Accounting Information Systems Ch 13: The Expenditure Cycle

13-2

Hint: You may need to use the VALUE function to transform the results of using the LEFT function to parse the lead digit in

each invoice amount.

13-3

However, the various character-parsing functions (LEFT, RIGHT, MID) all return their results as

text. Therefore, we need to transform that result back into a number by using the VALUE

13.4 Match threats in the first column to appropriate control procedures in the second

column. More than one control may be applicable.

Threat

Control Procedure

1. _d,e__ Failing to take available purchase

discounts for prompt payment.

a. Only accept deliveries for which an

approved purchase order exists.

2. _f__ Recording and posting errors in

accounts payable.

b. Document all transfers of inventory.

3. _l__ Paying for items not received.

c. Restrict physical access to inventory.

4. __h,o_ Kickbacks.

d. File invoices by due date.

5. _b,c,g_ Theft of inventory.

e. Maintain a cash budget.

6. _m,l_ Paying the same invoice twice.

f. Automated comparison of total change in

cash to total changes in accounts payable.

7. _g,b,c_ Stockouts.

g. Adopt a perpetual inventory system.

8. __h,i,j,o_ Purchasing items at inflated

prices.

h. Require purchasing agents to disclose

financial or personal interests in suppliers.

9. __k,q_ Misappropriation of cash.

i. Require purchases to be made only from

approved suppliers.

10. _h,i,o,p__ Purchasing goods of inferior

quality.

j. Restrict access to the supplier master data.

11. __a_ Wasted time and cost of returning

unordered merchandise to suppliers.

k. Restrict access to blank checks.

12. __n_ Accidental loss of purchasing data.

l. Only issue checks for a complete voucher

package (receiving report, supplier

invoice, and purchase order).

13. __j_ Disclosure of sensitive supplier

information (e.g., banking data).

m. Cancel or mark “Paid” all supporting

documents in a voucher package when a

check is issued.

n. Regular backup of the expenditure cycle

database.

o. Train employees how to respond properly

to gifts or incentives offered by suppliers.

p. Hold purchasing managers responsible for

costs of scrap and rework.

q. Reconciliation of bank account by

someone other than the cashier.

13.5 Use Table 13-2 to create a questionnaire checklist that can be used to evaluate

controls for each of the basic activities in the expenditure cycle (ordering goods,

receiving, approving supplier invoices, and cash disbursements).

a. For each control issue, write a Yes/No question such that a “No” answer

represents a control weakness. For example, one question might be “Are

supporting documents, such as purchase orders and receiving reports, marked

“paid” when a check is issued to the vendor?”

A wide variety of questions is possible. Below is a sample list:

Question

Yes

No

1. Is access to supplier master data restricted?

2. Are additions to supplier master data regularly reviewed and all

changes investigated?

3. Is sensitive data encrypted while stored in the database?

4. Does a backup and disaster recovery plan exist?

5. Have backup procedures been tested within the past year?

6. Are appropriate data entry edit controls used?

7. Is a perpetual inventory maintained?

8. Are physical counts of inventory taken regularly and used to adjust

the perpetual inventory records?

9. Are competitive bids used when ordering expensive items?

10. Are purchasing agents required to disclose financial interests in

suppliers?

11. Are budgets set for service expenses and are variances investigated?

12. Is the system configured to generate purchase orders only to suppliers

listed in the database?

13. Are receiving dock employees trained to accept deliveries only when

an approved purchase order exists?

14. Are receiving dock employees trained about the importance of

accurately counting all items delivered?

15. Do receiving dock employees inspect all deliveries for quality?

16. Do both receiving dock employees and inventory control employees

sign off on the transfer of items?

17. Is physical access to inventory restricted?

18. Are invoices only approved for payment when accompanied by both a

purchase order and receiving report?

19. Is supporting documentation cancelled or marked “Paid” when a

check is generated?

20. Are invoices filed by due date (adjusted for any discounts for early

payment)?

