Part 3

Valuation of Securities

Chapters in This Part

Chapter 6 Interest Rates and Bond Valuation

Chapter 7 Stock Valuation

Integrative Case 3: Encore International

© 2015 Pearson Education, Inc.

Chapter 6

Interest Rates and Bond Valuation

Instructor’s Resources

Overview

This chapter begins with a thorough discussion of interest rates, yield curves, and their relationship to required

returns. Features of the major types of bond issues are presented along with their legal issues, risk characteristics,

and indenture convents. The chapter then introduces students to the important concept of valuation and

demonstrates the impact of cash flows, timing, and risk on value. It explains models for valuing bonds and the

calculation of yield-to-maturity using either an approximate yield formula or calculator. Students learn how

interest rates may affect their ability to borrow and expand business operations or assets under personal control.

Suggested Answers to Opener-in-Review Questions

a. With short-term interest rates near 0 percent in 2013, suppose the Treasury decided to replace maturing

notes and bonds by issuing new Treasury bills, thus shortening the average maturity of U.S. debt

outstanding. Discuss the pros and cons of this strategy.

The U.S. Treasury would face many of the same considerations as those faced by a company that is considering

Another concern that the U.S. Treasury would have to face is whether the financing adjustment would diminish

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 107

b. The average maturity of outstanding U.S. Treasury debt is a little more than 5 years. Suppose a newly

issued 5-year Treasury note has a coupon rate of 2 percent and sells for par. What happens to the value

of this bond if the inflation rate rises 1 percentage point, causing the yield-to-maturity on the 5-year note

to jump to 3 percent shortly after it is issued?

Debt priced at par provides a coupon payment sufficient to pay the required rate of return. Hence, if the

c. Assume that the “average” Treasury security outstanding has the features described in part b. If total

U.S. debt is $16 trillion and an increase in inflation causes yields on Treasury securities to increase by 1

percentage point, by how much would the market value of outstanding debt fall? What does this suggest

about the incentives of government policy makers to pursue policies that could lead to higher inflation?

Based on the information provided in the Opener, a few calculations can lead us to an approximation for this

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 108

Answers to Review Questions

1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for

2. The term structure of interest rates is the relationship of the rate of return to the time to maturity for any class

3. For a given class of securities, the slope of the curve reflects an expectation about the movement of interest

4. a. According to the expectations theory, the yield curve reflects investor expectations about future interest

b. The liquidity preference theory is an explanation for the upward-sloping yield curve. This theory states

c. The market segmentation theory is another theory that can explain any of the three curve shapes. Because

5. In the Fisher equation, r r* IP RP, the risk premium, RP, consists of the following issuer- and

issue-related components:

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 109

The risks that are debt specific are default, maturity, and contractual provisions.

6. Most corporate bonds are issued in denominations of $1,000 with maturities of 10 to 30 years. The stated

7. Long-term lenders include restrictive covenants in loan agreements in order to place certain operating and/or

financial constraints on the borrower. These constraints are intended to assure the lender that the borrowing

Violation of any of the standard or restrictive loan provisions gives the lender the right to demand immediate

8. Short-term borrowing is normally less expensive than long-term borrowing due to the greater uncertainty

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 110

9. If a bond has a conversion feature, the bondholders have the option of converting the bond into a certain

10. Current yields are calculated by dividing the annual interest payment by the current price. Bonds are quoted

11. Eurobonds are bonds issued by an international borrower and sold to investors in countries with currencies

12. A financial manager must understand the valuation process in order to judge the value of benefits received

13. Three key inputs to the valuation process are

14. The valuation process applies to assets that provide an intermittent cash flow or even a single cash flow over

15. The value of any asset is the PV of future cash flows expected from the asset over the relevant time period.

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 111

16. The basic bond valuation equation for a bond that pays annual interest is:

0

1

1 1

(1 ) (1 )

n

t n

d d

t

V I M

r r

=

é ù é ù

= ´ + ´

ê ú ê ú

+ +

ë û

ë û

å

where:

a. The annual interest must be converted to semiannual interest by dividing by two.

b. The number of years to maturity must be multiplied by two.

c. The required return must be converted to a semiannual rate by dividing it by two.

