P5-39. Personal finance: Compounding frequency and time value

LG 5; Challenge

a. (1) N 10; I 8%, PV $2,000 (2) N 20, I 4%, PV $2,000

b. (1) ieff (1 0.08/1)1 1 (2) ieff (1 0.08/2)2 1

c. Compounding continuously will result in $133 more dollars at the end of the 10-year period than

d. The more frequent the compounding, the larger the future value. This result is shown in part a by the

P5-40. Personal finance: Comparing compounding periods

LG 5; Challenge

a. (1) Annually: N 2, I 12%, PV $15,000

b. The future value of the deposit increases from $18,816 with annual compounding to $19,068.77 with

c. The maximum future value for this deposit is $19,068.77, resulting from continuous compounding, which

P5-41. Personal finance: Annuities and compounding

LG 3, 5; Intermediate

a.

(1) Annual

(2) Semiannual

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 76

(3) Quarterly

b. The sooner a deposit is made, the sooner the funds will be available to earn interest and contribute to

P5-42. Deposits to accumulate growing future sum

LG 6; Basic

Case Terms Calculation Payment

A12%, 3 yrs. N 3, I 12, FV $5,000 $1,481.74

P5-43. Personal finance: Creating a retirement fund

LG 6; Intermediate

P5-44. Personal finance: Accumulating a growing future sum

LG 6: Intermediate

Step 1: Determining the cost of a home in 20 years.

Step 2: Determining how much has to be saved annually to afford a home.

P5-45. Personal finance: Deposits to create a perpetuity

LG 3, 6; Intermediate

P5-46. Personal finance: Inflation, time value, and annual deposits

LG 2, 3, 6; Challenge

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 77

c. Because John will have an additional year on which to earn interest at the end of the 25 years, his

