(20 min.) E9-52B

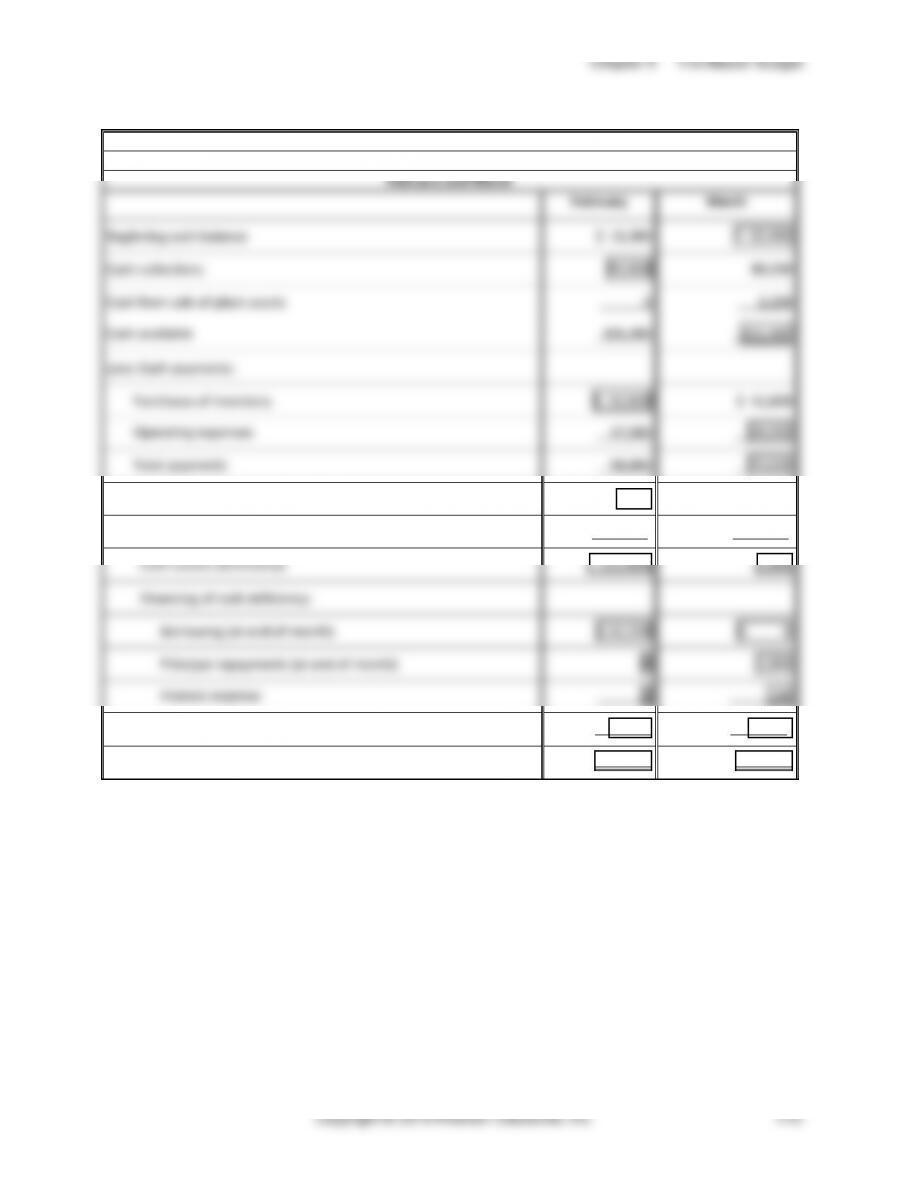

Reilly Adventures

Cash Budget

February and March

February

March

Beginning cash balance

$ 16,300

$ 20,000

Cash collections

90,000

80,200

Cash from sale of plant assets

0

2,200

Cash available

106,300

102,400

Less: Cash payments:

Purchases of inventory

$ 50,900

$ 41,600

Operating expenses

47,900

38,000

Total payments

98,800

79,600

(1) Ending cash balance before financing

7,500

22,800

Less: Minimum cash balance desired

(20,000)

(20,000)

Cash excess (deficiency)

(12,500)

2,800

Financing of cash deficiency:

Borrowing (at end of month)

$ 12,500

$ 0

Principal repayments (at end of month)

0

2,604

Interest expense

0

196

(2) Total effects of financing

12,500

(2,800)

Ending cash balance (1) + (2)

