P18-6. Personal finance: Divestitures

LG 3; Easy

P18-7. Ratio of exchange and EPS

LG 3; Intermediate

a. Number of additional shares needed 1.8 4,000 7,200

b. Number of additional shares needed 2.0 4,000 8,000

c. Number of additional shares needed 2.2 4,000 8,800

d. P/E calculations:

© 2015 Pearson Education, Inc.

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 385

P18-8. EPS and merger terms

LG 3; Challenge

P18-9. Ratio of exchange

LG 3; Intermediate

Case Ratio of Exchange Market Price Ratio of Exchange

A $ 30 ¸ $50 0.60 ($50 0.60) ¸ $25 1.20

P18-10. Expected EPS—merger decision

LG 3; Challenge

a. Graham & Sons—Premerger

Year Earnings EPS

2012 $200,000 $2.000

b. (1) New shares issued 100,000 0.6 60,000

Year Earnings/Shares EPS

2012 [($800,000 $200,000) ¸ 260,000] 0.6 $

2.308

© 2015 Pearson Education, Inc.

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 386

(2) New shares issued 100,000 0.8 80,000

Year Earnings/Shares EPS

2012 [($800,000 $200,000) ¸ 280,000] 0.8 $2.857

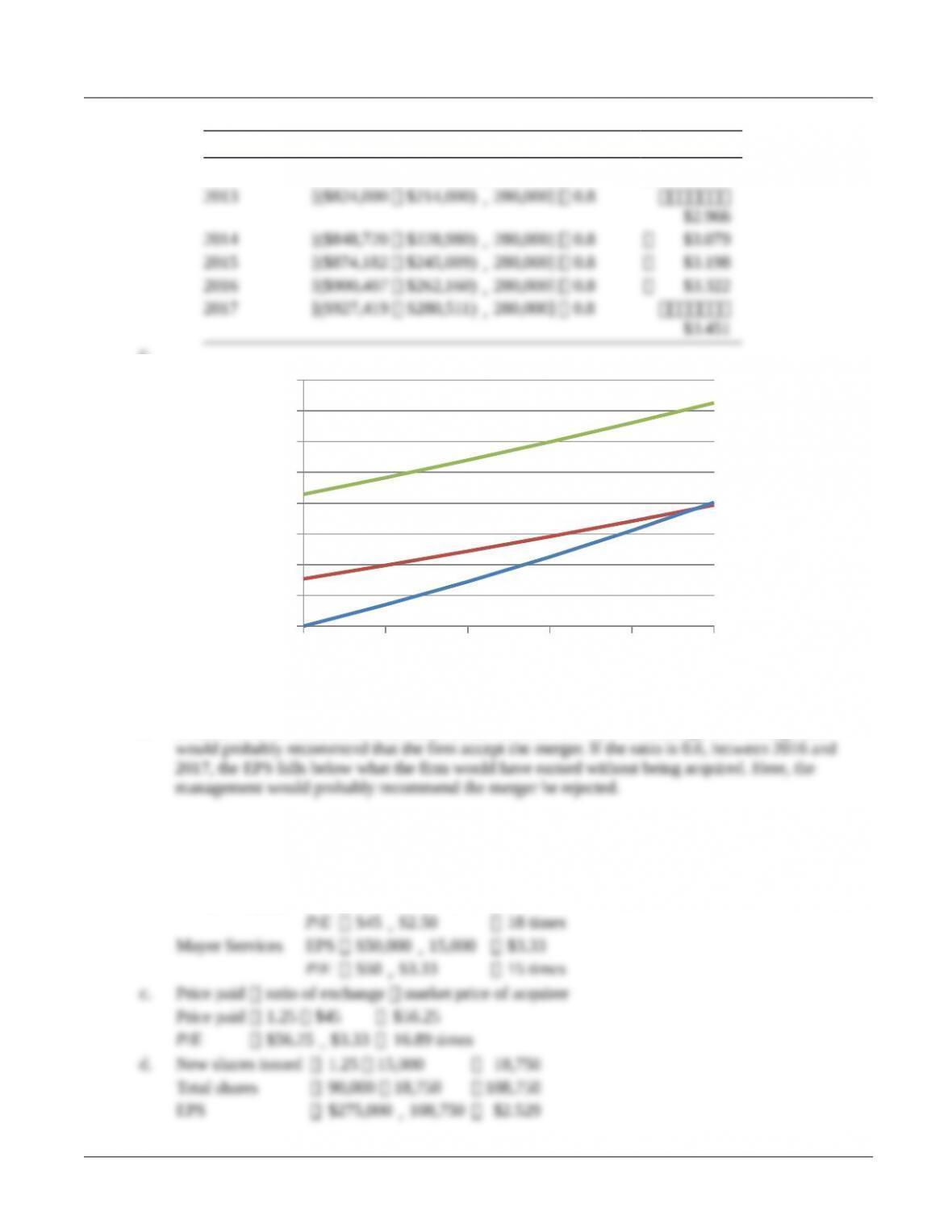

c.

2012 2013 2014 2015 2016 2017

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

3.60

YEAR

EPS($)

d. Graham & Sons’ shareholders are much better off at the 0.8 ratio of exchange. The management

P18-11. EPS and postmerger price

LG 3; Challenge

a. Market price ratio of exchange: ($45 1.25) ¸ $50 1.125

b. Henry Company EPS $225,000 ¸ 90,000 $2.50

© 2015 Pearson Education, Inc.

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 387

P18-12. Holding company

LG 4; Challenge

a. Total assets controlled: $35,000 ¸ ($500,000 $900,000) 2.5%

P18-13. Voluntary settlements

LG 5; Basic

P18-14. Voluntary settlements

LG 5; Basic

a. Extension

P18-15. Voluntary settlements—payments

LG 5; Intermediate

a. $75,000 now; composition

P18-16. Personal finance: Bankruptcy legislation—wage-earner plan

LG 5; Easy

a. Outstanding debt

$28,000

© 2015 Pearson Education, Inc.

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 388

P18-17. Ethics problem

LG 5, 6; Intermediate

These employees and suppliers may believe that the company’s problems are only temporary and that

Case

Case studies are available on www.myfinancelab.com.

Deciding Whether to Acquire or Liquidate Procras Corporation

In this case, the student is asked to analyze two alternatives, acquiring a bankrupt firm or liquidating it, to see

which makes more sense for Rome Industries.

b. Postmerger EPS:

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 389

Claims of general creditors:

Creditor Claims Amount Settlement at 50%*

Chapter 18 Mergers, LBOs, Divestitures, and Business Failure 390

Corporate restructurings are the focus of this chapter’s look at special topics in financial management. The

financial structure of the firm is not static and instead undergoes a constant evolution for a variety of reasons. This

© 2015 Pearson Education, Inc.