P5-15. Personal finance: Time value and discount rates

LG 2; Intermediate

a. (1) N 10, I 6%, FV $1,000,000 (2) N 10, I 9%, FV $1,000,000

(3) N 10, I 12%, FV $1,000,000

b. (1) N 15, I 6%, FV $1,000,000 (2) N 15, I 9%, FV $1,000,000

(3) N 15, I 12%, FV $1,000,000

c. As the discount rate increases, the present value decreases. This decrease is due to the higher

P5-16. Personal finance: Time value comparisons of single amounts

LG 2; Intermediate

a. AN 3, I 11%, FV $28,500 BN 9, I 11%, FV $54,000

CN 20, I 11%, FV $160,000

b. Alternatives A and B are both worth greater than $20,000 in term of the present value.

c. The best alternative is B because the present value of B is greater than either A or C and is also greater

P5-17. Personal finance: Cash flow investment decision

LG 2; Intermediate

AN 5, I 10%, FV $30,000 BN 20, I 10%, FV $3,000

CN 10, I 10%, FV $10,000 DN 40, I 10%, FV $15,000

Purchase Do Not Purchase

A B

P5-18. Calculating deposit needed

LG 2; Challenge

Step 1: Determination of future value of initial investment

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 76

Step 2: Determination of future value of second investment

Step 3: Calculation of initial investment

P5-19. Future value of an annuity

LG 3; Intermediate

a. Future value of an ordinary annuity vs. annuity due

(1) Ordinary Annuity (2) Annuity Due

AN 10, I 8%, PMT $2,500 $36,216.41 1.08 $39,113.72

BN 6, I 12%, PMT $500 $4,057.59 1.12 $4,544.51

b. The annuity due results in a greater future value in each case. By depositing the payment at the

P5-20. Present value of an annuity

LG 3; Intermediate

a. Present value of an ordinary annuity vs. annuity due

(1) Ordinary Annuity (2) Annuity Due

AN 3, I 7%, PMT $12,000 $31,491.79 1.07 $33,696.22

b. The annuity due results in a greater present value in each case. By depositing the payment at the

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 77

P5-21. Personal finance: Time value—annuities

LG 3; Challenge

a. Annuity C (Ordinary) Annuity D (Due)

(1) N 10, I 10%, PMT $2,500 N 10, I 10%, PMT $2,200

Annuity Due Adjustment

$35,062.33 1.1 $38,568.57

(2) N 10, I 20%, PMT $2,500 N 10, I 20%, PMT $2,200

Annuity Due Adjustment

$57,109.10 1.2 $68,530.92

b. (1) At the end of year 10, at a rate of 10%, Annuity C has a greater value ($39,843.56 vs.

c. Annuity C (Ordinary) Annuity D (Due)

(1) N 10, I 10%, PMT $2,500 N 10, I 10%, PMT $2,200

(2) N 10, I 20%, PMT $2,500 N 10, I 20%, PMT $2,200

d. (1) At the beginning of the 10 years, at a rate of 10%, Annuity C has a greater value ($15,361.42 vs.

(2) At the beginning of the 10 years, at a rate of 20%, Annuity D has a greater value ($11,068.13 vs.

e. Annuity C, with an annual payment of $2,500 made at the end of the year, has a higher present value at

P5-22. Personal finance: Retirement planning

LG 3; Challenge

a. N 40, I 10%, PMT $2,000 b. N 30, I 10%, PMT $2,000

c. By delaying the deposits by 10 years, the total opportunity cost is $556,197. This difference is due to

d. Annuity Due:

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 78

P5-23. Personal finance: Value of a retirement annuity

LG 3; Intermediate

P5-24. Personal finance: Funding your retirement

LG 2, 3; Challenge

a. N 30, I 11%, PMT $20,000 b. N 20, I 9%, FV $173.875.85

c. Both values would be lower. In other words, a smaller sum would be needed in 20 years for

d. N 30, I 10%, PMT $20,000 b. N 20, I 10%, FV $188,538.29

P5-25. Personal finance: Value of an annuity vs. a single amount

LG 2, 3; Intermediate

a. N 25, I 5%, PMT $40,000

b. N 25, I 7%, PMT $40,000

c. View this problem as an investment of $500,000 to get a 25-year annuity of $40,000. The discount

P5-26. Perpetuities

LG 3; Basic

Case Equation Value

A $20,000 0.08 $250,000

B$100,000 0.10 $1,00,000

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 79

P5-27. Personal finance: Creating an endowment

LG 3; Intermediate

a. 6% interest rate

b. 9% percent interest rate

($600 3) 0.09 $20,000

P5-28. Value of a mixed stream

LG 4; Challenge

a.

Cash Flow

Stream Year

Number of Years

to Compound Cash flow

Interest

Rate Future Value

A1 2 $ 900 $ 1,128.96

B1 4 $30,000 $ 47,205.58

C1 3 $ 1,200 $1,685.91

b. If payments are made at the beginning of each period the present value of each of the end-of-period

P5-29. Personal finance: Value of a single amount vs. a mixed stream

LG 4; Intermediate

Lump-Sum Deposit

Mixed Stream of Payments

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 80

Beginning of

Year

Number of Years

to Compound Cash Flow Interest Rate Future Value

1 5 $ 2,000 7% $ 2,805.10

Gina should select the stream of payments over the front-end lump sum payment. Her future wealth will

be higher by $1,596.51.

P5-30. Value of mixed streams

LG 4; Basic

Project A

CF1 $2,000, CF2 $3,000, CF3 $4,000, CF4 $6,000, CF5 $8,000

P5-31. Present value—Mixed streams

LG 4; Intermediate

a. Stream A

b. Cash flow stream A, with a present value of $109,856, is higher than cash flow stream B’s present

P5-32. Value of a mixed stream

LG 1, 4; Intermediate

a.