$ 20,000

$ 20,000

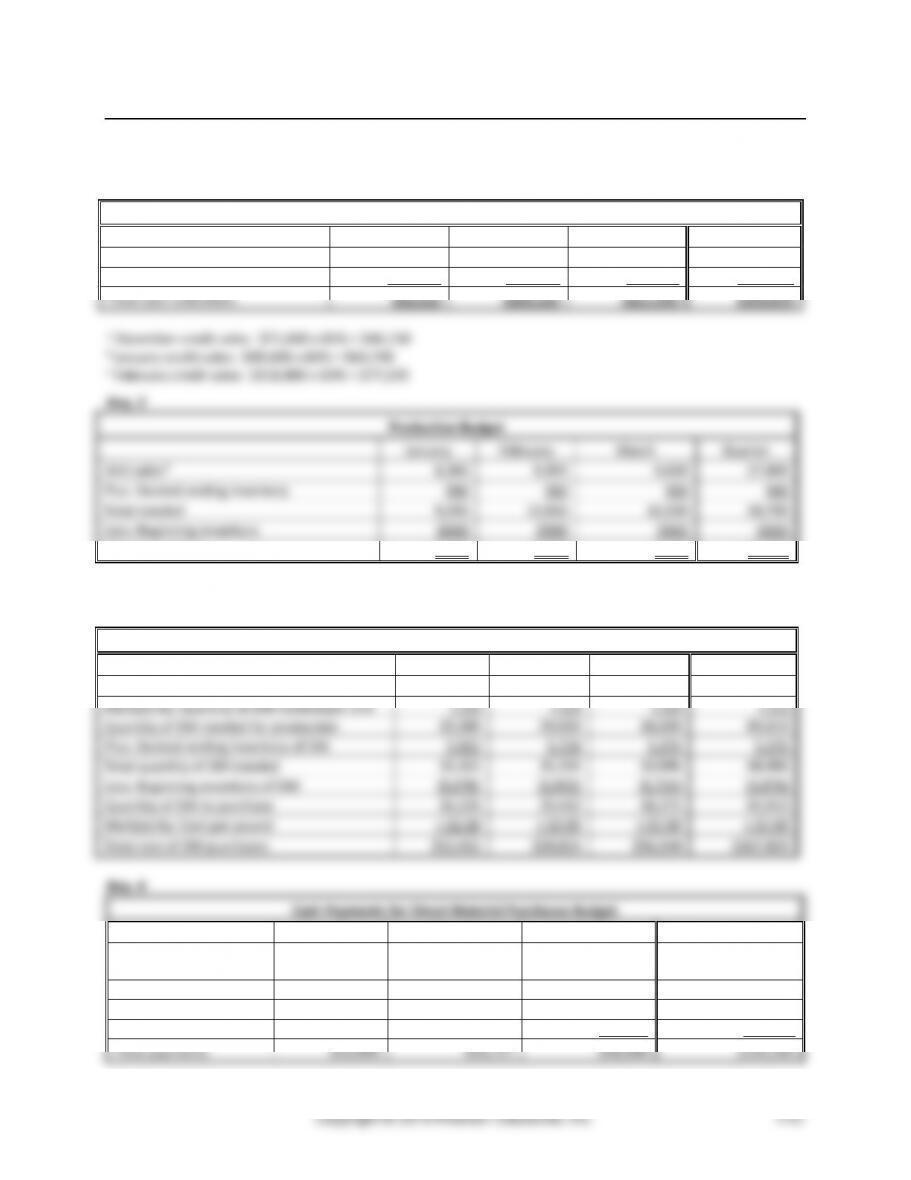

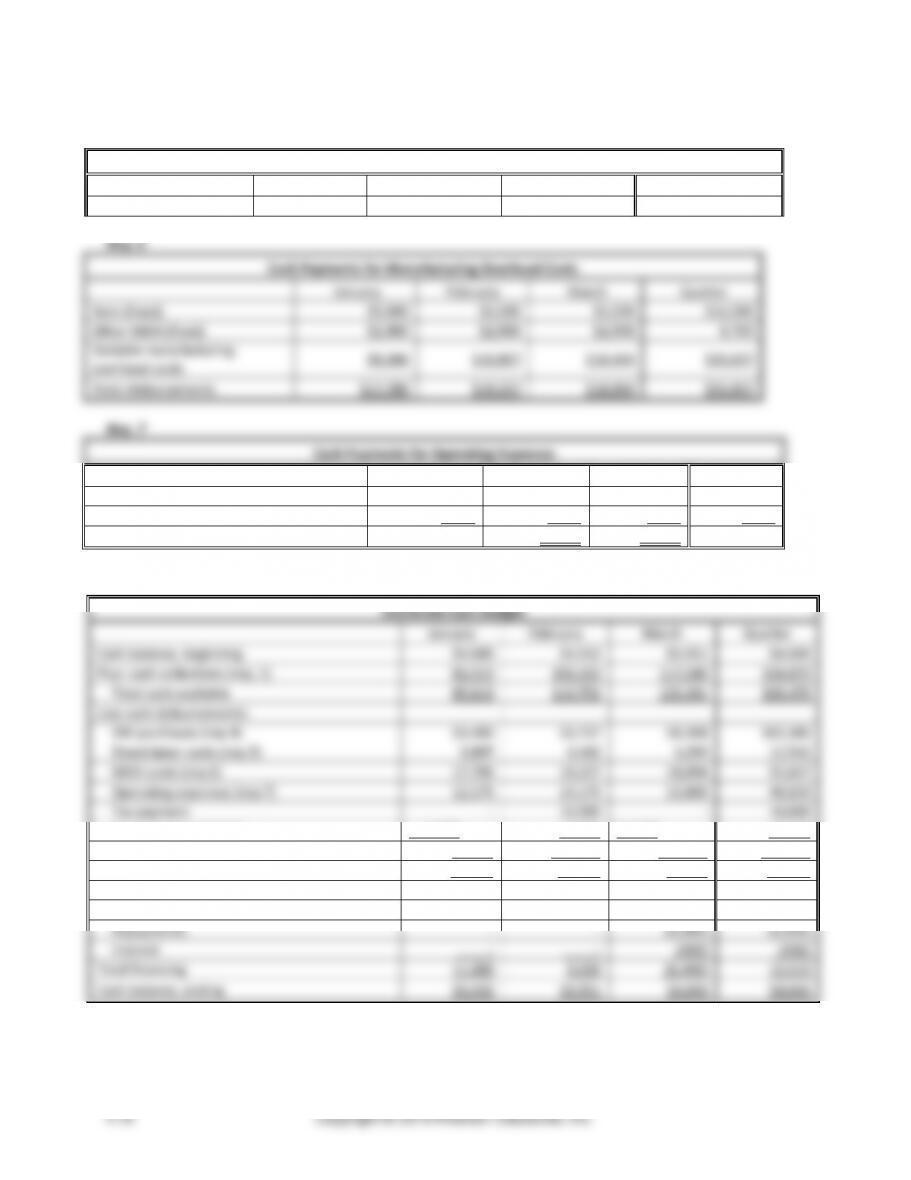

(15-20 min.) E9-53B

Tempest Readers

Inventory, Purchases, and Cost of Goods Sold Budget

Nine Months Ended September 30

QUARTER ENDED

NINE-MONTH

March 31

June 30

Sept.30

TOTAL

Cost of goods sold:

(0.60 × $100,000)

