P3-20. Common-size statement analysis

LG 5; Intermediate

Creek Enterprises

Common-Size Income Statement

for the Years Ended December 31, 2014 and 2015

2015 2014

Sales revenue 100.0% 100.0%

P3-21. The relationship between financial leverage and profitability

LG 4, 5; Challenge

a. (1)

total liabilities

Debt ratio total assets

=

Pelican

Timberland

$1,000,000

Debt ratio 0.10 10%

$10,000,000

$5,000,000

Debt ratio 0.50 50%

$10,000,000

= = =

= = =

(2)

earning before interest and taxes

Times interest earned interest

=

Pelican

Timberland

$6,250,000

Times interest earned 62.5

$100,000

$6,250,000

Times interest earned 12.5

$500,000

= =

= =

© 2015 Pearson Education, Inc.

b. (1)

operating profit

Operating profit margin sales

=

Pelican

Timberland

$6,250,000

Operating profit margin 0.25 25%

$25,000,000

$6,250,000

Operating profit margin 0.25 25%

$25,000,000

= = =

= = =

(2)

Earnings available for common stockholders

Net profit margin sales

=

Pelican

Timberland

$3,690,000

Net profit margin 0.1476 14.76%

$25,000,000

$3,450,000

Net profit margin 0.138 13.80%

$25,000,000

= = =

= = =

(3)

Earnings available for common stockholders

Return on total assets total assets

=

Pelican

Timberland

$3,690,000

Return on total assets 0.369 36.9%

$10,000,000

$3,450,000

Return on total assets 0.345 34.5%

$10,000,000

= = =

= = =

(4)

Earnings available for common stockholders

Return on common equity Common stock equity

=

Pelican

Timberland

$3,690,000

Return on common equity 0.41 41.0%

$9,000,000

$3,450,000

Return on common equity 0.69 69.0%

$5,000,000

= = =

= = =

Pelican is more profitable than Timberland, as shown by the higher operating profit margin, net profit

margin, and return on assets. However, the return on common equity for Timberland is higher than

that of Pelican.

c. Even though Pelican is more profitable, Timberland has a higher ROE than Pelican due to the

P3-22. Ratio proficiency

LG 6; Basic

a.

Gross profit sales gross profit margin

Gross profit $40,000,000 0.8 $32,000,000

= ´

= ´ =

b.

Cost of goods sold sales gross profit

Cost of goods sold $40,000,000 $32,000,000 $8,000,000

= –

= – =

c.

Operating profit sales operating profit margin

Operating profit $40,000,000 0.35 $14,000,000

= ´

= ´ =

d.

Operating expenses gross profit operating profit

Operating expenses $32,000,000 $14,000,000 $18,000,000

= –

= – =

e.

Earnings available for common shareholders

sales net profit margin $40,000,000 0.08 $3,200,000= ´ = ´ =

f.

sales $40,000,000

Total assets $20,000,000

total asset turnover 2

= = =

g.

earnings available for common shareholders

Total common equity

ROE

$3,200,000

Total common equity $16,000,000

0.20

=

= =

h.

sales

Accounts receivable average collection period

365

$40,000,000

Accounts receivable 62.2 days 62.2 $109,589.041 $6,816,438.36

365

= ´

= ´ = ´ =

Liquidity: The current and quick ratios show a weaker position relative to the industry average.

Activity: All activity ratios indicate a faster turnover of assets compared to the industry. Further analysis

Debt: The firm uses more debt than the average firm, resulting in higher interest obligations that

Profitability: The firm has a higher gross profit margin than the industry, indicating either a higher

b. Fox Manufacturing Company needs improvement in its liquidity ratios and possibly a reduction in its

P3-24. Financial statement analysis

LG 6; Intermediate

a.

