P7-13. Personal finance: Common stock value—variable growth

LG 4; Challenge

P0

0 1

1

(1 )

(1 )

N t

t

ts

D g

r

=

´ +

+

å

1

2

1

(1 ) ( )

N

N

s s

D

r r g

+

´

+ –

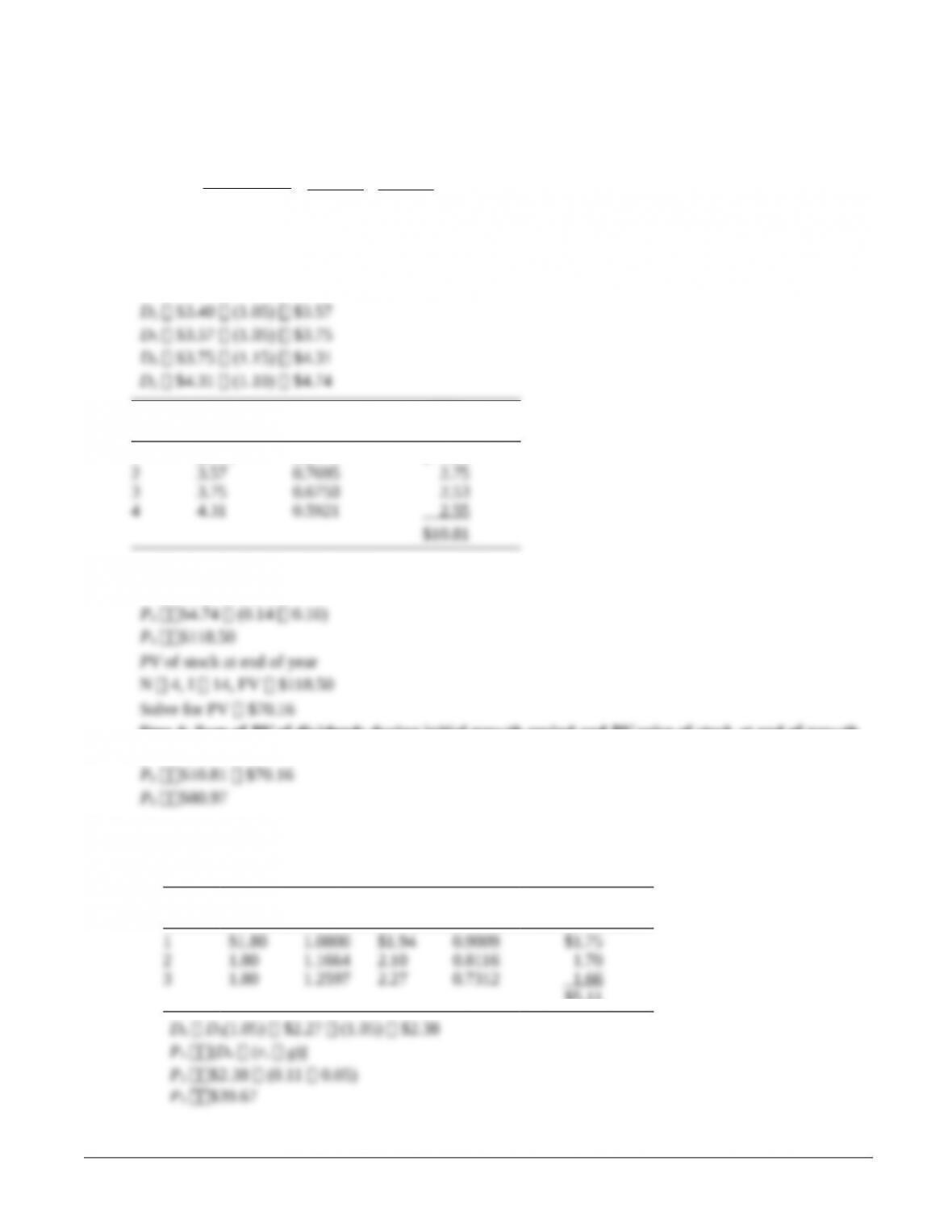

P0 PV of dividends during initial growth period PV of price of stock at end of growth period.

Steps 1 and 2: Value of cash dividends and PV of annual dividends

D1 $3.40 (1.00) $3.40

t Dt1/(1.14)t

PV

of Dividends

1 $3.40 0.8772 $ 2.98

Step 3: PV of price of stock at end of initial growth period

P4 [D5 (rs g)]

Step 4: Sum of PV of dividends during initial growth period and PV price of stock at end of growth

period

P7-14. Common stock value—variable growth

LG 4; Challenge

a.

t D01.08tDt1/(1.11)t

PV

of Dividends

$5.11

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 128

PV of stock at end of year 3

b. The PV of the first 3 year’s dividends is the same as in part a.

c. The PV of the first 3 year’s dividends is the same as in part a.