$ 60,000

(0.60 × $150,000)

$ 90,000

(0.60 × $125,000)

$ 75,000

$225,000

Plus: Desired ending inventory

[$15,000 + (0.15 × $90,000)]

28,500

[$15,000 + (0.15 × $75,000)]

26,250

[$15,000 + (0.15 × 0.60 × $220,000)]

34,800

Total inventory required

88,500

116,250

109,800

Less: Beginning inventory

(14,000)

(28,500)

(26,250)

Amount of inventory to purchase

$ 74,500

$ 87,750

$ 83,550

Chapter 9 The Master Budget

Problems (Group A)

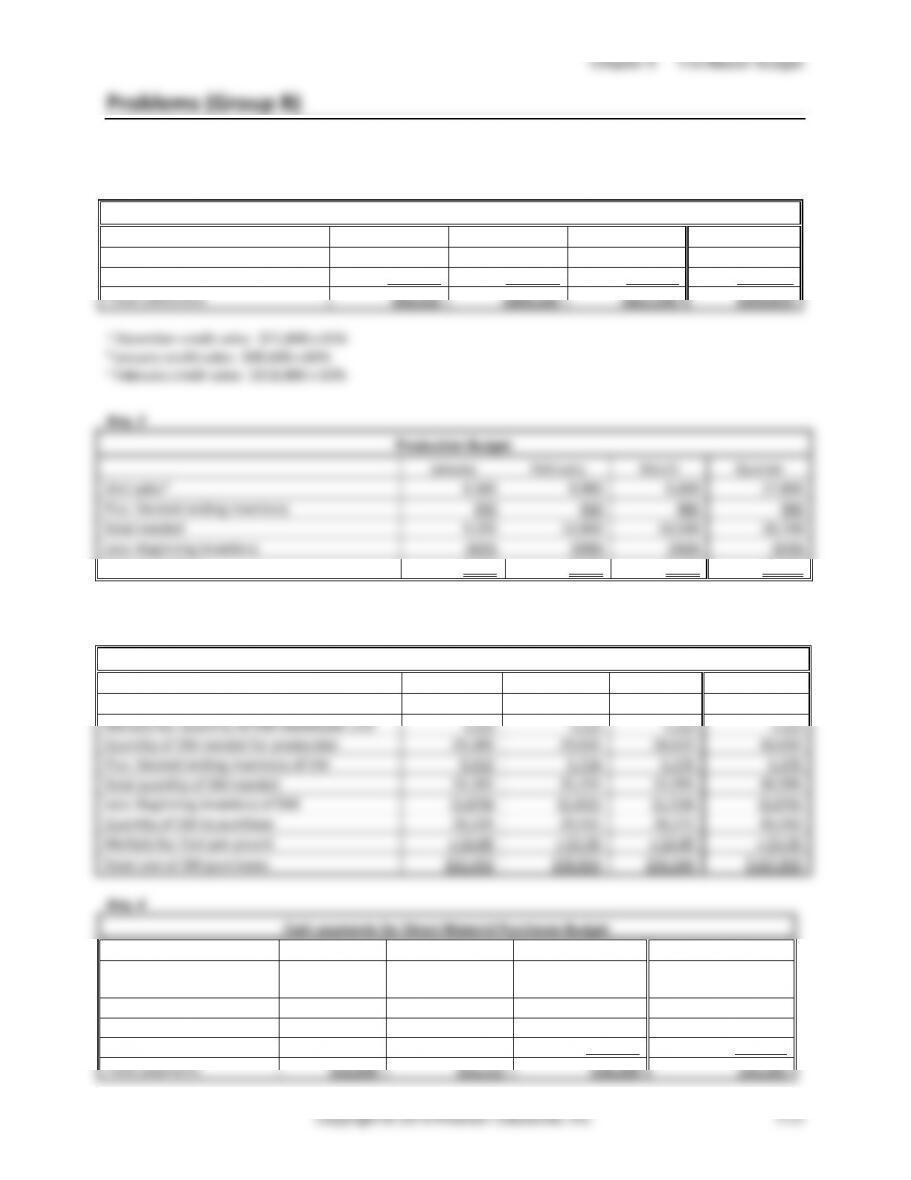

(60 min.) P9-54A

Req. 1

Cash Collections Budget

January

February

March

Quarter

Cash sales (35%)

$34,860

$41,580

$40,320

$116,760

Credit sales (65%)

$46,150a

$64,740b

$77,220c

$188,110

Total cash collections

$81,010

$106,320

$117,540

$304,870

a December credit sales: $71,000 x 65% = $46,150

b January credit sales: $99,600 x 65% = $64,740

c February credit sales: $118,800 x 65% = $77,220

Req. 2

Production Budget

January

February

March

Quarter

Unit sales*

8,300

9,900

9,600

27,800

Plus: Desired ending inventory

990

960

900

900

Total needed

9,290

10,860

10,500

28,700

Less: Beginning inventory

(830)

(990)

(960)

(830)

Units to produce

8,460

9,870

9,540

27,870

*Hint: Unit sales = Sales in dollars ÷ Selling price per unit

Req. 3

Direct Materials Budget

January

February

March

Quarter

Units to be produced

8,460

9,870

9,540

27,870

Multiply by: Quantity of DM needed per unit

× 3.0

× 3.0

× 3.0

× 3.0

Quantity of DM needed for production

25,380

29,610

28,620

83,610

Plus: Desired ending inventory of DM

5,922

5,724

5,376

5,376

Total quantity of DM needed

31,302

35,334

33,996

88,986

Less: Beginning inventory of DM

(5,076)

(5,922)

(5,724)

(5,076)

