Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 11

AUDITING COMPUTER-BASED INFORMATION SYSTEMS

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

11.1 Auditing an AIS effectively requires that an auditor have some knowledge of computers and

their accounting applications. However, it may not be feasible for every auditor to be a

computer expert. Discuss the extent to which auditors should possess computer expertise to

be effective auditors.

Since most organizations make extensive use of computer-based systems in processing data, it is

essential that computer expertise be available in the organization's audit group. Such expertise

should include:

Not all auditors need to possess expertise in all of these areas. However, there is certainly some

minimum level of computer expertise that is appropriate for all auditors to have. This would

include:

11.2 Should internal auditors be members of systems development teams that design and

implement an AIS? Why or why not?

11.3 At present, no Berwick employees have auditing experience. To staff its new internal audit

function, Berwick could (a) train some of its computer specialists in auditing, (b) hire

experienced auditors and train them to understand Berwick’s information system, (c) use a

combination of the first two approaches, or (d) try a different approach. Which approach

would you support, and why?

11.4 The assistant finance director for the city of Tustin, California, was fired after city officials

discovered that she had used her access to city computers to cancel her daughter’s $300 water

bill. An investigation revealed that she had embezzled a large sum of money from Tustin in

this manner over a long period. She was able to conceal the embezzlement for so long because

the amount embezzled always fell within a 2% error factor used by the city’s internal

auditors. What weaknesses existed in the audit approach? How could the audit plan be

improved? What internal control weaknesses were present in the system? Should Tustin’s

internal auditors have discovered this fraud earlier?

Audit approach weaknesses

practice.

Audit plan improvements

Internal control weaknesses

Should the auditors have detected the audit earlier?

11.5 Lou Goble, an internal auditor for a large manufacturing enterprise, received an

anonymous note from an assembly-line operator who has worked at the company’s West

Coast factory for the past 15 years. The note indicated that there are some fictitious

employees on the payroll as well as some employees who have left the company. He offers no

proof or names. What computer-assisted audit technique could Lou use to help him

substantiate or refute the employee’s claim? (CIA Examination, adapted)

11.6. Explain the four steps of the risk-based audit approach, and discuss how they apply to the

overall security of a company.

The risk-based audit approach provides a framework for conducting information system audits. It

consists of the following 4 steps:

11.7. Compare and contrast the frameworks for auditing program development/acquisition and for

auditing program modification.

The two are similar in that:

The two are dissimilar in that:

SUGGESTED SOLUTIONS TO THE PROBLEMS

11.1 You are the director of internal auditing at a university. Recently, you met with Issa Arnita,

the manager of administrative data processing, and expressed the desire to establish a more

effective interface between the two departments. Issa wants your help with a new

computerized accounts payable system currently in development. He recommends that your

department assume line responsibility for auditing suppliers’ invoices prior to payment. He

also wants internal auditing to make suggestions during system development, assist in its

installation, and approve the completed system after making a final review.

Would you accept or reject each of the following? Why?

a. The recommendation that your department be responsible for the pre-audit of

supplier's invoices.

b. The request that you make suggestions during system development.

c. The request that you assist in the installation of the system and approve the system after

making a final review.

11.2 As an internal auditor for the Quick Manufacturing Company, you are participating in the

audit of the company’s AIS. You have been reviewing the internal controls of the computer

system that processes most of its accounting applications. You have studied the company’s

extensive systems documentation. You have interviewed the information system manager,

operations supervisor, and other employees to complete your standardized computer internal

control questionnaire. You report to your supervisor that the company has designed a

successful set of comprehensive internal controls into its computer systems. He thanks you for

your efforts and asks for a summary report of your findings for inclusion in a final overall

report on accounting internal controls.

Have you forgotten an important audit step? Explain. List five examples of specific audit

procedures that you might recommend before reaching a conclusion.

11.3 As an internal auditor, you have been assigned to evaluate the controls and operation of a

computer payroll system. To test the computer systems and programs, you submit

independently created test transactions with regular data in a normal production run.

List four advantages and two disadvantages of this technique.

a. Advantages

b. Disadvantages

• Does not require extensive programming knowledge

• Approach and results are easy to understand.

• The complete system may be reviewed.

• Results are often easily checked.

• An opinion may be formed as to the system's data

processing accuracy.

• A regular computer program may be used.

• It may save time.

• The auditor gains experience.

• The auditor maintains control over the test.

• Invalid data can be submitted to test for rejections.

• Impractical to test all error possibilities.

• May be unable to relate input data to

output reports in a complex system.

• If independent files are not used, it may be

difficult to reverse or back out test data.

• Preparation of satisfactory test transactions

may be time consuming.

(CIA Examination, adapted)

a. Advantages

b. Disadvantages

• Extensive programming knowledge is not necessary.

• Understandable approach and results.

• Revision on the complete system

• Results are often easily evaluated.

