P13-6. Breakeven point—changing costs/revenues

LG 1; Intermediate

a. Q F (P VC)Q $40,000 ($10 $8.00) 20,000 books

b. Q $44,000 ($10 − $8.00) 22,000 books

c. Q $40,000 ($10.50 − $8.00) 16,000 books

d. Q $40,000 ($10 − $8.50) 26,667 books

e. The operating breakeven point is directly related to fixed and variable costs and inversely related to

selling price. Increases in costs raise the operating breakeven point, while increases in price lower it.

P13-7. Breakeven analysis

LG 1; Challenge

a.

= = =

– –

$4,000 2,000 figurines

( ) $8.00 $6.00

FC

QP VC

b. Sales $10,000

Less:

Fixed costs 4,000

Variable costs ($6 1,500) 9,000

EBIT $3,000

c. Sales $15,000

Less:

Fixed costs 4,000

Variable costs ($6 1,500) 9,000

EBIT $2,000

d.

+ +

= = = =

– –

EBIT $4,000 $4,000 $8,000 4,000 units

$8 $6 $2

FC

QP VC

e. One alternative is to price the units differently based on the variable cost of the unit. Those more

costly to produce will have higher prices than the less expensive production models. If they wish to

maintain the same price for all units they may need to reduce the selection from the 15 types currently

available to a smaller number that includes only those that have an average variable cost below $5.33

($8 $4,000/1,500 units).

P13-8. EBIT sensitivity

LG 2; Intermediate

a. and b.

8,000 Units 10,000 Units 12,000 Units

Sales $72,000 $90,000 $108,000

Less: Variable costs 40,000 50,000 60,000

Less: Fixed costs 20,000 20,000 20,000

EBIT $12,000 $20,000 $ 28,000

c.

Unit Sales 8,000 10,000 12,000

Percentage (8,000 10,000) 10,000 (12,000 10,000) 10,000

© 2015 Pearson Education, Inc.

Change in

unit sales 20% 0 20%

Percentage (12,000 20,000) 20,000 (28,000 20,000) 20,000

Change in

EBIT 40% 0 40%

d. EBIT is more sensitive to changing sales levels; it increases/decreases twice as much as sales.

P13-9. DOL

LG 2; Intermediate

a.

$380,000 8,000 units

( ) $63.50 $16.00

FC

QP VC

= = =

– –

9,000 Units 10,000 Units 11,000 Units

b.

Sales $571,500 $635,000 $698,500

Less: Variable costs 144,000 160,000 176,000

Less: Fixed costs 380,000 380,000 380,000

EBIT $ 47,500 $ 95,000 $142,500

c.

Change in unit sales 1,000 0 1,000

% change in sales 1,000 10,000 10% 0 1,000 10,000 10%

Change in EBIT $47,500 0 $47,500

% Change in EBIT $47,500 95,000 = 50% 0 $47,500 95,000 = 50%

d.

% change in EBIT

% change in sales

50 10 5 50 10 5

e.

´ –

=´ – –

[ ( )]

DOL [ ( )]

Q P VC

Q P VC FC

´ –

=´ – –

[10,000 ($63.50 $16.00)]

DOL [10,000 ($63.50 $16.00) $380,000]