D4 D3(1.10) 2.50

P7-15. Personal finance: Common stock value—all growth models

LG 4; Challenge

a. P0 (CF0 r)

c. Steps 1 and 2: Value of cash dividends and PV of annual dividends

t D01.12tDt1/(1.18)t

PV

of Dividends

$78,626.83

Step 3: PV of price of stock at end of initial growth period

D2 1 $53,312 (1 0.07)

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 129

Step 4: Sum of PV of dividends during initial growth period and PV price of stock at end of growth

period

P7-16. Free cash flow (FCF) valuation

LG 5; Challenge

a. The value of the total firm is accomplished in three steps.

(1) Calculate the PV of FCF from 2021 to infinity.

(2) Add the PV of the cash flow obtained in (1) to the cash flow for 2020.

(3) Find the PV of the cash flows for 2016 through 2020.

Year FCF 1/(1.11)tPV

2016 $200,000 0.9009 $ 180,180

b. Calculate the value of the common stock.

c. Value per share $2,151,874 200,000 shares $10.76

P7-17. Personal finance: Using the free cash flow valuation model to price an IPO

LG 5; Challenge

a. The value of the firm’s common stock is accomplished in four steps.

(1) Calculate the PV of FCF from 2020 to infinity.

Year FCF 1/(1.08)tPV

2016 $700,000 0.9259 $ 648,130

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 130

(4) Calculate the value of the common stock using Equation 7.8.

b. Based on this analysis, the IPO price of the stock is over valued by $0.74 ($12.50 $11.76), and you

should not buy the stock.

c. The revised value of the firm’s common stock is calculated in four steps.

(1) Calculate the PV of FCF from 2020 to infinity.

(2) Add the PV of the cash flow obtained in (1) to the cash flow for 2019.

(3) Find the PV of the cash flows for 2016 through 2019.

Year FCF 1/(1.08)tPV

2016 $700,000 0.9259 $ 648,130

(4) Calculate the value of the common stock using Equation 7.8.

VS VC VD VP

P7-18. Book and liquidation value

LG 5; Intermediate

a. Book value per share:

Book value of assets (liabilities + preferred stock at book value)

number of shares outstanding

–

$780,000 $420,000

Book value per share $36 per share

10,000

–

= =

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 131

b. Liquidation value:

Cash $40,000 Liquidation Value of Assets 722,000

Marketable

Liquidation value of assets

Liquidation value per share Number of shares outstanding

=

$302,000

Liquidation value per share $30.20 per share

10,000

= =

c. Liquidation value is below book value per share and represents the minimum value for the firm. It is

P7-19. Valuation with price/earnings multiples

LG 5; Basic

Firm EPS P/EStock Price

A 3.0 (6.2) $18.60

P7-20. Management action and stock value

LG 6; Intermediate

a. P0 $3.15 (0.15 0.05) $31.50

P7-21. Integrative—risk and valuation and CAPM formulas

LG 4, 6; Intermediate

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 132

P7-22. Integrative—risk and valuation

LG 4, 6; Challenge

a. 14.8% 10% 4%

b. N 6, PV $1.73, FV $2.45

c. A decrease in the risk premium would decrease the required rate of return, which in turn would

increase the price of the stock.

P7-23. Integrative—risk and valuation

LG 4, 6; Challenge

a. Estimate growth rate:

b. (1) rs 0.14

(2) rs

P7-24. Ethics problem

LG 4; Intermediate

a. This is a zero-growth dividend valuation problem, so

b. Using the new discount rate of 12% (11% 1% credibility risk premium), we have

The value decline is the difference between parts a and b:

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 133

Case

Case studies are available on www.myfinancelab.com.

Assessing the Impact of Suarez Manufacturing’s Proposed Risky Investment on Its

Stock Value

a. Current per-share value of common stock growth rate of dividends:

Chapter 7 Stock Valuation 134

Spreadsheet Exercise

The answer to Chapter 7’s Azure Corporation spreadsheet problem is located on the Instructor’s Resource Center

at www.pearsonhighered.com/irc under the Instructor’s Manual.

Group Exercise

Group exercises are available on www.myfinancelab.com.

This chapter’s exercise takes the groups back to the future. The semester began with the fictitious firms having

Integrative Case 3: Encore International

This case focuses on the valuation of a firm. The student explores various methods of valuation, including the

a.

$60,000,000

Book value per share $24

2,500,000

= =

b.

