P11-27. Integrative—determining relevant cash flows

LG 3, 4, 5, 6; Challenge

a.

Initial Investment A B

Installed cost of new asset

*Book value of old asset: [1 (0.20 0.32 0.19)] ($32,000) $9,280

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 226

b.

Calculation of Operating Cash Flows

Year

Profits before

Depreciation

and Taxes

Depre-ciatio

n

Net Profits

before

Taxes Taxes

Net Profits

after

Taxes

Operating

Cash

Inflows

Hoist A

1 $21,000 $9,600 $11,400 $4,560 $6,840 $16,440

Hoist B

1 $22,000 $12,000 $10,000 $4,000 $6,000 18,000

Existing Hoist

1 $14,000 $3,840 $10,160 $4,064 $6,096 $9,936

Calculation of Incremental Cash Flows

Incremental Cash Flow

Year Hoist A Hoist B Existing Hoist Hoist A Hoist B

1 $16,440 $18,000 $9,936 $6,504 $8,064

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 227

c. Terminal cash flow:

(A) (B)

After-tax proceeds form sale of new asset

1Book value of Hoist A at end of year 5 $2,400

Year 5 relevant cash flow—Hoist A:

Year 5 relevant cash flow—Hoist B:

d.

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 228

P11-28. Integrative—complete investment decision

LG 1, 2, 3, 4, 5, 6; Challenge

a. Initial investment:

Installed cost of new press

After-tax proceeds from sale of old asset

Taxes on sale of existing press* 480,000

*Book value $0

b.

Calculation of Operating Cash Flows

Year Revenues Expenses Depreciation

Net Profits

before Taxes Taxes

Net Profits

after Taxes

Cash

Flow

1 $1,600,000 $800,000 $440,000 $360,000 $144,000 $216,000 $656,000

d. PV of cash inflows:

Year CF PVIF11%,nPV

1 $656,000 0.901 $ 591,056

1 2 3 4 5 6

$656,000 $761,600 $647,200 $585,600 $585,600 $44,000

$0 $1,480,000

(1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR)

= + + + + + –

+ + + + + +

IRR 35%

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 229

e. The NPV is a positive $959,289, and the IRR of 35% is well above the cost of capital of 11%. Based

