Chapter 4

Cash Flow and Financial Planning

Instructor’s Resources

Overview

This chapter introduces the student to the financial planning process, with the emphasis on short-term (operating)

financial planning and its two key components: cash planning and profit planning. Cash planning requires

preparation of the cash budget, while profit planning involves preparation of a pro forma income statement and

balance sheet. The text illustrates through example how these budgets and statements are developed. The

weaknesses of the simplified approaches (judgmental and percent-of-sales methods) of pro forma statement

preparation are outlined. The distinction between operating cash flow and free cash flow is presented and

discussed. Current tax law regarding the depreciation of assets and the effect on cash flow are also described. The

firm’s cash flow is analyzed through classification of sources and uses of cash. The student is guided in a

step-by-step preparation of the statement of cash flows and the interpretation of this statement. This chapter ties in

every person’s need to set goals, estimate income, and budget expenditures to the firm’s need to effectively engage

in these activities.

Suggested Answer to Opener-in-Review Question

The chapter opener described a company that reported increases in revenues and profits, but even so, the

company’s free cash flow was negative. Explain why a profitable, expanding business may have negative

free cash flow.

A firm’s free cash flow (FCF) represents the cash available to investors—the providers of debt (creditors) and

equity (owners)—after the firm has met all operating needs and paid for net investments in fixed assets and current

assets.

When a firm is expanding, it may have to make additional investments in inventory, receivables, and fixed assets

such as machinery. Cash outlays for those investments don’t necessarily show up immediately in the profit

calculation, but they do reduce free cash flow. A firm may be generating high revenue and profit but may not have

enough to pay the creditors and owners. This can happen when a company needs to make significant investment,

higher than the operating cash flow, into fixed capital or working capital. When a business is in an expansion

phase, the firm has to make higher amount of investment in fixed assets and current assets to meet the growth

requirements.

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 52

Answers to Review Questions

1. The first four classes of property specified by the MACRS system categorized by the length of the

depreciation (recovery) period are called 3-, 5-, 7-, and 10-years property:

Recovery Period Definition

3 years Research and experiment equipment and certain special tools

2. The cash flow from operating activities relates to the firm’s production cyclefrom the purchase of raw materials

to the finished product. Any expenses incurred directly related to this process are considered operating flows.

3. A decrease in a cash balance is a source of cash flow because cash flow must have been released for some

4. Depreciation (and amortization and depletion) is a cash inflow to the firm because it is treated as a noncash

5. Cash flows shown in the statement of cash flows are divided into three categories and presented in the order

6. Operating cash flows take net profits after tax and add in depreciation and other noncash charges. The net

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 53

7. Operating cash flow is the cash flow generated from a firm’s normal operations of producing and selling its

8. The financial planning process is the development of long-term strategic financial plans that guide the

9. Three key statements resulting from short-term financial planning are (1) the cash budget, (2) the pro forma

10. The cash budget is a statement of the firm’s planned cash inflows and outflows. It is used to estimate its

11.The basic format of the cash budget is presented in the table below.

Cash Budget Format

Jan. Feb. Nov. Dec.

Total cash receipts $XX $XX $XX $XX

The components of the cash budget are defined as follows:

12. The ending cash balance without financing, along with any required minimum cash balance, can be used to

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 54

13. Uncertainty in the cash budget is due to the uncertainty of ending cash values, which are based on forecasted

14. Pro forma statements are used to provide a basis for analyzing future profitability and overall financial

15. In the percent-of-sales method for preparing a pro forma income statement, the financial manager begins with

16. A pro forma income statement constructed using the percentage-of-sales method generally tends to understate

17. The judgmental approach is used to develop the pro forma balance sheet by estimating some balance sheet

18. The balancing, or “plug,” figure used in the pro forma balance sheet prepared with the judgmental approach is

19. Simplified approaches to preparing pro forma statements have two basic weaknesses: (1) the assumption that the

20. The financial manager may perform ratio analysis and may possibly prepare source and use statements from

Suggested Answer to Focus on Practice Box: Free Cash Flow

at Cisco Systems

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 55

What are some of the possible ways that corporate accountants might be able to change their earnings to

portray a more favorable earnings statement?

