Chapter 11

Capital Budgeting Cash Flows

Instructor’s Resources

Overview

This chapter expands upon the capital budgeting techniques presented in the last chapter (Chapter 10). Shareholder

wealth maximization relies upon selection of projects that have positive net present values. The most important

and difficult aspect of the capital budgeting process is developing good estimates of the relevant cash flows.

Chapter 11 focuses on the basics of determining relevant after-tax cash flows of a project, from the initial cash

outlay to annual cash stream of costs and benefits and terminal cash flow. It also describes the special concerns

facing capital budgeting for the multinational company. The text highlights how capital budgeting will be a critical

aspect of the professional life and personal life of students upon graduation.

Suggested Answer to Opener-in-Review Question

Assuming that the average comic book store has a life of about 10 years, what is the NPV of opening a new

store if the required rate of return in this business is 10%? You may assume that the $250,000 in initial

inventory will be recovered at the end of the 10th year (in addition to the annual operating cash flow for that

year). What is the IRR that one can earn by opening up a new store?

Assume that by offering merchandise discounts to customers who are opening new stores, Diamond can

reduce the required initial inventory investment from $250,000 to $150,000. Maintaining all other

assumptions as previously stated, how will this affect the NPV and IRR earned on a new comic book store?

Answers to Review Questions

1. Capital budgeting projects should be evaluated using incremental after-tax cash flows because after-tax cash

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 226

2. The three components of cash flow for any project are (1) initial investment, (2) operating cash flows, and (3)

3. Sunk costs are costs that have already been incurred and thus the money has already been spent. Opportunity

4. To minimize long-term currency risk, companies can finance a foreign investment in local capital markets so

5. a. The cost of the new asset is the purchase price. (Outflow)

b. Installation costs are any added costs necessary to get an asset into operation. (Outflow)