Quantity of DM to purchase

26,226

29,412

28,272

83,910

Multiply by: Cost per pound

× $2.00

× $2.00

× $2.00

× $2.00

Total cost of DM purchases

$52,452

$58,824

$56,544

$167,820

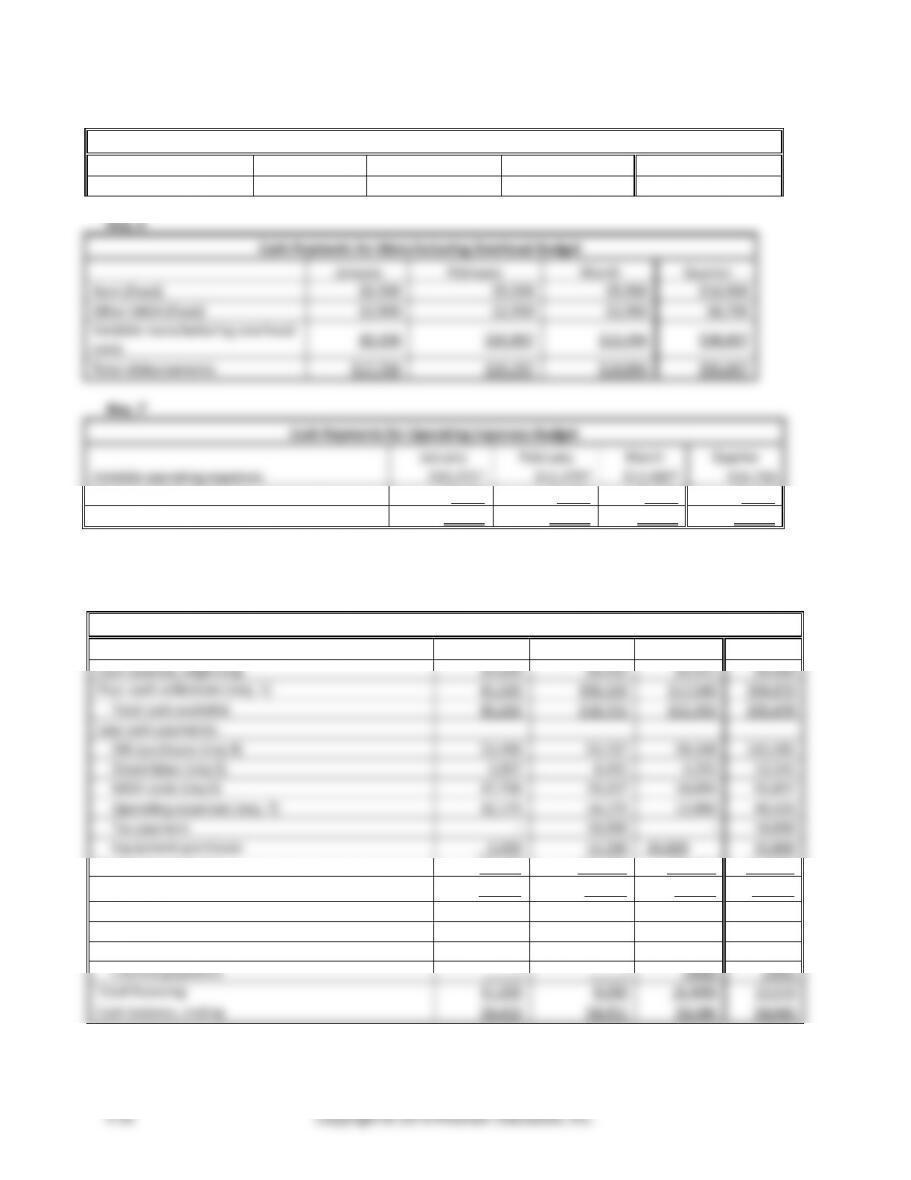

Req. 4

Cash Payments for Direct Material Purchases Budget

January

February

March

Quarter

December purchases

(From AP)

$43,000

$43,000

January purchases

$10,490

$41,962

$52,452

February purchases

$11,765

$47,059

$58,824

March purchases

$11,309

$11,309

Total payments

$53,490

$53,727

$58,368

$165,585

Managerial Accounting 4e Solutions Manual

(continued) P9-54A

Req. 5

Cash Payments for Direct Labor Budget

January

February

March

Quarter

Direct labor

$3,807

$4,442

$4,293

$12,542

Rent (fixed)

Other MOH (fixed)

Total disbursements

Variable operating expenses

$12,375*

Fixed operating expenses

$5,400

Total payments for operating expenses

$12,175

$14,175

Chapter 9 The Master Budget

(continued) P9-54A

Req. 9

Budgeted Manufacturing Cost per Unit

Direct materials cost per unit

$6.00

Direct labor cost per unit

0.45

Variable manufacturing costs per unit

1.10

Fixed manufacturing overhead per unit

$0.70

Cost of manufacturing each unit

$8.25

Req. 10

Damon Manufacturing

Budgeted Income Statement

For the Quarter Ended March 31

Sales

$333,600

Less: Cost of goods sold

(229,350)

Gross profit

104,250

Less: Operating expenses

(40,150)

Less: Depreciation expense

(4,800)

Operating income

$59,300

Less: interest expense

(490)

Less: income tax expense @ 30%

(17,643)

