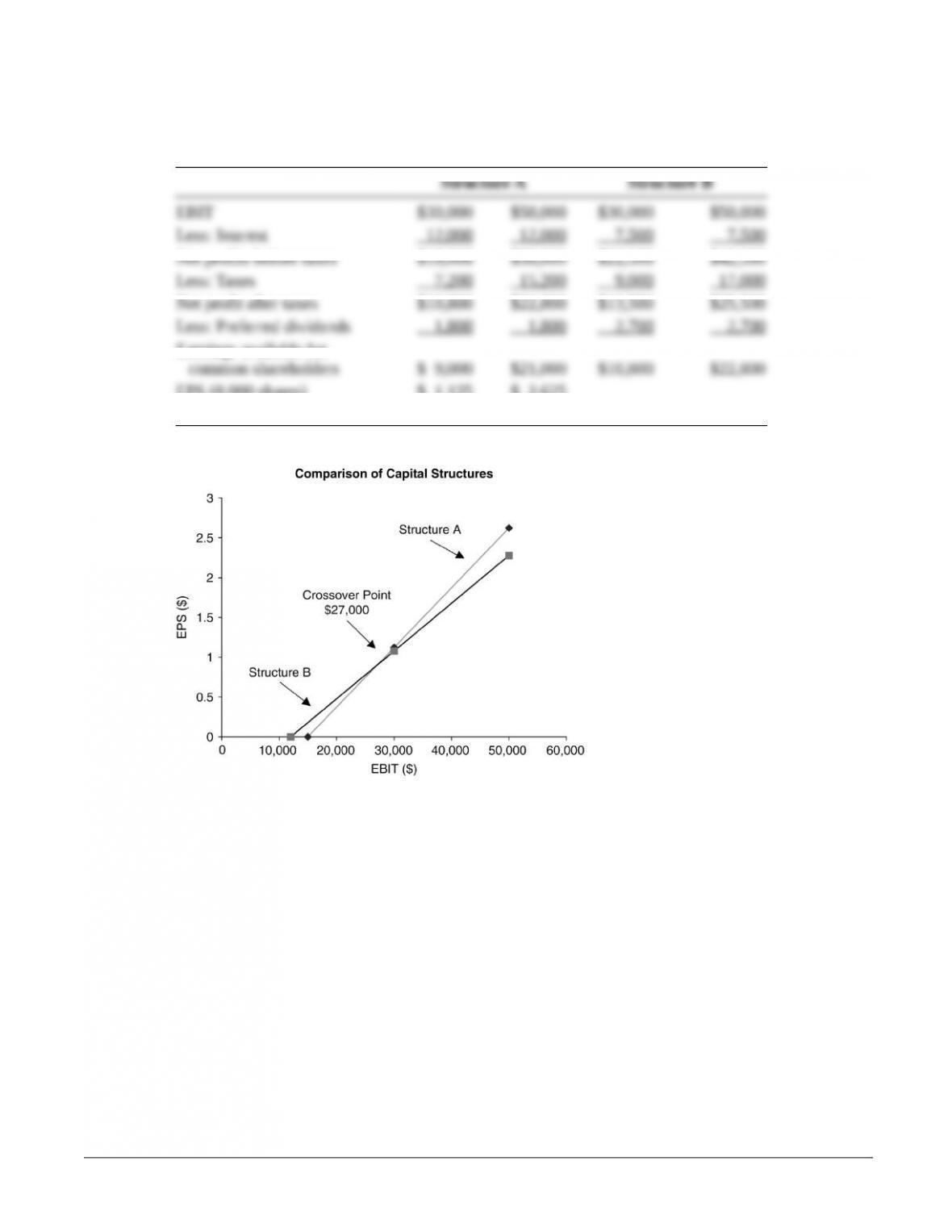

P13-23. EBIT-EPS and preferred stock

LG 5: Intermediate

a.

Structure A Structure B

EBIT $30,000 $50,000 $30,000 $50,000

Less: Interest 12,000 12,000 7,500 7,500

Net profits before taxes $18,000 $38,000 $22,500 $42,500

Less: Taxes 7,200 15,200 9,000 17,000

Net profit after taxes $10,800 $22,800 $13,500 $25,500

Less: Preferred dividends 1,800 1,800 2,700 2,700

Earnings available for

common shareholders $ 9,000 $21,000 $10,800 $22,800

EPS (8,000 shares) $ 1.125 $ 2.625

EPS (10,000 shares) $ 1.08 $ 2.28

b.

c. Structure A has greater financial leverage, hence greater financial risk.

d. If EBIT is expected to be below $27,000, Structure B is preferred. If EBIT is expected to be above

$27,000, Structure A is preferred.

e. If EBIT is expected to be $35,000, Structure A is recommended since changes in EPS are much

greater for given values of EBIT.

© 2015 Pearson Education, Inc.