6. The book value of an asset is its strict accounting value.

Book value installed cost of asset – accumulated depreciation

7. The asset may be sold (1) for more than its book value, (2) for the amount of its book value, or

8. The depreciable value of an asset is the installed cost of a new asset and is based on the depreciable cost of

9. Depreciation is used to decrease the firm’s total tax liability and then is added back to net profits after taxes to

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 227

10. To calculate incremental operating cash inflow for both the existing situation and the proposed project, the

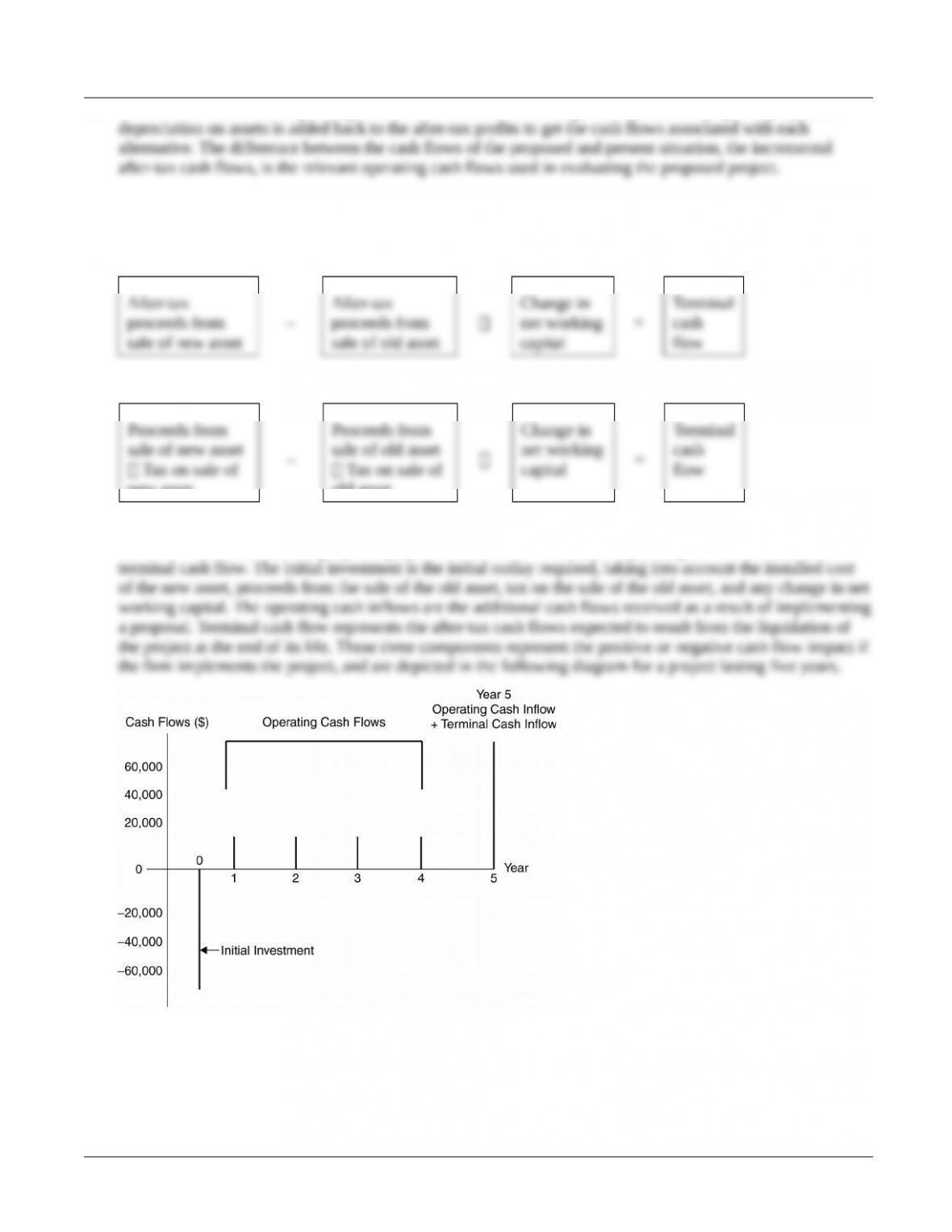

11.The terminal cash flow is the cash flow resulting from termination and liquidation of a project at the end of its

economic life. The form of calculating terminal cash flows is shown below:

Terminal Cash Flow Calculation:

Extended Presentation:

new asset

old asset

12. The relevant cash flows necessary for a conventional capital budgeting project are the incremental after-tax

cash flows attributable to the proposed project: the initial investment, the operating cash inflows, and the

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 228

Suggested Answer to Focus on Ethics Box:

A Question of Accuracy

What would your options be when faced with the demands of an assertive chief executive officer (CEO) who

expects you to “make it work”? Brainstorm several options.

There is a chance that you may be working for an “assertive CEO” at some point in your career. This may be by

choice or by chance. While the “make it work” mandate may seem like an order to do anything it takes to

Suggested Answer to Global Focus Box:

Changes May Influence Future Investments in China

Although China has been actively campaigning for foreign investment, how do you think having

a communist government affects its foreign investment?

Having a communist government has a negative effect on foreign direct investment (FDI). As in all investments

Answers to Warm-Up Exercises

E11-1. Categorizing a firm’s expenditures

Answer: In this case, the tuition reimbursement should be categorized as a capital expenditure because the

E11-2. Classification of project costs and cash flows

Answer: $3.5 billion already spent—sunk cost (irrelevant)

E11-3. Finding the initial investment

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 229

Answer: $20,000 Purchase price of new machinery

E11-4. Book value and recaptured depreciation

Answer: Book value $175,000 $124, 250 $50,750

E11-5. Initial investment

Answer: Initial investment purchase price installation costs – after-tax proceeds from sale of old

Solutions to Problems

Note: The MACRS depreciation percentages used in the following problems appear in Chapter 4, Table 4.2. The

P11-1. Classification of expenditures

LG 2; Basic

a. Operating expenditure—lease expires within one year.

b. Capital expenditure—patent rights exist for many years.

