Chapter 7

Stock Valuation

Instructor’s Resources

Overview

This chapter continues on the valuation process introduced in Chapter 6 for bonds. Models for valuing preferred

and common stock are presented. For common stock, the zero growth, constant growth, and variable growth

models are examined. The relationship between stock valuation and efficient markets is presented. The role of

venture capitalists and investment bankers is also discussed. The free cash flow model is explained and compared

with the dividend discount models. Other approaches to common stock valuation and their shortcomings are

explained. The chapter ends with a discussion of the interrelationship between financial decisions, expected return,

risk, and a firm’s value. Stock valuation from the perspective of the one’s professional life is contrasted with stock

valuation from a personal perspective.

Suggested Answer to Opener-in-Review Question

Tesla Motors shares were initially offered to investors at $17. Three years later the price was $90 per share.

What was the compound annual return that Tesla investors owned over this period? Given that Tesla paid

no dividends and was not expect to start paying dividends anytime soon, what method might analysts have

used to value the company’s shares in 2013? The company sold 13.3 million shares in its IPO with a par

value of $0.001 per share. How much paid-in capital did Tesla record on its balance sheet as a result of the

IPO? Do you think the highly favorable Consumer Reports review of the Model S boosted Tesla’s stock

primarily because the review reduced the company’s risk or because it boosted expected cash flows?

Compound annual return = ($90 ÷ $17)1/3 − 1 = 74.29%

Answers to Review Questions

1. Equity capital is permanent capital representing ownership, while debt capital represents a loan that must be

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 128

2. Common stockholders are the true owners of the firm because they invest in the firm only upon the

3. Rights offerings protect against dilution of ownership by allowing existing stockholders to purchase

4. Authorized shares are stated in a company’s corporate charter that specifies the maximum number of shares

5. Issuing stock outside of their home markets can benefit corporations by broadening the investor base and also

allowing them to become better integrated into the local business scene. A local stock listing both increases

6. Preferred stockholders have a fixed claim on a firm’s income that takes precedence over the claim of common

7. Cumulative preferred stock gives the holder the right to receive any dividends in arrears prior to the payment

8. Venture capitalists (VC) are typically business entities that are organized for the purpose of investing in

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 129

9. Institutional venture capitalists are most commonly organized in one of four ways.

10. The general steps that a private firm must go through to go public via an IPO are listed below.

11. The investment banker’s (IB) main activity is to underwrite the issue. In addition to underwriting, the IB

12. The efficient market hypothesis says that in an efficient market, investors would buy an asset if the expected

13. According to the efficient market hypothesis:

a. Securities prices are in equilibrium (fairly priced with expected returns equal to required returns);

b. Securities prices fully reflect all public information available and will react quickly to new information;

and

c. Investors should therefore not waste time searching for mispriced (over- or undervalued) securities.

The efficient market hypothesis is generally accepted as being reasonable for securities traded on major

14. a. The zero growth model of common stock valuation assumes a constant, nongrowing dividend stream. The

stock is valued as a perpetuity and discounted at a rate rs:

0s

P D r= ¸

b. The constant growth model of common stock valuation, also called the Gordon model, assumes that

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 130

1

0

s

D

Pr g

=–

c. The variable growth model of common stock valuation assumes that dividends grow at a variable rate.

1

0 1

0

12

(1 ) 1

(1 ) (1 ) ( )

N t N

t N

ts s s

D

D g

Pr r r g

+

=

æ ö

´ +

= + ´

ç ÷

+ + –

è ø

å

15. The free cash flow valuation model takes the PV of all future free cash flows of a firm. Because this PV

16. a. Book value is the value of the stock in the event all assets are liquidated for their book value and the

b. Liquidation value is the actual amount each common stockholder would expect to receive if the firm’s

c. Price earnings multiples are another way to estimate common stock value. The share value is estimated

17. A decision or action by the financial manager can have an effect on the risk and expected return of the stock,

18. CAPM: rs RF [bj (rm RF)] and bj 1.00:

a. As the risk premium increases, required return increases and stock price falls.

b. As the risk-free rate declines, the required return would also decline. Substituting ks into the Gordon

c. As D1 decreases, the P0 also decreases since the numerator in the dividend valuation models will decline.

d. As g increases, the P0 also increases. In the Gordon growth model the value of (r g) in the denominator

Suggested Answer to Focus on Practice Box: Understanding Human

Behavior Helps Us Understand Investor Behavior

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 131

Theories of behavioral finance can apply to other areas of human behavior in addition to investing. Think of

a situation in which you may have demonstrated one of these behaviors. Share with a classmate.