P11-29. Integrative—investment decision

LG 1, 2, 3, 4, 5, 6; Challenge

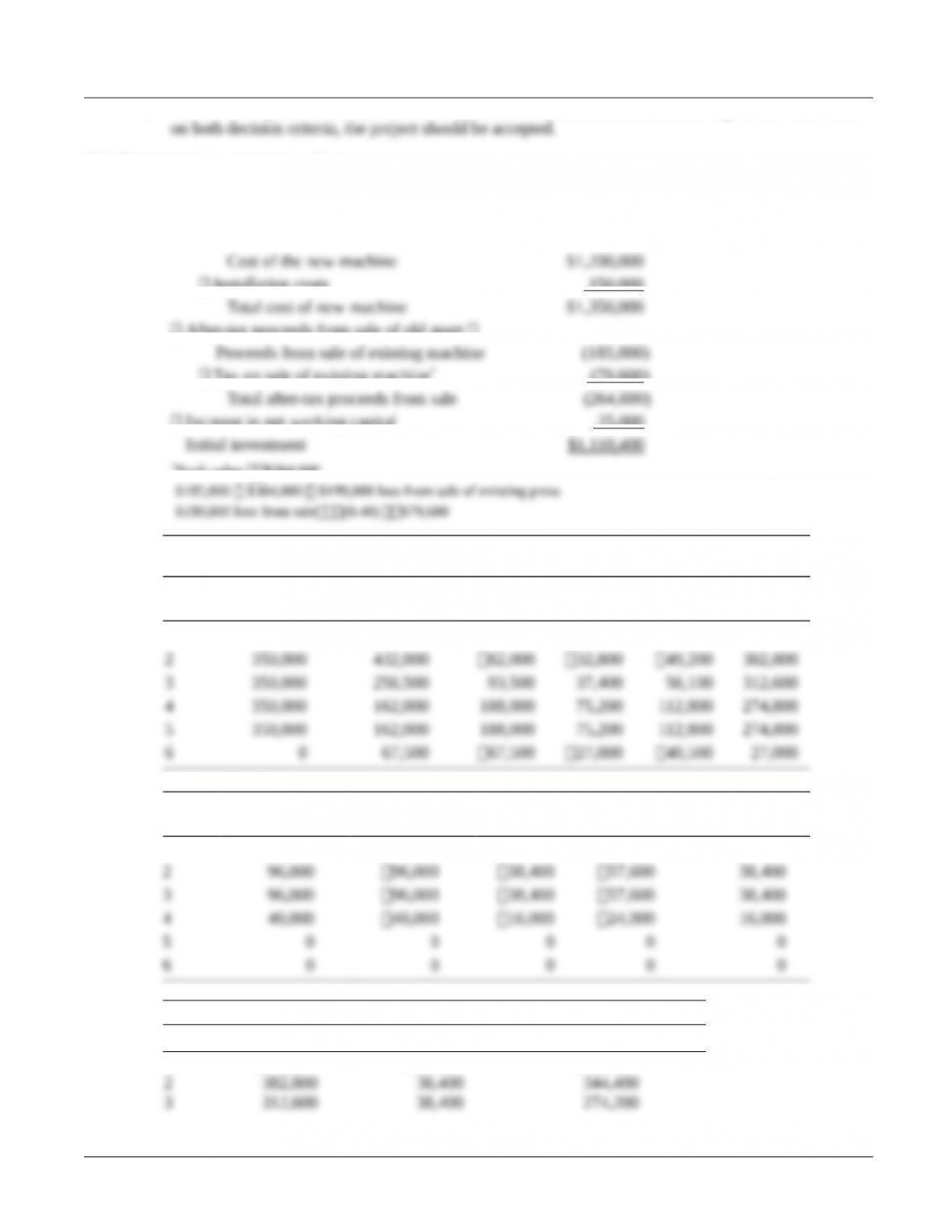

a. Initial investment:

Installed cost of new asset

Installation costs 150,000

After-tax proceeds from sale of old asset

Tax on sale of existing machine* (79,600)