= =

$475,000

DOL 5.00

$95,000

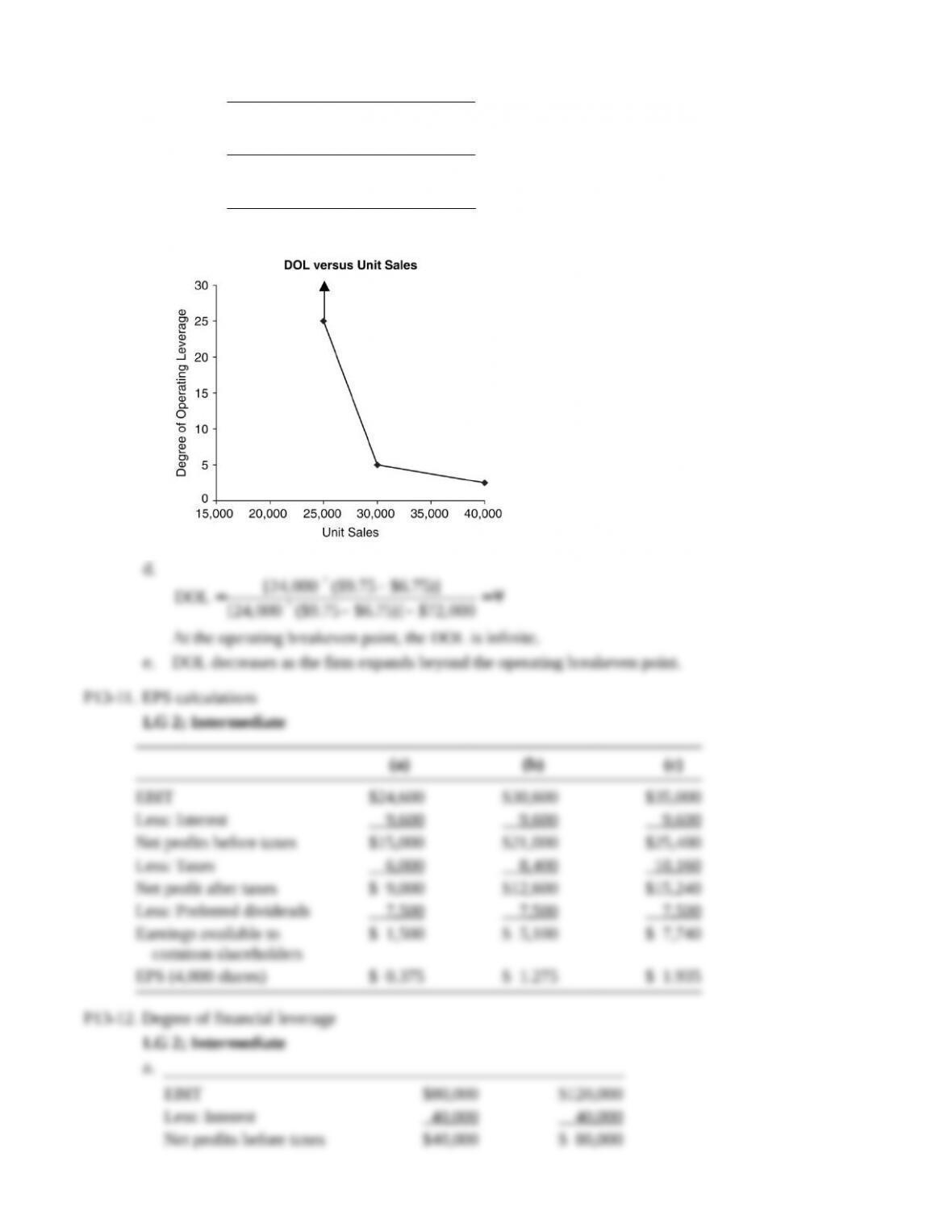

P13-10. DOL—graphic

LG 2; Intermediate

a.

$72,000 24,000 units

( ) $9.75 $6.75

FC

QP VC

= = =

– –

b.

´ –

=´ – –

[ ( )]

DOL [ ( )]

Q P VC

Q P VC FC

´ –

= =

´ – –

[25,000 ($9.75 $6.75)]

DOL 25.0

[25,000 ($9.75 $6.75)] $72,000

´ –

= =

´ – –

[30,000 ($9.75 $6.75)]

DOL 5.0

[30,000 ($9.75 $6.75)] $72,000

´ –

= =

´ – –

[40,000 ($9.75 $6.75)]

DOL 2.5

[40,000 ($9.75 $6.75)] $72,000

c.

d.

´ –

= =¥

´ – –

[24,000 ($9.75 $6.75)]

DOL [24,000 ($9.75 $6.75)] $72,000

At the operating breakeven point, the DOL is infinite.

e. DOL decreases as the firm expands beyond the operating breakeven point.