Net income

$41,167

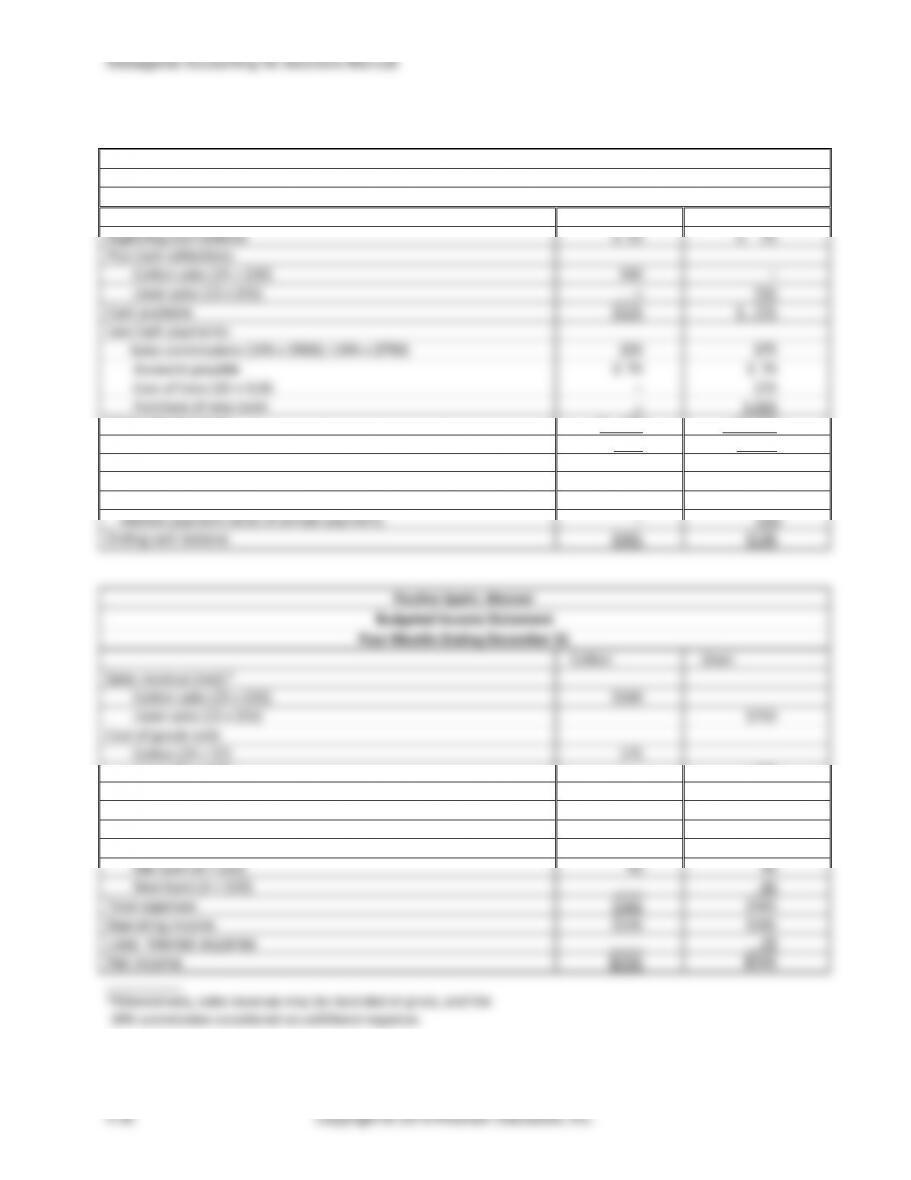

(60-75 min.) P9-55A

Req. 1

Pauline Spahr, Weaver

Cash Budget

Four Months Ending December 31

Cotton

Linen

Beginning cash balance

$ 25

$ 25

Plus Cash collections:

Cotton sales (25 × $20)

500

–

Linen sales (15 x $50)

–

750

Cash available

$525

$ 775

Less Cash payments:

Sales commissions (10% x $500); (10% x $750)

$50

$75

Accounts payable

$ 74

$ 74

Cost of linen (15 × $18)

–

270

Purchase of new loom

–

1,000

Total cash payments

$ 124

$1,419

Ending cash balance before financing

401

(644)

Financing of cash deficiency:

Borrowing

–

$1,000

Principal payment

–

(200)

Interest payment (4/12 of annual payment)

–

(20)

Ending cash balance

$401

$136

Pauline Spahr, Weaver

Budgeted Income Statement

Four Months Ending December 31

Cotton

Linen

Sales revenue (net):*

Cotton sales (25 x $20)

$500

Linen sales (15 x $50)

$750

Cost of goods sold:

Cotton (25 × $7)

175

Linen (15 × $18)

270

Sales Commissions

Cotton (10% x $500)

50

Linen (10% x $750

75

Depreciation expense:

Old loom (4 × $10)

40

40

New loom (4 × $20)

80

Total expenses

$265

$465

Operating income

$235

$285

Less: Interest expense

20

Net income

$235

$265

__________

*Alternatively, sales revenue may be recorded at gross, and the

10% commission considered an additional expense.

Chapter 9 The Master Budget

(continued) P9-55A

Req. 1

Pauline Spahr, Weaver

Budgeted Balance Sheet

December 31

Cotton

Linen

Cotton

Linen

Current assets

Current liabilities

Cash

$401

$136

Bank loan payable

$0

$800

Inventory of cotton

0

175

Total liabilities

0

800

Total current assets

401

311

Fixed assets:

Owners’ equity

Loom(s)

500

1,500

Cotton loom

621

Accumulated

depreciation:

Cotton loom and linen loom

611

Cotton loom

(280)

(280)

Linen loom

(80)

Total fixed assets

220

1,140

Total assets

$621

$1,451

Total liabilities and owners’ equity

$621

$1,451

Req. 2

Based on financial considerations only, Spahr should continue making cotton placemats and should not purchase