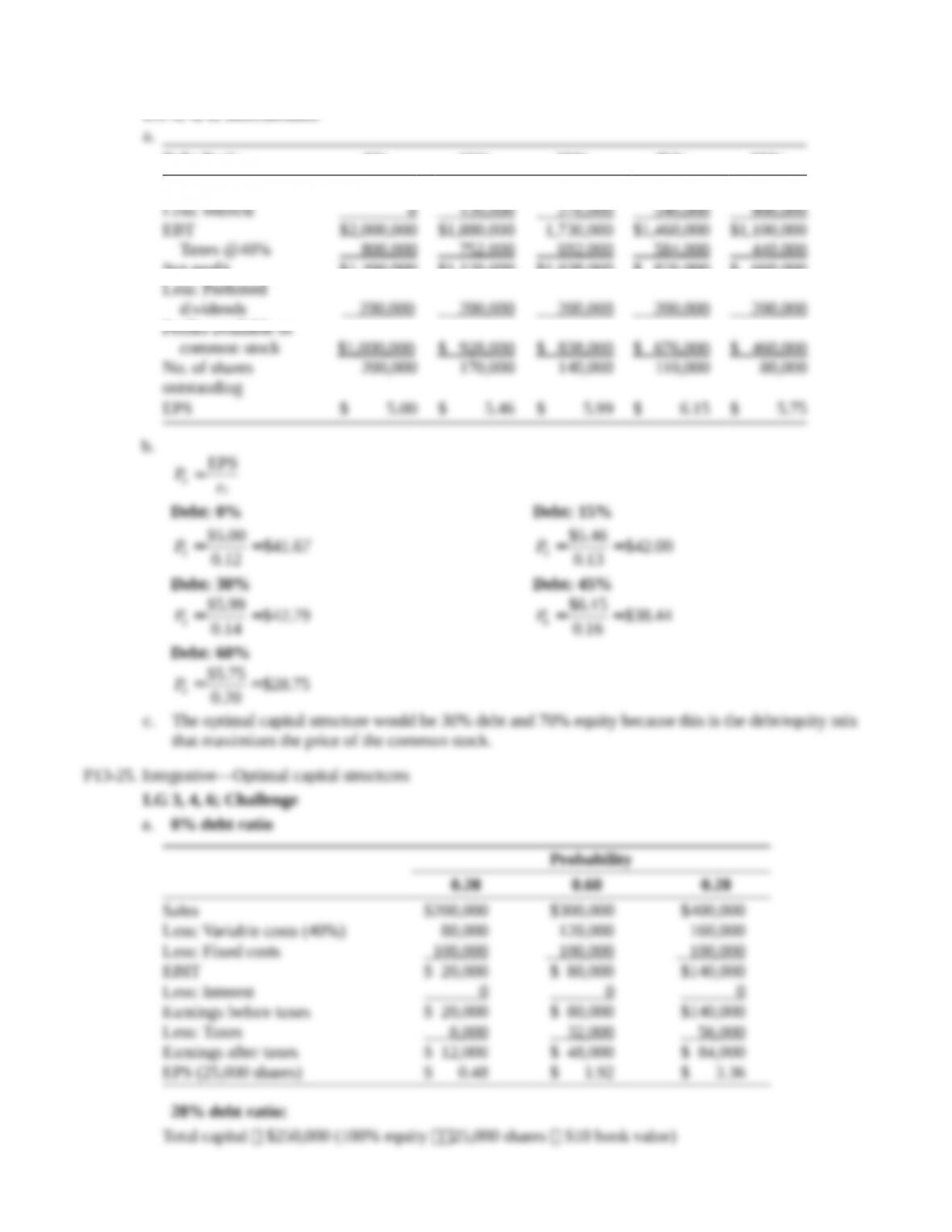

P13-24. Integrative—optimal capital structure

LG 3, 4, 6; Intermediate

a.

Debt Ratio 0% 15% 30% 45% 60%

EBIT $2,000,000 $2,000,000 $2,000,000 $2,000,000 $2,000,000

Less: Interest 0 120,000 270,000 540,000 900,000

EBT $2,000,000 $1,880,000 1,730,000 $1,460,000 $1,100,000

Taxes @40% 800,000 752,000 692,000 584,000 440,000

Net profit $1,200,000 $1,128,000 $1,038,000 $ 876,000 $ 660,000

Less: Preferred

dividends 200,000 200,000 200,000 200,000 200,000

Profits available to

common stock $1,000,000 $ 928,000 $ 838,000 $ 676,000 $ 460,000

No. of shares

outstanding

200,000 170,000 140,000 110,000 80,000

EPS $ 5.00 $ 5.46 $ 5.99 $ 6.15 $ 5.75

b.

=

0

EPS

s

Pr

Debt: 0% Debt: 15%

= =

0

$5.00 $41.67

0.12

P

= =

0

$5.46 $42.00

0.13

P

Debt: 30% Debt: 45%

= =

0

$5.99 $42.79

0.14

P

= =

0

$6.15 $38.44

0.16

P

Debt: 60%

= =

0

$5.75 $28.75

0.20

P

c. The optimal capital structure would be 30% debt and 70% equity because this is the debt/equity mix

that maximizes the price of the common stock.

