P10-10. NPV—mutually exclusive projects

LG 3; Intermediate

a. and b.

Press A

c. Ranking—using NPV as criterion

Rank Press NPV

1 C $15,043.89

d. Profitability Indexes

Profitability Index S Present Value Cash Inflows ¸ Investment

e. The profitability index measure indicates that Press C is the best, then Press B, then Press A

(which is unacceptable). This is the same ranking as was generated by the NPV rule.

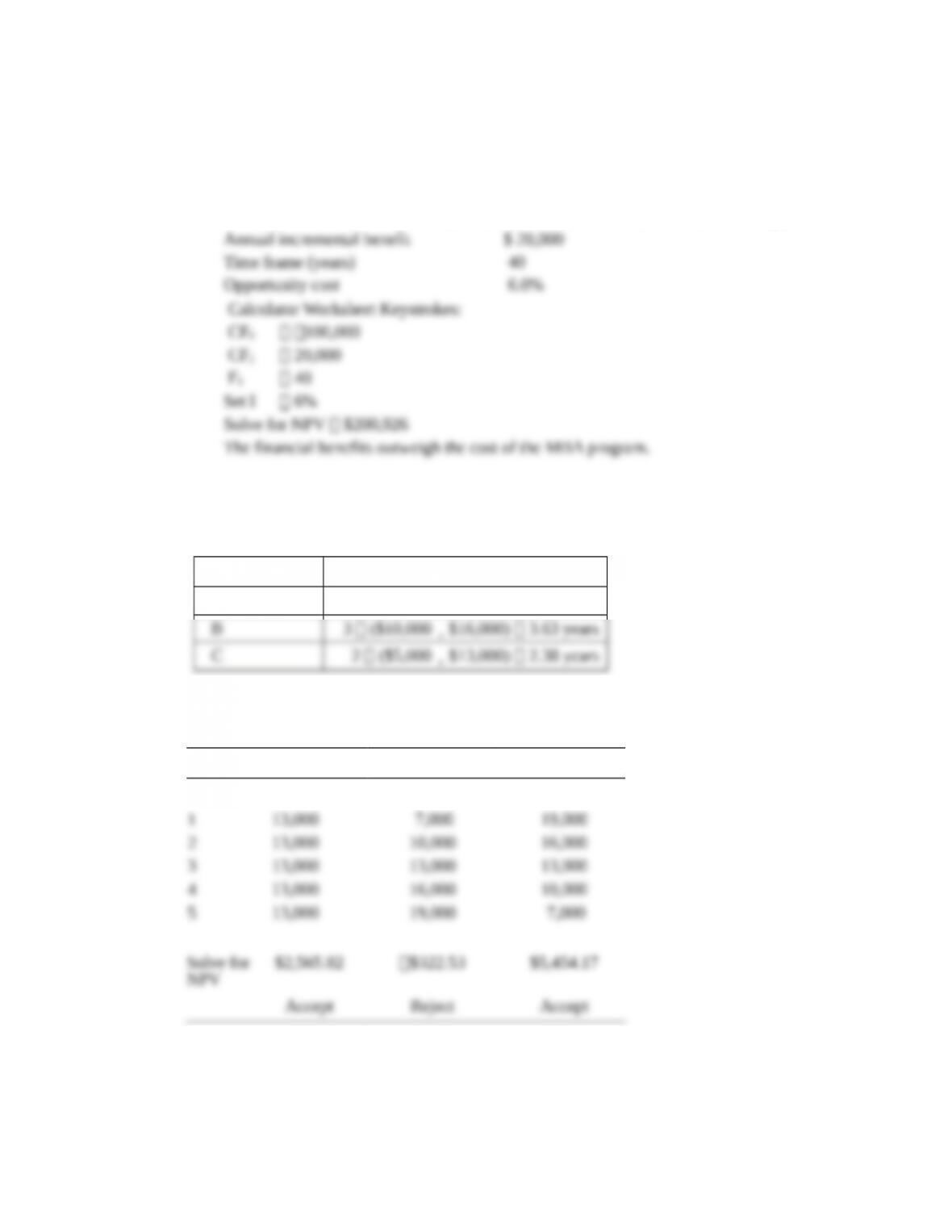

P10-11. Personal finance: Long-term investment decisions, NPV method

LG 3

Key information:

Cost of MBA program $100,000

($50,000 for tuition and $50,000 for lost earnings)

P10-12. Payback and NPV

LG 2, 3; Intermediate

a.

Project Payback Period

A $40,000 ¸ $13,000 3.08 years

Project C, with the shortest payback period, is preferred.

b. Worksheet keystrokes

Year Project A Project B Project C

0$40,000 $40,000 $40,000

Project C is preferred using the NPV as a decision criterion.

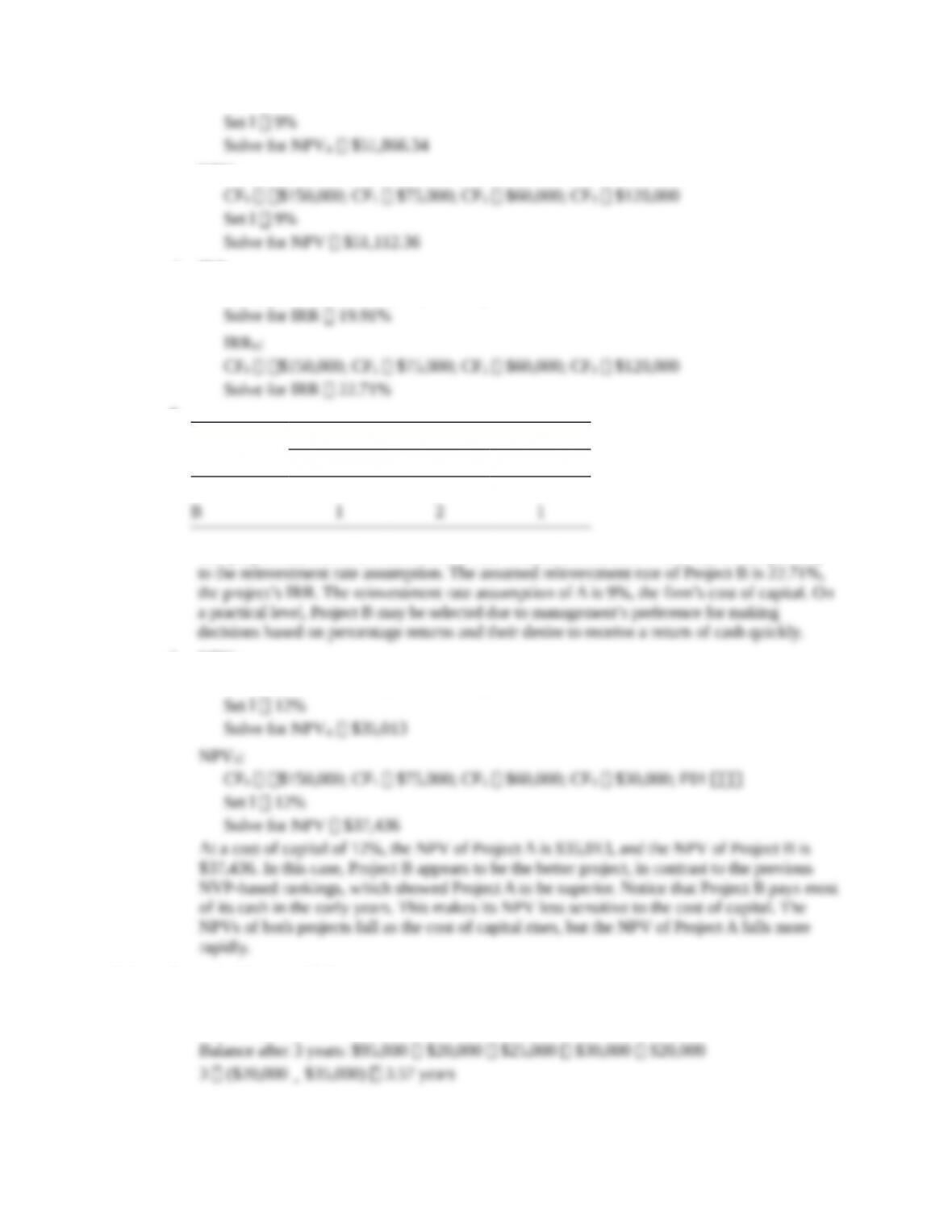

c. At a cost of 16%, Project C has the highest NPV. Because of Project C’s cash flow

P10-13. NPV and EVA

LG 3; Intermediate

a. NPV $2,500,000 $240,000 ¸ 0.09 $166,667

P10-14. IRR—Mutually exclusive projects

LG 4; Intermediate

IRR is found by solving:

1

$0 initial investment

(1 IRR)

nt

t

t

CF

=

é ù

= –

ê ú

+

ë û

å

Project A

Project B

CF0 $490,000; CF1 $150,000; CF2 $150,000; CF3 $150,000; CF4 $150,000

Project C

CF0 $20,000; CF1 $7500; CF2 $7500; CF3 $7500; CF4 $7500; CF5 $7500

Project D

P10-15. IRR

LG 4; Intermediate

The IRR of the project is 4%. Because the IRR is lower than the firm’s cost of capital, the firm

P10-16. IRR—Mutually exclusive projects

LG 4; Intermediate

a. and b.

Project X

1 2 3 4 5

$100,000 $120,000 $150,000 $190,000 $250,000

$0 $500,000

(1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR)

= + + + + –

+ + + + +

CF0 −$500,000; CF1 $100,000; CF2 $120,000; CF3 $150,000; CF4 $190,000

CF5 $250,000

Solve for IRR 15.67; because IRR cost of capital, accept the project.

Project Y

1 2 3 4 5

$140,000 $120,000 $95,000 $70,000 $50,000

$0 $325,000

(1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR)

= + + + + –

+ + + + +

CF0 $325,000; CF1 $140,000; CF2 $120,000; CF3 $95,000; CF4 $70,000

CF5 $50,000

Solve for IRR 17.29%; because IRR cost of capital, accept the project.

c. Project Y, with the higher IRR, is preferred, although both are acceptable.

P10-17. Personal Finance: Long-term investment decisions, IRR method

LG 4; Intermediate

IRR is the rate of return at which NPV equals zero

P10-18. IRR, investment life, and cash inflows

LG 4; Challenge

a. N 10, PV −$61,450, PMT $10,000

b. I 15%, PV $61,450, PMT $10,000

c. N 10, I 15%, PV $61,450

P10-19. NPV and IRR

LG 3, 4; Intermediate

a. N 7, I 10%, PMT $4,000

b. N 7, PV $18,250, PMT $4,000

c. The project should be accepted because the NPV 0 and the IRR the cost of capital.

P10-20. NPV, with rankings

LG 3, 4; Intermediate

a. NPVA $45,665.50 (N 3, I 15, PMT $20,000) $50,000

b.

Rank Press NPV

1 C $7,088.02

c. Using the calculator, the IRRs of the projects are:

Project IRR

A 9.70%

P10-21. All techniques, conflicting rankings

LG 2, 3, 4: Intermediate

a.

Project A Project B

Year

Cash

Inflows

Investment

Balance Year

Cash

Inflows

Investment

Balance

0$150,000 0 $150,000

NPVB:

d. IRRA:

CF0 $150,000; CF1 $45,000; F1 6

e.

Rank

Project Payback NPV IRR

A 2 1 2

The project that should be selected is A. The conflict between NPV and IRR is due partially

f. NPVA:

CF0 $150,000; CF1 $45,000; F1 6

P10-22. Payback, NPV, and IRR

LG 2, 3, 4; Intermediate

a. Payback period

b. NPV computation

c.

1 2 3 4 5

$20,000 $25,000 $30,000 $35,000 $40,000

$0 $95,000

(1 IRR) (1 IRR) (1 IRR) (1 IRR) (1 IRR)

= + + + + –

+ + + + +

CF0 $95,000; CF1 $20,000; CF2 $25,000; CF3 $30,000; CF4 $35,000

CF5 $40,000

Solve for IRR 15.36%

d. NPV $9,080; because NPV 0, accept

P10-23. NPV, IRR, and NPV profiles

LG 3, 4, 5; Challenge

a. and b.

Project A