P13-11. EPS calculations

LG 2; Intermediate

(a) (b) (c)

EBIT $24,600 $30,600 $35,000

Less: Interest 9,600 9,600 9,600

Net profits before taxes $15,000 $21,000 $25,400

Less: Taxes 6,000 8,400 10,160

Net profit after taxes $ 9,000 $12,600 $15,240

Less: Preferred dividends 7,500 7,500 7,500

Earnings available to

common shareholders

$ 1,500 $ 5,100 $ 7,740

EPS (4,000 shares) $ 0.375 $ 1.275 $ 1.935

P13-12. Degree of financial leverage

LG 2; Intermediate

a.

EBIT $80,000 $120,000

Less: Interest 40,000 40,000

Net profits before taxes $40,000 $ 80,000

Less: Taxes (40%) 16,000 32,000

Net profit after taxes $24,000 $ 48,000

EPS (2,000 shares) $ 12.00 $ 24.00

b.

EBIT

DFL 1

EBIT (1 )

I PD T

=é ù

æ ö

– – ´

ê ú

ç ÷

–

è ø

ë û

= =

– –

$80,000

DFL 2

[$80,000 $40,000 0]

c.

EBIT $80,000 $120,000

Less: Interest 16,000 16,000

Net profits before taxes $64,000 $104,000

Less: Taxes (40%) 25,600 41,600

Net profit after taxes $38,400 $ 62,400

EPS (3,000 shares) $ 12.80 $ 20.80

= =

– –

$80,000

DFL 1.25

[$80,000 $16,000 0]

P13-13. Personal finance: Financial leverage

LG 2; Challenge

a.

Current DFL Initial Values Future Value

Percentage

Change

Available for making loan payment

Less: Loan payments

Available after loan payments

$3,000

$1,000

$2,000

$3,300

$1,000

$2,300

10.0%

0.0%

15.0%

DFL 15% ÷ 10% 1.50

Proposed DFL Initial Values Future Value

Percentage

Change

Available for making loan payment

Less: Loan payments

Available after loan payments

$3,000

$1,350

$1,650

$3,300

$1,350

$1,950

10.0%

0.0%

18.2%

DFL 18.2% ÷ 10% 1.82

b. and c. Based on his calculations, the amount that Max will have available after loan payments with his

current debt changes by 1.5% for every 1% change in the amount he will have available for making

the loan payment. This is less responsive and therefore less risky than the 1.82% change in the amount

available after making loan payments with the proposed $350 in monthly debt payments. Although it

appears that Max can afford the additional loan payments, he must decide if, given the variability of

Max’s income, he would feel comfortable with the increased financial leverage and risk.

P13-14. DFL and graphic display of financing plans

LG 2, 5; Challenge

a.

=é ù

æ ö

– – ´

ê ú

ç ÷

–

è ø

ë û

EBIT

DFL 1

EBIT (1 )

I PD T

= =

– –

$67,500

DFL 1.5

[$67,500 $22,500 0]

b.

c.

= =

é ù

– –

ê ú

ë û

$67,500

DFL 1.93

$6,000

$67,500 $22,500 0.6

d. See graph, which is based on the following equation and data points.

Financing EBIT EPS

Original

financing

plan

$67,500

($67,000 $22,500)(1 0.4) $1.80

15,000

– – =

$17,500

($17,500 $22,500)(1 0.4) $0.20

15,000

– – =–

Revised

financing

plan

$67,500

($67,000 $22,500)(1 0.4) 6,000 $1.40

15,000

– – – =

$17,500

($17,500 $22,500)(1 0.4) 6,000 $0.60

15,000

– – – =–

e. The lines representing the two financing plans are parallel because the number of shares of common

stock outstanding is the same in each case. The financing plan, including the preferred stock, results

in a higher financial breakeven point and a lower EPS at any EBIT level.

P13-15. Integrative—multiple leverage measures

LG 1, 2; Intermediate

a.

$28,000

Operating breakeven 175,000 units

$0.16

= =

b.