P13-25. Integrative—Optimal capital structures

LG 3, 4, 6; Challenge

a. 0% debt ratio

Probability

0.20 0.60 0.20

Sales $200,000 $300,000 $400,000

Less: Variable costs (40%) 80,000 120,000 160,000

Less: Fixed costs 100,000 100,000 100,000

EBIT $ 20,000 $ 80,000 $140,000

Less: Interest 0 0 0

Earnings before taxes $ 20,000 $ 80,000 $140,000

Less: Taxes 8,000 32,000 56,000

Earnings after taxes $ 12,000 $ 48,000 $ 84,000

EPS (25,000 shares) $ 0.48 $ 1.92 $ 3.36

20% debt ratio:

Total capital $250,000 (100% equity 25,000 shares $10 book value)

Amount of debt 20% $250,000 $50,000

Amount of equity 80% 250,000 $200,000

Number of shares $200,000 $10 book value 20,000 shares

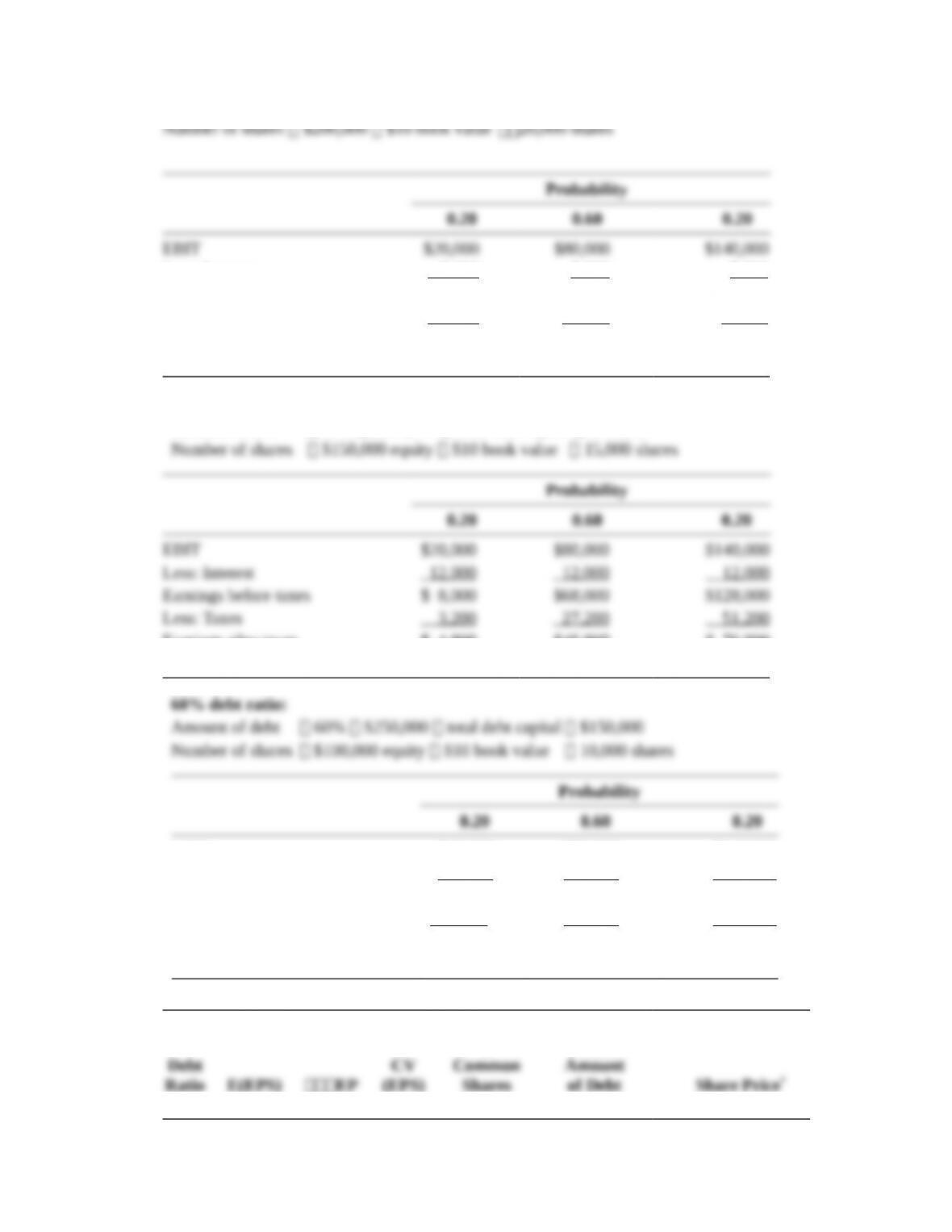

Probability

0.20 0.60 0.20

EBIT $20,000 $80,000 $140,000

Less: Interest 5,000 5,000 5,000

Earnings before taxes $15,000 $75,000 $135,000

Less: Taxes 6,000 30,000 54,000

Earnings after taxes $ 9,000 $45,000 $ 81,000

EPS (20,000 shares) $ 0.45 $ 2.25 $ 4.05

40% debt ratio:

Amount of debt 40% $250,000 total debt capital $100,000

Number of shares $150,000 equity $10 book value 15,000 shares

Probability

0.20 0.60 0.20

EBIT $20,000 $80,000 $140,000

Less: Interest 12,000 12,000 12,000

Earnings before taxes $ 8,000 $68,000 $128,000

Less: Taxes 3,200 27,200 51,200

Earnings after taxes $ 4,800 $40,800 $ 76,800

EPS (15,000 shares) $ 0.32 $ 2.72 $ 5.12

60% debt ratio:

Amount of debt 60% $250,000 total debt capital $150,000

Number of shares $100,000 equity $10 book value 10,000 shares

Probability

0.20 0.60 0.20

EBIT $20,000 $80,000 $140,000

Less: Interest 21,000 21,000 21,000

Earnings before taxes $ (1,000) $59,000 $119,000

Less: Taxes (400) 23,600 47,600

Earnings after taxes $ (600) $35,400 $ 71,400

EPS (10,000 shares) $ (0.06) $ 3.54 $ 7.14

Debt

Ratio E(EPS) EP

S)

CV

(EPS)

Number

of

Common

Shares

Dollar

Amount

of Debt Share Price*

0% $1.92 0.9107 0.4743 25,000 0 $1.92/0.16 $12.00

20% $2.25 1.1384 0.5060 20,000 $ 50,000 $2.25/0.17 $13.24

40% $2.72 1.5179 0.5581 15,000 $100,000 $2.72/0.18 $15.11

60% $3.54 2.2768 0.6432 10,000 $150,000 $3.54/0.24 $14.75

*Share price: E(EPS) required return for CV for E(EPS), from table in problem.

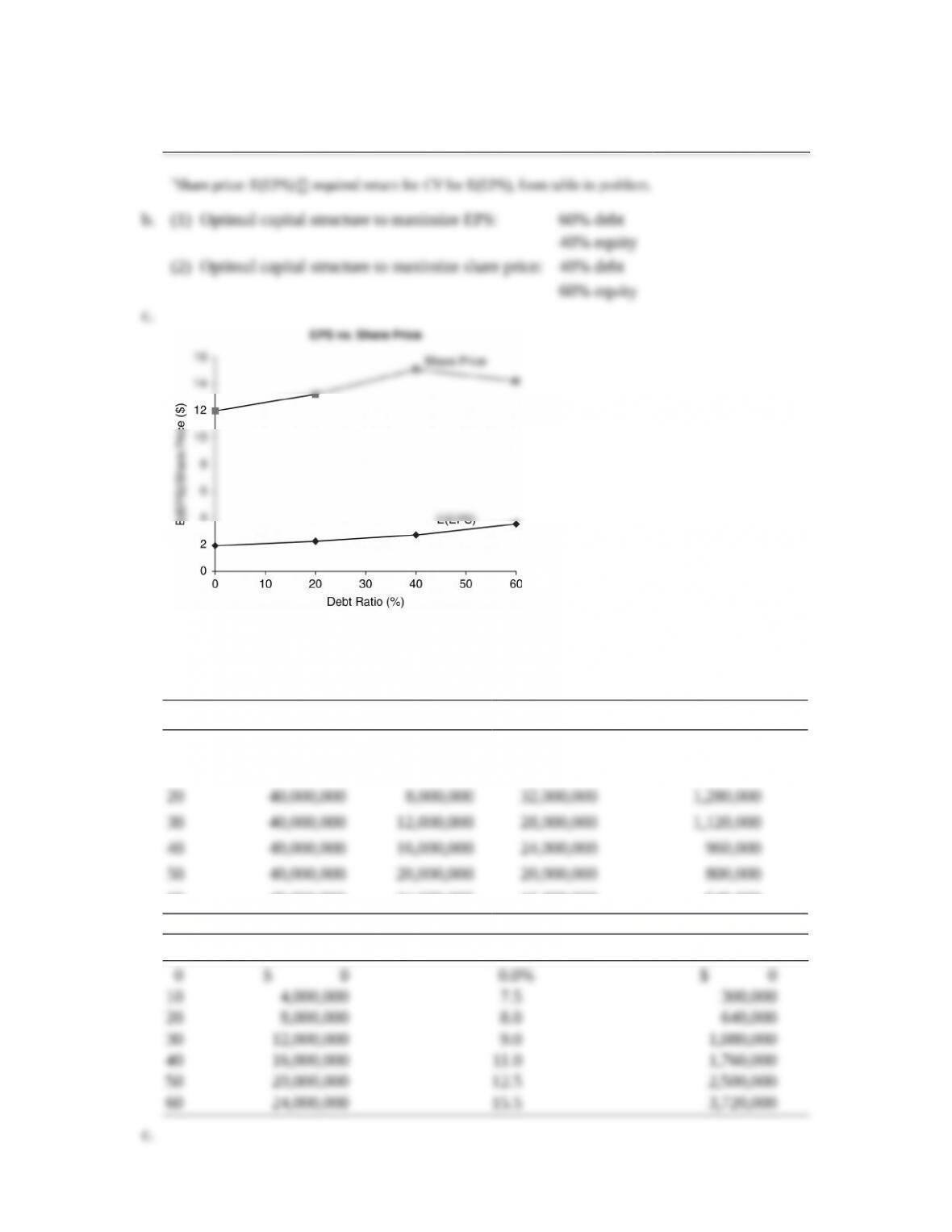

b. (1) Optimal capital structure to maximize EPS: 60% debt

40% equity

(2) Optimal capital structure to maximize share price: 40% debt

60% equity

c.

P13-26. Integrative—optimal capital structure

LG 3, 4, 5, 6; Challenge

a.