21. Is access to blank checks restricted?

22. Is access to the EFT system restricted?

23. Is the bank account regularly reconciled by someone not involved in

issuing checks?

Accounting Information Systems Ch 13: The Expenditure Cycle

13–

6

b. For each Yes/No question, write a brief explanation of why a “No” answer represents a

control weakness.

Question

Reason a “No” answer represents a weakness

1

Unrestricted access to supplier master data could facilitate fraud by allowing the creation of

fake suppliers to whom checks can be issued.

2

Failure to investigate all changes to supplier master data may allow fraud to occur because

unauthorized suppliers may not be detected.

3

Failure to encrypt sensitive data can result in the unauthorized disclosure of banking-related

information about suppliers.

4

If a backup and disaster recovery plan does not exist, the organization may lose important

data.

5

If the backup plan is not tested regularly, it may not work.

6

Without proper data entry edit controls, errors in purchasing, receiving, and paying suppliers

can occur.

7

Without a perpetual inventory system, shortages and excess inventory is more likely.

8

Without periodic physical counts, the perpetual inventory records are likely to be incorrect.

9

Without competitive bids, purchases may be at higher than necessary prices.

10

Non-disclosure of personal interests in suppliers creates a conflict of interest and may lead to

kickbacks and other forms of fraud.

11

Without budgets and analyses of services expenses, these expenses can be fraudulently

inflated to cover up fraud.

12

If generating purchase orders is not restricted to suppliers in the database, purchases may be

made from unauthorized suppliers which may result in paying too much, receiving inferior

quality goods, or violating laws.

13

If receiving dock employees accept deliveries without an approved purchase order, this may

result in higher costs and wasted time processing deliveries and then returning those

unordered items.

14

Failure to count deliveries accurately will create errors in inventory records and may result in

paying for goods not received.

15

Failure to inspect the quality of goods at the receiving dock increases the risk of production

delays when the problem is discovered later.

16

Failure to acknowledge the transfer of goods increases the risk of loss and precludes

assigning responsibility for any shortages.

17

Inadequate physical security increases the risk of theft of inventory.

18

Failure to require a voucher package can result in paying for items not ordered or not

received.

19

Failure to cancel supporting documents can result in paying the same invoice twice.

20

Failure to file invoices by due date increases the risk of not taking advantage of discounts for

prompt payment.

21

Unrestricted access to blank checks increases the risk of misappropriation of funds.

22

Unrestricted access to the EFT system increases the risk of misappropriation of funds.

23

Lack of an independent bank account reconciliation increases the risk of fraud going

undetected. It also precludes the timely identification of unauthorized disbursements,

possibly resulting in the bank refusing to correct the problem.