Increase in net working capital 25,000

*Book value $384,000

Calculation of Operating Cash Flows

New Machine

Year

Reduction in

Operating Costs Depreciation

Net Profits

before Taxes Taxes

Net Profits

after Taxes

Cash

Flow

1 $350,000 $270,000 $80,000 $32,000 $48,000 $318,000

Existing Machine

Year Depreciation

Net Profits

before Taxes Taxes

Net Profits

after Taxes

Cash

Flow

1 $152,000 $152,000 $60,800 $91,200 $60,800

Incremental Operating Cash Flows

Year New Machine Existing Machine Incremental Cash Flow

1 $318,000 $60,800 $257,200

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 230

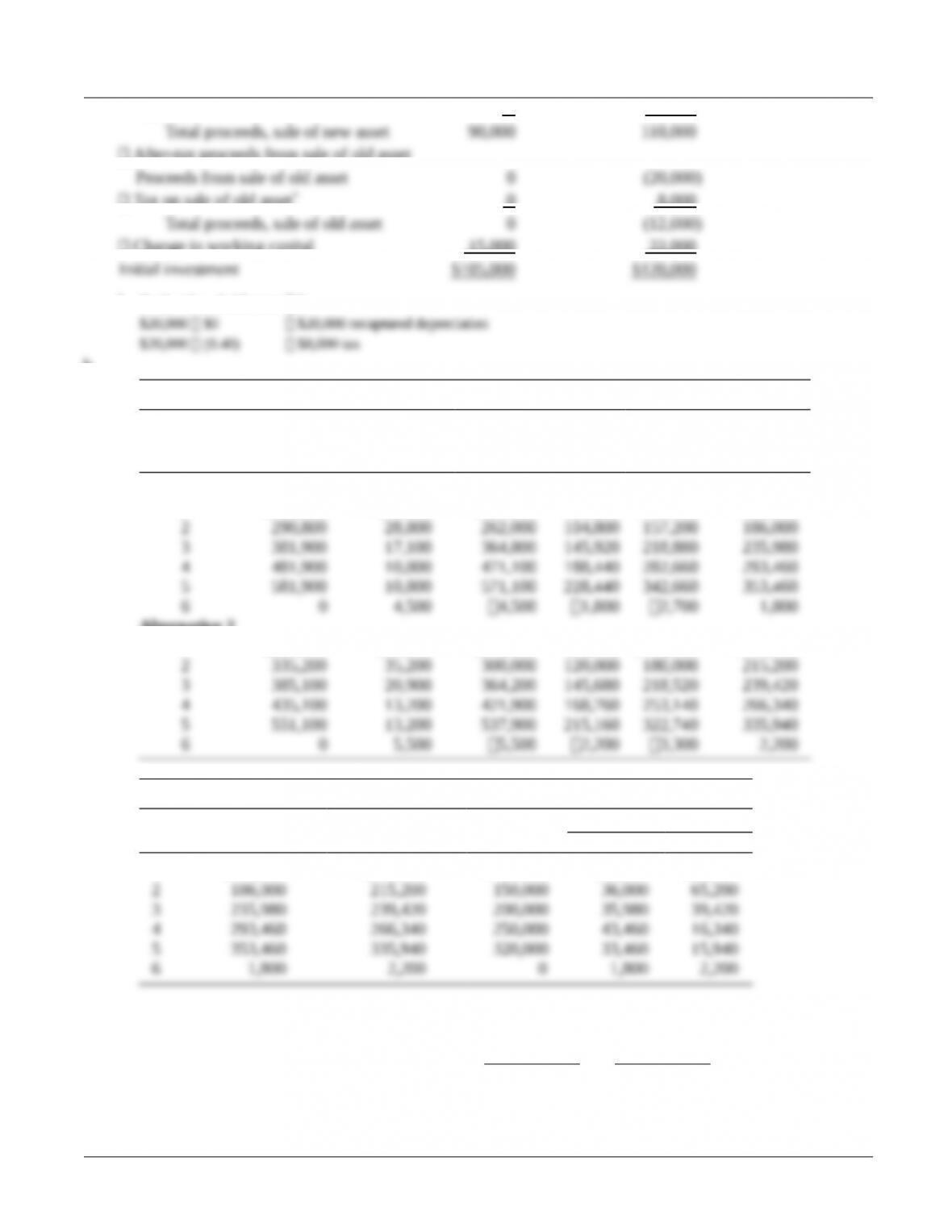

Terminal cash flow:

After-tax proceeds from sale of new asset

Tax on sale of new asset* (53,000)

After-tax proceeds from sale of old asset 0

Change in net working capital 25,000

*Book value of new machine at the end of year 5 is $67,500

b. CF0 $1,110,400, CF1 257,200, CF2 $344,400, CF3 $274,200,

c.

1 2 3 4 5

$257,200 $344,400 $274,200 $258,800 $446,800

$0 $1,110,400

(1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR)

= + + + + –

+ + + + +

IRR 12.2%

Calculator solution: 12.24%

d. Because the NPV 0 and the IRR cost of capital, the new machine should be purchased.

e. 12.24%. The criterion is that the IRR must equal or exceed the cost of capital; therefore, 12.24% is the

P11-30. Ethics problem

LG 2; Intermediate

The person who came up with the idea for a new investment may have a selfish interest in seeing the

Case

Case studies are available on www.myfinancelab.com.

Developing Relevant Cash Flows for Clark Upholstery Company’s Machine Renewal

or Replacement Decision

Clark Upholstery is faced with a decision to either renew its major piece of machinery or to replace the machine.

The case tests the students’ understanding of the concepts of initial investment and relevant cash flows.

a. Initial Investment:

Alternative 1 Alternative 2

Installed cost of new asset

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 231

Installation costs 0 10,000

After-tax proceeds from sale of old asset

Tax on sale of old asset* 0 8,000

Change in working capital 15,000 22,000

*Book value of old asset 0

b.