% Debt Total Assets $ Debt $ Equity No. of Shares @ $25

0 $40,000,000 $ 0 $40,000,000 1,600,000

10 40,000,000 4,000,000 36,000,000 1,440,000

20 40,000,000 8,000,000 32,000,000 1,280,000

30 40,000,000 12,000,000 28,000,000 1,120,000

40 40,000,000 16,000,000 24,000,000 960,000

50 40,000,000 20,000,000 20,000,000 800,000

60 40,000,000 24,000,000 16,000,000 640,000

b.

% Debt $ Total Debt Before Tax Cost of Debt, kd$ Interest Expense

0 $ 0 0.0% $ 0

10 4,000,000 7.5 300,000

20 8,000,000 8.0 640,000

30 12,000,000 9.0 1,080,000

40 16,000,000 11.0 1,760,000

50 20,000,000 12.5 2,500,000

60 24,000,000 15.5 3,720,000

c.

%

Debt

$ Interest

Expense EBT

Taxes

@40% Net Income

# of

Shares EPS

0 $ 0 $8,000,000 $3,200,000 $4,800,000 1,600,000 $3.00

10 300,000 7,700,000 3,080,000 4,620,000 1,440,000 3.21

20 640,000 7,360,000 2,944,000 4,416,000 1,280,000 3.45

30 1,080,000 6,920,000 2,768,000 4,152,000 1,120,000 3.71

40 1,760,000 6,240,000 2,496,000 3,744,000 960,000 3.90

50 2,500,000 5,500,000 2,200,000 3,300,000 800,000 4.13

60 3,720,000 4,280,000 1,712,000 2,568,000 640,000 4.01

d.

% Debt EPS rSP0

0 $3.00 10.0% $30.00

10 3.21 10.3 31.17

20 3.45 10.9 31.65

30 3.71 11.4 32.54

40 3.90 12.6 30.95

50 4.13 14.8 27.91

60 4.01 17.5 22.91

e. The optimal proportion of debt would be 30% with equity being 70%. This mix will maximize the

price per share of the firm’s common stock and thus maximize shareholders’ wealth. Beyond the 30%

level, the cost of capital increases to the point that it offsets the gain from the lower-costing debt

financing.

P13-27. Integrative—optimal capital structure

LG 3, 4, 5, 6; Challenge

a.

Probability

0.30 0.40 0.30

Sales $600,000 $900,000 $1,200,000

Less: Variable costs (40%) 240,000 360,000 480,000

Less: Fixed costs 300,000 300,000 300,000

EBIT $ 60,000 $240,000 $ 420,000

b.

Debt Ratio

Amount

of Debt

Amount

of Equity

Number of Shares of

Common Stock*

0% $ 0 $1,000,000 40,000

15% 150,000 850,000 34,000

30% 300,000 700,000 28,000

45% 450,000 550,000 22,000

60% 600,000 400,000 16,000

* Dollar amount of equity $25 per share Number of shares of common stock.

c

Amount Before Tax

Debt Ratio of Debt Cost of Debt Annual Interest

0% $ 0 0.0% $ 0

15% 150,000 8.0 12,000

30% 300,000 10.0 30,000

45% 450,000 13.0 58,500

60% 600,000 17.0 102,000

d. EPS [(EBIT interest) (1 T)] number of common shares outstanding

Debt Ratio Calculation EPS

0% ($60,000 $0) (0.6) 40,000 shares $0.90

($240,000 $0) (0.6) 40,000 shares 3.60

($420,000 $0) (0.6) 40,000 shares 6.30

15% ($60,000 $12,000) (0.6) 34,000 shares $0.85

($240,000 $12,000) (0.6) 34,000 shares 4.02

($420,000 $12,000) (0.6) 34,000 shares 7.20

30% ($60,000 $30,000) (0.6) 28,000 shares $0.64

($240,000 $30,000) (0.6) 28,000 shares 4.50

($420,000 $30,000) (0.6) 28,000 shares 8.36

45% ($60,000 $58,500) (0.6) 22,000 shares $0.04

($240,000 $58,500) (0.6) 22,000 shares 4.95

($420,000 $58,500) (0.6) 22,000 shares 9.86

60% ($60,000 $102,000) (0.6) 16,000 shares $1.58

($240,000 $102,000) (0.6) 16,000 shares 5.18

($420,000 $102,000) (0.6) 16,000 shares 11.93

e. (1) E(EPS) 0.30(EPS1) 0.40(EPS2) 0.30(EPS3)

Debt Ratio Calculation E(EPS)

0% 0.30 (0.90) 0.40 (3.60) 0.30 (6.30)

0.27 1.44 1.89 $3.60

15% 0.30 (0.85) 0.40 (4.02) 0.30 (7.20)

0.26 1.61 2.16 $4.03

30% 0.30 (0.64) 0.40 (4.50) 0.30 (8.36)

0.19 1.80 2.51 $4.50

45% 0.30 (0.04) 0.40 (4.95) 0.30 (9.86)

0.01 1.98 2.96 $4.95

60% 0.30 (1.58) 0.40 (5.18) 0.30 (11.93)

