Chapter 5

Time Value of Money

Instructor’s Resources

Overview

This chapter introduces an important financial concept: the time value of money. The present value and future of a

sum, as well as the present and future values of an annuity, are explained. Special applications of the concepts

include intra-year compounding, mixed cash flow streams, mixed cash flows with an embedded annuity,

perpetuities, deposits to accumulate a future sum, and loan amortization. Numerous business and personal financial

applications are used as examples. The chapter drives home the need to understand time value of money at the

professional level because funding for new assets and programs must be justified using these techniques. Decisions

in a student’s personal life should also be acceptable on the basis of applying time-value-of-money techniques to

anticipated cash flows.

Suggested Answer to Opener-in-Review Question

The city of Cincinnati gave up the right to collect parking fees over a 30-year period in exchange for a lump

sum of $92 million plus a 30-year annuity of $3 million. Suppose that if the city had not entered into that

arrangement, it would have collected parking fees the following year of $6 million (net of operating costs),

and those fees would have grown at a steady 3% for the next 30 years. At an interest rate of 4%, what is the

present value of the parking revenue that the city could have collected? Using the same 4% to value the

payments that the city was set to receive in their privatization deal, do you think that the city made the right

decision? Why or why not?

Total PV of giving up the right to collect parking fees:

I = 4; N = 30; PMT = 3

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 76

Answers to Review Questions

1. Future value (FV), the value of a present amount at a future date, is calculated by applying compound interest

2. A single amount cash flow refers to an individual standalone value occurring at one point in time. An annuity

3. Compounding of interest occurs when an amount is deposited into a savings account and the interest paid

FVn PV(1 r)n

4. A decrease in the interest rate lowers the future amount of a deposit for a given holding period because the

5. Present value is the current dollar value of a future amount. It indicates how much money today would be

PV FVn (1 r)n

6. An increasing required rate of return would reduce the present value of a future amount because future dollars

7. Present value calculations are the exact inverse of compound interest calculations. Using compound interest,

8. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

9. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

10. An ordinary annuity is one for which payments occur at the end of each period. An annuity due is one for

11. The most efficient ways to calculate present value of an ordinary annuity are using an algebraic equation, a

12. You can calculate the future value of an annuity due by multiplying the value calculated for an ordinary

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 77

13. You can calculate the present value of an annuity due by multiplying the value calculated for an ordinary

14. A perpetuity is an infinite-lived annuity. By multiplying the PV by the required rate of return, i, the perpetual

15. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

16. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

17. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

18. The future value of a mixed stream of cash flows is calculated by multiplying each year’s cash flow by

19. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

20. As interest is compounded more frequently than once a year, both (a) the future value for a given holding

21. Continuous compounding assumes interest will be compounded an infinite number of times per year, at

22. The nominal annual rate is the contractual rate that is quoted to the borrower by the lender. The effective

23. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

24. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

25. Answers will vary for question because values are algorithmically generated in MyFinanceLab.

26. The size of the equal annual end-of-year deposits needed to accumulate a given amount over a certain time

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 78

27. Amortizing a loan into equal annual payments involves finding the future payments whose present value at

28. The best way to determine an unknown number of periods is through the use of a calculator or spreadsheet. In

Suggested Answer to Focus on Practice Box:

New Century Brings Trouble for Subprime Mortgages

As a reaction to problems in the subprime area, lenders tightened lending standards. What effect do you

think this change had on the housing market?

The tightening of lending standards following the subprime fiasco further depressed home prices, which in 2007

Suggested Answer to Focus on Ethics Box:

How Fair Is “Check into Cash”?

The 391% mentioned is an annual nominal rate [15% (365/14)]. Should the 2-week rate (15%) be

compounded to calculate the effective annual interest rate?

No, the rollover fee is a simple $15 per 2-week period. In other words, the 15% 2-week rate is only applied to the

Answers to Warm-Up Exercises

E5-1. Future value of a lump-sum investment

E5-2. Finding the future value

Answer: Because the interest is compounded monthly, the number of periods is 4 12 48 and the monthly

interest rate is 1/12th of the annual rate.