Zach Industries

Ratio Analysis

Industry

Average

Actual

2014

Actual

2015

Current ratio 1.80 1.84 1.04

b. Liquidity: Zach Industries’ liquidity position has deteriorated from 2014 to 2015 and is inferior to the

P3-25. Integrative—complete ratio analysis

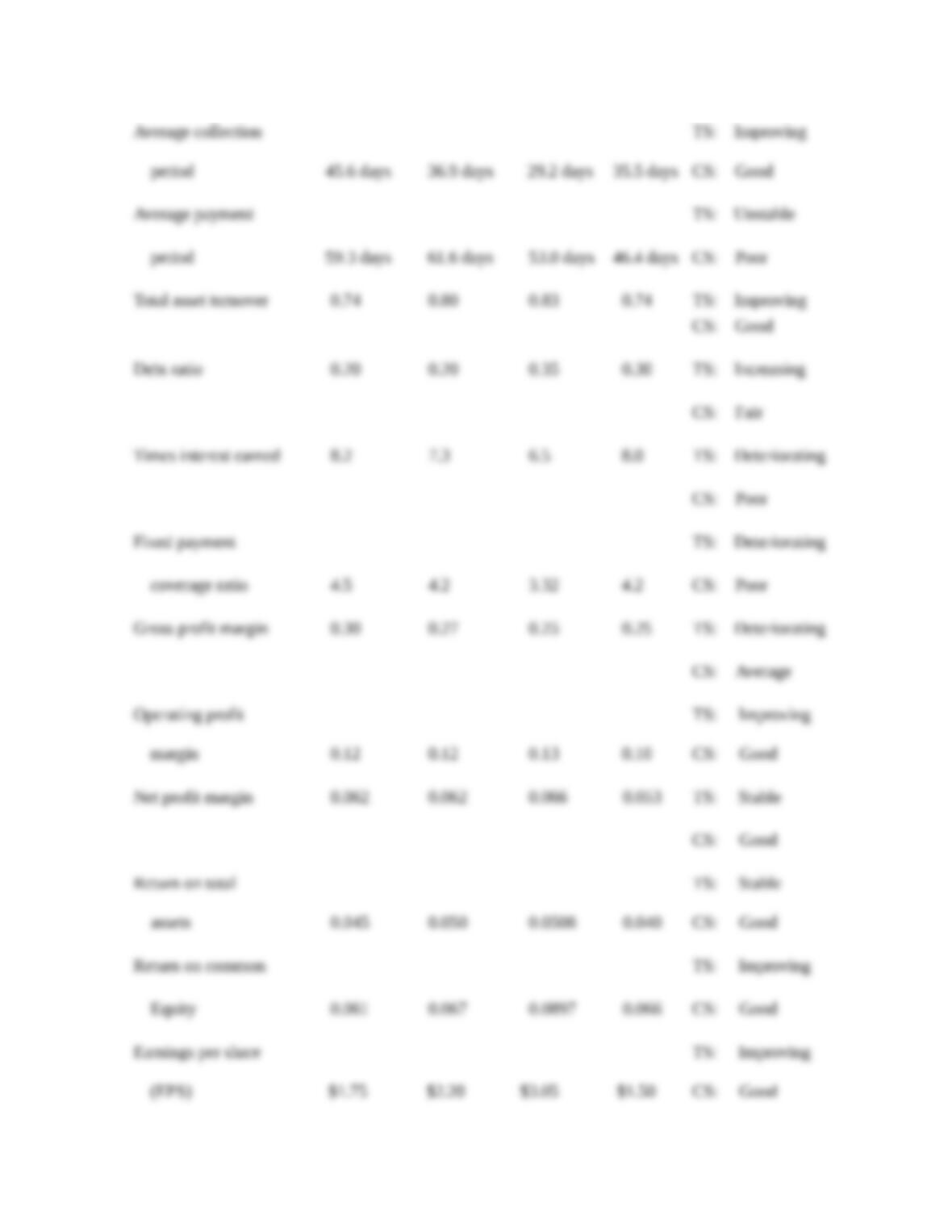

LG 6; Challenge

Sterling Company

Ratio Analysis

Actual Actual Actual

Industry

Average TS: Time-Series

Ratio 2010 2014 2015 2015 CS: Cross-Sectional

CS: Fair

Equity 0.061 0.067 0.0897 0.066 CS: Good

P3-26. DuPont system of analysis

LG 6; Intermediate

a.

Margin(%) Turnover = ROA(%) FL Multiple = ROE(%)

2015

2014

2013

b. Profitability: Industry net profit margins are decreasing; Johnson’s net profit margins have fallen

less.

Efficiency: Both industry’s and Johnson’s asset turnover have increased.