$450

$675

$275

$175

Managerial Accounting 4e Solutions Manual

(continued) P9-55A

Chapter 9 The Master Budget

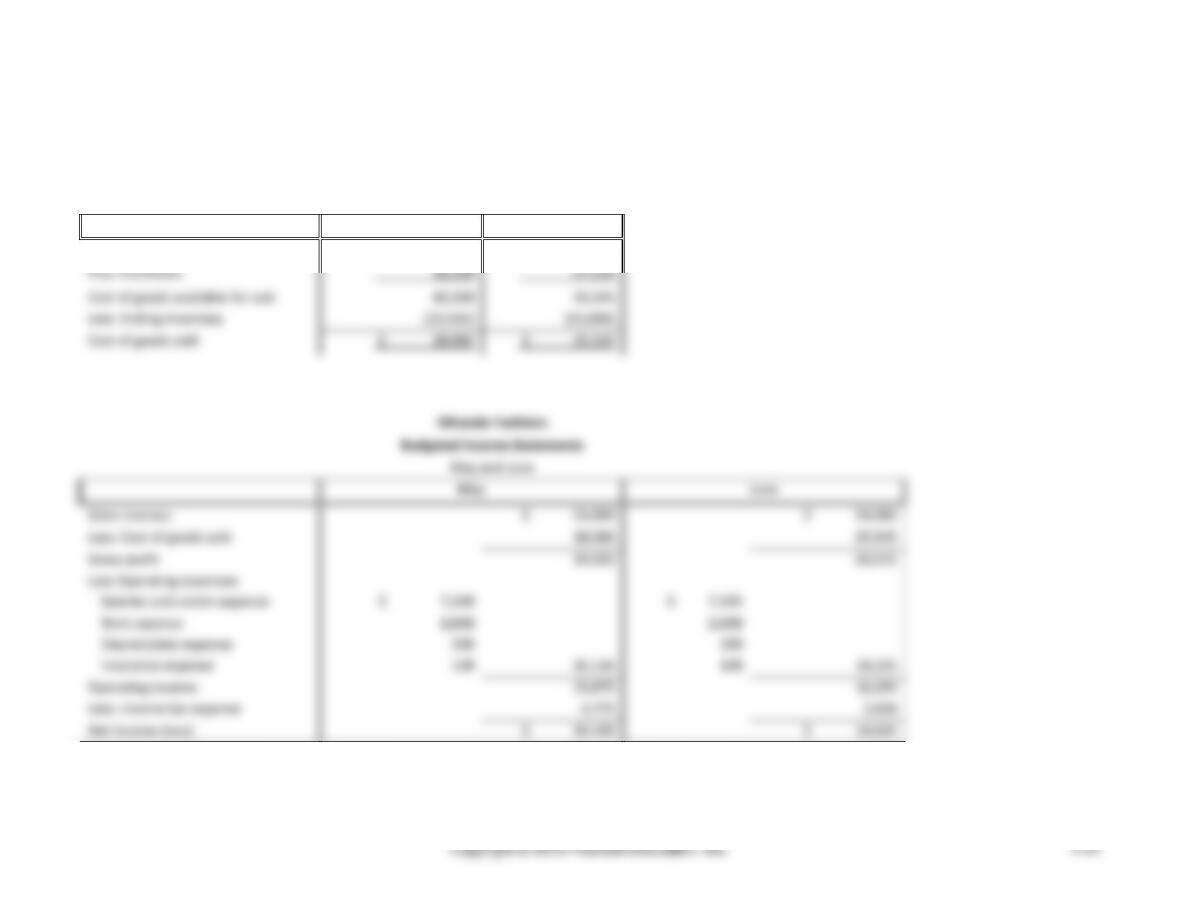

(30 min.) P9-56A

Miranda Fashions

Schedule of Cost of Goods Sold

May and June

May

June

Beginning inventory

$ 16,000

$ 23,515

Plus: Purchases

26,500

27,030

Cost of goods available for sale

42,500

50,545

Less: Ending inventory

(23,515)

(25,000)

Cost of goods sold

$ 18,985

$ 25,545

Miranda Fashions

Budgeted Income Statements

May and June

May

June

Sales revenue

$ 53,000

$ 54,060

Less: Cost of goods sold

18,985

25,545

Gross profit

34,015

28,515

Less Operating expenses:

Salaries and comm expense

$ 7,240

$ 7,325

Rent expense

2,600

2,600

Depreciation expense

200

200

Insurance expense

100

10,140

100

10,225

Operating income

23,875

18,290

Less: Income tax expense

4,775

3,658

Net income (loss)