There are many ways in which a company can increase earnings reported in a given year. They can lease instead of

Suggested Answer to Focus on Ethics Box:

How Much Is a CEO Worth?

Do you think shareholder activists would have been as upset with Nardelli’s severance package had The

Home Depot performed much better under his leadership?

It is likely that there would have been less disappointment with Mr. Nardelli’s severance package if the Home

Answers to Warm-Up Exercises

E4-1. Depreciation schedule

Answer:

Recovery Year Depreciation

1 $13,000

E4-2. Cash flows (inflows and outflows)

Answer:

a. Marketable securities increased Cash Outflow

E4-3. Operating cash flow

Answer: OCF [EBIT (1 T)] depreciation

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 56

EBIT Sales –Cost of goods sold − Operating expenses

E4-4. Free cash flow

Answer: FCF OCF Net fixed asset investment (NFAI) Net current asset investment (NCAI)

NFAI Change in net fixed assets depreciation

E4-5. Estimating net profits before taxes

Answer:

Rimier Corp

Pro Forma

Income Statement 2016

Sales revenue $650,000

Less: Cost of goods sold

Solutions to Problems

P4-1. Depreciation

LG 1; Basic

Depreciation Schedule

Year Cost (1)

Percentages

from Table 4.2 (2)

Depreciation

[(1) (2)] (3)

Asset A

1 $17,000 33% $ 5,610

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 57

P4-2. Depreciation

LG 1; Basic

Depreciation Schedule

Cork stopper machine

Year

Cost

(1)

Percentages

from Table 4.2

(2)

Depreciation

[(1) (2)]

(3)

1 $10,000 33% $ 3,300

P4-3. MACRS depreciation expense, taxes, and cash flow

LG 1, 2; Challenge

a. Depreciation expense $80,000 0.20 $16,000 (MACRS depreciation percentages found in Table

4.2 in the text.)

b. New taxable income $430,000 $16,000 $414,000

P4-4. Depreciation and accounting cash flow

LG 1, 2; Intermediate

a. Operating cash flow

Sales revenue $400,000

Less: Total costs before depreciation,

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 58

b. Depreciation and other noncash charges serve as a tax shield against income, increasing annual cash

flow.

P4-5. Classifying inflows and outflows of cash

LG 2; Basic

Item

Change

($) I/O Item

Change

($) I/O

Cash 100 O Accounts receivable 700 I

Note 1: Think of cash in terms of money in a checking account.

Note 2: As a noncash charge, depreciation is not really an I/O at all, but it will be reported as a positive

P4-6. Finding operating and free cash flows

LG 2; Intermediate

a. NOPAT EBIT (1 t)

b. OCF NOPAT depreciation

c. FCF OCF net fixed asset investment* net current asset investment**

* Net fixed asset investment change in net fixed assets depreciation

** Net current asset investment change in current assets change in

d. Keith Corporation has positive cash flows from operating activities. Depreciation is approximately the

