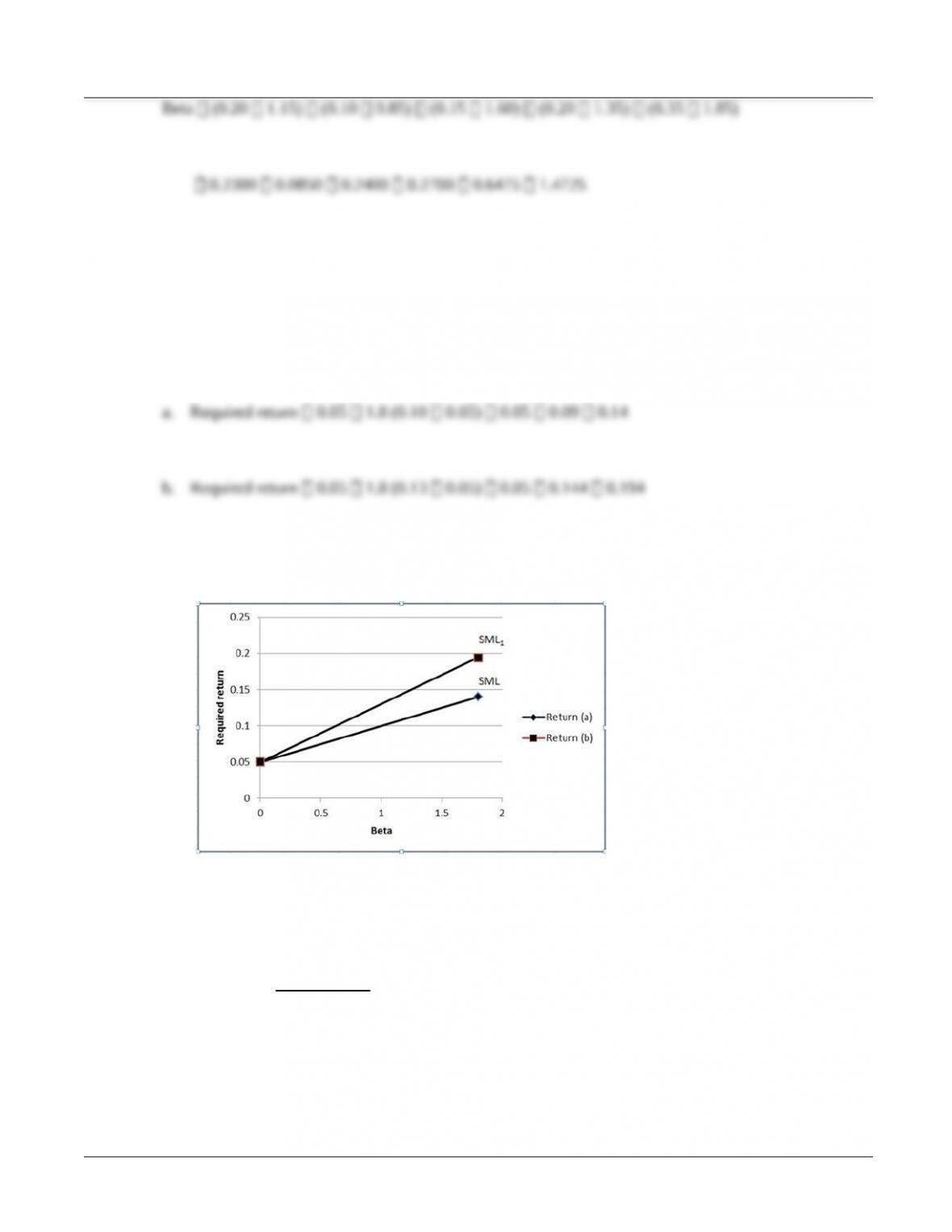

E8-6. Calculating the required rate of return

Answer:

c. Although the risk-free rate does not change, as the market return increases, the required return on

the asset rises by 180% of the change in the market’s return.

Solutions to Problems

P8-1. Rate of return:

1

1

( )

t

t t t

t

P P C

r = P

–

––

+

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 154

LG 1; Basic

P8-2. Return calculations:

1

1

( )

t t t

tt

P P C

r = P

––

–

+

LG 1; Basic

Investment Calculation rt(%)

A ($100 $800 $1,100) $800 −164.00

P8-3. Risk preferences

LG 1; Intermediate

a. The risk-neutral manager would accept Investments X and Y because these have higher returns than

b. The risk-averse manager would accept Investment X because it provides the highest return and has the

c. The risk-seeking manager would accept Investments Y and Z because he or she is willing to take

d. Traditionally, financial managers are risk averse and would choose Investment X because it provides

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 155

P8-4. Risk analysis

LG 2; Intermediate

a.

Expansion Range

A 24% 16% 8%

b. Project A is less risky because the range of outcomes for A is smaller than the range for Project B.

c. Because the most likely return for both projects is 20% and the initial investments are equal, the

d. The answer is no longer clear because it now involves a risk-return tradeoff. Project B has a slightly

P8-5. Risk and probability

LG 2; Intermediate

a.

Camera Range

R 30% 20% 10%

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 156

b.

Possible

Outcomes

Probability

Pri

Expected Return

ri

Weighted

Value (%)(ri Pri)

Camera R Pessimistic 0.25 20 5.00%

Camera S Pessimistic 0.20 15 3.00%

c. Camera S is considered more risky than Camera R because it has a much broader range of outcomes.