0.47 2.07 3.58 $5.18

(2) EPS

Debt

Ratio Calculation

0%

s= – ´ + – ´ + – ´

2 2 2

EPS

[(0.90 3.60) 0.3] [(3.60 3.60) 0.4] [(6.30 3.60) 0.3]

s= + +

EPS

2.187 0 2.187

s=

EPS

4.374

s=

EPS

2.091

15%

s= – ´ + – ´ + – ´

2 2 2

EPS

[(0.85 4.03) 0.3] [(4.03 4.03) 0.4] [(7.20 4.03) 0.3]

Debt

Ratio Calculation

s= + +

EPS

3.034 0 3.034

s=

EPS

6.068

s=

EPS

2.463

30%

s= – ´ + – ´ + – ´

2 2 2

EPS

[(0.64 4.50) 0.3] [(4.50 4.50) 0.4] [(8.36 4.50) 0.3]

s= + +

EPS

4.470 0 4.470

s=

EPS

8.94

s=

EPS

2.99

45%

s= – ´ + – ´ + – ´

2 2 2

EPS

[(0.04 4.95) 0.3] [(4.95 4.95) 0.4] [(9.86 4.95) 0.3]

EPS

7.232 0 7.232s= + +

s=

EPS

14.464

s=

EPS

3.803

60%

s= – – ´ + – ´ + – ´

2 2 2

EPS

[( 1.58 5.18) 0.3] [(5.18 5.18) 0.4] [(11.930 5.18) 0.3]

s= + +

EPS

13.669 0 13.669

s=

EPS

27.338

EPS

5.229s=

(3)

Debt Ratio EPS E(EPS) CV

0% 2.091 3.60 0.581

15% 2.463 4.03 0.611

30% 2.990 4.50 0.664

45% 3.803 4.95 0.768

60% 5.229 5.18 1.009

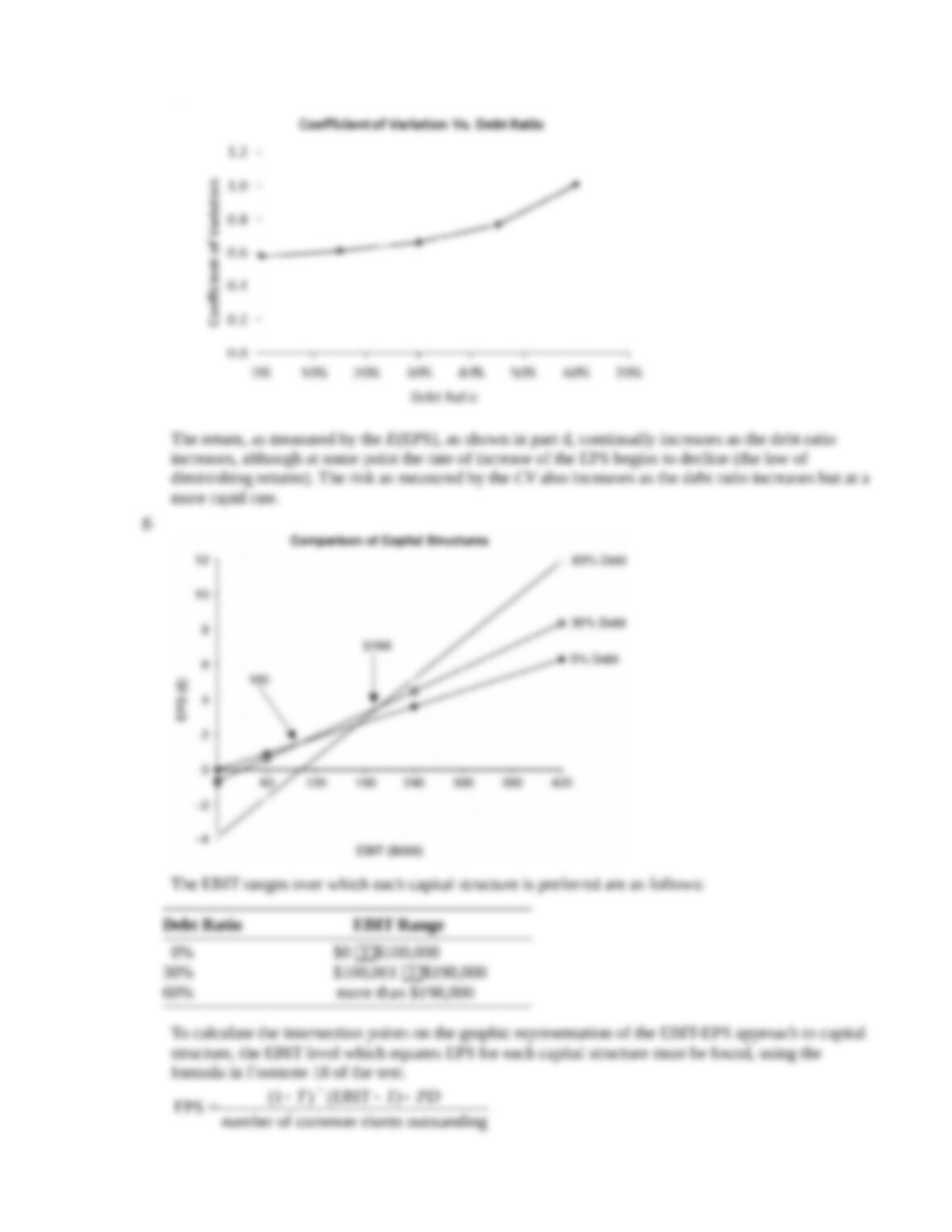

f. (1)

(2)

The return, as measured by the E(EPS), as shown in part d, continually increases as the debt ratio

increases, although at some point the rate of increase of the EPS begins to decline (the law of

diminishing returns). The risk as measured by the CV also increases as the debt ratio increases but at a

more rapid rate.

g.