13-7

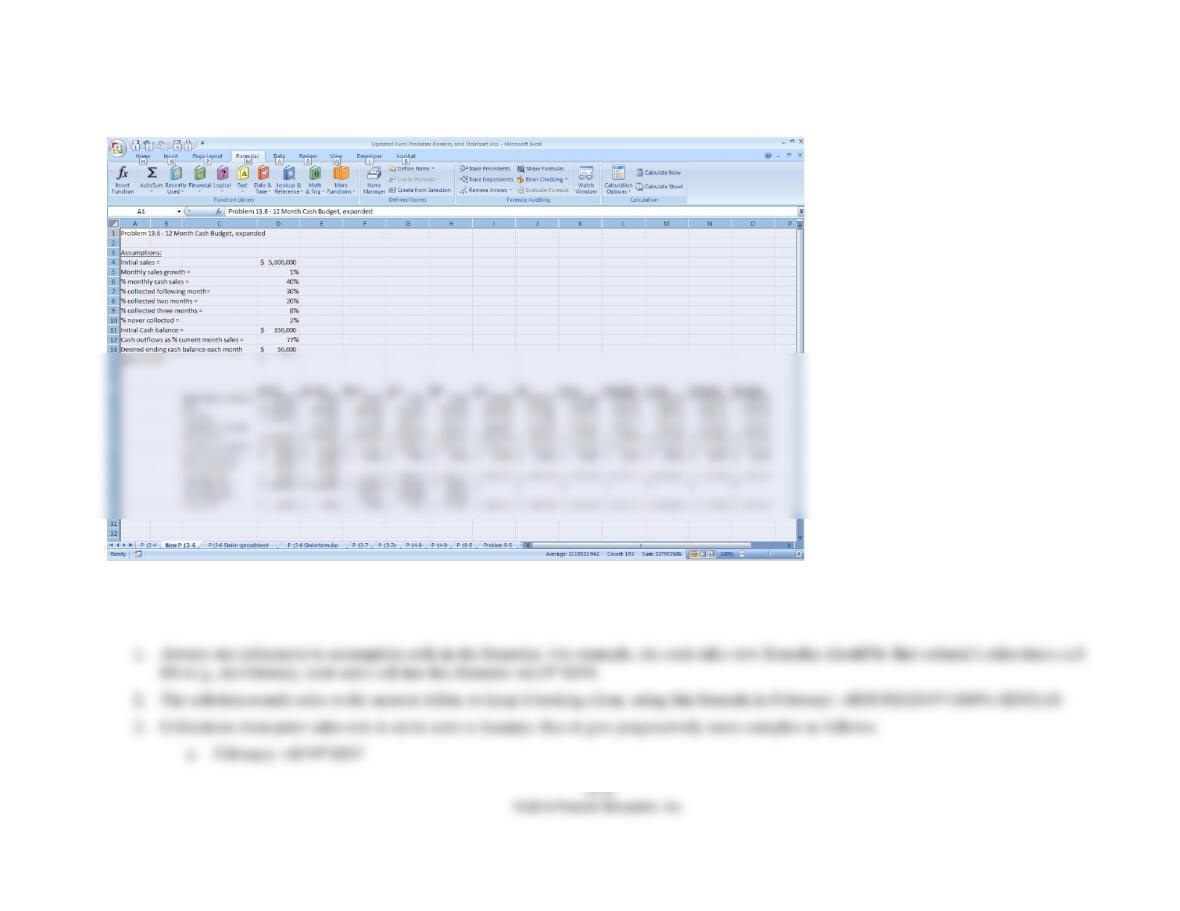

13.6 EXCEL PROJECT

a. Expand the cash budget you created in Problem 12.4 to include a row for expected cash outflows equal to 77% of the

current month’s sales.

b. Also add a row to calculate the amount of cash that needs to be borrowed, in order to maintain a minimum cash

balance of $50,000 at the end of each month.

c. Add another row to show the cash inflow from borrowing.

d. Add another row to show the cumulative amount borrowed.

e. Add another row to show the amount of the loan that can be repaid, being sure to maintain a minimum ending

balance of $50,000 each month.

Accounting Information Systems Ch 13: The Expenditure Cycle

Explanation of solution:

Accounting Information Systems Ch 13: The Expenditure Cycle

13–

9

13–

11

Accounting Information Systems Ch 13: The Expenditure Cycle

13.7 The following table presents the results of using a CAAT tool to interrogate the XYZ Company’s ERP system for expenditure

cycle activities. It shows the number of times each employee performed a specific task.

Order

Inventory

Maintain

Supplier

Master File

(add, delete,

edit)

Receive

Inventory

Approve

Supplier

Invoices

for

Payment

Pay

Suppliers

Via EFT

Sign

Checks

Mail

Checks

Reconcile

Bank

Account

Employee A

150

5

Employee B

100

100

100

Employee C

306

7

10

Employee D

70

10

10

Employee E

425

Employee F

150

125

Employee G

400

25

Employee H

1

Employee I

300

Required

Identify three examples of improper segregation of duties and explain the nature of each problem you find.

1. Employee A orders inventory and maintains supplier master – can alter supplier master to order from unapproved suppliers.

2. Employee C places orders and approves invoices – could order for personal use.

3. Employee C maintains supplier master file and approves invoices, so could submit and approve payments to fictitious vendors.

