13.11 The ABC Company performs its expenditure cycle activities using its integrated

ERP system as follows:

• Employees in any department can enter purchase requests for items they note as

being either out of stock or in small quantity.

• The company maintains a perpetual inventory system.

• Each day, employees in the purchasing department process all purchase requests

from the prior day. To the extent possible, requests for items available from the

same supplier are combined into one larger purchase order in order to obtain

volume discounts. Purchasing agents use the Internet to compare prices in order

to select suppliers. If an Internet search discovers a potential new supplier, the

purchasing agent enters the relevant information in the system, thereby adding

the supplier to the approved supplier list. Purchase orders above $10,000 must

be approved by the purchasing department manager. EDI is used to transmit

purchase orders to most suppliers, but paper purchase orders are printed and

mailed to suppliers who are not EDI capable.

• Receiving department employees have read-only access to outstanding purchase

orders. Usually, they check the system to verify existence of a purchase order

prior to accepting delivery, but sometimes during rush periods they unload

trucks and place the items in a corner of the warehouse where they sit until there

is time to use the system to retrieve the relevant purchase order. In such cases, if

no purchase order is found, the receiving employee contacts the supplier to

arrange for the goods to be returned.

• Receiving department employees compare the quantity delivered to the quantity

indicated on the purchase order. Whenever a discrepancy is greater than 5%,

the receiving employee sends an email to the purchasing department manager.

The receiving employee uses an online terminal to enter the quantity received

before moving the material to the inventory stores department.

• Inventory is stored in a locked room. During normal business hours an

inventory employee allows any employee wearing an identification badge to

enter the storeroom and remove needed items. The inventory storeroom

employee counts the quantity removed and enters that information in an online

terminal located in the storeroom.

• Occasionally, special items are ordered that are not regularly kept as part of

inventory, from a specialty supplier who will not be used for any regular

purchases. In these cases, an accounts payable clerk creates a one-time supplier

record.

• All supplier invoices (both regular and one-time) are routed to accounts payable

for review and approval. The system is configured to perform an automatic 3-

way match of the supplier invoice with the corresponding purchase order and

receiving report.

• Each Friday, approved supplier invoices that are due within the next week are

routed to the treasurer’s department for payment. The cashier and treasurer are

the only employees authorized to disburse funds, either by EFT or by printing a

check. Checks are printed on dedicated printer located in the treasurer’s

department, using special stock paper that is stored in a locked cabinet

accessible only to the treasurer and cashier. The paper checks are sent to

accounts payable to be mailed to suppliers.

• Monthly, the treasurer reconciles the bank statements and investigates any

discrepancies with recorded cash balances.

Required:

a. Identify weaknesses in ABC’s existing expenditure cycle procedures, explain the

resulting problems, and suggest as solution.

Weakness/Problem

Applicable Control

Purchase requests are not reviewed and

approved prior to submission. This can

result in ordering unnecessary items.

Purchase requisitions should be reviewed and

approved by the originating department’s

manager prior to being processed.

A formal inventory control system (EOQ,

MRP, or JIT) is not used. This is likely to

result in both shortages and excess

inventory.

A formal inventory control system should be

used to plan purchases to minimize the

combined costs of stock outs, excess

inventory, and ordering costs.

There is no mention of periodic physical

counts of inventory. Thus, the perpetual

inventory records are likely to become

inaccurate over time. It will also not be

possible to detect theft of inventory in a

timely manner.

Regular physical counts of inventory need to

be conducted.

Discrepancies with the perpetual inventory

records need to be promptly investigated.

Any purchasing agent can add new

suppliers to the approved supplier master

file without approval. As a result, the

approved supplier master file may

contain unreliable or non-existent

suppliers.

Restrict the number of employees who can

make changes to the approved supplier list.

Periodically print a report of all changes and

review them to ensure that they have all been

approved.

Selection of suppliers is based solely on

price. As a result, inferior quality

products could be purchased, resulting in

increased costs due to warranty repairs,

scrap, or rework.

Criteria for selecting suppliers should include

information on supplier reliability and

product quality.

The system should be configured to track

actual supplier performance against promised

delivery dates.

Receiving department employees have

access to the quantities ordered on

purchase orders. This may lead them to

not actually count every delivery,

especially during busy times, but instead

simply visually compare the quantity

delivered to the quantity ordered.

Reconfigure the system and do not permit

receiving department employees’ to access

quantity ordered information.

Receiving department employees

sometimes unload deliveries without

verifying the existence of an approved

purchase order. This wastes time in

unloading and then subsequently

contacting the supplier to return the

unordered items.

Schedule additional help during busy periods.

Create a policy requiring receiving

department employees to always verify the

existence of a valid purchase order before

accepting delivery.

Publish and enforce sanctions for violating

this policy.

Receiving department employees inform

purchasing of discrepancies between

quantities received and ordered greater

than 5%. They may fail to do this during

busy periods, resulting in failure to

timely resolve problems.

Configure the system to compare quantities

received to quantities ordered. The system

should send discrepancies exceeding a

tolerable deviation directly to the purchasing

manager.

The identity of employees removing

inventory from the storeroom is not

recorded. This makes it difficult to

investigate the cause of any discrepancies

between recorded and actual counts of

inventory.

The identity of employees removing

inventory should be recorded. This can be

done either by swiping an ID badge or by

entering a user ID in an online terminal.