Leverage: Only Johnson shows an increase in leverage from 2014 to 2015, while the industry has had

c. Areas that require further analysis are profitability and debt. Because the total asset turnover is

P3-27. Complete ratio analysis, recognizing significant differences

LG 6; Intermediate

a.

Home Health, Inc.

Ratio 2014 2015 Difference

Proportional

Difference

Current ratio 3.25 3.00 – 0.25 – 7.69%

Market/book ratio 1.40 1.25 – 0.15 – 10.71%

b.

Ratio

Proportional

Difference Company’s Favor

Quick ratio – 12.00% No

c. The most obvious relationship is associated with the increase in the ROE value. The increase in this

P3-28. Ethics problem

LG 1; Intermediate

Case

Case studies are available on www.myfinancelab.com.

Assessing Martin Manufacturing’s Current Financial Position

Martin Manufacturing Company is an integrative case study addressing financial analysis techniques. The

company is a capital-intensive firm that has poor management of accounts receivable and inventory. The industry

average inventory turnover can fluctuate from 10 to 100 depending on the market.

a. Ratio calculations

Financial Ratio 2012

Current ratio $1,531,181 $616,000 = 2.5%

Times interest earned $153,000 $93,000 = 1.6%

Return on total assets $36,000 $3,125,000 = 1.2%

Historical Ratios

Martin Manufacturing Company

Ratio

Actual

2010

Actual

2011

Actual

2012

Industry

Average

Current ratio 1.7 1.8 2.5 1.5

Average collection period (days) 50.7 55.8 58.0 46.0

Total asset turnover (times) 1.5 1.5 1.6 2.0

b. Liquidity: The firm has sufficient current assets to cover current liabilities. The trend is upward and is much

higher than the industry average. This is an unfavorable position because it indicates too much inventory.

Activity: The inventory turnover is stable but much lower than the industry average. This indicates the firm is

holding too much inventory. The average collection period is increasing and much higher than the industry

average. These are both indicators of a problem in collecting payment.

The total asset turnover ratio is stable but significantly lower than the industry average. This indicates that the

sales volume is not sufficient for the amount of committed assets.

Debt: The debt ratio has increased and is substantially higher than the industry average. This places the

company at high risk. Typically industries with heavy capital investment and higher operating risk try to

minimize financial risk. Martin Manufacturing has positioned itself with both heavy operating and financial

risk. The times-interest-earned ratio also indicates a potential debt service problem. The ratio is decreasing

and is far below the industry average.

Profitability: The gross profit margin is stable and quite favorable when compared to the industry average.

The net profit margin, however, is deteriorating and far below the industry average. When the gross profit

margin is within expectations but the net profit margin is too low, high interest payments may be to blame.

The high financial leverage has caused the low profitability.

Market: The market price of the firm’s common stock shows weakness relative to both earnings and book

value. This result indicates a belief by the market that Martin’s ability to earn future profits faces increasing

uncertainty as perceived by the market.

c. Martin Manufacturing clearly has a problem with its inventory level, and sales are not at an appropriate level for

its capital investment. As a consequence, the firm has acquired a substantial amount of debt which, due to the

high interest payments associated with the large debt burden, is depressing profitability. These problems are

being picked up by investors as shown in their weak market ratios.

Spreadsheet Exercise

The answer to Chapter 3’s Dayton, Inc., financial statements spreadsheet problem is located on the Instructor’s

Resource Center at www.pearsonhighered.com/irc under the Instructor’s Manual.

Group Exercise

Group exercises are available on www.myfinancelab.com.

This chapter’s group focuses solely on the group’s shadow firm. Groups are asked to investigate and describe their

firm’s latest 10-K obtained from the Securities and Exchange website (www.sec.gov). From the filing, the groups

are asked to calculate the basic ratios as done in the text and discuss each ratio’s importance. This leads to a

comparison of these ratios over the most recent years. The number of years is up to the instructor’s discretion. A shorter

number of years is probably most desirable because this often can be accomplished from the single 10-K filing.

The conclusion of this assignment is calculation of the DuPont analysis for their shadow firm. This exercise

shouldn’t require much assistance, particularly if students have made a good choice for their firm in Chapter 1.

Modifications could include dropping the intertemporal analysis and focusing solely on the most recent year.

Alternatively, groups could be asked to compare the ratios from their shadow firm with the ratios from another

firm within the same industry.