$ 19,100

$ 14,632

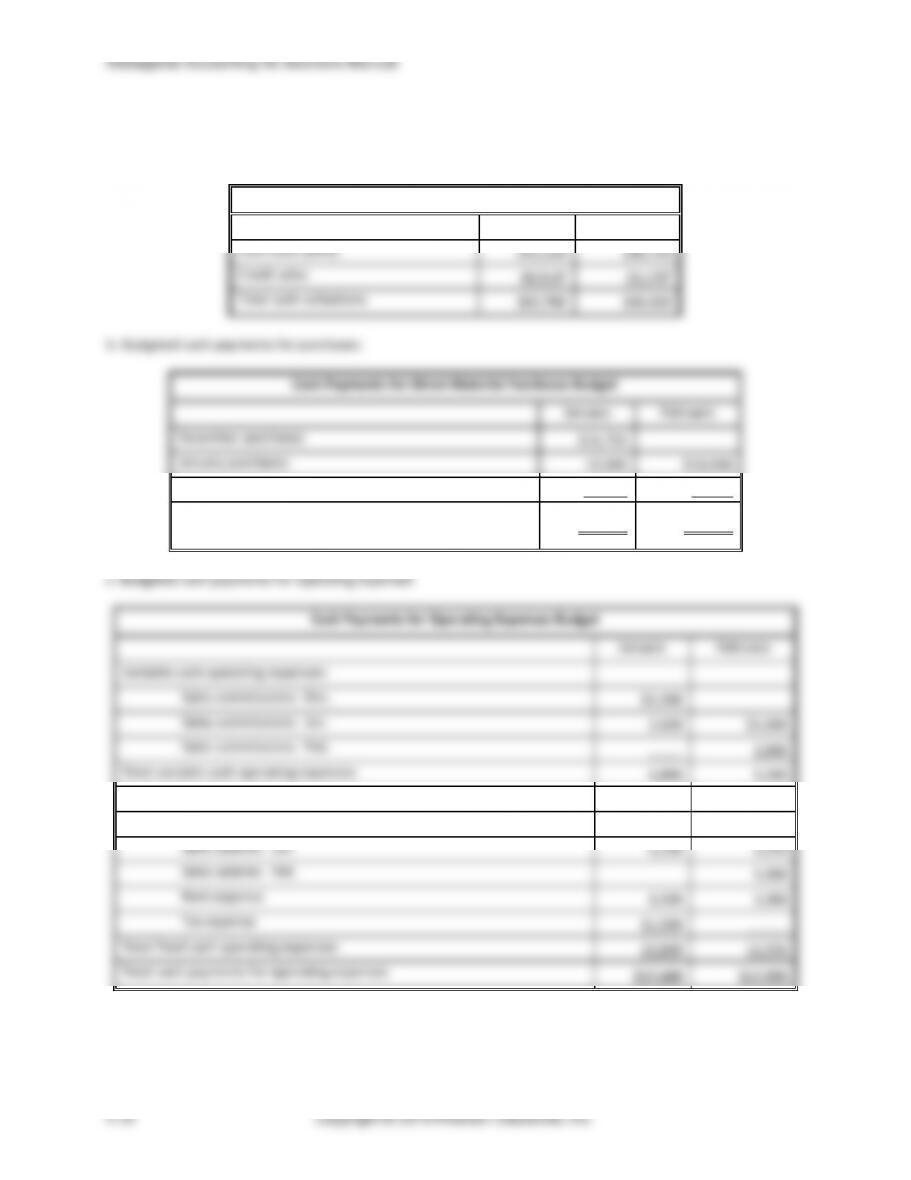

(30 min.) P9-57A

Req. 1

a. Budgeted cash collections:

Cash Collections Budget

January

February

Cash sales (65%)

$42,250

$46,150

Credit sales

20,510a

23,170b

Total cash collections

$62,760

$69,320

b. Budgeted cash payments for purchases:

Cash Payments for Direct Material Purchases Budget

January

February

December purchases

$11,750

January purchases

10,500

$10,500

February purchases

12,750

Total cash payments for direct material purchases

$22,250

$23,250

January

February

Variable cash operating expenses:

$2,280

$2,600

Total variable cash operating expenses

Fixed cash operating expenses:

11,500

Total fixed cash operating expenses

Chapter 9 The Master Budget

(continued) P9-57A

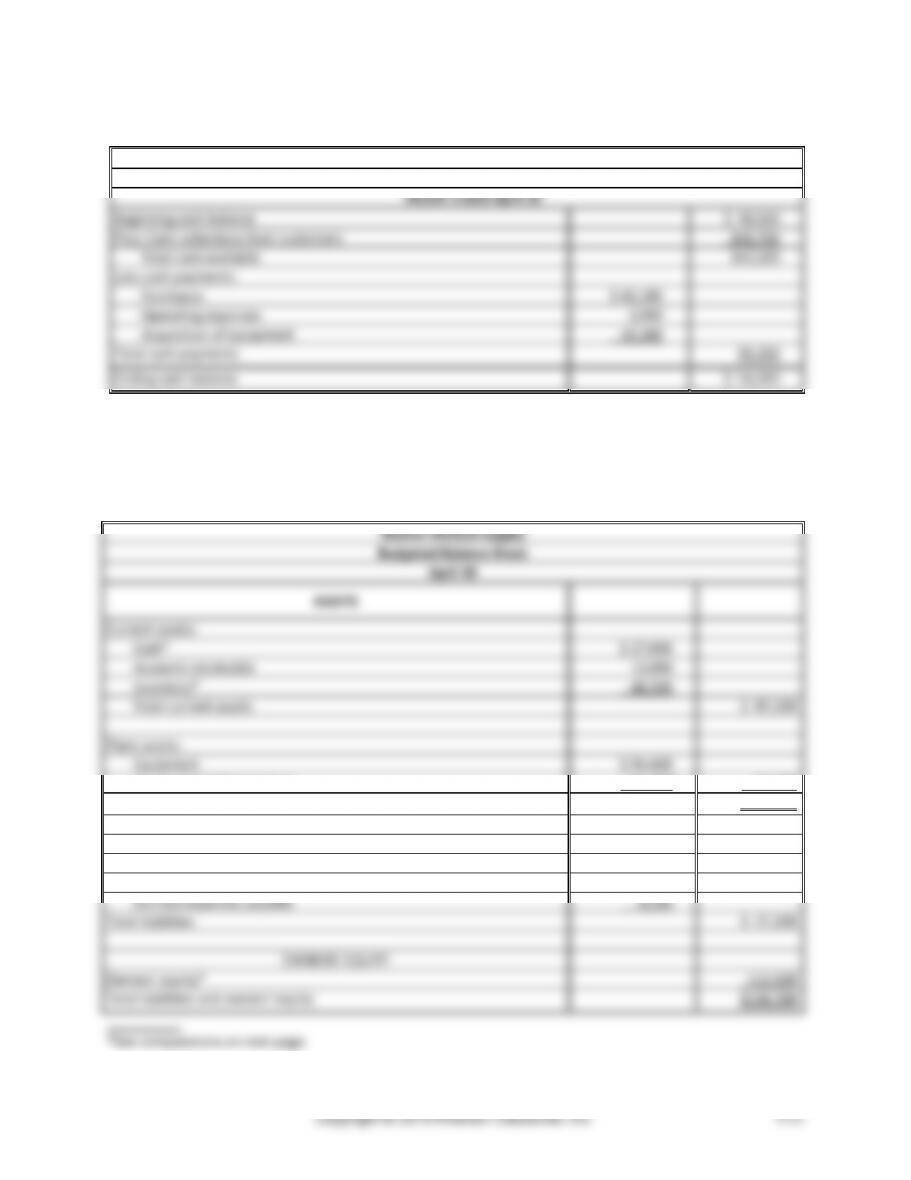

Req. 2

Combined Cash Budget

January

February

Cash balance, beginning

$23,000

$35,830

Add: cash collections (1a)

62,760

69,320

Total cash available

85,760

105,150

Less: cash payments

Direct material purchases (1b)

22,250

23,250

Operating expenses (1c)

27,680

17,990

Total cash payments

49,930

41,240

Ending cash balance

$35,830

$63,910

Managerial Accounting 4e Solutions Manual

(50-60 min.) P9-58A

Req. 1

Boxton Medical Supply

Budgeted Balance Sheet

April 30

ASSETS

Current assets:

Cash*

$51,000

Accounts receivable

18,000

Inventory*

34,800

Total current assets

$ 103,800

Plant assets:

Equipment

$94,400

Accumulated depreciation

(42,000)

52,400

Total assets

$156,200

LIABILITIES

Current liabilities:

Accounts payable

$18,100

Accrued expenses payable

9,100

Total liabilities

$ 27,200

OWNERS’ EQUITY

Owners’ equity*

129,000

Total liabilities and owners’ equity

$156,200

__________

Computations:

Cash:

Inventory:

Beginning balance……..