The EBIT ranges over which each capital structure is preferred are as follows:

Debt Ratio EBIT Range

0% $0 $100,000

30% $100,001 $198,000

60% more than $198,000

To calculate the intersection points on the graphic representation of the EBIT-EPS approach to capital

structure, the EBIT level which equates EPS for each capital structure must be found, using the

formula in Footnote 18 of the text.

– ´ – –

=(1 ) (EBIT )

EPS number of common shares outstanding

T I PD

Set EPS 0% EPS 30%

EPS 30% EPS 60%

The first calculation, EPS 0% EPS 30%, is illustrated:

– – –

=

0%

[(1 0.4)(EBIT $0) 0]

EPS 40,000 shares

– – –

=

30%

[(1 0.4)(EBIT $30,000) 0]

EPS 28,000 shares

16,800 EBIT 24,000 EBIT 720,000,000= –

720,000,000

EBIT= $100,000

7,200 =

The major problem with this approach is that is does not consider maximization of shareholder wealth

(i.e., share price).

h.

Debt Ratio EPS rsShare Price

0% $3.60 0.100 $36.00

15% $4.03 0.105 $38.38

30% $4.50 0.116 $38.79

45% $4.95 0.140 $35.36

60% $5.18 0.200 $25.90

i. To maximize EPS, the 60% debt structure is preferred.

To maximize share value, the 30% debt structure is preferred.

A capital structure with 30% debt is recommended because it maximizes share value and satisfies the

goal of maximization of shareholder wealth.

P13-28. Ethics problem

LG 3; Intermediate

Informaon asymmetry applies to situaons in which one party has more and beer informaon than the other

interested party(ies). This appears to be exactly the situaon in which managers overleverage or lead a buyout of

the company. Exisng bondholders and possibly stockholders are harmed by the !nancial risk of overleveraging,

and exisng stockholders are harmed if they accept a buyout price less than that warranted by accurate and

complete informaon.

The board of directors has a !duciary duty toward stockholders and, hopefully, bears an ethical concern toward

bondholders as well. The board can and should insist that management divulge all informaon it possesses on the

future plans and risks the company faces (although cauon to keep this out of the hands of competors is

warranted). The board should be cauous to select and retain chief execuve o#cers (CEOs) with high integrity and

connue to emphasize an ethical tone “at the top.” (Students will no doubt think of other creave mechanisms to

deal with this situaon.)

Case

Case studies are available on www.myfinancelab.com.

Evaluating Tampa Manufacturing’s Capital Structure

This case asks the student to evaluate Tampa Manufacturing’s current and proposed capital structures in terms of

maximization of EPS and financial risk before recommending one. It challenges the student to go beyond just the

numbers and consider the overall impact of his or her choices on the firm’s financial policies.

a. Times interest earned calculaons

Current

10% Debt

Alternative A

30% Debt

Alternative B

50% Debt

Debt $1,000,000 $3,000,000 $5,000,000

Coupon rate 0.09 0.10 0.12

Interest $ 90,000 $ 300,000 $ 600,000

EBIT $1,200,000 $1,200,000 $1,200,000

Interest $ 90,000 $ 300,000 $ 600,000

Times interest earned 13.33 4 2

As the debt rao increases from 10% to 50%, so do both !nancial leverage and risk. At 10% debt

and $1,200,000 EBIT, the !rm has more than 13 mes coverage of interest payments; at 30%, it sll has

4 mes coverage. At 50% debt, the highest !nancial leverage, coverage drops to 2 mes, which may not provide

enough cushion. Both the mes interest earned and debt raos should be compared to those of the prinng equipment

industry.

b. EBIT-EPS calculaons (using any two EBIT levels)