4. Employee D maintains supplier master and approves invoices – can submit and approve invoices from fictitious suppliers.

5. Employee D approves invoices and makes EFT payments – could approve disbursal of funds to self.

6. Employee G approves invoices and mails checks – by getting custody of signed checks, has opportunity to alter.

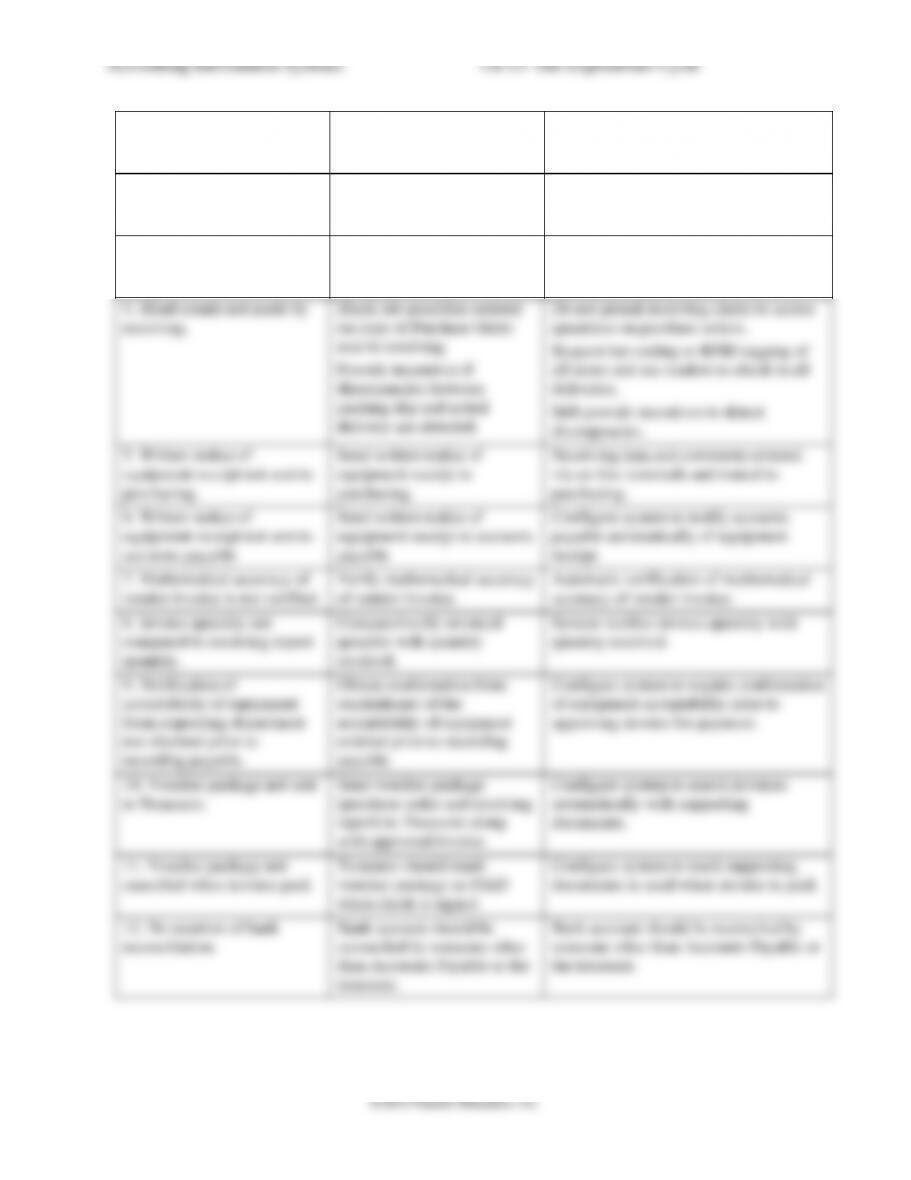

13.8 The following list identifies several important control features. For each control, (1)

describe its purpose and (2) explain how it could be best implemented in an integrated ERP

system.