$40

/ ratio 6.4

$6.25

P E = =

c. (1) rs RF risk premiumEncore

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 135

As risk premiums rise, required return also rises.

d. Zero growth:

1

0

s

D

Pr

=

0

$4.00 $25

0.16

P= =

e. (1) Constant growth:

1

0

( )

s

D

Pr g

=–

0

($4.00 1.06) $4.24 $42.40

(0.16 0.06) 0.10

P´

= = =

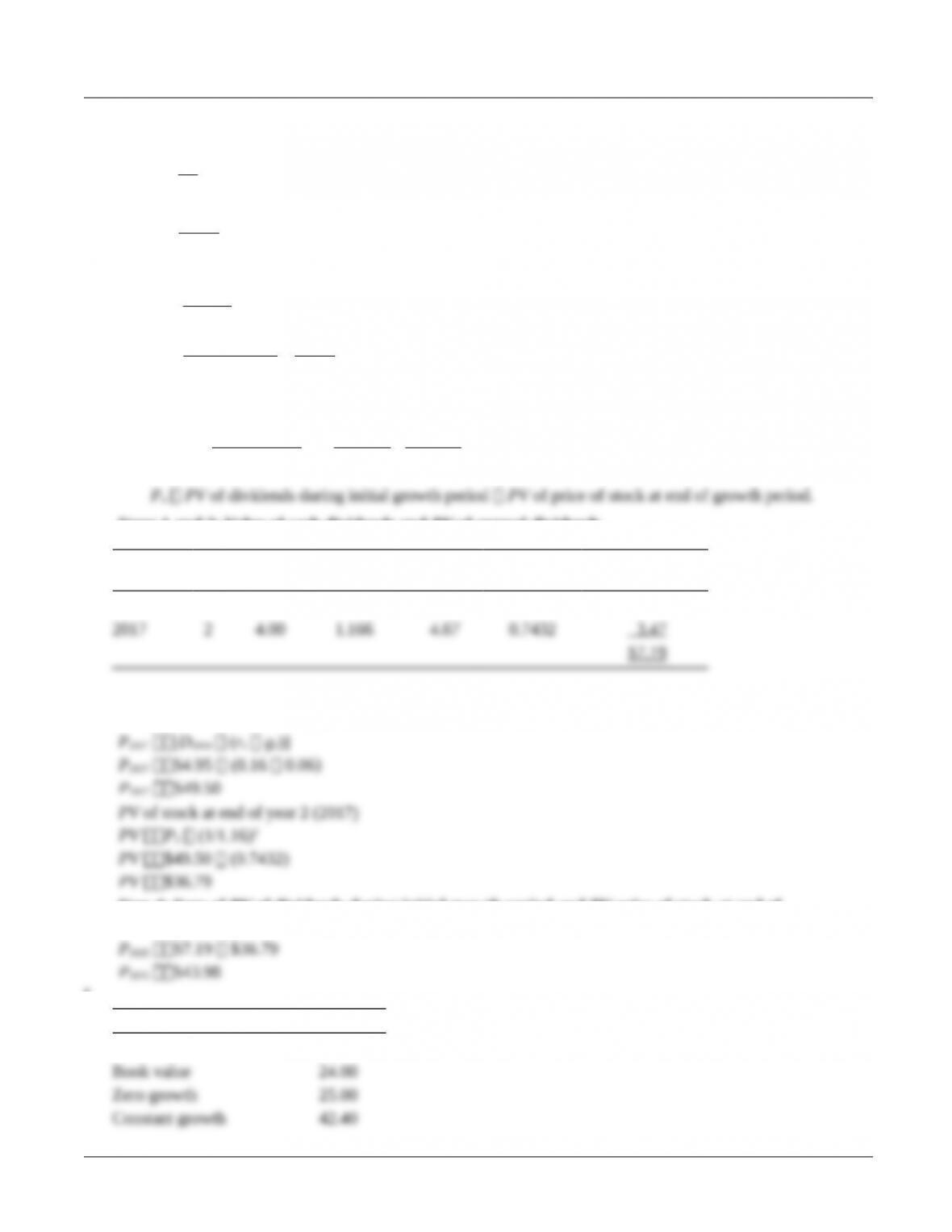

–

(2) Variable growth model: PV of dividends

1

0 1

0

12

(1 ) 1

(1 ) (1 ) ( )

nN

N

ts s s

D g t D

Pr t r r g

+

=

æ ö é ù

´ +

= + ´

ç ÷ ê ú

+ + –

è ø ë û

å

Steps 1 and 2: Value of cash dividends and PV of annual dividends

Year t D01.08tDt1/1.16t

PV

of Dividends

2016 1 $4.00 1.080 $4.32 0.8621 $3.72

Step 3: PV of price of stock at end of initial growth period

D2018 $4.67 (1 .06) $4.95

Step 4: Sum of PV of dividends during initial growth period and PV price of stock at end of

growth period

f.

Valuation Method Per Share

Market value $40.00

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 136

Variable growth 43.98

© 2015 Pearson Education, Inc.