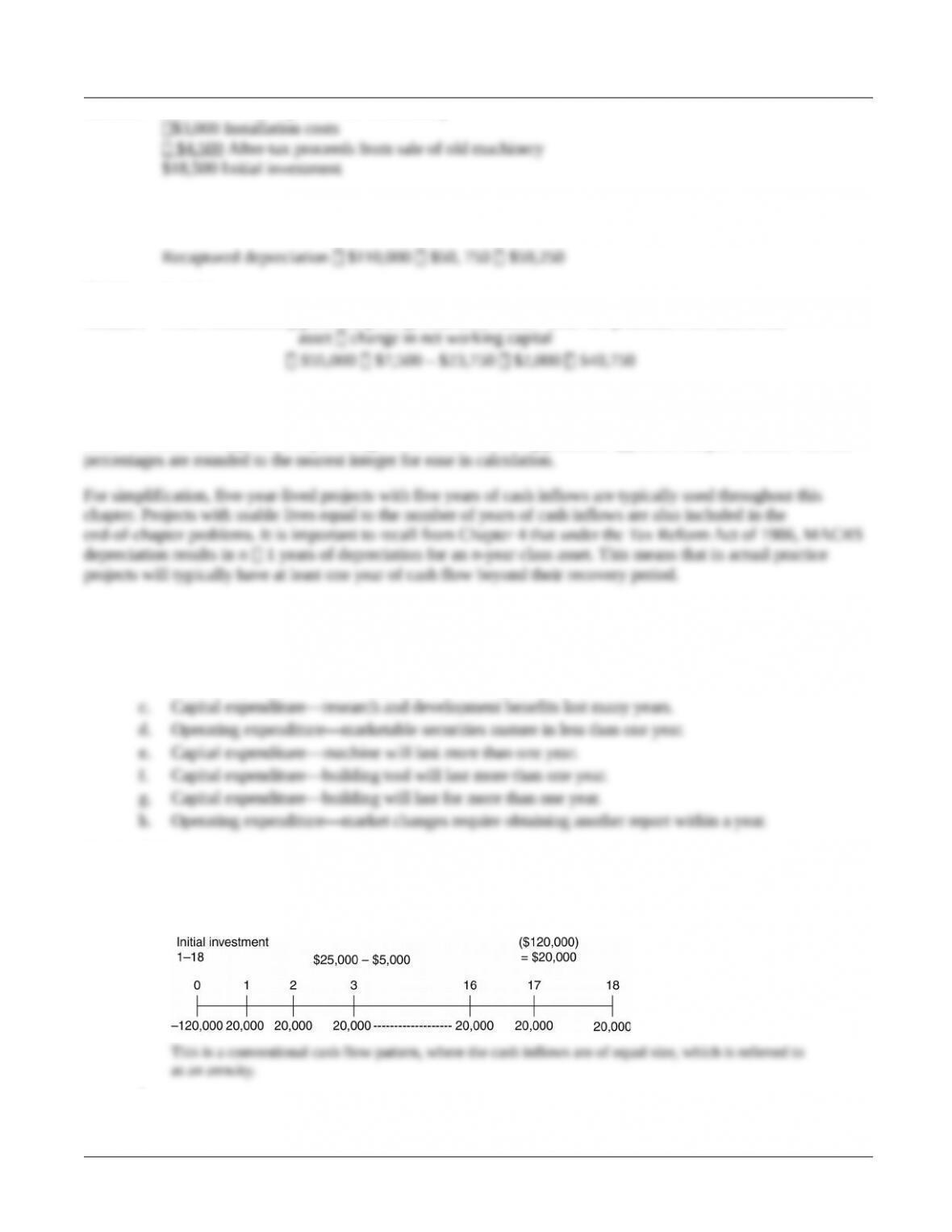

P11-2. Relevant cash flow and timeline depiction

LG 1, 2; Intermediate

a.

Year Cash Flow

b.

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 230

c.