17. A bond sells at a discount when the required return exceeds the coupon rate. A bond sells at a premium when

18. If the required return on a bond is constant until maturity and different from the coupon interest rate, the

19. To protect against the impact of rising interest rates, a risk-averse investor would prefer bonds with short

20. The yield-to-maturity (YTM) on a bond is the rate investors earn if they buy the bond at a specific price and

21. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

22. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

23. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

Suggested Answer to Focus on Practice Box:

I-Bonds Adjust for Inflation

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 112

What effect do you think the inflation-adjusted interest rate has on the cost of an I-bond in comparison with

similar bonds with no allowance for inflation?

The cost of the I-bond when issued is the face value ($25 or more). Because the bond has an inflation protection

feature, the Treasury Department can issue the I-bond at slightly lower interest rates than comparable bonds.

Suggested Answer to Focus on Ethics Box:

Can We Trust the Bond Raters?

What ethical issues may arise because the companies that issue bonds pay the rating agencies

to rate their bonds?

The rating agencies have an incentive to keep their customers (i.e., the issuers) happy in order to secure future

business. Some suggest that the relationship between the agencies’ and the issuers is one of the factors that

contributed to the subprime crisis. The concern is that rating agencies might hesitate to give low ratings, fearing

that bond issues would no longer pay to have their bonds rated.

Answers to Warm-Up Exercises

E6-1. Finding the real rate of interest

Answer: r* RF IP

E6-2. Yield curve

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 113

b. {(4.51% 10) (3.7% 5)} 5

d. Yield curves may slope up for many reasons beyond expectations of rising interest rates. According to

E6-3. Calculating inflation expectation

Answer: The inflation expectation for a specific maturity is the difference between the yield and the real interest

rate at that maturity.

Maturity Yield Real Rate of Interest Inflation Expectation

3 months 1.41% 0.80% 0.61%

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 114

E6-4. Real returns

Answer: A T-bill can experience a negative real return if its interest rate is less than the inflation rate as

E6-5. Calculating risk premium

Answer: We calculate the risk premium of other securities by subtracting the risk-free rate, 4.51%, from each

nominal interest rate.

Security Nominal interest rate Risk premium

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 115

E6-6. The basic valuation model

Answer: Find the PV of the cash flow stream for each asset by discounting the expected cash flows using the

Chapter 6 Interest Rates and Bond Valuation 116

E6-8. Bond valuations using required rates of return

Answer: a. Student answers will vary but any required rate of return above the coupon rate will cause the

b. Student answers will vary but should be consistent with their answers to part a.

