Chapter 14

Payout Policy

Instructor’s Resources

Overview

Chapter 14 concentrates on the payout decision from the viewpoint of both the firm and the investors. The types of

payout policies, forms of dividends, and their possible effects on the value of the firm are included in this chapter.

The arguments for the relevancy and irrelevancy of dividends are presented. The legal, contractual, and internal

constraints affecting dividend policy are discussed. An introduction to dividend reinvestment plans is included.

The chapter notes that dividend cash outflows reduce corporate assets while enhancing personal wealth and,

therefore, have implications for both the student’s professional life and personal life.

Suggested Answer to Opener-in-Review Question

The chapter opener described Whirlpool’s decision to dramatically increase its dividend in early 2013 to

$0.625 per share. When it made that announcement, Whirlpool indicated that the date of record for the

dividend would be Friday, May 17, and the payment date would be Saturday, June 15. When would you

expect the stock to go ex dividend? The market price of Whirlpool stock just before the ex dividend date

was $129. Immediately after the stock went ex dividend the market price was $129.67. Is that price change

surprising? Calculate the return that an investor might have earned if she had purchased the stock before

the ex dividend date, sold the stock immediately afterward, and received the dividend a few weeks later.

The ex dividend date is usually two days before the date of record, so in this case it would be May 15. Normally,

we would expect that a stock’s price would drop by roughly the amount of the dividend when it goes ex dividend

because the stock price should reflect the fact that the firm no longer has a claim on the cash used to pay the

dividend. Whirlpool’s stock went up after it went ex dividend, so that is something of a surprise. The return that an

investor would have earned is ($129.67 + $0.625 – $129) / $129 = 1%. That is not a large return, but keep in mind

that to earn this required return the investor needs to have capital invested for just one day.

Answers to Review Questions

1. The two primary ways in which a rm can distribute cash to shareholders is through a dividend payment and share

2. Rapidly growing rms may not have su)cient funds available to support all acceptable projects. Such rms depend

3. Dividends are divided by earnings in computaon of the dividend payout rao. Because dividends are more stable than

4. All holders of a rm’s stock in the rm’s stock ledger on the date of record, which is set by the directors, will receive a

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 310

5. The Jobs and Growth Tax Reconciliaon Act of 2003 substanally reduced the marginal tax rate on dividends received

6. Dividend reinvestment plans enable stockholders to use dividends to acquire full or fraconal shares at li%le or no

7. The residual theory of dividends suggests that a rm’s dividend payment should be the amount le7 over (the residual)

8. The dividend irrelevance theory proposed by Miller and Modigliani (M & M) states that in a perfect world the value of a

9. a. Legal constraints prohibit the corporaon from paying out cash dividends that are considered part of a rm’s “legal

b. Contractual constraints limit a rm’s ability to pay dividends according to the restricve covenants in a loan

c. Growth prospects limit the amount of cash dividends because a rm needs to direct all available funds to nance

d. Owner consideraons take into account factors that lead to a dividend policy favorably a:ecng the majority of

e. Market consideraons are the percepons of the stockholders and their response to the dividend policy, which

10. With a constant-payout-rao dividend policy, a rm pays out a certain percentage of earnings each period. A regular

11. A stock dividend is a dividend paid in the form of stock made to exisng owners. Although stock dividends are more

costly to issue than cash dividends, the advantages generally outweigh these costs. Stock dividends are a means of

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 311

12. A stock split is a method of increasing the number of shares belonging to each shareholder. A stock split reduces the par

Suggested Answer to Focus on Ethics Box: Are Buybacks Really

a Bargain?

Do you agree that corporate managers would manipulate their stock’s value prior to a buyback, or do you

believe that corporations are more likely to initiate a buyback to enhance shareholder value?

Student answers will vary based on their views and experiences and their faith, or lack thereof, in corporate

management. As the vignette points out, the study that shows increased earnings after buybacks can be interpreted

Suggested Answer to Focus on Practice Box: Capital Gains and

Dividend Tax Treatment Extended to 2012

How might the expected future reappearance of higher tax rates on individuals receiving dividends affect

corporate dividend payout?