• An opinion may be formed as to the system's data

processing accuracy.

• Make use of a regular computer program

• Time saving

• The auditor gains experience.

• The auditor maintains control over the test.

• Impossible to test all error cases.

• Not easy to identify a connection between

input data and output reports in a complex

system.

• Trouble in reserving or back out test data

due to the lack of use of independent files

• Preparation of satisfactory test transactions

may be time consuming.

11.4 You are involved in the audit of accounts receivable, which represent a significant portion of

the assets of a large retail corporation. Your audit plan requires the use of the computer, but

you encounter the following reactions:

For each situation, state how the auditor should proceed with the accounts receivable audit.

a. The computer operations manager says the company’s computer is running at full

capacity for the foreseeable future and the auditor will not be able to use the system for

audit tests.

b. The computer scheduling manager suggests that your computer program be stored in

the computer program library so that it can be run when computer time becomes

available.

c. You are refused admission to the computer room.

d. The systems manager tells you that it will take too much time to adapt the auditor’s

computer audit program to the computer’s operating system and that company

programmers will write the programs needed for the audit.

(CIA Examination, adapted)

11.5 You are a manager for the CPA firm of Dewey, Cheatem, and Howe (DC&H). While

reviewing your staff’s audit work papers for the state welfare agency, you find that the test

data approach was used to test the agency’s accounting software. A duplicate program copy,

the welfare accounting data file obtained from the computer operations manager, and the test

transaction data file that the welfare agency’s programmers used when the program was

written were processed on DC&H’s home office computer. The edit summary report listing

no errors was included in the working papers, with a notation by the senior auditor that the

test indicates good application controls. You note that the quality of the audit conclusions

obtained from this test is flawed in several respects, and you decide to ask your subordinates

to repeat the test.

Identify three existing or potential problems with the way this test was performed. For each

problem, suggest one or more procedures that might be performed during the revised test to

avoid flaws in the audit conclusions.

Problems

Suggested Solutions

Duplicate copy of the program may not be a

true duplicate of the current version.

• Source code comparison.

• Reprocessing (use previously valid program).

• Process test transactions concurrently with live

ones, on a concealed basis.

Duplicate copy of the file may not be a true

duplicate of the current version.

• Obtain the live file and duplicate it under audit

control.

• Process test transactions concurrently with live

ones, on a concealed basis.

Programmer's test data file

a. was not independently prepared, and

b. may not have contained any erroneous

transactions to test the program’s ability

to detect errors.

• Auditor must devise their own test transactions,

either (a) manually, or (b) using a test data

generator. Erroneous transactions should

deliberately be included.

The test only checks the programs, not the

source data controls, error procedures, etc.

• Process test transactions concurrently with live

ones, on a concealed basis.

• Use mini-company test (Integrated Test

Facility).

Audit senior's conclusion has no basis (no

supporting evidence).

• Must predetermine the result of test data

processing, and then compare these to actual

results.

11.6 You are performing an information system audit to evaluate internal controls in Aardvark

Wholesalers’ (AW) computer system. From an AW manual, you have obtained the following job

descriptions for key personnel:

Director of information systems: Responsible for defining the mission of the information systems

division and for planning, staffing, and managing the IS department.

Manager of systems development and programming: Reports to director of information systems.

Responsible for managing the systems analysts and programmers who design, program, test,

implement, and maintain the data processing systems. Also responsible for establishing and monitoring

documentation standards.

Manager of operations: Reports to director of information systems. Responsible for management of

computer center operations, enforcement of processing standards, and systems programming,

including implementation of operating system upgrades.

Data entry supervisor: Reports to manager of operations. Responsible for supervision of data entry

operations and monitoring data preparation standards.

Operations supervisor: Reports to manager of operations. Responsible for supervision of computer

operations staff and monitoring processing standards.

Data control clerk: Reports to manager of operations. Responsible for logging and distributing

computer input and output, monitoring source data control procedures, and custody of programs and

data files.

b. Name two positive and two negative aspects (from an internal control standpoint) of this

organizational structure.

c. What additional information would you require before making a final judgment on the

adequacy of AW’s separation of functions in the information systems division?

a. Prepare an organizational chart for AW’s information systems division.

Director of

Information

Systems

Manager of

Systems

Development and

Programming

Manager of

Operations

Data Entry

Supervision

Operations

Supervisor

Data Control

Clerk

11.7 Robinson’s Plastic Pipe Corporation uses a data processing system for inventory. The input to

this system is shown in Table 11-7. You are using an input controls matrix to help audit the

source data controls.