Student answers will vary. Examples:

Suggested Answer to Focus on Ethics Box: Understanding:

Psst! Have You Heard Any Good Quarterly Earnings Forecasts Lately?

What temptations might managers face if they have provided earnings guidance to investors and later find

it difficult to meet the expectations that they helped create?

The real costs associated with providing quarterly guidance include direct costs such as the time senior

Answers to Warm-Up Exercises

E7-1. Using debt ratio to calculate a firm’s total liabilities

Answer:

Debt ratio total liabilities total assets= ¸

Total liabilities debt ratio total assets

0.75 $5,200,000 $3,900,000

= ´

= ´ =

E7-2. Determining net proceeds from the sale of stock

Answer:

Net proceeds (1,000,000 $20 0.95) (250,000 $20 0.90)

$19,000,000 $4,500,000 $23,500,000

= ´ ´ + ´ ´

= + =

E7-3. Preferred and common stock dividends

E7-4. Price/earning ratios

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 132

Answer: Earnings per share (EPS) $11,200,000 4,600,000 $2.43 per share

E7-5. Using the zero-growth model to value stock

E7-6. Capital asset pricing model

Answer: Step 1: Calculate the required rate of return.

Solutions to Problems

P7-1. Authorized and available shares

LG 2; Basic

a. Maximum shares available for sale

b.

$48,000,000

Total shares needed 800,000 shares

$60

= =

c. Aspin must amend its corporate charter to authorize the issuance of additional shares.

P7-2. Preferred dividends

LG 2; Intermediate

a. $8.80 per year or $2.20 per quarter.

b. $2.20. For a noncumulative preferred only the latest dividend has to be paid before dividends can be

c. $8.80. For cumulative preferred all dividends in arrears must be paid before dividends can be paid on

common stock. In this case the board must pay the three dividends missed plus the current dividend.

P7-3. Preferred dividends

LG 2; Intermediate

Case Answer Explanation

© 2015 Pearson Education, Inc.

Chapter 7 Stock Valuation 133

P7-4. Convertible preferred stock

LG 2; Challenge

a. Conversion value conversion ratio stock price 5 $20 $100

b. Based on comparison of the preferred stock price versus the conversion value, the investor should

c. If the investor converts to common stock, she will begin receiving $1.00 per share per year

P7-5. Preferred stock valuation

LG 4; Basic

a. The annual dividend is 10% × $65 or $6.50

b. Because the dividend stream is a perpetuity, the value of stock is just the annual dividend divided by

c. To find the value of the shares in this case, recognize that the dividend stream will be identical to that

P7-6. Personal finance: common stock valuation—zero growth

LG 4; Intermediate

$5.00

Value of stock when purchased $31.25

0.16

$5.00

Value of stock when sold $41.67

0.12

Sally’s capital gain is $10.42 ($41.67 $31.25) per share.

Sally’s total capital gain is 100 $1,042.00.

= =

= =

–

´

P7-7. Preferred stock valuation: PS0 Dp rp

LG 4; Intermediate

a. PS0 $6.40 0.093

b. PS0 $6.40 0.105

The investor would lose $7.87 per share ($68.82 $60.95) because as the required rate of return on