Just as the lowering of the individual tax rates on corporate dividends has stimulated corporate dividend payouts,

The expectation of a return to the 2001 dividend tax policy could in fact be keeping some companies from jumping

Answers to Warm-Up Exercises

E14-1. Relevant dividend dates

Answer: The firm will need $260,000 of cash to pay the dividend. Because a weekend intervenes, the stock will

E14-2. Residual theory of dividend payout

Answer: 1. New investments $2,700,000

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 312

E14-3. Legal constraints on dividend payout

Answer: If legal capital is dened solely as the par value of common stock, Ashkenazi will be able to pay out paid-in capital

in excess of par plus all retained earnings.

E14-4. Constant dividend payout rao

Answer: The first step in analyzing the Kopi scenario is to determine the historical payout ratio.

Year EPS Dividend/Share Dividend Payout Ratio

2012 $1.75 $0.95 54.29%

E14-5. Stock dividend

Answer: After the 10% stock dividend, Hilo’s stockholder’s equity account is as follows:

Solutions to Problems

P14-1. Dividend payment procedures

LG 1; Basic

a. Debit Credit

Retained earnings (Dr.) $330,000

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 313

Dividends payable (Cr.) $330,000

b. Ex dividend date is Thursday, July 6.

d. The dividend payment will result in a decrease in total assets equal to the amount of the payment.

e. Notwithstanding general market fluctuations, the stock price would be expected to drop by the amount

P14-2. Personal finance: Dividend payment

LG 1; Intermediate

a. Friday, May 7

P14-3. Residual dividend policy

LG 2; Intermediate

a. Residual dividend policy means that the firm will consider its investment opportunities first. If after

meeting these requirements there are funds left, the firm will pay the residual out in the form of

dividends. Thus, if the firm has excellent investment opportunities, the dividend will be smaller than if

investment opportunities are limited.

b. Proposed

Capital budget $2,000,000 $3,000,000 $4,000,000

c. The amount of dividends paid is reduced as capital expenditures increase. Thus, if the firm chooses

P14-4. Dividend constraints

LG 3; Intermediate

a. Maximum dividend:

$1,900,000 $4.75 per share

400,000 =

b. Largest dividend without borrowing:

$160,000 $0.40 per share

400,000 =

c. In part a, cash and retained earnings each decrease by $1,900,000.

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 314

P14-5. Dividend constraints

LG 3; Intermediate

a. Maximum dividend:

$40,000 $1.60 per share

25,000 =

b. A $20,000 decrease in cash and retained earnings is the result of a $0.80 per share dividend.

c. Cash is the key constraint because a firm cannot pay out more in dividends than it has in cash, unless

it borrows.