Current 10% Debt

100,000 Shares

Alternative A: 30% Debt

70,000 Shares

Alternative B: 50% Debt

40,000 Shares

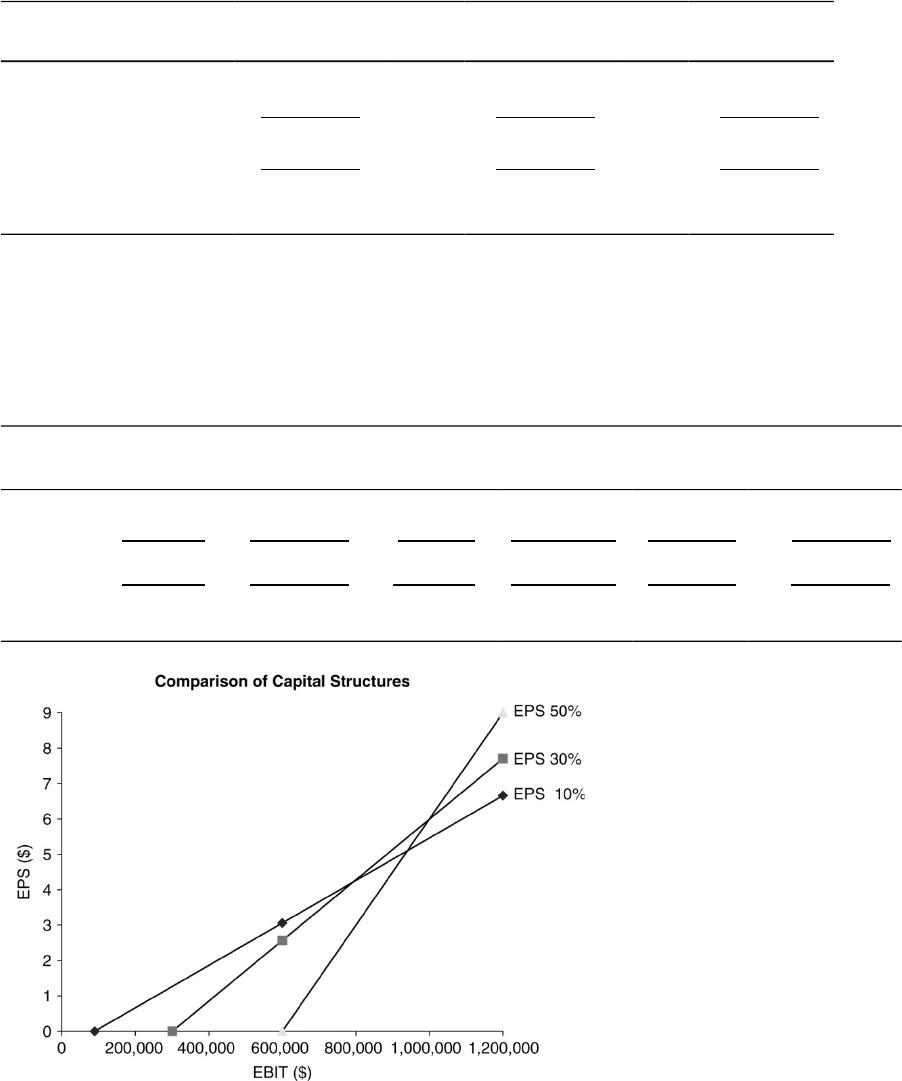

EBIT $600,000 $1,200,000 $600,000 $1,200,000 $600,000 $1,200,000

Interest 90,000 90,000 300,000 300,000 600,000 600,000

PBT $510,000 $1,110,000 $300,000 $ 900,000 $ 0 $ 600,000

Taxes 204,000 444,000 120,000 360,000 0 240,000

PAT $306,000 $ 666,000 $180,000 $ 540,000 $ 0 $ 360,000

EPS $3.06 $ 6.66 $ 2.57 $ 7.71 0 $ 9.00

c. If Tampa Manufacturing’s EBIT is $1,200,000, EPS is highest with the 50% debt rao. The steeper slope of the lines

represenng higher debt levels demonstrates that !nancial leverage increases as the debt rao increases. Although EPS

is highest at 50%, the company must also take into consideraon the !nancial risk of each alternave. The drawback to

the EBIT-EPS approach is its emphasis on maximizing EPS rather than owner’s wealth. It does not take risk into account.

Also, if EBIT falls below about $750,000 (intersecon of 10% and 30% debt), EPS is higher with a capital structure of

10%.

d. Market value: P0 EPS rs

Current: $6.66 0.12 $55.50

Alternative A—30%: $7.71 0.13 $59.31

Alternative B—50%: $9.00 0.18 $50.00

e. Alternave A, 30% debt, appears to be the best alternave. Although EPS is higher with Alternave B, the !nancial risk

is high; mes interest earned is only 2 mes. Alternave A has a moderate risk level, with 4 mes coverage of interest

earned, and provides increased market value. Choosing this capital structure allows the !rm to bene!t from !nancial

leverage while not taking on too much !nancial risk.

Spreadsheet Exercise

The answer to Chapter 13’s determination of the optimal capital structure at Starstruck Company spreadsheet

problem is located on the Instructor’s Resource Center at www pearsonhighered.com/irc under the Instructor’s

Manual.

Group Exercise

Group exercises are available on www.myfinancelab.com.

This chapter links with the previous chapter to continue the valuation process of the firm. The first step is to

retrieve the most recent income statement of their shadow firm. The most important measures from the income

statement include measures of leverage such as EBIT, and fixed and variable operating costs. Using this

information, a similar income statement is designed for the fictitious firm.

After assigning a per-unit price for their product the groups, calculate the operating breakeven point of their

fictitious firm. This should be done using a simple graph of sales revenue and total operating costs, highlighting

the breakeven sales unit level. Next, the groups are required to calculate the DOL at a base sales level.

Returning to their shadow firm, the groups are required to calculate the firm’s DFL at its current levels of EPS and

EBIT. Likewise, the groups are asked to calculate the shadow firm’s DTL at current sales and EPS levels. Equation

13.11 is then used to value the shadow firm and the group’s fictitious firm, using information previously estimated

in earlier assignments. The complexity of this assignment can be mitigated through use of a real-world example.