P5-47. Loan payment

LG 6; Basic

Loan

AN 3, I 8%, PV $12,000 BN 10, I 12%, PV $60,000

P5-48. Personal finance: Loan amortization schedule

LG 6; Intermediate

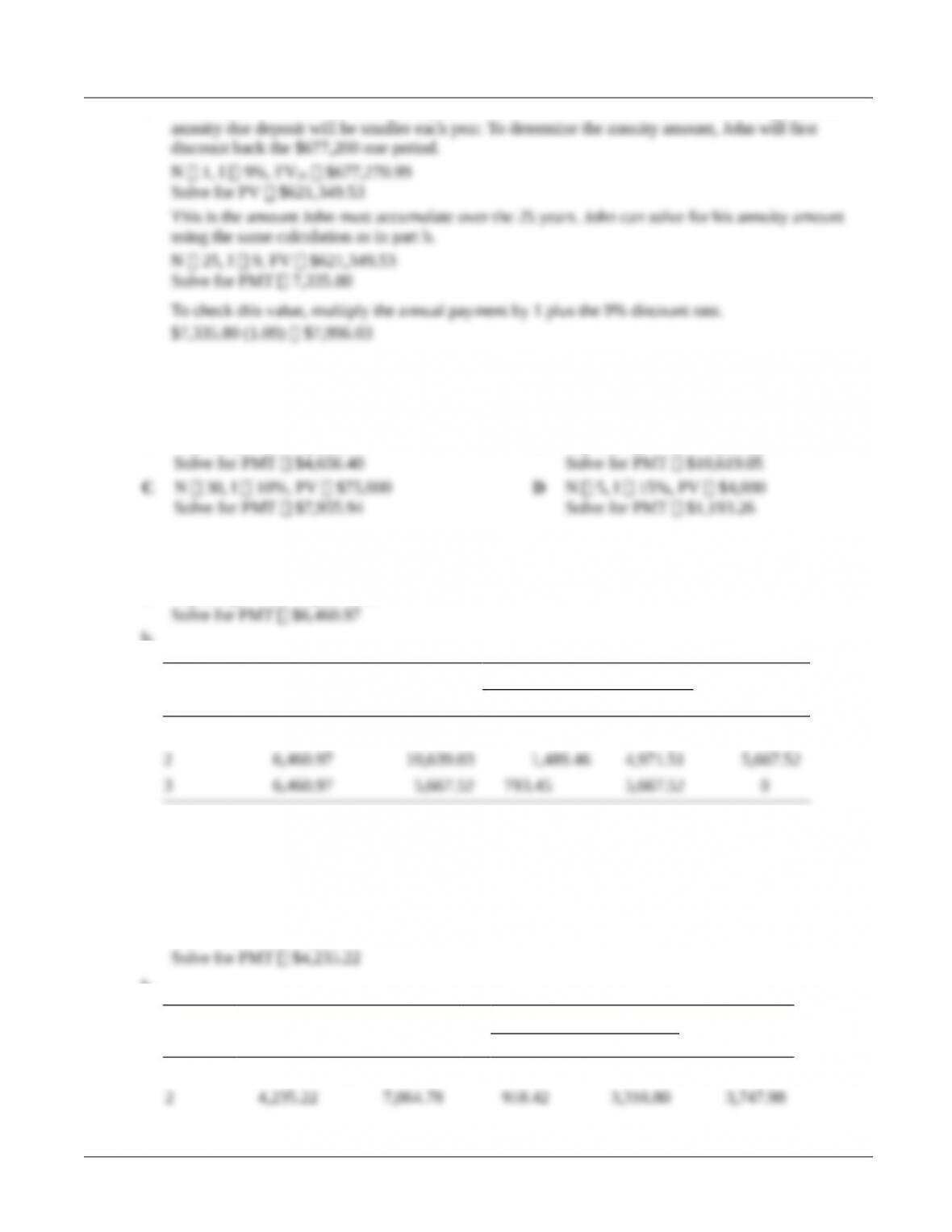

a. N 3, I 14%, PV $15,000

b.

End of

Year

Loan

Payment

Beginning-of-

Year Principal

Payments End-of-Year

Principal

Interest Principal

1 $6,460.97 $15,000.00 $2,100.00 $4,360.97 $10,639.03

c. Through annual end-of-the-year payments, the principal balance of the loan is declining, causing less

interest to be accrued on the balance.

P5-49. Loan interest deductions

LG 6; Challenge

a. N 3, I 13%, PV $10,000

b.

End of

Year

Loan

Payment

Beginning-of-

Year Principal

Payments End-of-Year

Principal

Interest Principal

1 $4,235.22 $10,000.00 $1,300.00 $2,935.22 $7,064.78

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 78

P5-50. Personal finance: Monthly loan payments

LG 6; Challenge

a. N 12 2 24, I 12%/12 1%, PV $4,000 ($4,500 500)

P5-51. Growth rates

LG 6; Basic

a. Case

AN 4, PV $500, FV $800.BN 9, PV $1,500, FV $2,280

b.

Case

c. The growth rate and the interest rate should be equal because they represent the same thing.

P5-52. Personal finance: Rate of return

LG 6, Intermediate

P5-53. Personal finance: Rate of return and investment choice

LG 6; Intermediate

b. Investment C provides the highest return of the four alternatives. Assuming equal risk for the

P5-54. Rate of return-annuity

LG 6; Basic

P5-55. Personal finance: Choosing the best annuity

LG 6; Intermediate

a. Annuity A Annuity B

N 20, PV $30,000, PMT $3,100 N 10, PV $25,000, PMT $3,900

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 79

Annuity C Annuity D

N 15, PV $40,000, PMT $4,200 N 12, PV $35,000, PMT 4,000

b. Annuity B gives the highest rate of return at 9% and would be the one selected based upon Raina’s

P5-56. Personal finance: Interest rate for an annuity

LG 6; Challenge

a. Defendants interest rate assumption

b. Prosecution interest rate assumption

c. N 25, I 9%, PV $2,000,000

P5-57. Personal finance: Loan rates of interest: PVAn PMT(PVIFAi%,n)

LG 6; Intermediate

a. Loan A Loan B

Loan C

b. Mr. Fleming should choose Loan B, which has the lowest interest rate.