Solutions to Problems

P6-1. Interest rate fundamentals: The real rate of return

LG1; Basic

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 117

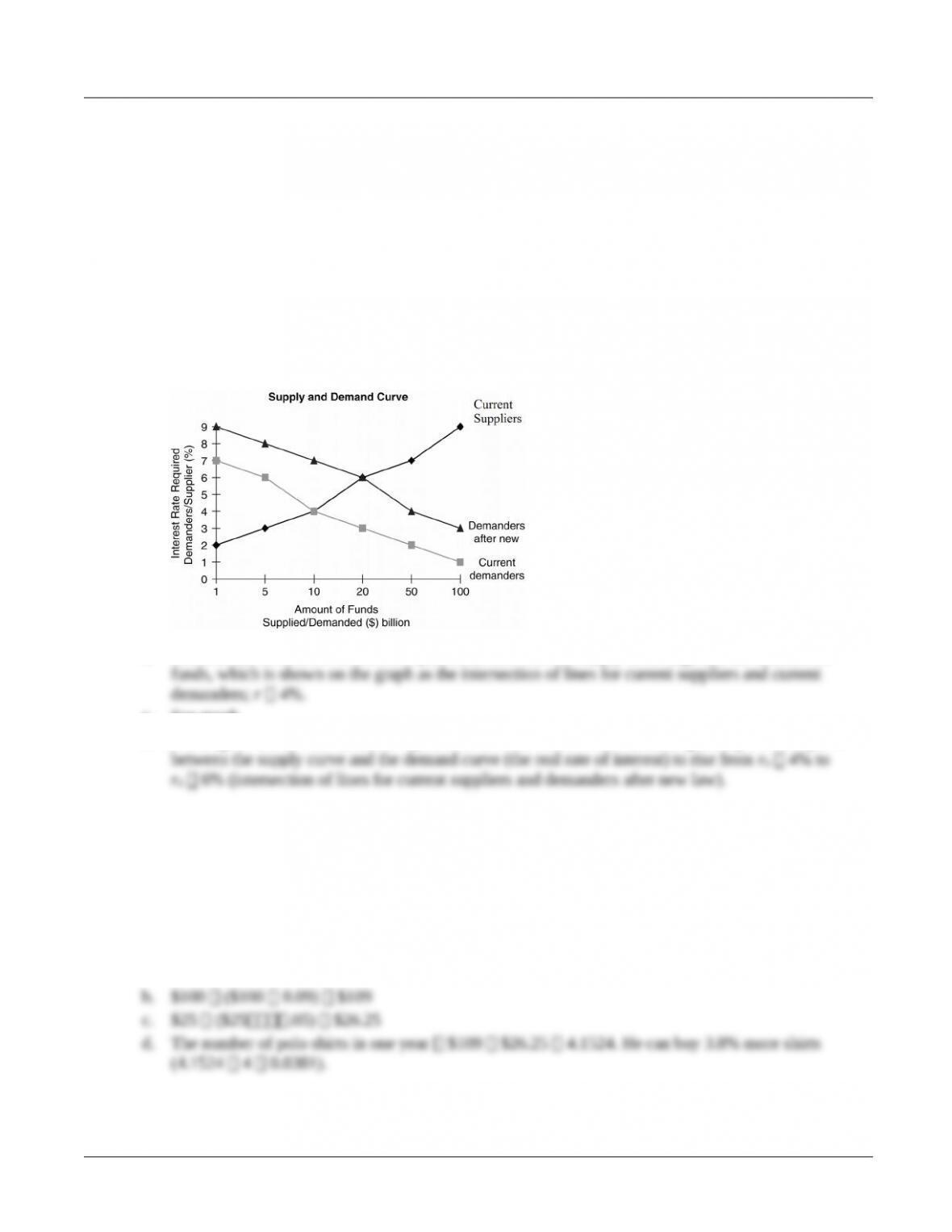

P6-2. Real rate of interest

LG 1; Intermediate

a.

b. The real rate of interest creates an equilibrium between the supply of savings and the demand for

c. See graph.

d. A change in the tax law causes an upward shift in the demand curve, causing the equilibrium point

P6-3. Personal finance: Real and nominal rates of interest

LG 1; Intermediate

a. Four shirts

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 118

e. The real rate of return is 9% 5% 4%. The change in the number of shirts that can be purchased is

determined by the real rate of return because the portion of the nominal return for expected inflation

(5%) is available just to maintain the ability to purchase the same number of shirts.