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 79

Column A Column B

Cell 1 Future value of a single amount

Cell B5 $2,420.99

E5-3. Comparing a lump sum with an annuity

Answer: This problem can be solved in either of two ways. Both alternatives can be compared as lump sums in

Method 1: Perform a lump sum comparison. Compare $1.3 million now with the present value of the

Method 2: Compare two annuities. Because the $100,000 per year is already an annuity, all that

E5-4. Comparing the present value of two alternatives

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 80

Answer: To solve this problem you must first find the present value of the expected savings over the

5-year life of the software.

Year Savings Estimate

Present Value

of Savings

1 $35,000 $32,110

E5-5. Compounding more frequently than annually

Answer: Partners’ Savings Bank:

1

2

1

2

1

1

$12,000 (1 0.03/2)

$12,000 (1 0.03/2) $12,000 1.030225 $12,362.70

m n

r

FV PV m

FV

FV

´

æ ö

= ´ +

ç ÷

è ø

= ´ +

= ´ + = ´ =

Selwyn’s:

rxn 0.0275 1

1

FV PV (e ) $12,000 (2.7183 )

$12,000 1.027882 $12,334.58

´

= ´ = ´

= ´ =

Joseph should choose the 3% rate with semiannual compounding.

E5-6. Determining deposits needed to accumulate a future sum

Answer: The financial calculator input is as follows:

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 81

Solutions to Problems

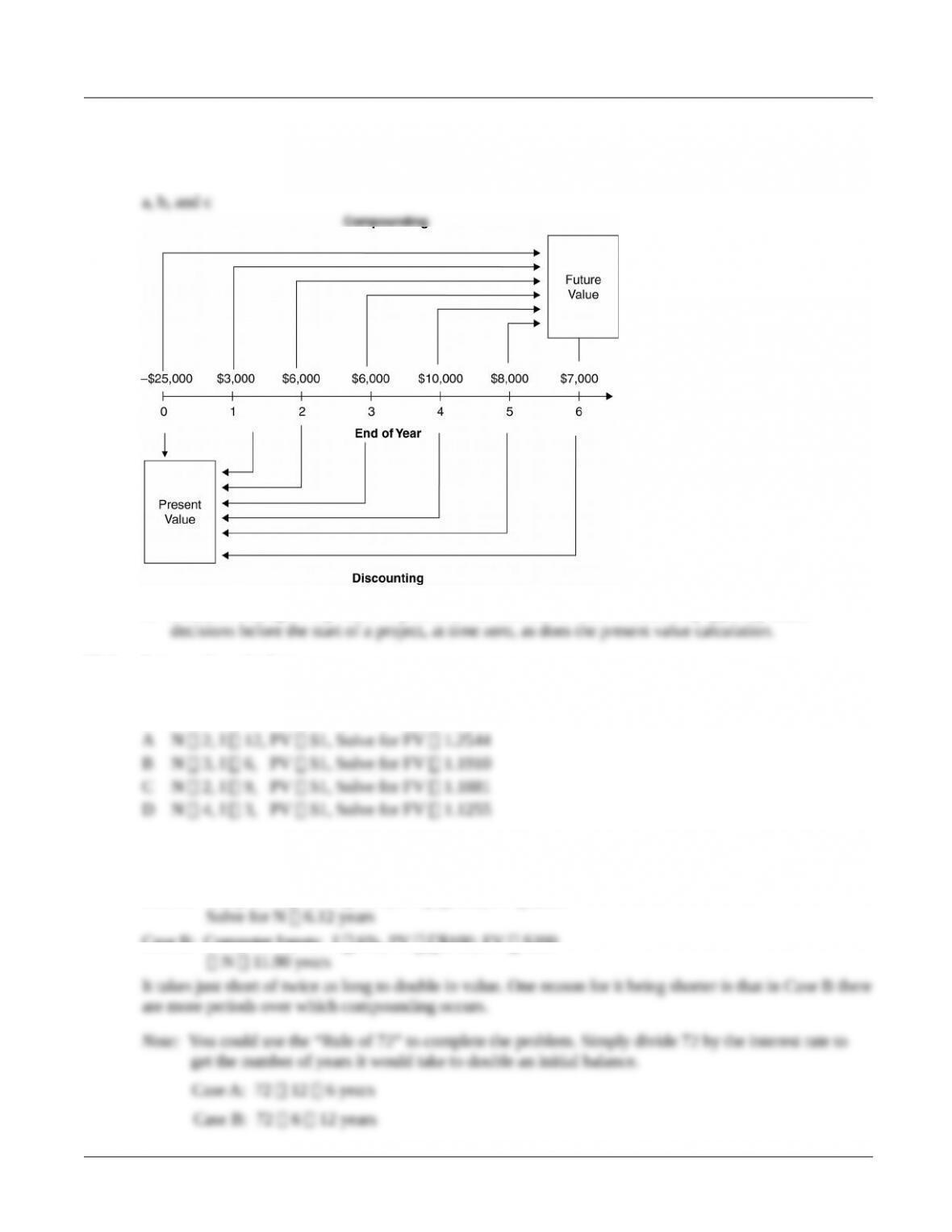

P5-1. Using a time line

LG 1; Basic

d. Financial managers rely more on present value than future value because they typically make

P5-2. Future value calculation

LG 2; Basic

Case

P5-3. Time to double

LG 1; Basic

Case A: Computer Inputs: I 12%, PV $100; FV $200

Case B: Computer Inputs: I 6%, PV $100; FV $200

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 82

P5-4. Future values

LG 2; Intermediate

Case Case

AN 20, I 5%, PV $200.BN 7, I/Y 8%; PV $4500.

P5-5. Personal finance: Time value

LG 2; Intermediate

a. (1) N 3, I 7%, PV $1,500 b. (1) Interest earned FV3 PV

$1,500.00

$337.56

(2) N 6, I 7%, PV $1,500 (2) Interest earned FV6 – FV3

–$1,837.56

$413.54

(3) N 9, I 7%, PV $1,500 (3) Interest earned FV9 FV6

–$2,251.10

$506.59

c. The fact that the longer the investment period is, the larger the total amount of interest collected will

P5-6. Personal finance: Time value

LG 2; Challenge

a. (1) N 5, I 2%, PV $14,000 (2) N 5, I 4%, PV $14,000

b. The car will cost $1,576.01 more with a 4% inflation rate than an inflation rate of 2%. This increase is

c. Future value at end of first 2 years:

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 83

P5-7. Personal finance: Time value

LG 2; Challenge

Deposit Now: Deposit in 10 Years:

P5-8. Personal finance: Time value

LG 2; Challenge

a. N 5, PV $10,200, FV 15,000 b. N 5, PV $8,150, FV $15,000

c. N 5, PV $7150, FV $15,000

P5-9. Personal finance: Single-payment loan repayment

LG 2; Intermediate

a. N 1, I 14%, PV $200 b. N 4, I 14%, PV $200

c. N 8, I 14%, PV $200

© 2015 Pearson Education, Inc.

Chapter 5 Time Value of Money 84

P5-10. Present value calculation:

1

PVIF (1 )

n

i

=+

LG 2; Basic

Case

AN 4, I 2, FV $1.00, Solve for PV $0.9238

P5-11. Present values

LG 2; Basic

Case PV

AN 4, I 12%, FV $7,000 $4,448.63

P5-12. Present value concept

LG 2; Intermediate

a. N 6, I 12%, FV $6,000 b. N 6, I 12%, FV $6,000

c. N 6, I 12%, FV $6,000

d. The answer to all three parts is the same. In each case, the same question is being asked but in a

P5-13. Personal finance: Time Value

LG 2; Basic

a. N 3, I 7%, FV $500

b. Jim should be willing to pay no more than $408.15 for this future sum given that his opportunity cost

P5-14. Time value: Present value of a lump sum

LG 2; Intermediate

© 2015 Pearson Education, Inc.