Chapter 7 Stock Valuation 134

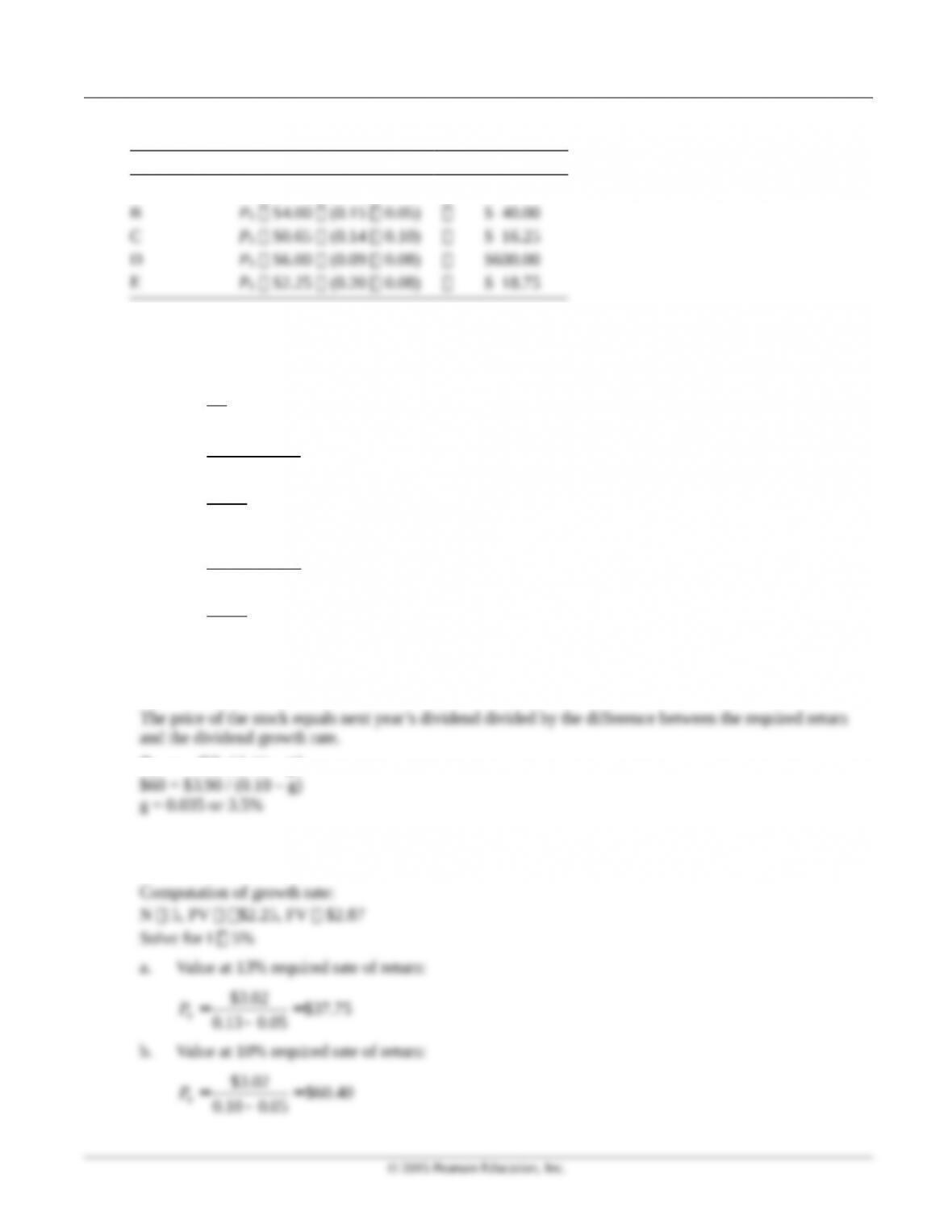

P7-8. Common stock value—constant growth: P0 D1 (rs g)

LG 4; Basic

Firm P0 D1 (rs g) Share Price

AP0 $1.20 (0.13 0.08) $ 24.00

P7-9. Common stock value—constant growth

LG 4; Intermediate

a.

1

0

$1.20 (1.05) 0.05

$28

$1.26 0.05 0.045 0.05 0.095 9.5%

$28

s

s

s

D

r g

P

r

r

= +

´

= +

= + = + = =

b.

$1.20 (1.10) 0.10

$28

$1.32 0.10 0.047 0.10 0.147 14.7%

$28

s

s

r

r

´

= +

= + = + = =

P7-10. Common stock value—constant growth:

LG 4; Intermediate

P0 = D1 / ( rs – g)

P7-11. Personal finance: Common stock value—constant growth: P0 D1 (rs g)

LG 4; Intermediate

Chapter 7 Stock Valuation 135

P7-12. Common stock value—variable growth:

LG 4; Challenge

Steps 1 and 2: Value of cash dividends and PV of annual dividends

t D01.25t Dt1/(1.15)tPV

of Dividends

1 $2.55 1.2500 $3.19 0.8696 $2.77

$9.05

Step 3: PV of price of stock at end of initial growth period

D3 1 $4.98 (1 0.10)

© 2015 Pearson Education, Inc.