Table 11-7 Parts Inventory Transaction File

Field Name

Field Type

Item number

Numeric

Description

Alphanumeric

Transaction date

Date

Transaction type

Alphanumeric

Document number

Alphanumeric

Quantity

Numeric

Unit cost

Monetary

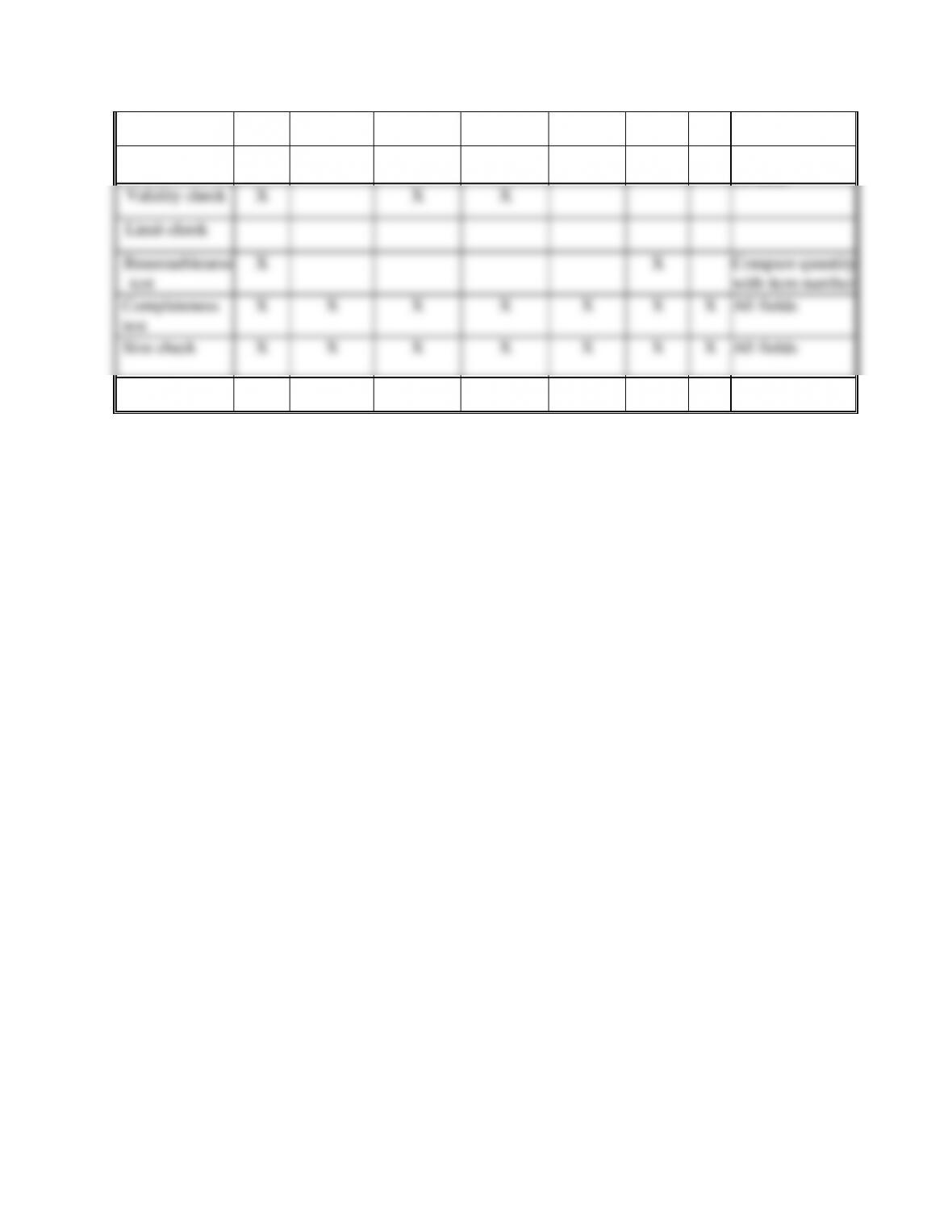

Prepare an input controls matrix using the format and input controls shown in Figure 11-3;

however, replace the field names shown in Figure 11-3 with those shown in Table 11-7. Place

checks in the matrix cells that represent input controls you might expect to find for each field.

Inventory transactions input control matrix:

RECORD

NAME:

Parts inventory

transactions

FIELD NAMES

Item

number

Description

Transaction

date

Transaction

type

Document

number

Quantity

Unit

cost

Comments

INPUT

CONTROLS:

Financial totals

X

Compute Total

cost if possible

Hash totals

X

X

Record counts

Yes

Cross-footing

balance

No

Visual

inspection

X

X

X

X

X

X

X

All fields

Check digit

verification

X

Prenumbered

forms

X

Use prenumbered

form

Turnaround

document

No

Edit program

Yes

Sequence check

X

Field check

X

X

X

X

Sign check

X

X

Also for balance

on hand

Validity check

X

X

X

Limit check

Reasonableness

test

X

X

Compare quantity

with item number

Completeness

test

Completeness

Test

Completeness

Test

X

X

X

X

X

X

X

All fields

Size check

X

X

X

X

X

X

X

All fields

Other: