P12-12. Risk classes and RADR

LG 4; Basic

a. Project X

Project Y

Project Z

b. Projects X and Y are acceptable with positive NPVs, while Project Z with a negative NPV is not.

P12-13. Unequal lives—ANPV approach

LG 5; Intermediate

a. Machine A

Machine B

Machine C

Rank Machine

b. Machine A

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 254

Machine B

Machine C

Rank Machine

c. Machine B should be acquired because it offers the highest ANPV. Not considering the difference in

project lives resulted in a different ranking based in part on Machine C’s NPV calculations.

P12-14. Unequal lives—ANPV approach

LG 5; Intermediate

a. Project X

Project Y

Project Z

Rank Project

b. Project X

Project Y

Project Z

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 255

Rank Project

c. Project Y should be acquired because it offers the highest ANPV. Not considering the difference in

project lives resulted in a different ranking based primarily on the unequal lives of the projects.

P12-15. Unequal lives—ANPV approach

LG 5; Intermediate

a. Sell

License

Manufacture

Rank Alternative

b. Sell

Rank Alternative

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 256

P12-16. NPV and ANPV decisions

LG 5; Challenge

a. – b. Unequal-Life Decisions

Annualized Net Present Value (ANPV)

Samsung Sony

P12-17. Real options and the strategic NPV

LG 6; Intermediate

a. Value of real options value of abandonment value of expansion value of delay

b. Due to the added value from the options, Rene should recommend acceptance of the capital

c. In general this problem illustrates that by recognizing the value of real options a project that would

P12-18. Capital rationing—IRR and NPV approaches

LG 6; Intermediate

a. Rank by IRR

Project IRR Initial Investment Total Investment

F 23% $2,500,000 $2,500,000

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 257

Projects F, E, and G require a total investment of $4,500,000 and provide a total present value of

$5,200,000 and, therefore, an NPV of $700,000.

b. Rank by NPV (NPV PV – Initial investment)

Project NPV Ini!al Investment

F $500,000 $2,500,000

c. The internal rate of return approach uses the entire $4,500,000 capital budget but provides $200,000

d. The firm should implement Projects B, F, and G, as explained in part c.

P12-19. Capital Rationing—NPV Approach

LG 6; Intermediate

Project Ini!al

investment

NPV at 13% PV

A $300,000 $ 84,000 $384,000

b. The optimal group of projects is Projects C, F, and G, resulting in a total net present value of

P12-20. Ethics problem

LG 4; Challenge

Student answers will vary. Some students might argue that companies should be held accountable for any

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 258

Case

Case studies are available on www.myfinancelab.com.

Evaluating Cherone Equipment’s Risky Plans for Increasing Its Production Capacity

a. 1. Plan X

Plan Y

2. Using a financial calculator, the IRRs are:

b. Plan X

Plan Y

Ranking

Plan NPV IRR RADRs

c. Both NPV and IRR achieved the same rela5ve rankings. However, making risk adjustments through the RADRs caused

d. Plan X

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 259

Plan Y

e. With the addi5on of the value added by the existence of real op5ons, the ordering of the projects is reversed. Project Y

f. Capital ra5oning could change the selec5on of the plan. Because Plan Y requires only $2,100,000 and Plan X requires

Spreadsheet Exercise

Group Exercise

Group exercises are available on www.myfinancelab.com.

Risk within long-term investment decisions is the topic of this chapter. The investment projects of the previous two

Integrative Case 5: Lasting Impressions Company

Integrative Case 5 involves a complete long-term investment decision. The Lasting Impressions Company is a

commercial printer faced with a replacement decision in which two mutually exclusive projects have been

proposed. The data for each press have been designed to result in conflicting rankings when considering the NPV and

IRR decision techniques. The case tests the students’ understanding of the techniques as well as the qualitative

aspects of risk and return decision making.

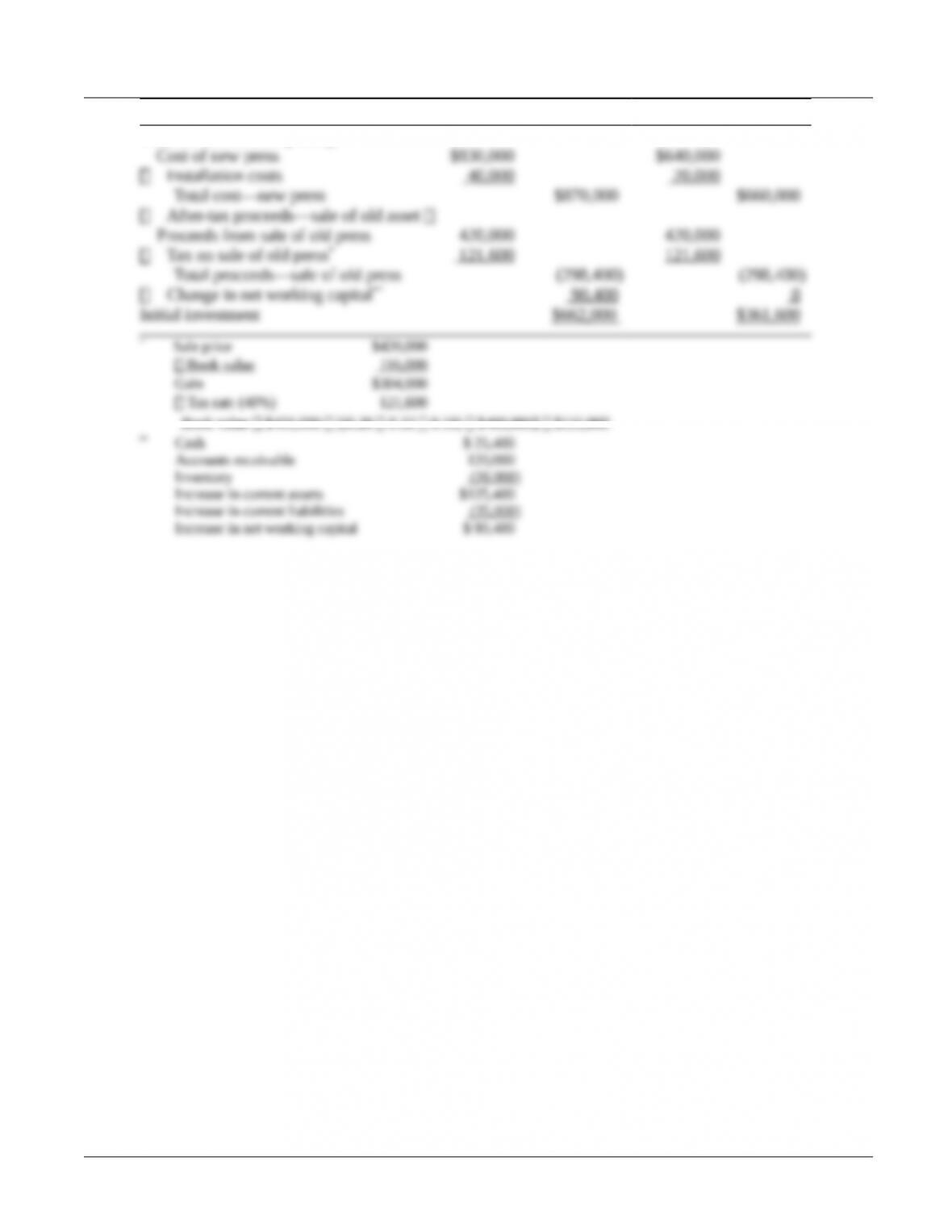

a. 1. Calcula5on of ini5al investment for Las5ng Impressions Company:

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 260

Press A Press B

Installed cost of new press

Book value $400,000 [(0.20 0.32 0.19) $400,000] $116,000

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 261

2. Depreciation

Year

Cost

Rate

Depreciation

Press A

1

$870,000

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 262

Press B

1

Existing Press

1

$400,000

0.12 (Yr. 4)

5

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 263

Operating cash inflows

Year

Earnings before

Depreciation

and Taxes

Depre-ciation

Earnings

before Taxes

Earnings

after

Taxes

Cash

Flow

Old

Cash

Flow

Incre-

mental

Cash

Flow

Existing Press

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 264

1

$120,000

$48,000

$72,000

$43,200

$91,200

2

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 265

Press A

1

$250,000

$174,000

$76,000

$45,600

$219,600

$91,200

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 266

Press B

1

$210,000

$132,000

$78,000

$46,800

$178,800

$91,200

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 267

2

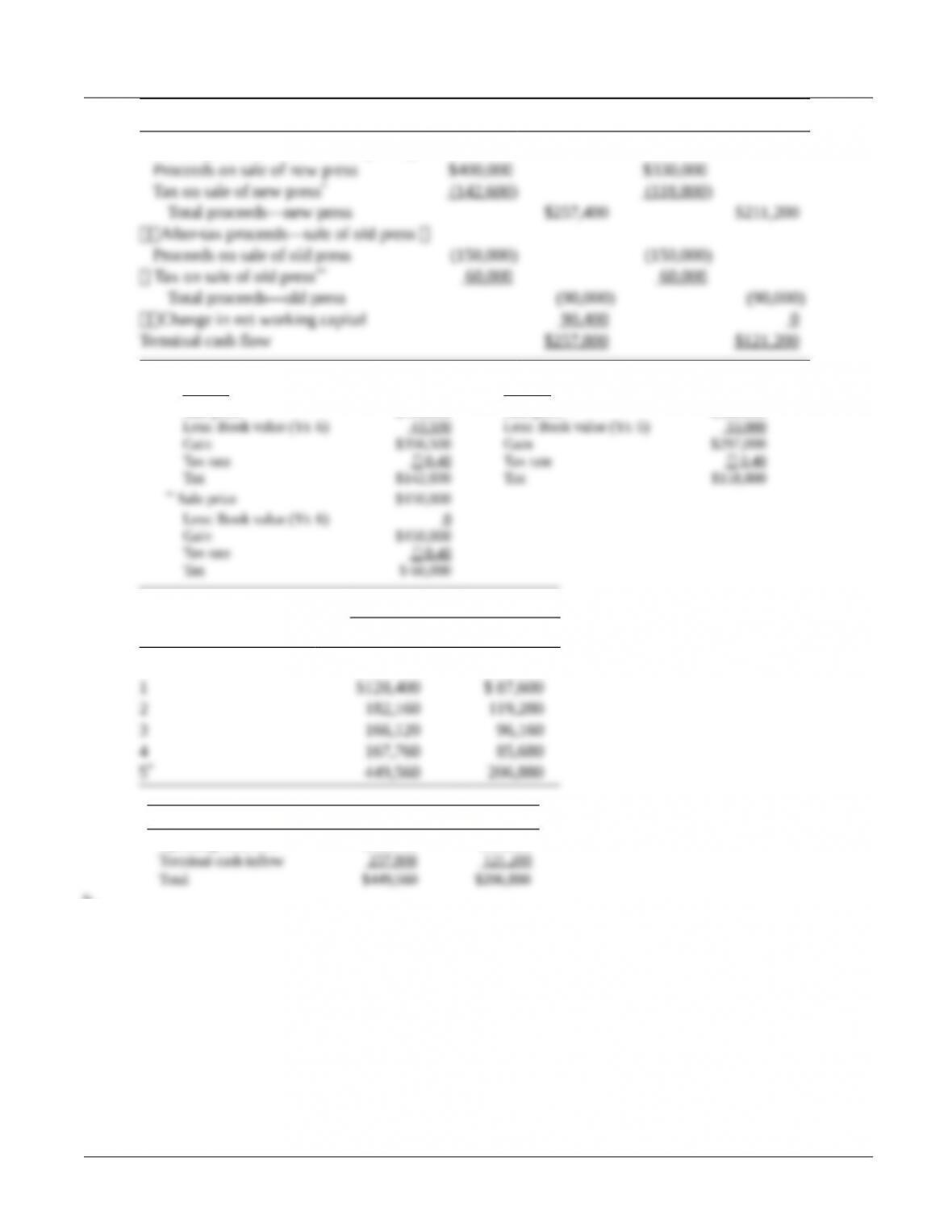

3. Terminal cash flow

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 268

Press A Press B

After–tax proceeds—sale of new press

* Press A Press B

Sale price $400,000 Sale price $330,000

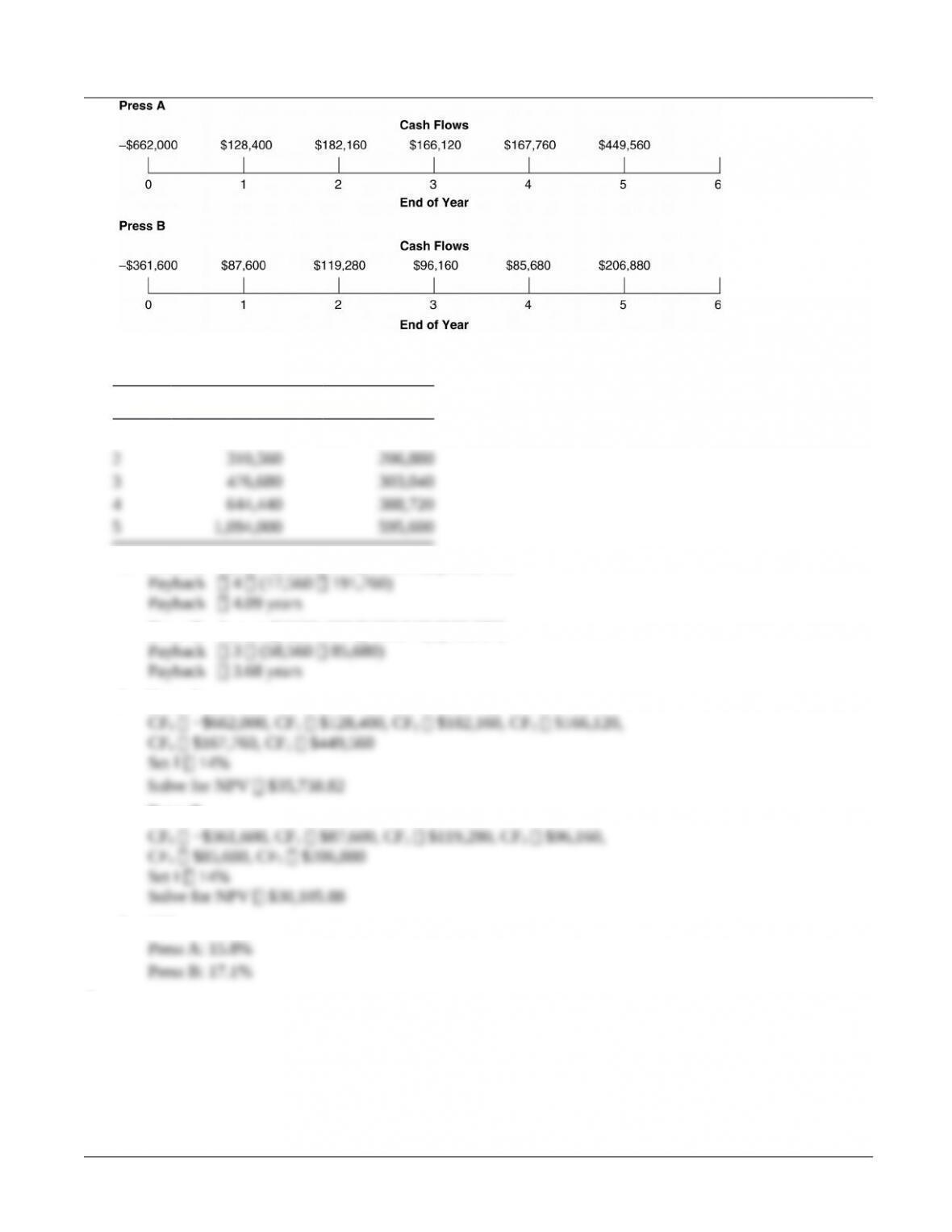

Cash Flows

Year Press A Press B

Initial investment ($662,000) ($361,600)

* Year 5 Press A Press B

Operating cash flow $191,760 $ 85,680

b.

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 269

c. Relevant cash )ow

Cumulative Cash Flows

Year Press A Press B

1 $128,400 $87,600

1. Press A: 4 years [(662,000 644,440) 191,760]

Press B: 3 years [(361,600 303,040) 85,680]

2. Press A

Press B

3. IRR:

d.

© 2015 Pearson Education, Inc.

Chapter 12 Risk and Refinements in Capital Budgeting 270

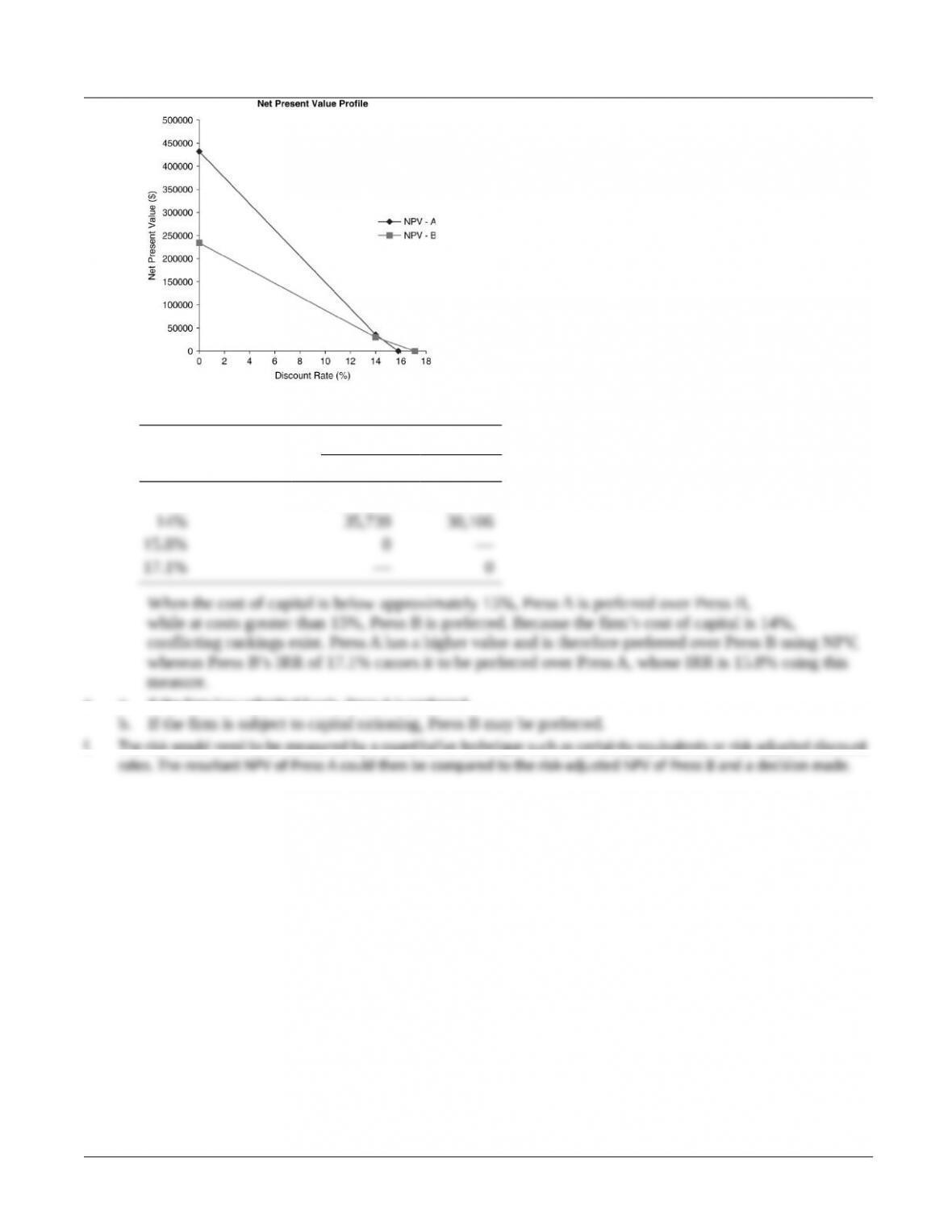

Data for NPV Profile

Discount Rate

NPV

Press A Press B

0% $432,000 $234,000

e. a. If the rm has unlimited funds, Press A is preferred.

f. The risk would need to be measured by a quan5ta5ve technique such as certainty equivalents or risk-adjusted discount

© 2015 Pearson Education, Inc.