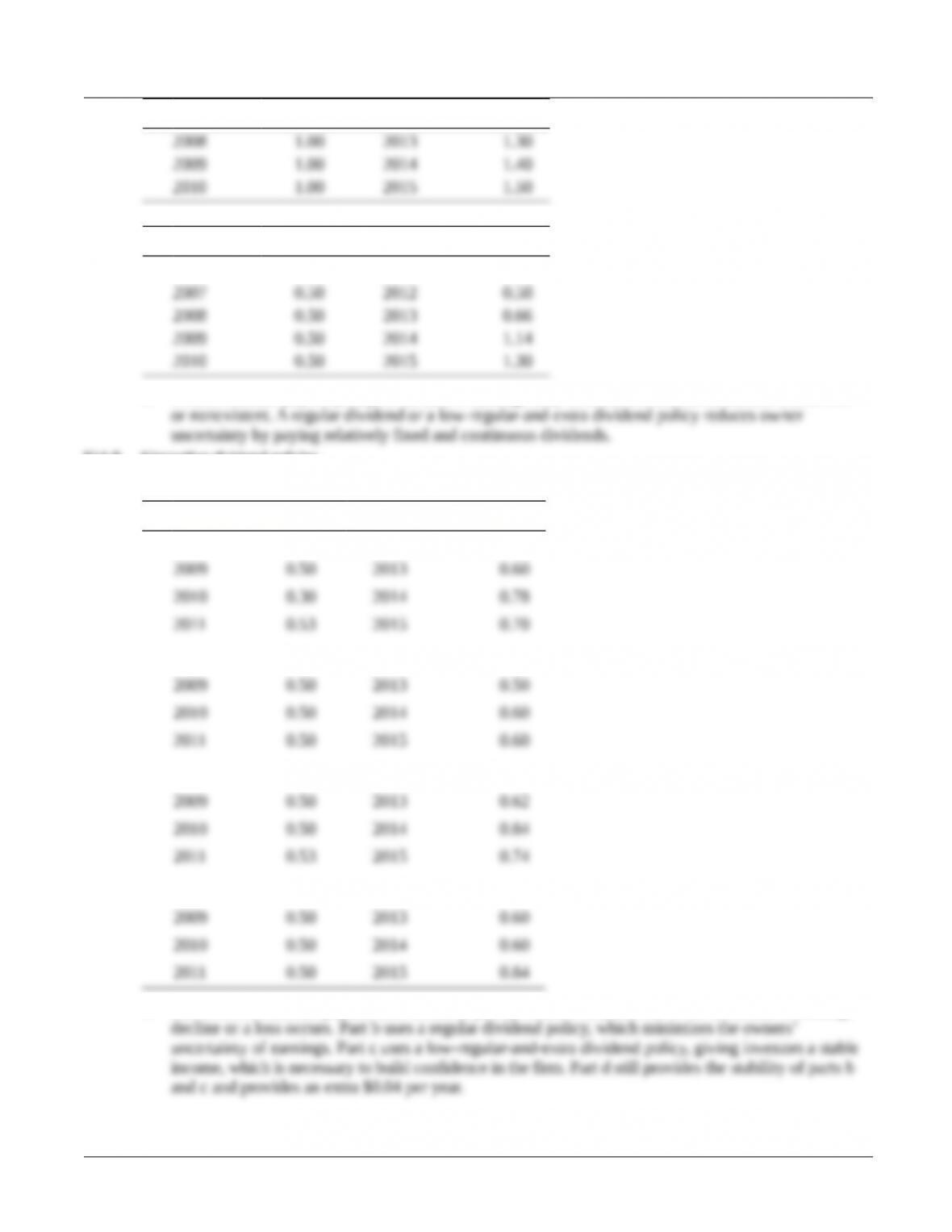

P14-6. Low-regular-and-extra dividend policy

LG 4; Intermediate

a. Year Payout % Year Payout %

b.

Year

25%

Payout

Actual

Payout $ Diff. Year

25%

Payout

Actual

Payout $ Diff.

2010 $0.49 0.50 0.01 2013 0.55 0.50 0.05

c. In this example, the firm would not pay any extra dividend because the actual dividend did not fall

d. If the firm expects the earnings to remain above the earnings per share (EPS) of $2.20, the dividend

P14-7. Alternative dividend policies

LG 4; Intermediate

Year Dividend Year Dividend

a. 2006 $0.10 2011 $1.28

b. 2006 $1.00 2011 $1.10

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 315

Year Dividend Year Dividend

Year Dividend Year Dividend

c. 2006 $0.50 2011 $0.66

d. With a constant-payout policy, if the firm’s earnings drop or a loss occurs, the dividends will be low

P14-8. Alternave dividend policies

LG 4; Challenge

Year Dividend Year Dividend

a. 2008 $0.22 2012 $0.00

b. 2008 $0.50 2012 $0.50

c. 2008 $0.50 2012 $0.50

d. 2008 $0.50 2012 $0.50

e. Part a uses a constant-payout-ratio dividend policy, which will yield low or no dividends if earnings