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 81

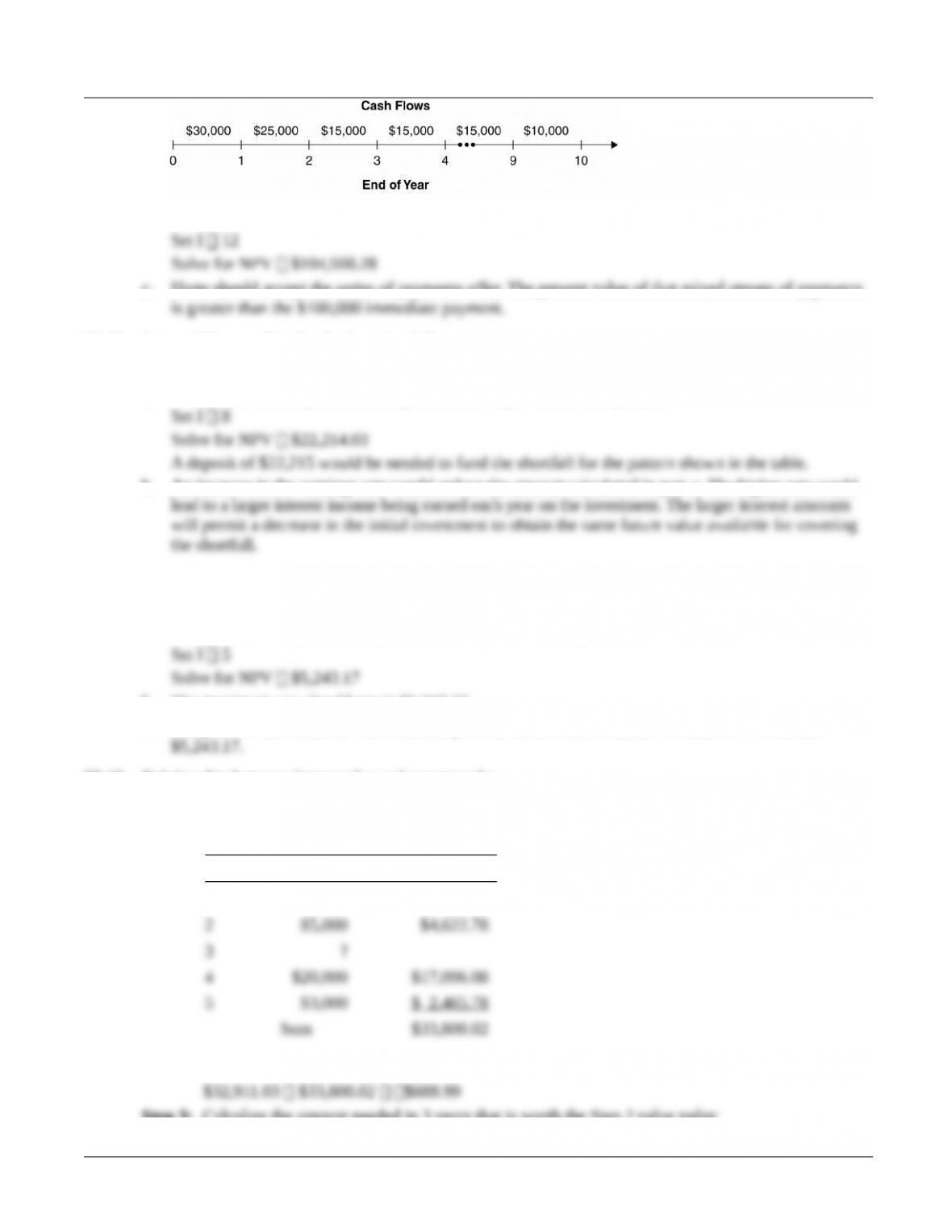

b. CF1 $30,000, CF2 $25,000, CF3 $15,000, F3 7, CF4 $10,000

c. Harte should accept the series of payments offer. The present value of that mixed stream of payments

P5-33. Personal finance: Funding budget shortfalls

LG 4; Intermediate

a. CF1 $5,000, CF2 $4,000, CF3 $6,000, CF4 $10,000, CF5 $3,000

b. An increase in the earnings rate would reduce the amount calculated in part a. The higher rate would

P5-34. Relationship between future value and present value-mixed stream

LG 4; Intermediate

a. CF1 $800, CF2 $900, CF3 $1,000, CF4 $1,500, CF5 $2,000

b. The maximum you should pay is $5,243.17.

c. A higher 7% discount rate will cause the present value of the cash flow stream to be lower than

P5-35. Relationship between future value and present value

LG 4; Intermediate

Step 1: Calculation of present value of known cash flows

Year CFtPV @ 4%

1 $10,000 $9,615.38

Step 2: Identify difference between total amount and sum in Step 1.

Step 3: Calculate the amount needed in 3 years that is worth the Step 2 value today

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 82

P5-36. Changing compounding frequency

LG 5; Intermediate

a. Compounding frequency

(1) Annual Semiannual

(2) Annual Semiannual

(3) AnnualSemiannual

b. Effective interest rate: ieff (1 r/m)m – 1

(1) Annual Semiannual

Quarterly

(2) Annual Semiannual

Quarterly

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 83

ieff 0.170 17%

(3) Annual Semiannual

P5-37. Compounding frequency, time value, and effective annual rates

LG 5; Intermediate

a. Compounding frequency:

b. Effective interest rate: ieff (1 r%/m)m – 1

c. The effective rates of interest rise relative to the stated nominal rate with increasing compounding

frequency.

P5-38. Continuous compounding: FVcont. PVex (e 2.7183)

LG 5; Intermediate

© 2015 Pearson Education, Inc.