Accounts payable clerks can create one-

time supplier records without review and

subsequently approve payments to those

suppliers. This creates the possibility of

fraudulent disbursements.

The system should be configured to print a

list of all one-time suppliers. Management

should review that list regularly.

Accounts payable should not be able to create

any new supplier records – that task should

only be done by the purchasing manager.

There is no indication that supporting

documents in the voucher package are

marked “cancelled” or “paid” after being

used to issue a check. This can result in

duplicate payments.

The system should be configured to mark

supporting documents in a voucher package

as PAID when used to generate a check or

EFT payment.

Checks are returned to accounts payable

to be mailed to suppliers. This provides

an opportunity to intercept and alter a

check.

Checks should be mailed by the cashier or the

cashier’s assistant.

The treasurer, who has the ability to write

checks and authorize EFT payments, also

reconciles the bank account. This

provides an opportunity to commit fraud

and cover up the discrepancy by altering

the reconciliation.

Someone other than the cashier or treasurer

should reconcile the bank account statement.

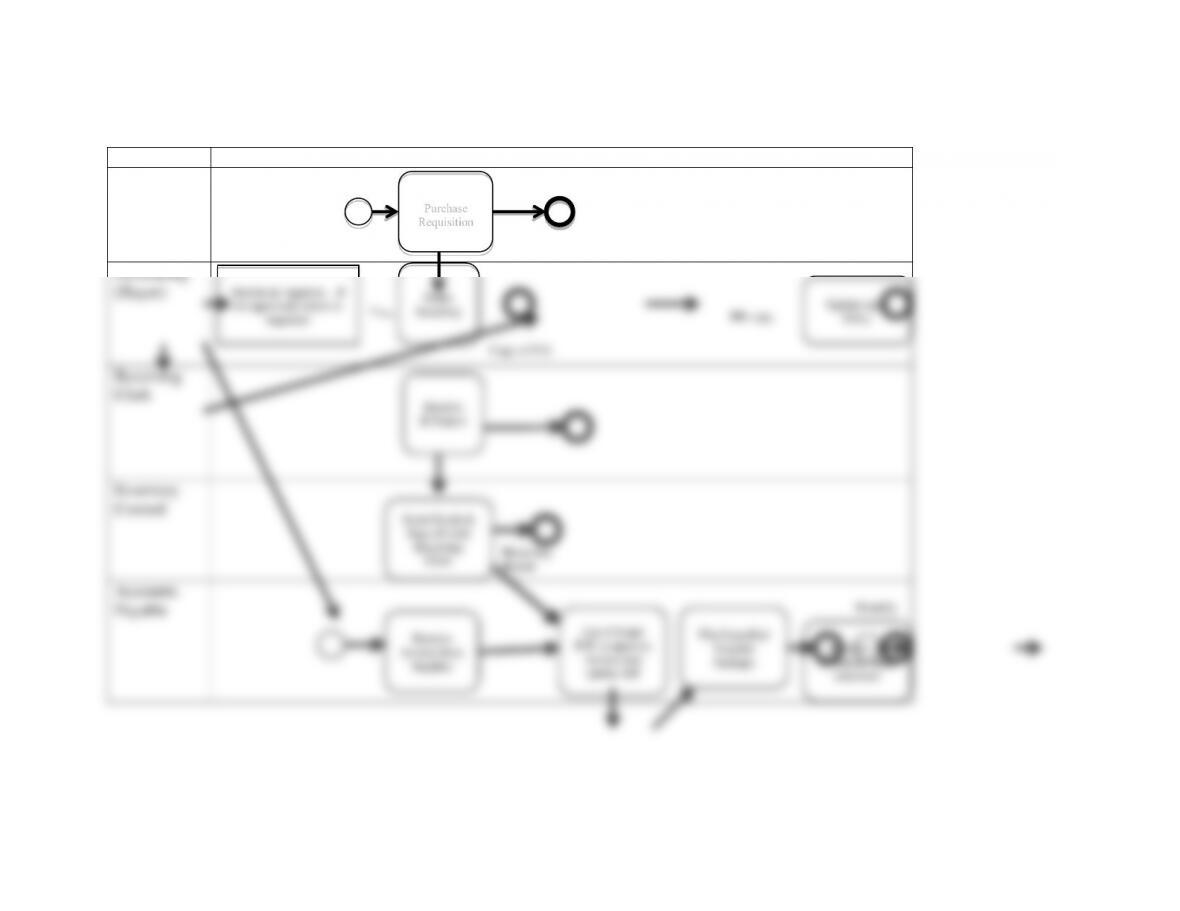

b. Draw a BPMN that reflects the ABC Company’s reengineered expenditure cycle processes.

Actual solution will depend upon which weaknesses were identified; this diagram addresses all the weaknesses.

Employee

Activity Performed (sequential, left-to-right across all rows)

Any

Employee

Purchasing

(Buyer)

Receiving

Clerk

Inventory

Control

Accounts

Payable

Purchase

Requisition

Order

Inventory

Receive

& Inspect

Use P.O and

R.R. to approve

invoice and

update A/P

Receive

Invoice from

Supplier

Receive &

Reconcile bank

statement

Review & Approve – if

not approved, return to

requester Update open

P.O.s

RR copy

Receiving

Report

Store Goods &

Sign off with

Receiving

Clerk

Copy of P.O.

File Cancelled

Voucher

Package

Monthly

Treasurer or

Cashier

Pay Supplier

& Cancel

Voucher

Package