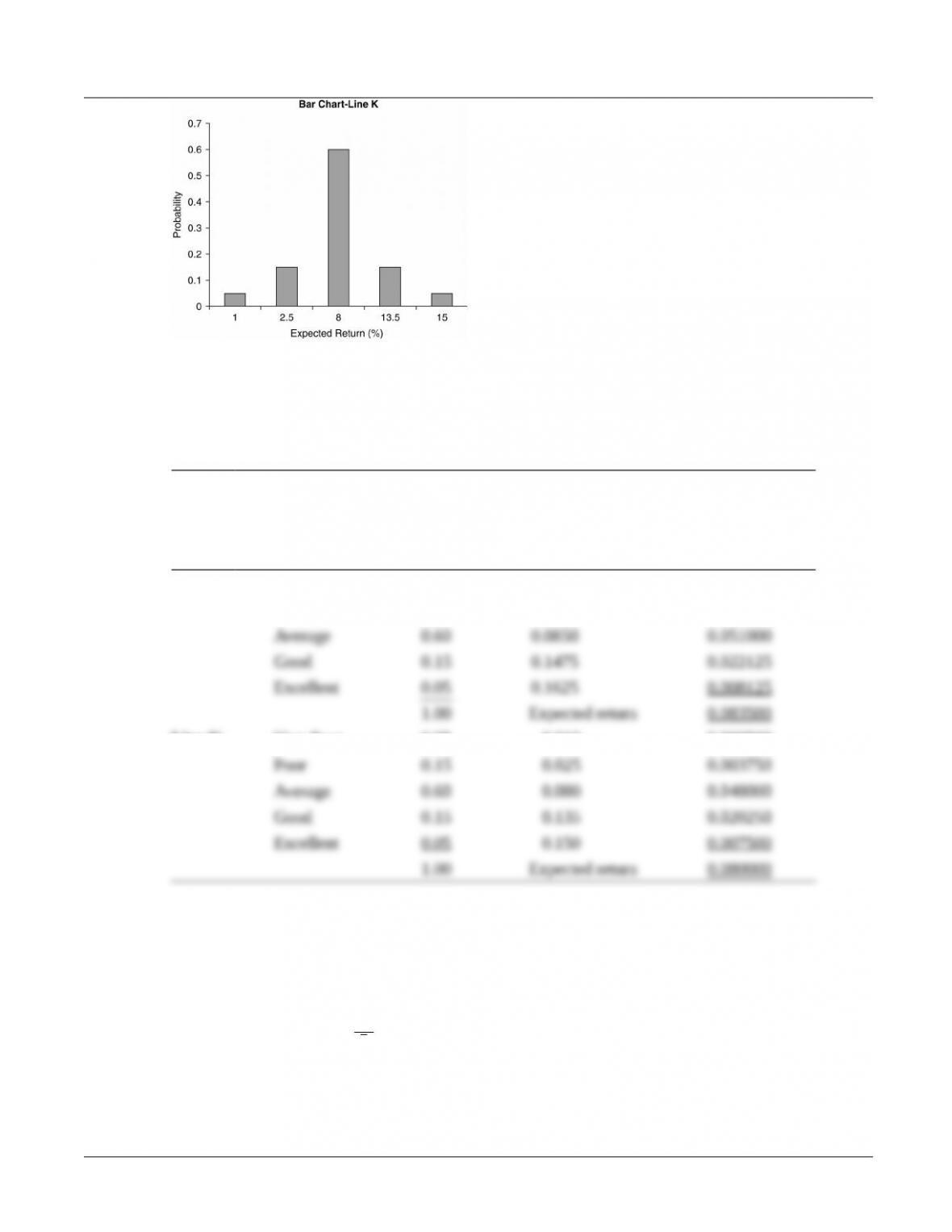

P8-6. Bar charts and risk

LG 2; Intermediate

a.

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 157

b.

Market

Acceptance

Probability

Pri

Expected Return

ri

Weighted Value

(ri Pri)

Line J Very Poor 0.05 0.0075 0.000375

Poor 0.15 0.0125 0.001875

Line K Very Poor 0.05 0.010 0.000500

c. Line K appears less risky due to a slightly tighter distribution than line J, indicating a lower range of

outcomes.

P8-7. Coefficient of variation:

r

CV r

s

=

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 158

LG 2; Basic

a. A

7% 0.3500

20%

A

CV = =

B

9.5% 0.4318

22%

B

CV = =

C

6% 0.3158

19%

C

CV = =

D

5.5% 0.3438

16%

D

CV = =

b. Asset C has the lowest coefficient of variation and is the least risky relative to the other choices.

P8-8. Standard deviation versus coefficient of variation as measures of risk

LG 2; Basic

a. Project A is least risky based on range with a value of 0.04.

b. Project A has the lowest standard deviation. The standard deviation measure fails to take into account

c. A

0.029 0.2417

0.12

A

CV = =

B

0.032 0.2560

0.125

B

CV = =

C

0.035 0.2692

0.13

C

CV = =

D

0.030 0.2344

0.128

D

CV = =

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 159

P8-9. Personal finance: Rate of return, standard deviation, coefficient of variation

LG 2; Challenge

a. Stock Price Variance

Year

Beginnin

g End Returns (Return–Average Return) 2

2012

14.36

21.55

50.07%

0.0495

b. Average return 72.31%

c. Sum of variances 2.2692

© 2015 Pearson Education, Inc.

Chapter 8 Risk and Return 160

d. 1.20 Coefficient of variation

e. The stock price of Hi-Tech, Inc. has definitely gone through some major price changes

© 2015 Pearson Education, Inc.