´ –

=´ – –

[ ( )]

DOL [ ( )]

Q P VC

Q P VC FC

´ –

= = =

´ – –

[400,000 ($1.00 $0.84)] $64,000

DOL 1.78

[400,000 ($1.00 $0.84)] $28,000 $36,000

c. EBIT (P Q) FC (Q VC)

EBIT ($1.00 400,000) $28,000 (400,000 $0.84)

EBIT $400,000 $28,000 $336,000

EBIT $36,000

=é ù

æ ö

– – ´

ê ú

ç ÷

–

è ø

ë û

EBIT

DFL 1

EBIT (1 )

I PD T

= =

é ù

æ ö

– –

ê ú

ç ÷

–

è ø

ë û

$36,000

DFL 1.35

$2,000

$36,000 $6,000 (1 0.4)

d.

*

[ ( )]

DTL

( ) (1 )

Q P VC

PD

Q P VC FC I T

´ –

=é ù

æ ö

´ – – – –

ê ú

ç ÷

–

è ø

ë û

´ –

=é ù

æ ö

´ – – – –

ê ú

ç ÷

–

è ø

ë û

[400,000 ($1.00 $0.84)]

DTL $2,000

400,000 ($1.00 $0.84) $28,000 $6,000 (1 0.4)

= = =

– –

$64,000 $64,000

DTL 2.40

[$64,000 $28,000 $9,333] $26,667

DTL DOL DFL

DTL 1.78 1.35 2.40

The two formulas give the same result.

*Degree of total leverage.

P13-16. Integrative—leverage and risk

LG 2; Intermediate

a.

´ –

= = =

´ – –

[100,000 ($2.00 $1.70)] $30,000

DOL 1.25

[100,000 ($2.00 $1.70)] $6,000 $24,000

R

= =

–

$24,000

DFL 1.71

[$24,000 $10,000]

R

= ´ =DTL 1.25 1.71 2.14

R

b.

´ –

= = =

´ – –

[100,000 ($2.50 $1.00)] $150,000

DOL 1.71

[100,000 ($2.50 $1.00)] $62,500 $87,500

W

= =

–

$87,500

DFL 1.25

[$87,500 $17,500]

W

= ´ =DTL 1.71 1.25 2.14

R

c. Firm R has less operating (business) risk but more financial risk than Firm W.

d. Two firms with differing operating and financial structures may be equally leveraged. Because total

leverage is the product of operating and financial leverage, each firm may structure itself differently

and still have the same amount of total risk.

P13-17. Integrative—multiple leverage measures and prediction

LG 1, 2; Challenge

a. Q FC (P VC) Q $50,000 ($6 $3.50) 20,000 latches

b. Sales ($6 30,000) $180,000

Less:

Fixed costs 50,000

Variable costs ($3.50 30,000) 105,000

EBIT 25,000

Less interest expense 13,000

EBT 12,000

Less taxes (40%) 4,800

Net profits $ 7,200

Net profits – Preference dividends = Earnings available for common stockholders

$7,200 – $7,000 = $200

c.

´ –

=´ – –

[ ( )]

DOL [ ( )]

Q P VC

Q P VC FC

´ –

= = =

´ – –

[30,000 ($6.00 $3.50)] $75,000

DOL 3.0

[30,000 ($6.00 $3.50)] $50,000 $25,000

d.

=é ù

æ ö

– – ´

ê ú

ç ÷

–

è ø

ë û

EBIT

DFL 1

EBIT (1 )

I PD T

= = =

– – ´ ¸

$25,000 $25,000

DFL 75.00

$25,000 $13,000 [$7,000 (1 0.6)] $333.33

e. DTL DOL DFL 3 75.00 225 (or 22,500%)

f.

15,000

Change in sales 50%

30,000

= =

Percentage change in EBIT % change in sales DOL 50% 3 150%

New EBIT $25,000 ($25,000 150%) $62,500

Percentage change in earnings available for common % changesales DTL

50% 225% 11,250%

New earnings available for common $200 ($200 11,250%) $22,700

P13-18. Personal finance: Capital structures

LG 3; Intermediate

a. Monthly mortgage payment ÷ Monthly gross income = $1,100 ÷ $4,500 = 24.44%

Kirsten’s ratio is less than the bank maximum of 28%.

b. Total monthly installment payment ÷ Monthly gross income

($375 + $1,100) ÷ $4,500 32.8%.

Kirsten’s ratio is less than the bank maximum of 37.0%. Because Kirsten’s debt-related expenses as a

percentage of her monthly gross income are less than bank-specified maximums, her loan application

should be accepted.