P4-7. Cash receipts

LG 4; Basic

April May June July August

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 59

Sales $65,000 $60,000 $70,000 $100,000 $100,000

P4-8. Cash disbursement schedule

LG 4; Basic

February March April May June July

Sales $500,000 $500,000 $560,000 $610,000 $650,000 $650,000

Purchases (0.60) $300,000 $336,000 $366,000 $390,000 $390,000

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 60

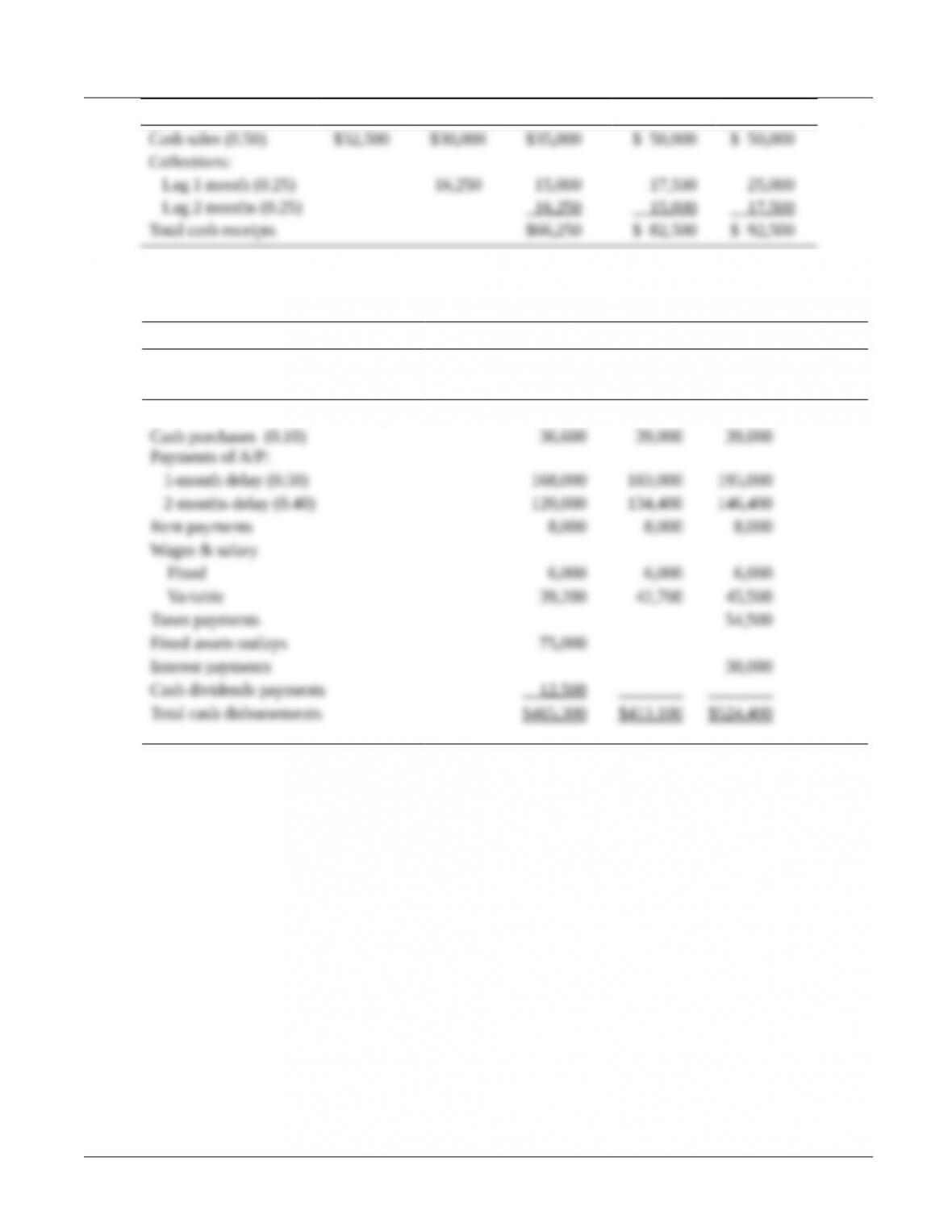

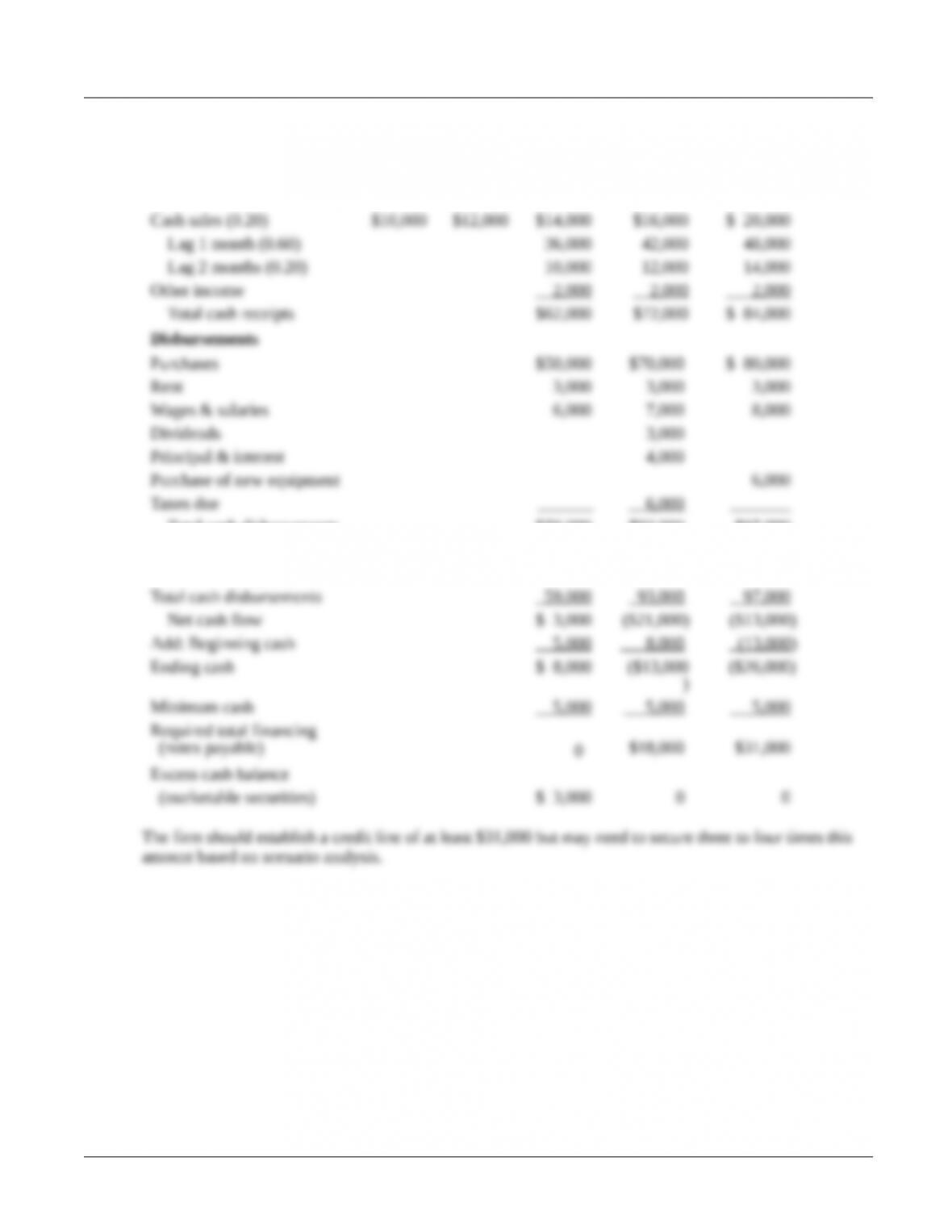

P4-9. Cash budget—basic

LG 4; Intermediate

March April May June July

Sales $50,000 $60,000 $70,000 $80,000 $100,000

Total cash disbursements $59,000 $93,000 $97,000

Total cash receipts $62,000 $72,000 $84,000

© 2015 Pearson Education, Inc.