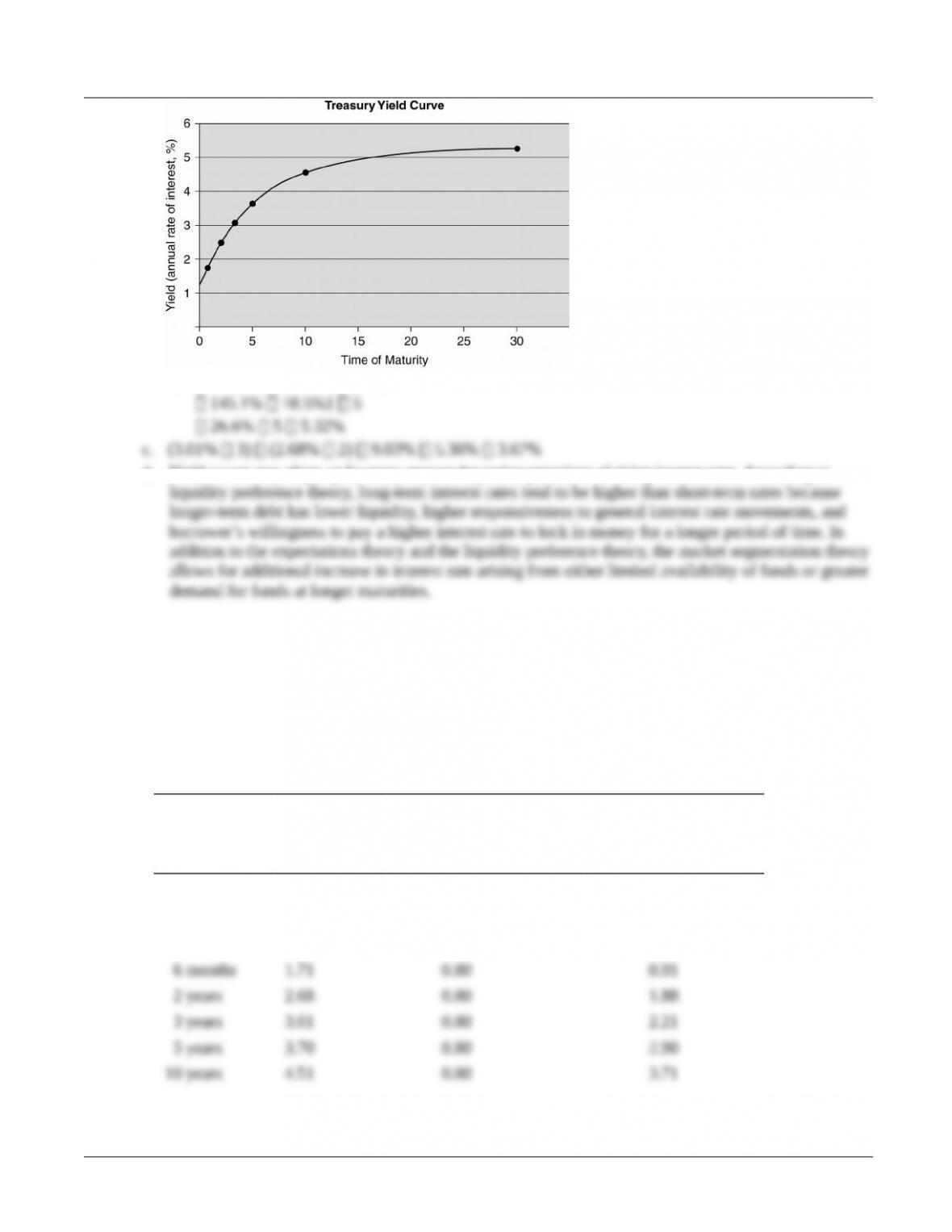

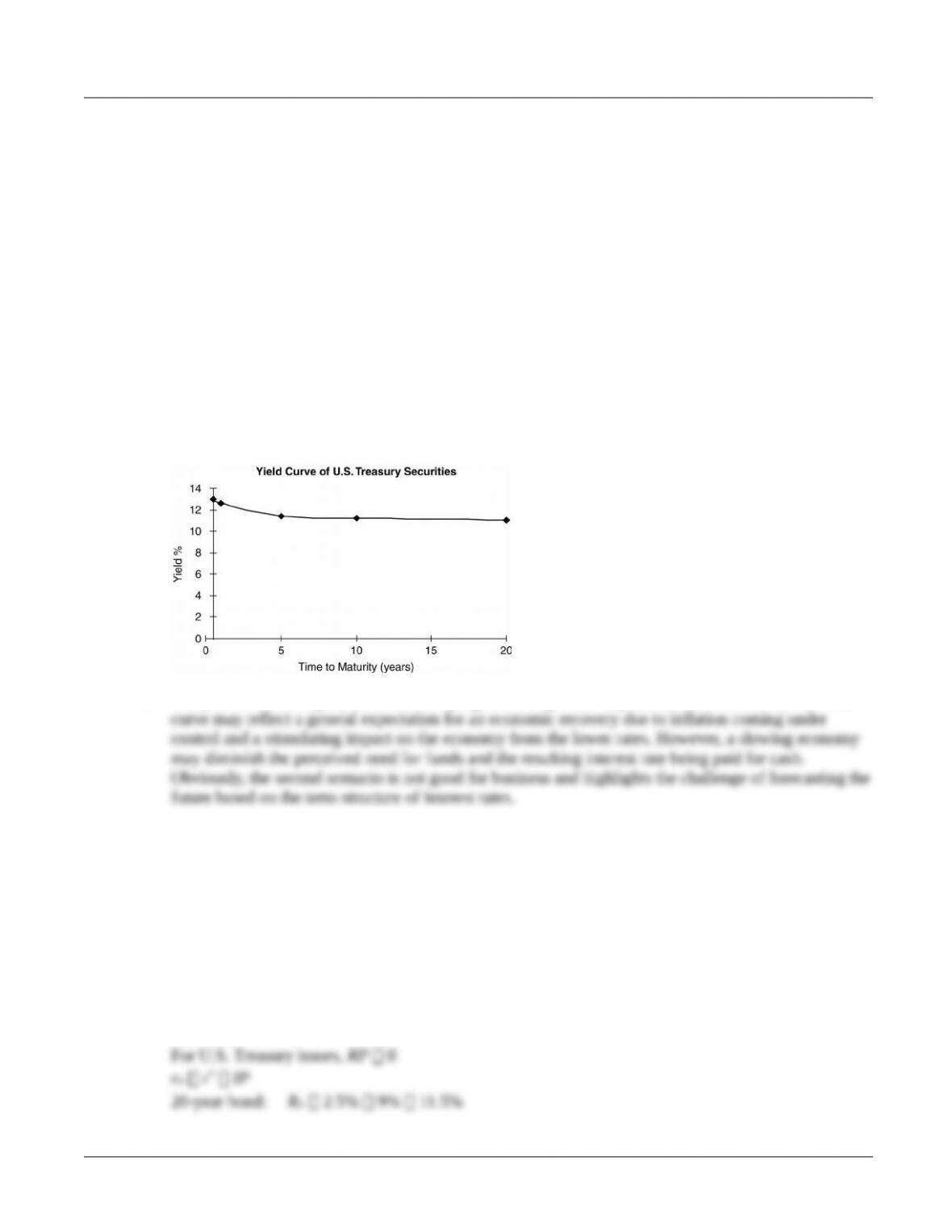

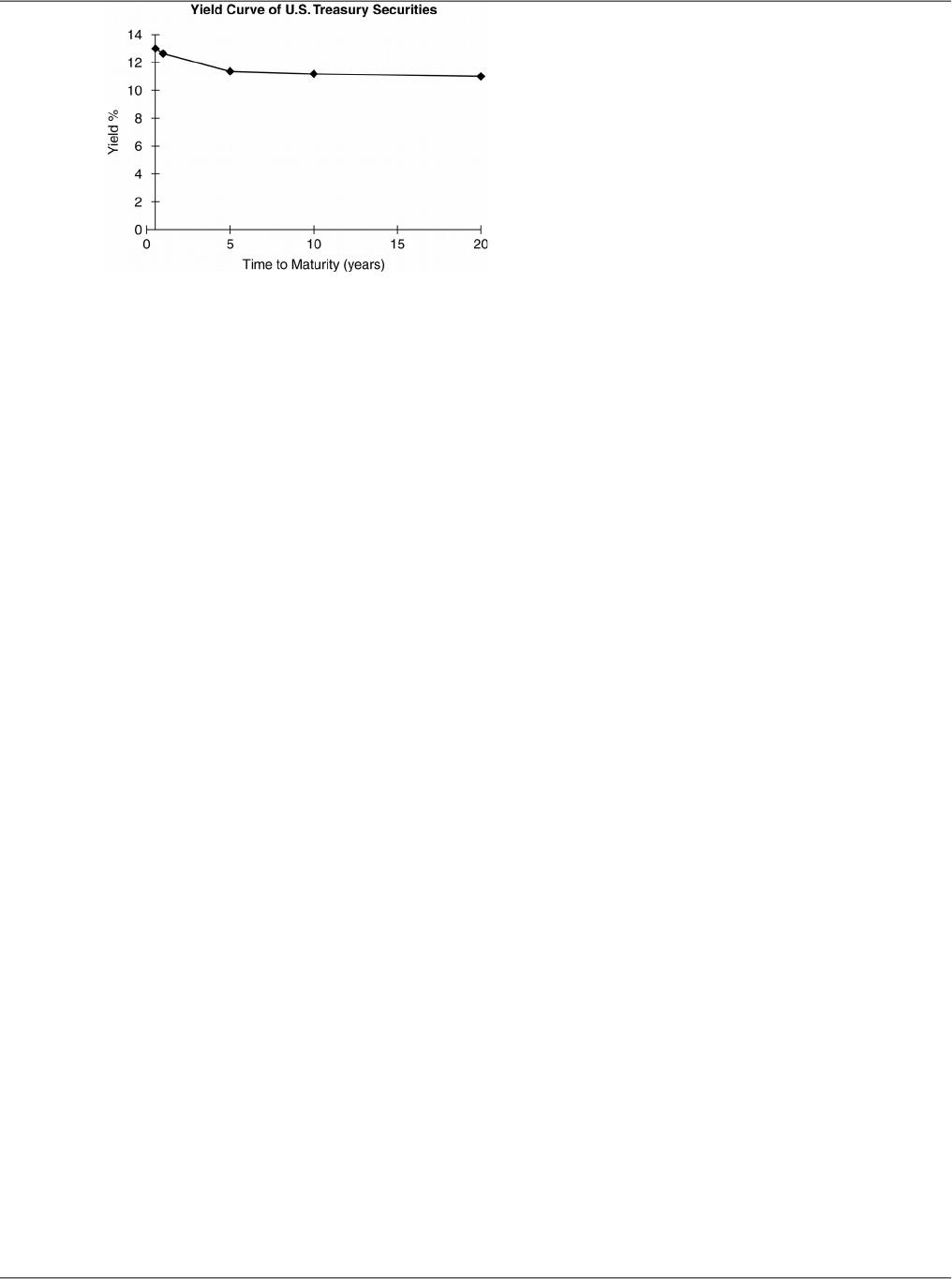

P6-4. Yield curve

LG 1; Intermediate

a.

b. The yield curve is slightly downward sloping, reflecting lower expected future rates of interest. The

P6-5. Nominal interest rates and yield curves

LG 1; Challenge

a. rl r* IP RP1

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 119

b. If the real rate of interest (r*) drops to 2.0%, the nominal interest rate in each case would decrease by

0.5% point.

c.