P13-19. Various capital structures

LG 3; Basic

Debt Ratio Debt Equity

10% $100,000 $900,000

20% $200,000 $800,000

30% $300,000 $700,000

40% $400,000 $600,000

50% $500,000 $500,000

60% $600,000 $400,000

90% $900,000 $100,000

Theoretically, the debt ratio cannot exceed 100%. Practically, few creditors would extend loans to

companies with exceedingly high debt ratios (70%).

P13-20. Debt and financial risk

LG 3; Challenge

a. EBIT Calculation

Probability 0.20 0.60 0.20

Sales $200,000 $300,000 $400,000

Less: Variable costs (70%) 140,000 210,000 280,000

Less: Fixed costs 75,000 75,000 75,000

EBIT $(15,000) $ 15,000 $ 45,000

Less: Interest 12,000 12,000 12,000

Earnings before taxes $(27,000) $ 3,000 $ 33,000

Less: Taxes (10,800) 1,200 13,200

Earnings after taxes $(16,200) $ 1,800 $ 19,800

b. EPS

Earnings after taxes $(16,200) $ 1,800 $ 19,800

Number of shares 10,000 10,000 10,000

EPS $ (1.62) $ 0.18 $ 1.98

=

= ´

å

1

Expected EPS EPS Pr

n

j j

i

Expected EPS ($1.62 0.20) ($0.18 0.60) ($1.98 0.20)

Expected EPS $0.324 $0.108 $0.396

Expected EPS $0.18

s

=

= – ´

å

2

EPS

1

(EPS EPS) Pr

n

i i

i

s= – – ´ + – ´ + – ´

2 2 2

EPS

[( $1.62 $0.18) 0.20] [($0.18 $0.18) 0.60] [($1.98 $0.18) 0.20]

s= ´ + + ´EPS ($3.24 0.20) 0 ($3.24 0.20)

s= +

EPS

$0.648 $0.648

s= =

EPS

$1.296 $1.138

s

= = =

EPS

EPS

1.138 6.32

Expected EPS 0.18

CV

c.

EBIT *$(15,000) $15,000 $45,000

Less: Interest 0 0 0

Net profit before taxes $(15,000) $15,000 $45,000

Less: Taxes (6,000) 6,000 18,000

Net profits after taxes $ (9,000) $ 9,000 $27,000

EPS (15,000 shares) $ (0.60) $ 0.60 $ 1.80

*From part a

Expected EPS ($0.60 0.20) ($0.60 0.60) ($1.80 0.20) $0.60

2 2 2

EPS

[( $0.60 $0.60) 0.20] [($0.60 $0.60) 0.60] [($1.80 $0.60) 0.20]s= – – ´ + – ´ + – ´

s= ´ + + ´EPS ($1.44 0.20) 0 ($1.44 0.20)

s= =

EPS

$0.576 $0.759

= =

EPS

$0.759 1.265

0.60

CV

d. Summary statistics

With Debt All Equity

Expected EPS $0.180 $0.600

EPS $1.138 $0.759

CVEPS 6.320 1.265

Including debt in Tower Interiors’ capital structure results in a lower expected EPS, a higher standard

deviation, and a much higher coefficient of variation than the all-equity structure. Eliminating debt

from the firm’s capital structure greatly reduces financial risk, which is measured by the coefficient of

variation.