P5-58. Number of years to equal future amount

LG 6; Intermediate

AI 7%, PV $300, FV $1,000 BI 5%, PV $12,000, FV $15,000

P5-59. Personal finance: Time to accumulate a given sum

LG 6; Intermediate

a. I 10%, PV $10,000, FV $20,000

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 80

P5-60. Number of years to provide a given return

LG 6; Intermediate

AI 11%, PV $1,000, PMT $250 BI 15%, PV $150,000, PMT $30,000

P5-61. Personal finance: Time to repay installment loan

LG 6; Intermediate

a. I 12%, PV $14,000, PMT $2,450

d. The higher the interest rate, the greater the number of time periods needed to repay the loan fully.

P5-62. Ethics problem

LG 6; Intermediate

This is a tough issue. Even back in the Middle Ages, scholars debated the idea of a “just price.” The

Case

Case studies are available on www.myfinancelab.com.

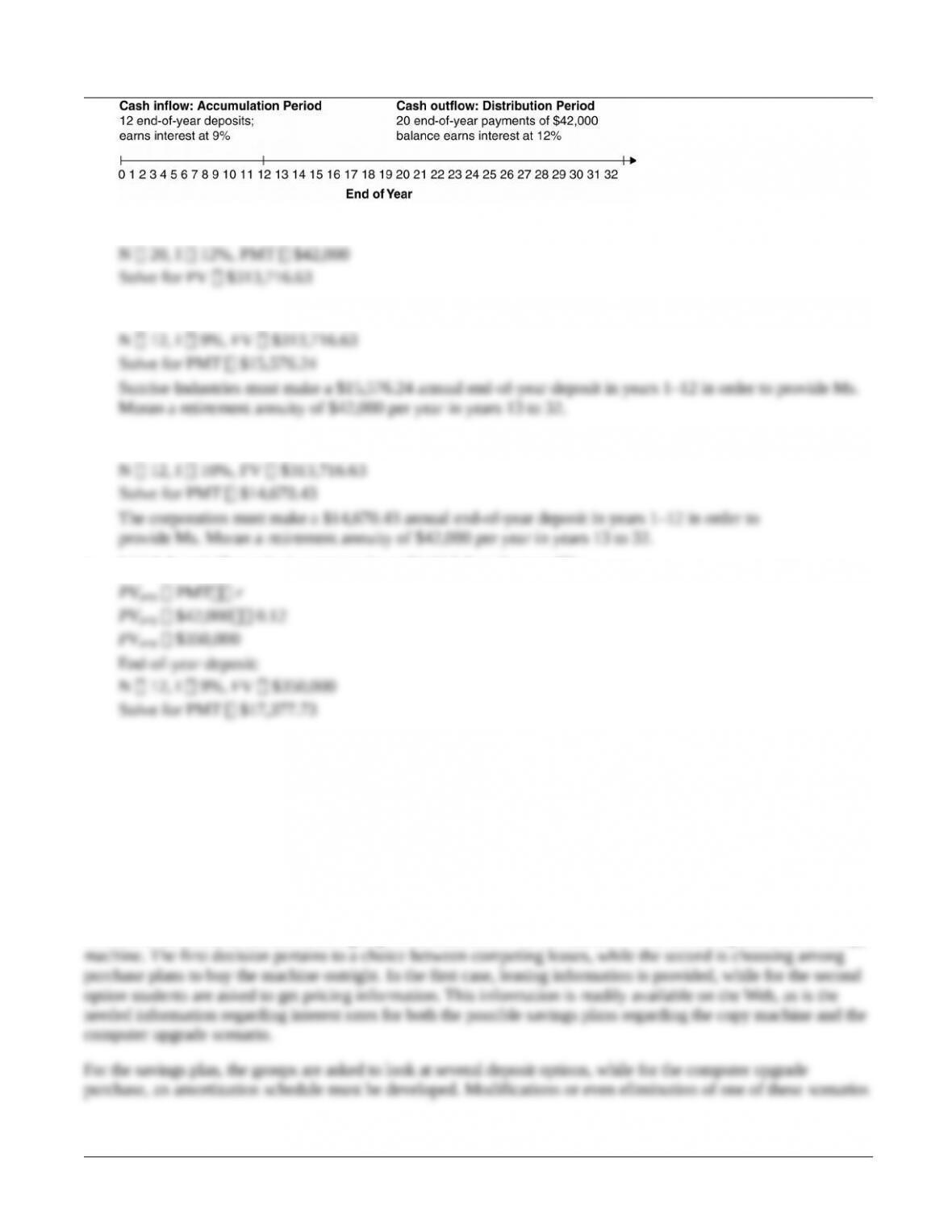

Finding Jill Moran’s Retirement Annuity

Chapter 5’s case challenges the student to apply present value and future value techniques to a real-world situation.

a.