a. Cancellation of the voucher package by the cashier after signing the check

b. Separation of duties of approving invoices for payment and signing checks

c. Prenumbering and periodically accounting for all purchase orders.

d. Periodic physical count of inventory.

e. Requiring two signatures on checks for large amounts

f. Requiring that a copy of the receiving report be routed through the inventory

stores department prior to going to accounts payable.

g. Requiring a regular reconciliation of the bank account by someone other than

the person responsible for writing checks

h. Maintaining an approved supplier list and checking that all purchase orders are

issued only to suppliers on that list

Item

Part I – Purpose

Part II – ERP System Control

a.

Prevent resubmission of invoices

for double payment

Control field in supplier invoice record to indicate

the document has been used

Control field in purchase order and receiving report

records to indicate the document has been used to

support payment.

b.

Prevent payment of fictitious

invoices

System matches all invoices to corresponding

receiving reports and purchase orders

Checks signed by cashier.

c.

Prevent unauthorized purchases.

Sequence check of all purchase orders.

d.

Verify the accuracy of recorded

amounts and detect losses.

Still need to count physical inventory periodically.

e.

Prevent large disbursements for

questionable reasons.

Still need two signatures.

f.

Verifies that items received were

placed in inventory and were not

stolen.

Receiving clerks enter that goods were transferred to

inventory.

Inventory clerks acknowledge receipt of goods via

terminals. System configured so that voucher

package requires that the receiving report include the

acknowledgement of receipt by inventory control.

g.

Detect unauthorized disbursements.

Still required.

h.

Ensure the purchase of quality

goods and prevent violations of

laws or company policies.

Validity check of supplier number on all purchase

orders.

Restrict access to the supplier master file

Verify all changes to the supplier master file

Restrictions on who can make changes to the supplier

master file.

13–

14

13.9 For good internal control, which of the following duties can be performed by the

same individual?

1. Approve purchase orders

2. Negotiate terms with suppliers

3. Reconcile the organization’s bank account

4. Approve supplier invoices for payment

5. Cancel supporting documents in the voucher package

6. Sign checks

7. Mail checks

8. Request inventory to be purchased

9. Inspect quantity and quality of inventory received

The cells in the following table marked with an X indicate duties that can be performed by the

same individual without creating an internal control weakness:

Duty

1

2

3

4

5

6

7

8

9

1

2

X

3

4

5

6

X

7

X

X

8

9

Accounting Information Systems Ch 13: The Expenditure Cycle

13–

15

13.10 Last year the Diamond Manufacturing Company purchased over $10 million worth

of office equipment under its “special ordering” system, with individual orders

ranging from $5,000 to $30,000. Special orders are for low-volume items that have

been included in a department manager’s budget. The budget, which limits the

types and dollar amounts of office equipment a department head can requisition, is

approved at the beginning of the year by the board of directors. The special

ordering system functions as follows:

Purchasing A purchase requisition form is prepared and sent to the purchasing

department. Upon receiving a purchase requisition, one of the five purchasing

agents (buyers) verifies that the requester is indeed a department head. The buyer

next selects the appropriate supplier by searching the various catalogs on file. The

buyer then phones the supplier, requests a price quote, and places a verbal order. A

prenumbered purchase order is processed, with the original sent to the supplier and

copies to the department head, receiving, and accounts payable. One copy is also

filed in the open-requisition file. When the receiving department verbally informs

the buyer that the item has been received, the purchase order is transferred from

the open to the filled file. Once a month, the buyer reviews the unfilled file to follow

up on open orders.

Receiving The receiving department gets a copy of each purchase order. When

equipment is received, that copy of the purchase order is stamped with the date and,

if applicable, any differences between the quantity ordered and the quantity

received are noted in red ink. The receiving clerk then forwards the stamped

purchase order and equipment to the requisitioning department head and verbally

notifies the purchasing department that the goods were received.

Accounts Payable Upon receipt of a purchase order, the accounts payable clerk

files it in the open purchase order file. When a vendor invoice is received, it is

matched with the applicable purchase order, and a payable is created by debiting

the requisitioning department’s equipment account. Unpaid invoices are filed by

due date. On the due date, a check is prepared and forwarded to the treasurer for

signature. The invoice and purchase order are then filed by purchase order number

in the paid invoice file.

Treasurer Checks received daily from the accounts payable department are

sorted into two groups: those over and those under $10,000. Checks for less than

$10,000 are machine signed. The cashier maintains the check signature machine’s

key and signature plate and monitors its use. Both the cashier and the treasurer sign

all checks over $10,000.

a. Describe the weaknesses relating to purchases and payments of “special orders”

by the Diamond Manufacturing Company.

b. Recommend control procedures that must be added to overcome weaknesses

identified in part a.

c. Describe how the control procedures you recommended in part b should be

modified if Diamond reengineered its expenditure cycle activities to make

maximum use of current IT (e.g., EDI, EFT, bar-code scanning, and electronic

forms in place of paper documents).

Weakness

Control

Effect of new IT

1. Buyer does not verify that

the department head’s request

is within budget.

Compare requested amounts

to total budget and YTD

expenditures.

System can automatically compare the

requested amount to the remaining

budget.

2. No procedures established

to ensure the best price is

obtained.

Solicit quotes/bids for large

orders.

EDI and Internet can be used to solicit

bids.

3. Buyer does not check

vendor’s past performance.

Prepare a vendor performance

report and use it when

selecting vendors.

Vendor performance ratings can be

updated automatically and made

available to buyer.

4. Blind counts not made by

receiving.

Black out quantities ordered

on copy of Purchase Order

sent to receiving

Provide incentives if

discrepancies between

packing slip and actual

delivery are detected.

Do not permit receiving clerks to access

quantities on purchase orders.

Request bar coding or RFID tagging of

all items and use readers to check in all

deliveries.

Still provide incentives to detect

discrepancies.

5. Written notice of

equipment receipt not sent to

purchasing.

Send written notice of

equipment receipt to

purchasing.

Receiving data and comments entered

via on-line terminals and routed to

purchasing.

6. Written notice of

equipment receipt not sent to

accounts payable

Send written notice of

equipment receipt to accounts

payable

Configure system to notify accounts

payable automatically of equipment

receipt.

7. Mathematical accuracy of

vendor invoice is not verified.

Verify mathematical accuracy

of vendor invoice.

Automatic verification of mathematical

accuracy of vendor invoice.

8. Invoice quantity not

compared to receiving report

quantity.

Compare/verify invoiced

quantity with quantity

received.

System verifies invoice quantity with

quantity received.

9. Notification of

acceptability of equipment

from requesting department

not obtained prior to

recording payable.

Obtain confirmation from

requisitioner of the

acceptability of equipment

ordered prior to recording

payable.

Configure system to require confirmation

of equipment acceptability prior to

approving invoice for payment.

10. Voucher package not sent

to Treasurer.

Send voucher package

(purchase order and receiving

report) to Treasurer along

with approved invoice.

Configure system to match invoices

automatically with supporting

documents.

11. Voucher package not

cancelled when invoice paid.

Treasurer should mark

voucher package as PAID

when check is signed.

Configure system to mark supporting

documents as used when invoice is paid.

12. No mention of bank

reconciliation.

Bank account should be

reconciled by someone other

than Accounts Payable or the

treasurer.

Bank account should be reconciled by

someone other than Accounts Payable or

the treasurer.

Accounting Information Systems Ch 13: The Expenditure Cycle

13–

17

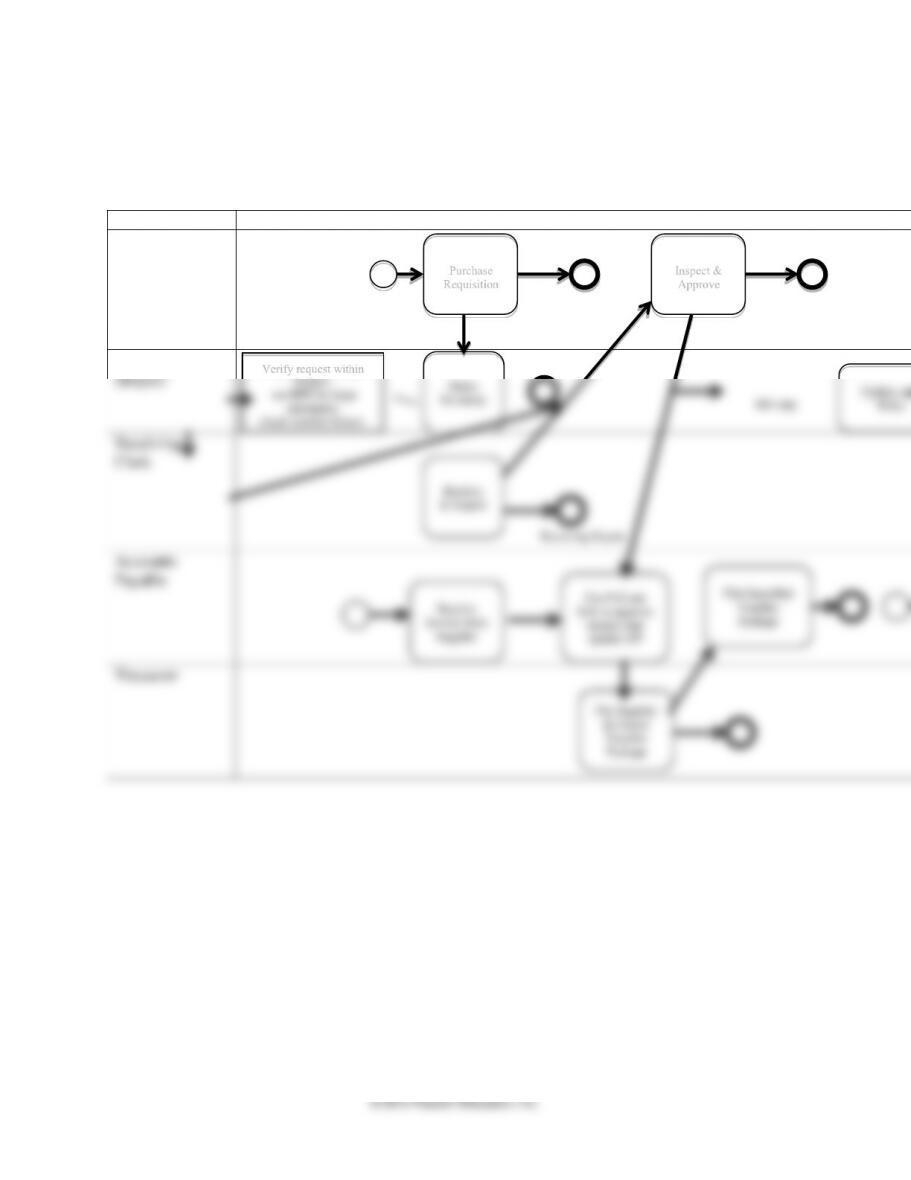

d. Draw a BPMN diagram that depicts Diamond’s reengineered expenditure cycle.

(CPA Examination, adapted)

Solution will vary depending upon which weaknesses were corrected. This BPMN

addresses all the weaknesses listed above.

Employee

Activity Performed (sequential, left-to-right across all rows)

Department

Heads

Purchasing

(Buyer)

Receiving

Clerk

Accounts

Payable

Treasurer

Purchase

Requisition

Order

Inventory

Receive

& Inspect

Use P.O and

R.R. to approve

invoice and

update A/P

Receive

Invoice from

Supplier

Pay Supplier

& Cancel

Voucher

Package

Verify request within

budget;

use RFP for large

purchases;

check supplier history

Update open

P.O.s

RR copy

Receiving Report

Inspect &

Approve

Equipment

Notification of acceptability

File Cancelled

Voucher

Package