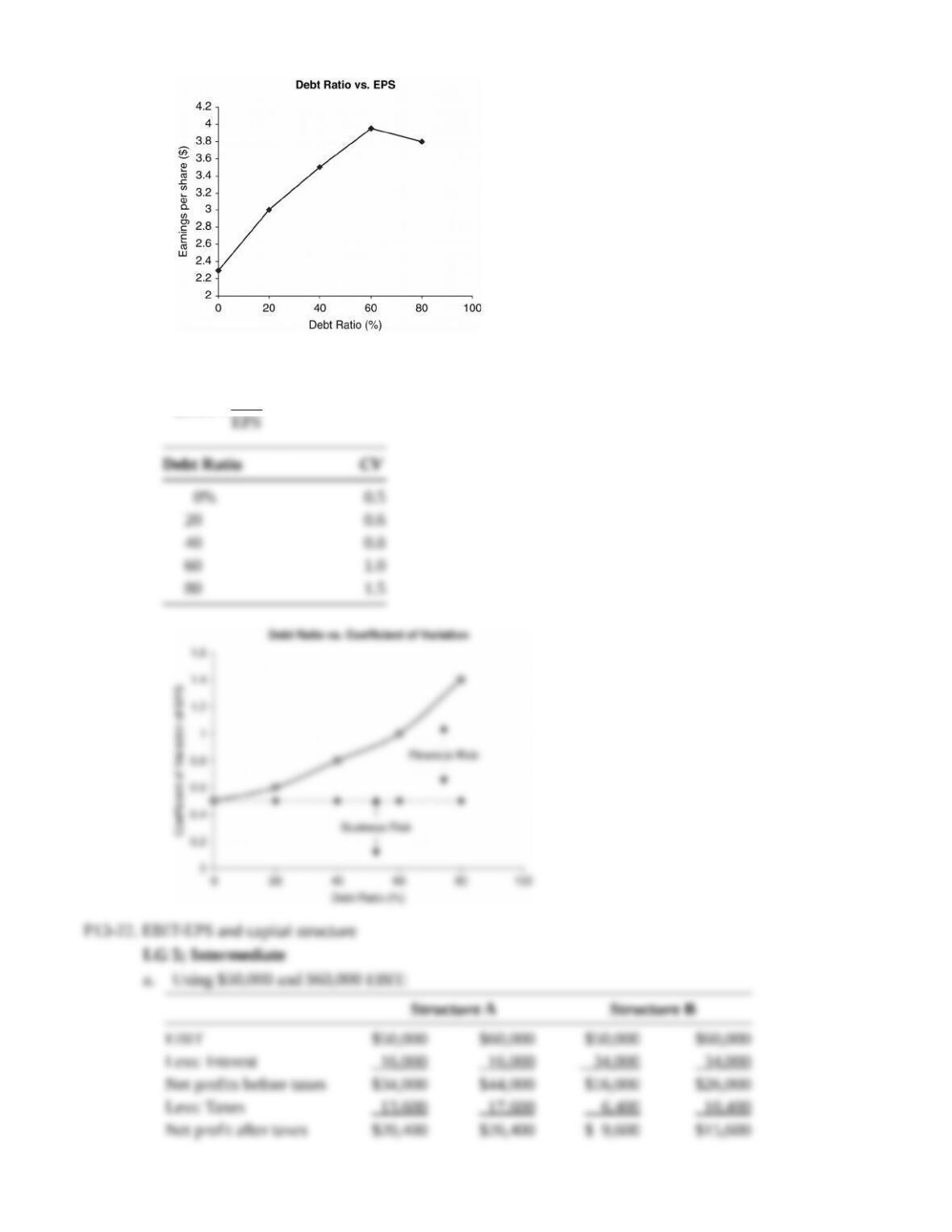

P13-21. EPS and optimal debt ratio

LG 4; Intermediate

a.

Maximum EPS appears to be at 60% debt ratio, with $3.95 per share earnings.

b.

s

=

EPS

EPS

EPS

CV

Debt Ratio CV

0% 0.5

20 0.6

40 0.8

60 1.0

80 1.5

P13-22. EBIT-EPS and capital structure

LG 5; Intermediate

a. Using $50,000 and $60,000 EBIT:

Structure A Structure B

EBIT $50,000 $60,000 $50,000 $60,000

Less: Interest 16,000 16,000 34,000 34,000

Net profits before taxes $34,000 $44,000 $16,000 $26,000

Less: Taxes 13,600 17,600 6,400 10,400

Net profit after taxes $20,400 $26,400 $ 9,600 $15,600

EPS (4,000 shares) $ 5.10 $ 6.60

EPS (2,000 shares) $ 4.80 $ 7.80

Financial breakeven points:

Structure A Structure B

$16,000 $34,000

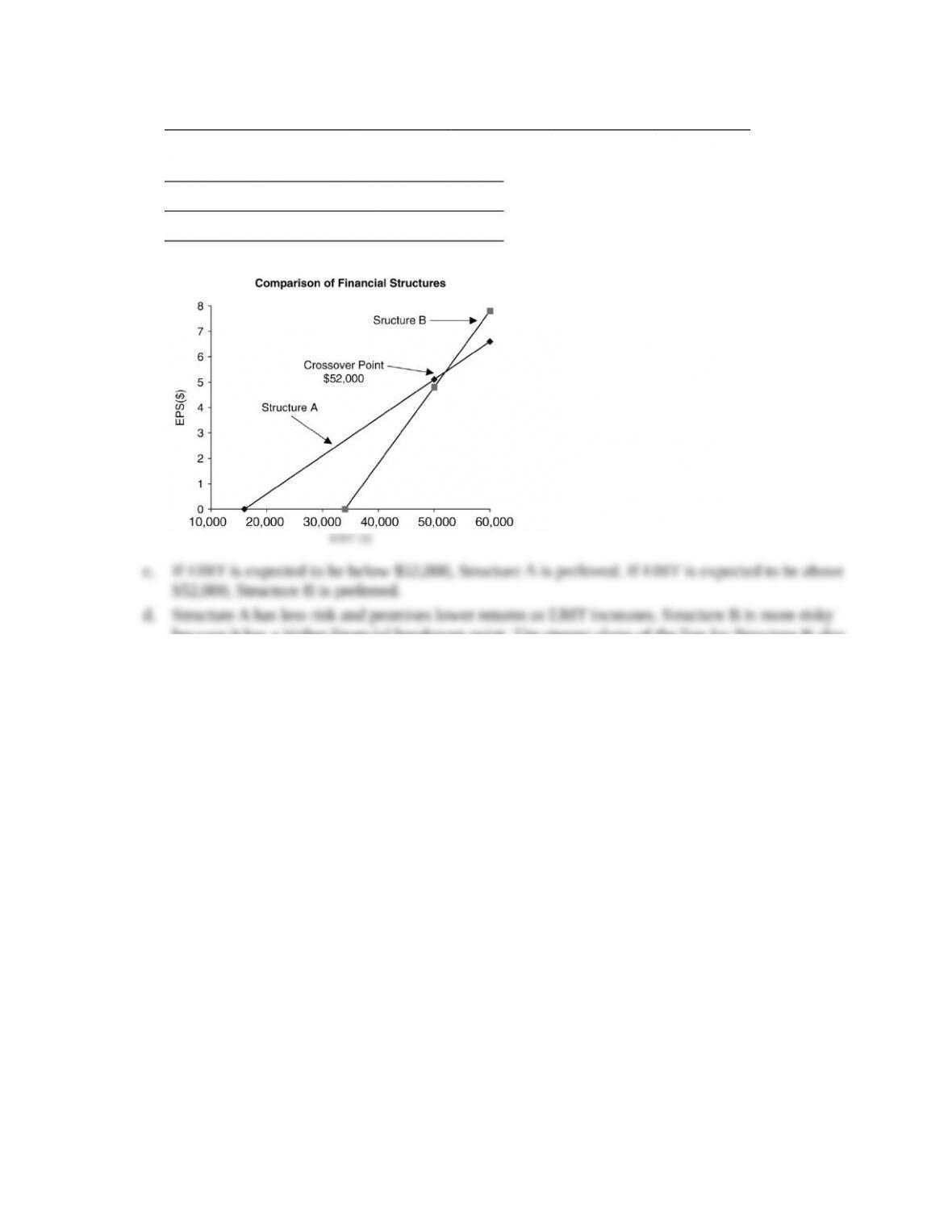

b.

c. If EBIT is expected to be below $52,000, Structure A is preferred. If EBIT is expected to be above

$52,000, Structure B is preferred.

d. Structure A has less risk and promises lower returns as EBIT increases. Structure B is more risky

because it has a higher financial breakeven point. The steeper slope of the line for Structure B also

indicates greater financial leverage.

e. If EBIT is greater than $75,000, Structure B is recommended because changes in EPS are much

greater for given values of EBIT.