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 81

b. Total amount to accumulate by end of year 12

c. End-of-year deposits at 9% interest

d. End-of-year deposits, 10% interest

e. Initial deposit if annuity is a perpetuity and initial deposit earns 9%:

Spreadsheet Exercise

The answer to Chapter 5’s Uma Corporation spreadsheet problem is located on the Instructor’s Resource Center at

www.pearsonhighered.com/irc under the Instructor’s Manual.

Group Exercise

Group exercises are available on www.myfinancelab.com.

This set of deliverables concerns each group’s fictitious firm. The first scenario involves the replacement of a copy

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 82

is perfectly allowable and shouldn’t affect future work. The same can be said of the final deliverable, involving a simple

calculation of the present value of a court-ordered settlement of a patent infringement case.

Integrative Case 2: Track Software, Inc.

Integrative Case 2, Track Software, Inc., places the student in the role of financial decision maker to introduce the basic

concepts of financial goal-setting, measurement of the firm’s performance, and analysis of the firm’s financial

condition. Because this seven-year–old software company has cash flow problems, the student must prepare and

analyze the statement of cash flows. Interest expense is increasing, and the firm’s financing strategy should be

evaluated in view of current yields on loans of different maturities. A ratio analysis of Track’s financial statements

is used to provide additional information about the firm’s financial condition. The student is then faced with a

cost/benefit tradeoff: Is the additional expense of a new software developer, which will decrease short-term profitability,

a good investment for the firm’s long-term potential? In considering these situations, the student becomes familiar

with the importance of financial decisions to the firm’s day-to-day operations and long-term profitability.

a. 1. Stanley is focusing on maximizing profit, as shown by the increase in net profits over the period

2. An agency problem exists when managers place personal goals ahead of corporate goals. Because Stanley

owns 40% of the outstanding equity, it is unlikely that an agency problem would arise at Track Software.

b. Earnings per share (EPS) calculation:

Year

Net Profits

After Taxes

EPS

(NPAT 50,000 shares)

2009 ($50,000) $ 0

Earnings per share has increased steadily, confirming that Stanley is concentrating his efforts on profit

maximization.

c. Calculation of Operating and Free Cash Flows

OCF EBIT(1 T) depreciation

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 83

d.

Ratio Analysis

Track Software, Inc.

Industry

Actual Average TS: Time-Series

Ratio 2014 2015 2015 CS: Cross-Sectional

Net working TS: Improving

capital $21,000 $58,000 $96,000 CS: Poor

Debt ratio 0.78 0.73 0.55 TS: Decreasing

CS: Poor

Times interest TS: Stable

Analysis of Track Software based on ratio data:

1. Liquidity: Track Software’s liquidity as reflected by the current ratio, net working capital, and acid-test

ratio has improved slightly or remained stable but overall is significantly below the industry average.

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 84

2. Activity: Inventory turnover has deteriorated considerably and is much worse than the industry average.

3. Debt: The firm’s debt ratio improved slightly from 2014 but is higher than the industry averages. The

4. Profitability: The firm’s gross, operating, and net profit margins have improved slightly in 2015 but

5. Stanley should make every effort to find the cash to hire the software developer. Because the major goal

e. Stanley is seeking to maximize the value of Track Software, not the earnings of any one period. As such, he

f. The investor would treat the $5,000 annual payment as an annuity. Dividing that payment by the 10%

g. The free cash flow is $20,200 annually. Treating that amount as an annuity and dividing by the 10% required

© 2015 Pearson Education, Inc.