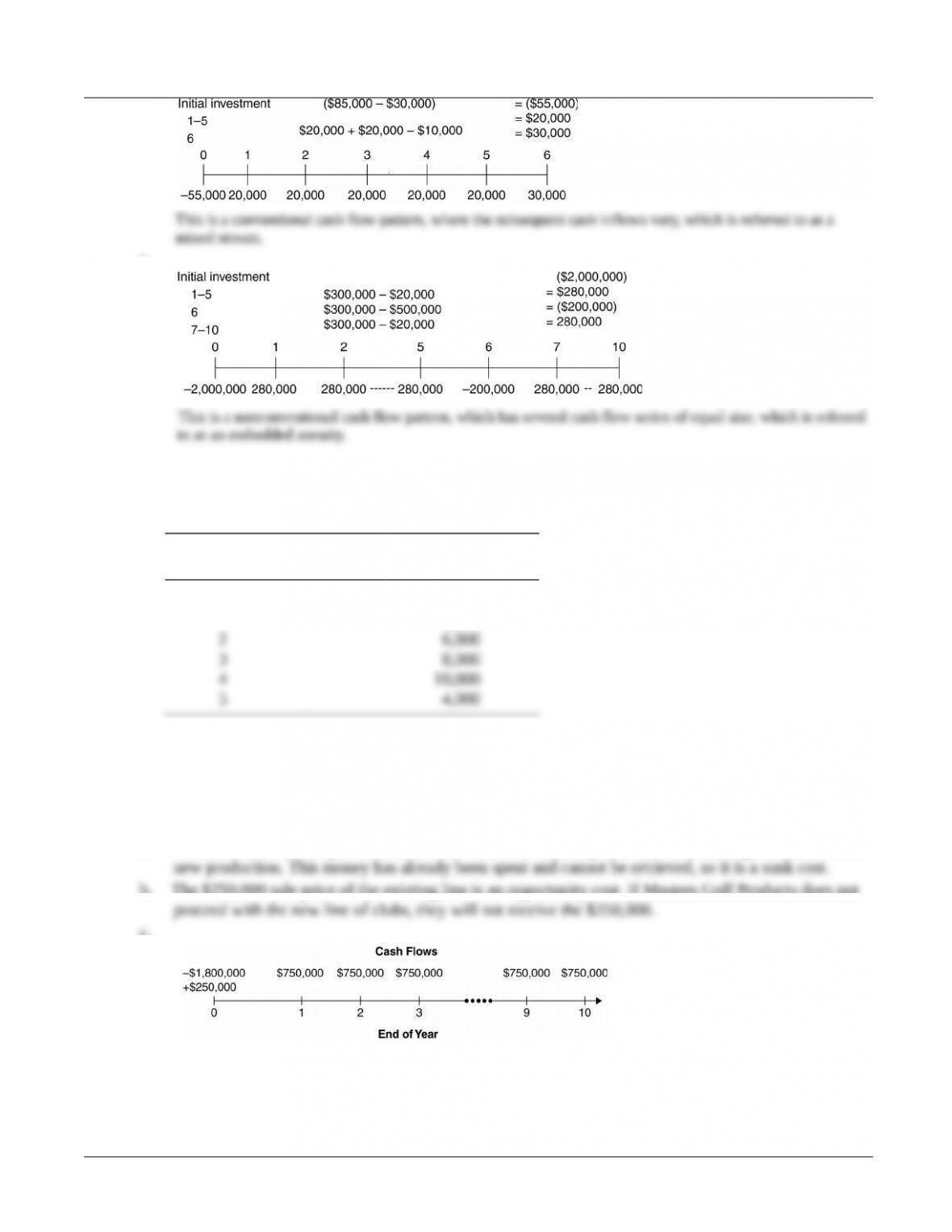

P11-3. Expansion versus replacement cash flows

LG 3; Intermediate

a.

Year Relevant Cash

Flows

Initial investment ($28,000)

1 4,000

b. An expansion project is simply a replacement decision in which all cash flows from the old asset are

zero.

P11-4. Sunk costs and opportunity costs

LG 2; Basic

a. The $1,000,000 development costs should not be considered part of the decision to go ahead with the

b. The $250,000 sale price of the existing line is an opportunity cost. If Masters Golf Products does not

c.

P11-5. Sunk costs and opportunity costs

LG 2; Intermediate

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 231

a. Sunk cost—The funds for the tooling had already been expended and would not change, no matter

b. Opportunity cost—The development of the computer programs can be done without additional

c. Opportunity cost—Covol will not have to spend any funds for floor space, but the lost cash inflow

d. Sunk cost—The money for the storage facility has already been spent, and no matter what decision

e. Opportunity cost—Forgoing the sale of the crane costs the firm $180,000 of potential cash inflows.

P11-6. Personal finance: Sunk and opportunity cash flows

LG 2; Intermediate

a. The sunk costs or cash outlays are expenditures that have been made in the past and have no effect

b. Sunk costs (cash flows):

Replace water heater

P11-7. Book value

LG 3; Basic

Asset

Installed

Cost

Accumulated

Depreciation

Book

Value

A $ 950,000 $ 674,500 $275,500

P11-8. Book value and taxes on sale of assets

LG 3, 4; Intermediate

a. Book value $80,000 (0.71 $80,000)

$23,200

b.

Sale Price

Capital

Gain

Tax on

Capital Gain

Depreciation

Recovery

Tax on

Recovery

Total

Tax

$100,000 $20,000 $8,000 $56,800 $22,720 $30,720

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 232

P11-9. Tax calculations

LG 3, 4; Intermediate

Current book value $200,000 [(0.52 ($200,000)] $96,000

(a) (b) (c) (d)

Capital gain $ 20,000 $ 0 $0 $ 0

P11-10. Change in net working capital calculation

LG 3; Basic

a.

Current Assets Current Liabilities

Cash $15,000 Accounts payable $90,000

b. Analysis of the purchase of a new machine reveals an increase in net working capital. This increase

c. Yes, in computing the terminal cash flow, the net working capital increase should be reversed.

P11-11. Calculating initial investment

LG 3, 4; Intermediate

a. Book value $325,000 (1 0.20 – 0.32) $325,000 0.48 $156,000

b. Sales price of old equipment $200,000

c. Cost of new machine $ 500,000

P11-12. Initial investment—basic calculation

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 233

LG 3, 4; Intermediate

Installed cost of new asset

P11-13. Initial investment at various sale prices

LG 3, 4; Intermediate

(a) (b) (c) (d)

Installed cost of new asset:

Cost of new asset $24,000 $24,000 $24,000 $24,000

Book value of existing machine $10,000 [1 (0.20 0.32 0.19)] $2,900

*Tax Calculations:

a. Recaptured depreciation $10,000 $2,900 $7,100

b. Recaptured depreciation $7,000 $2,900 $4,100

c. 0 tax liability

d. Loss on sale of existing asset $1,500 $2,900 ($1,400)

P11-14. Calculating initial investment

LG 3, 4; Challenge

© 2015 Pearson Education, Inc.

Chapter 11 Capital Budgeting Cash Flows 234

a. Book value ($60,000 0.31) $18,600

b. Sales price of old equipment $35,000

c. Changes in current asset accounts

d. Cost of new roaster $130,000

© 2015 Pearson Education, Inc.