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 316

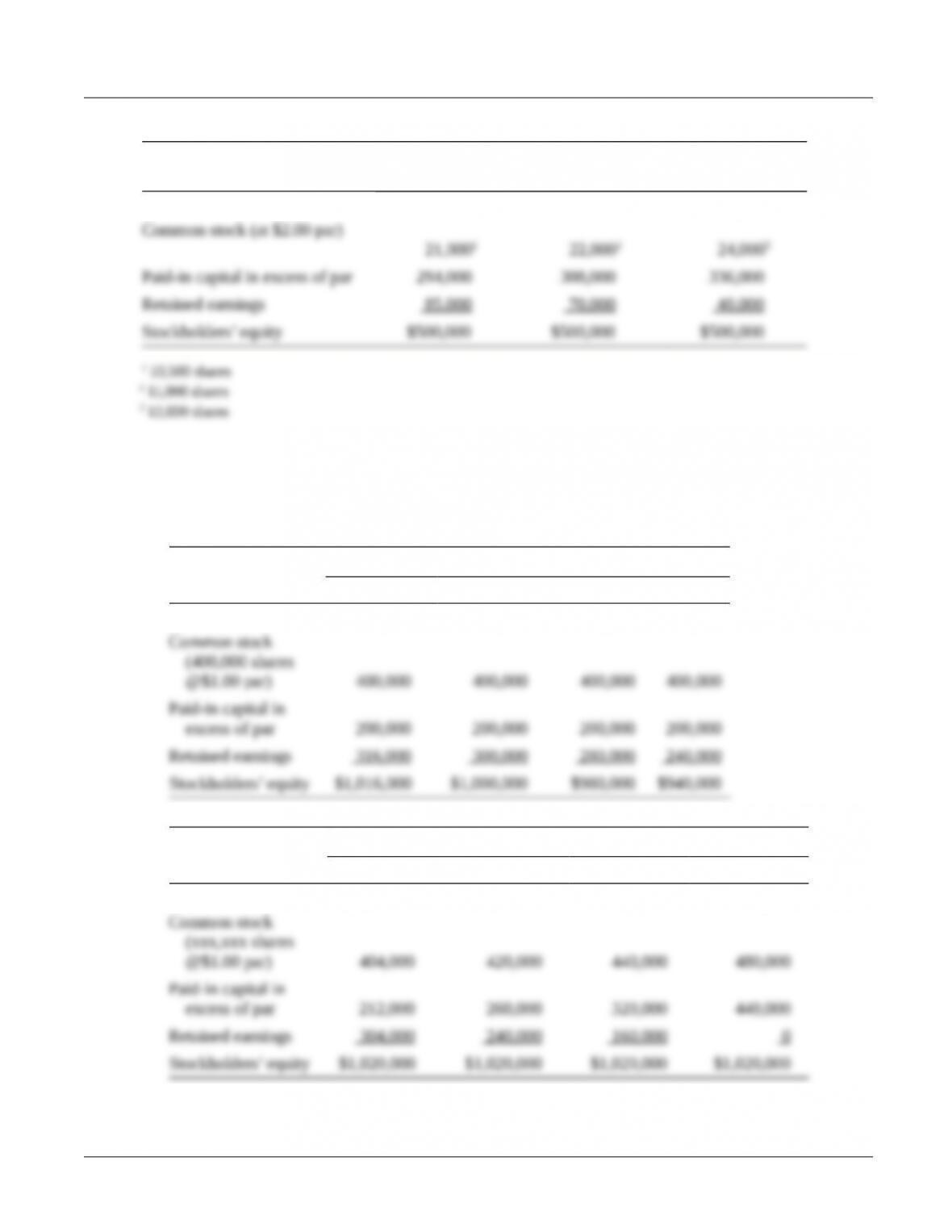

P14-9. Stock dividend—firm

LG 5; Intermediate

(a) 5%

Stock Dividend

(b) (1) 10%

Stock Dividend

(b) (2) 20%

Stock Dividend

Preferred stock $100,000 $100,000 $100,000

c. Stockholders’ equity has not changed. Funds have only been redistributed between the stockholders’

equity accounts.

P14-10. Cash versus stock dividend

LG 5; Intermediate

a.

Cash Dividend

$0.01 $0.05 $0.10 $0.20

Preferred stock $ 100,000 $ 100,000 $100,000 $100,000

b.

Stock Dividend

1% 5% 10% 20%

Preferred stock $ 100,000 $ 100,000 $ 100,000 $ 100,000

© 2015 Pearson Education, Inc.

Chapter 14 Payout Policy 317

c. Stock dividends do not affect stockholders’ equity; they only redistribute retained earnings into

P14-11. Personal finance: Stock dividend—investor

LG 5; Intermediate

a.

= =

$80,000

EPS $2.00

40,000

b.

= =

400

Percent ownership 1.0%

40,000

c. Percent ownership after stock dividend: 440 44,000 1%; stock dividends maintain the same

d. Market price: $22 1.10 $20 per share

e. Her proportion of ownership in the firm will remain the same, and as long as the firm’s earnings

P14-12. Personal finance: Stock dividend—investor

LG 5; Challenge

a.

= =

$120,000

EPS $2.40 per share

50,000

= =

500

b. Percent ownership 1.0%

50,000

His proportionate ownership remains the same in each case

c.

$40

Market price $38.10

1.05

= =

$40

Market price $36.36

1.10

= =

The market price of the stock will drop to maintain the same proportion because more shares are being

used.

d.

= =

$2.40

EPS $2.29 per share

1.05

= =

$2.40

EPS $2.18 per share

1.10

e. Value of holdings: $20,000 under each plan.

As long as the firm’s earnings remain unchanged, his total share of earnings will be the same.

f. The investor should have no preference because the only value is of a psychological nature. After a

stock split or dividend, however, the stock price tends to go up faster than before.