Calculation of Operating Cash Inflows

Year

Profits before

Depreciation

and Taxes Depre-ciation

Net Profits

before Taxes Taxes

Net Profits

after Taxes

Operating

Cash

Inflows

Alternative 1

1 $198,500 $18,000 $180,500 $72,200 $108,300 $126,300

Alternative 2

1 $235,500 $22,000 $213,500 $85,400 $128,100 $150,100

Calculation of Incremental Cash Inflows

Incremental Cash Flow

Year Alternative 1 Alternative 2 Existing Alt. 1 Alt. 2

1 $126,300 $150,100 $100,000 $26,300 $50,100

3 235,980 239,420 200,000 35,980 39,420

4 293,460 266,340 250,000 43,460 16,340

After-tax proceeds from sale of old asset

Tax on sale of old asset** 800 800

Change in working capital 15,000 22,000

*Book value of Alternative 1 at end of year 5: $4,500

Book value of Alternative 2 at end of year 5: $5,500

** Book value of old asset at end of year 5: $0

Alternative 1

Year 5 relevant cash flow: Operating cash flow: $33,460

Alternative 2

Year 5 relevant cash flow: Operating cash flow: $15,940

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 233

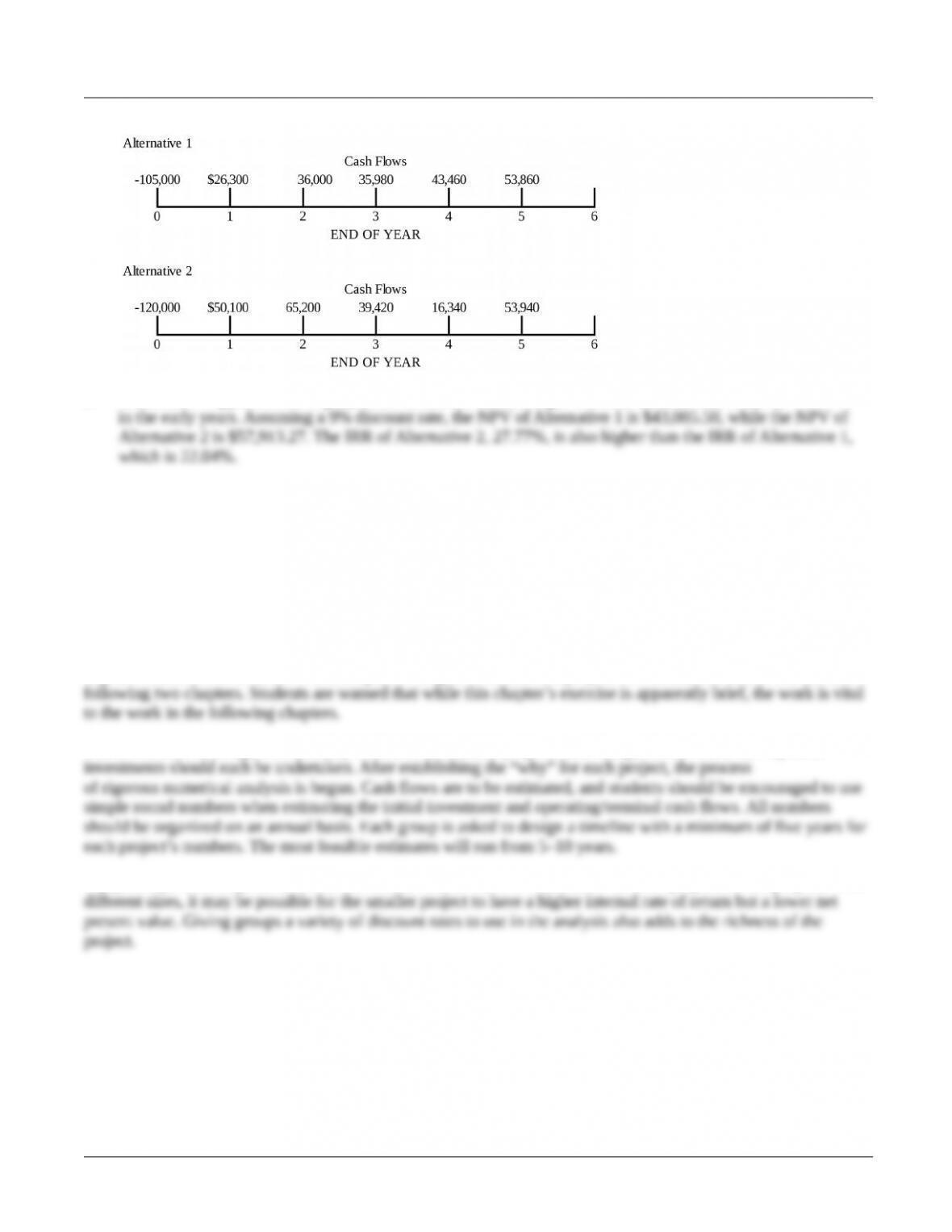

d. Alternative 1

e. Alternative 2 appears to be slightly better because it has the larger incremental cash flow amounts

Spreadsheet Exercise

The answer to Chapter 11’s Damon Corporation spreadsheet problem is located on the Instructor’s Resource

Center at www.pearsonhighered.com/irc under the Instructor’s Manual.

Group Exercise

Group exercises are available on www.myfinancelab.com.

Capital investment is revisited in this chapter. A long-term investment project will be detailed across this and the

The first task is to design two mutually exclusive investment projects. The design should focus on why these

A payback period, net present value, and internal rate of return are estimated for both projects. If the projects have

© 2015 Pearson Education, Inc.