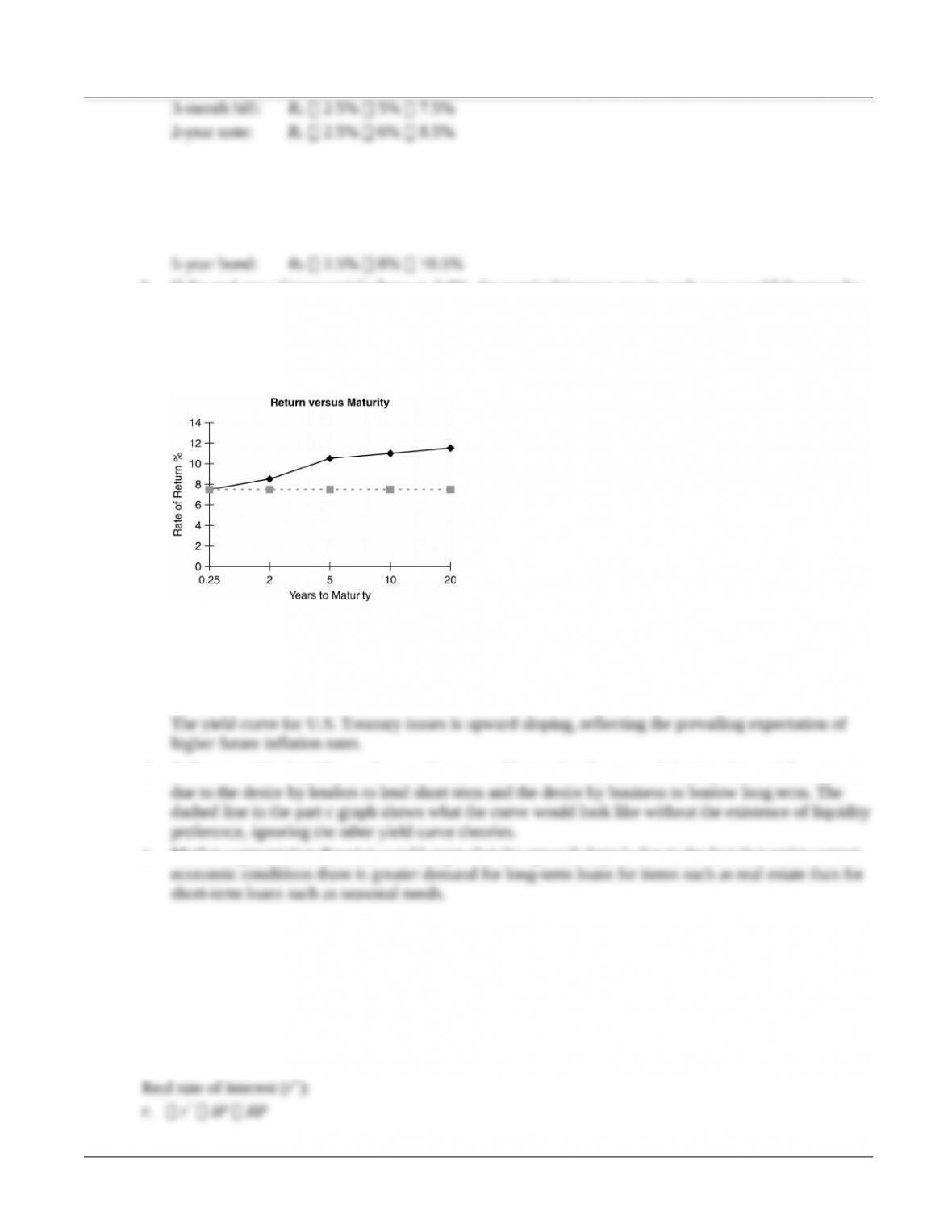

d. Followers of the liquidity preference theory would state that the upward-sloping shape of the curve is

e. Market segmentation theorists would argue that the upward slope is due to the fact that under current

P6-6. Nominal and real rates and yield curves

LG 1; Challenge

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 120

a.

Security

Nominal

Rate (rj) – IP

Real Rate of

Interest (r*)

A 12.6% – 9.5% 3.1%

b. The real rate of interest decreased from January to March, remained stable from March through

c.

© 2015 Pearson Education, Inc.

Chapter 6 Interest Rates and Bond Valuation 121

d. The yield curve is slightly downward sloping, reflecting lower expected future rates of interest. The

curve may reflect a current, general expectation for an economic recovery due to inflation coming

under control and a stimulating impact on the economy from the lower rates.

© 2015 Pearson Education, Inc.