Chapter 4 Cash Flow and Financial Planning 61

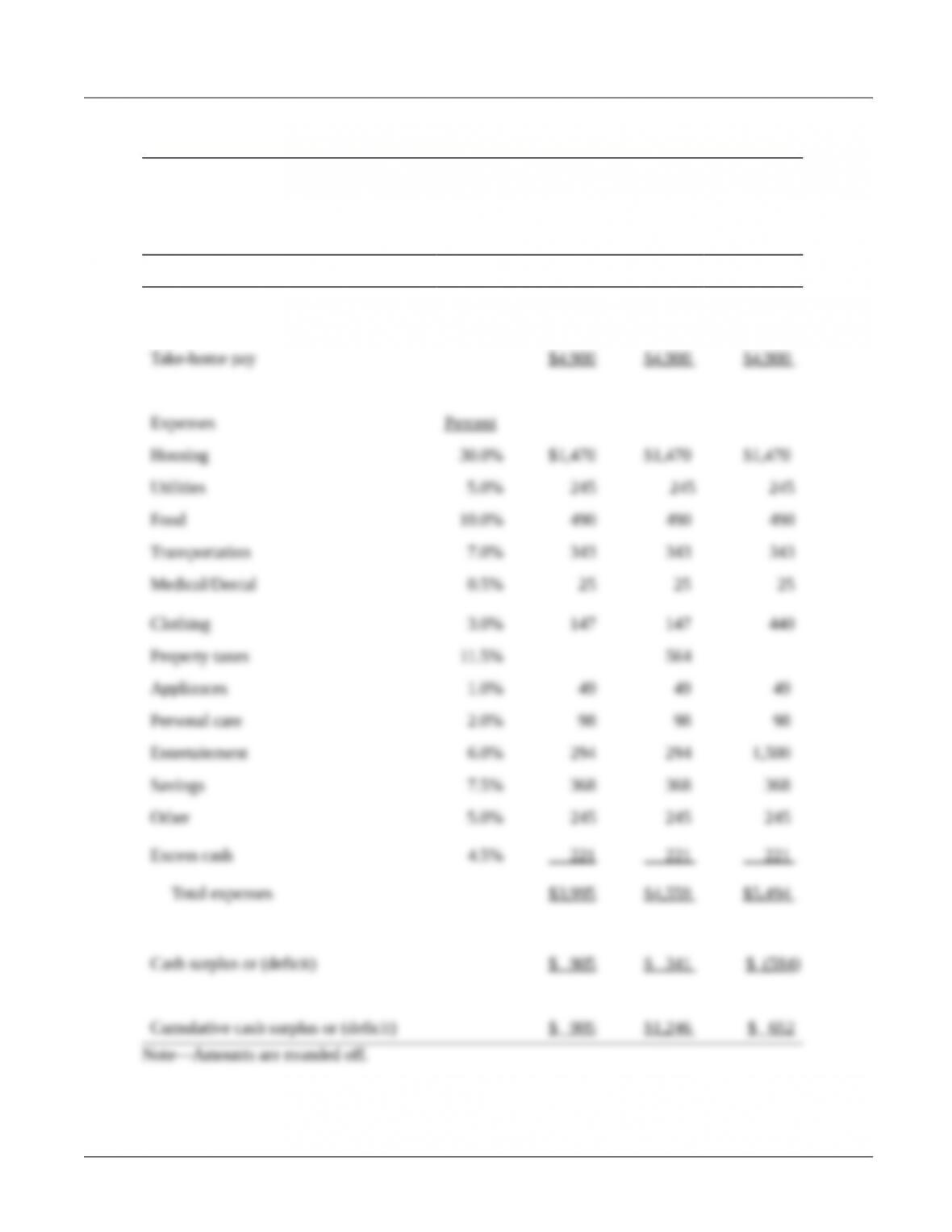

P4-10. Personal finance: Preparation of cash budget

LG 4; Basic

Sam and Suzy Sizeman

Personal Budget

for the Period October—December 2016

October November December

Income

© 2015 Pearson Education, Inc.