$ 40,500

Beginning balance ……………………..

$ 29,100

Cash sales

Purchases

54,000

46,200

Collections

47,700

Cost of goods sold

Ending balance …………………………..

(40,500)

$ 34,800

Payments of March 31

liabilities………………

(17,000)

Cash purchases…………

(10,000)

Payments for April (credit) purchases

(18,100)

Purchase of equipment

(42,200)

Operating expenses

(3,900)

Ending balance…………

$ 51,000

Chapter 9 The Master Budget

(continued) P9-58A

Req. 2

Boxton Medical Supply

Combined Cash Budget

Month Ended April 30

Beginning cash balance

$ 40,500

Plus: Cash collections from customers

101,700

Total cash available

142,200

Less cash payments:

Purchases

$ 45,100

Operating expenses

3,900

Acquisition of equipment

42,200

Total cash payments

91,200

Ending cash balance

$ 51,000

Req. 3

The amount of cash available for equipment purchases in April, before financing, if the minimum desired ending cash

balance is $19,000 (and disregarding the $42,200 initially budgeted for equipment purchases) is $74,200.

Req. 4

4a.

Boxton Medical Supply

Budgeted Balance Sheet

April 30

ASSETS

Current assets:

Cash*

$ 27,000

Accounts receivable

12,000

Inventory*

48,300

Total current assets

$ 87,300

Plant assets:

Equipment

$ 94,400

Accumulated depreciation

(42,000)

52,400

Total assets

$139,700

LIABILITIES

Current liabilities:

Accounts payable

$ 18,100

Accrued expenses payable

9,100

Total liabilities

$ 27,200

OWNERS’ EQUITY

Owners’ equity*

112,500

Total liabilities and owners’ equity

$139,700

__________

*See computations on next page.

Managerial Accounting 4e Solutions Manual

(continued) P9-58A

(4a. continued)

Computations:

Cash:

Inventory:

Beginning balance …………………………..

$ 40,500

Beginning balance….

$ 29,100

Cash sales

Purchases

36,000

46,200

Collections

41,700

Cost of goods sold

Ending balance………

(27,000)

$ 48,300

Payments of March 31

liabilities ……………………………………

(17,000)

Cash purchases ……………………………….

(10,000)

Payments for April

(credit) purchases

(18,100)

Purchase of equipment

(42,200)

Operating expenses

(3,900)

Ending balance ………………………………….

$ 27,000

costs. These costs remain the same whether sales are $90,000 or $60,000.

Because expenses do not decline as much as sales declines, income declines more rapidly than sales. In the original

analysis in Req. 1, income was $36,000. However, when sales decline to $60,000 in Req. 4, income declines to $19,500 .

This is a 45.8% decline in income.

(10-20 min) P9-59A

Cost of goods sold…

November

Copyright © 2015 Pearson Education, Inc.

9-55

(60 min.) P9-60B

Req. 1

Cash Collections

January

February

March

Quarter

Cash sales (35%)

$34,860

$41,580

$40,320

$116,760

Credit sales (65%)

$46,150a

$64,740b

$77,220c

$188,110

Total collections

$81,010

$106,320

$117,540

$304,870

a December credit sales: $71,000 x 65%

b January credit sales: $99,600 x 65%

c February credit sales: $118,800 x 65%

Req. 2

Production Budget

January

February

March

Quarter

Unit sales*

8,300

9,900

9,600

27,800

Plus: Desired ending inventory

990

960

900

900

Total needed

9,290

10,860

10,500

28,700

Less: Beginning inventory

(830)

(990)

(960)

(830)

Units to produce

8,460

9,870

9,540

27,870

*Hint: Unit sales = Sales in dollars ÷ Selling price per unit

Req. 3

Direct Materials Budget

January

February

March

Quarter

Units to be produced

8,460

9,870

9,540

27,870

Multiply by: Quantity of DM needed per unit

× 3.0

× 3.0

× 3.0

× 3.0

Quantity of DM needed for production

25,380

29,610

28,620

83,610

Plus: Desired ending inventory of DM

5,922

5,724

5,376

5,376

Total quantity of DM needed

31,302

35,334

33,996

88,986

Less: Beginning inventory of DM

(5,076)

(5,922)

(5,724)

(5,076)

Quantity of DM to purchase

26,226

29,412

28,272

83,910

Multiply by: Cost per pound

× $2.00

× $2.00

× $2.00

× $2.00

Total cost of DM purchases

$52,452

$58,824

$56,544

$167,820

Req. 4

Cash payments for Direct Material Purchases Budget

January

February

March

Quarter

December purchases

(From AP)

$43,000

$43,000

January purchases

$10,490 a

$41,962 b

$52,452

February purchases

$11,765c

$47,059d

$58,824

March purchases

$11,309e

$11,309

Total payments

$53,490

$53,727

$58,368

165,585

Managerial Accounting 4e Solutions Manual

(continued) P9-60B

Req. 5

Cash Payments for Direct Labor Budget

January

February

March

Quarter

Direct labor

$3,807

$4,442

$4,293

$12,542

Quarter

Rent (fixed)

Other MOH (fixed)

$2,900

overhead costs

Total disbursements

Variable operating expenses

Fixed operating expenses

Total disbursements

$14,175