Chapter 9 The Master Budget

(25−30 min.) E9-31A

Games Corporation

Budgeted Balance Sheet

March 31

ASSETS

Current Assets:

Casha

$ 6,400

Accounts receivable

3,175

Inventory

16,185

$25,760

Plant assets:

Furniture and fixtures

34,300

Accumulated depreciation ($29,830 + $900)

(30,730)

3,570

Total assets

$29,330

LIABILITIES

Current liabilities:

Accounts payable

$ 2,000

Total liabilities

$ 2,000

OWNERS’ EQUITY

Stockholders’ equityb

27,330

Total liabilities and owners’ equity

$29,330

14,100

$27,330

Managerial Accounting 4e Solutions Manual

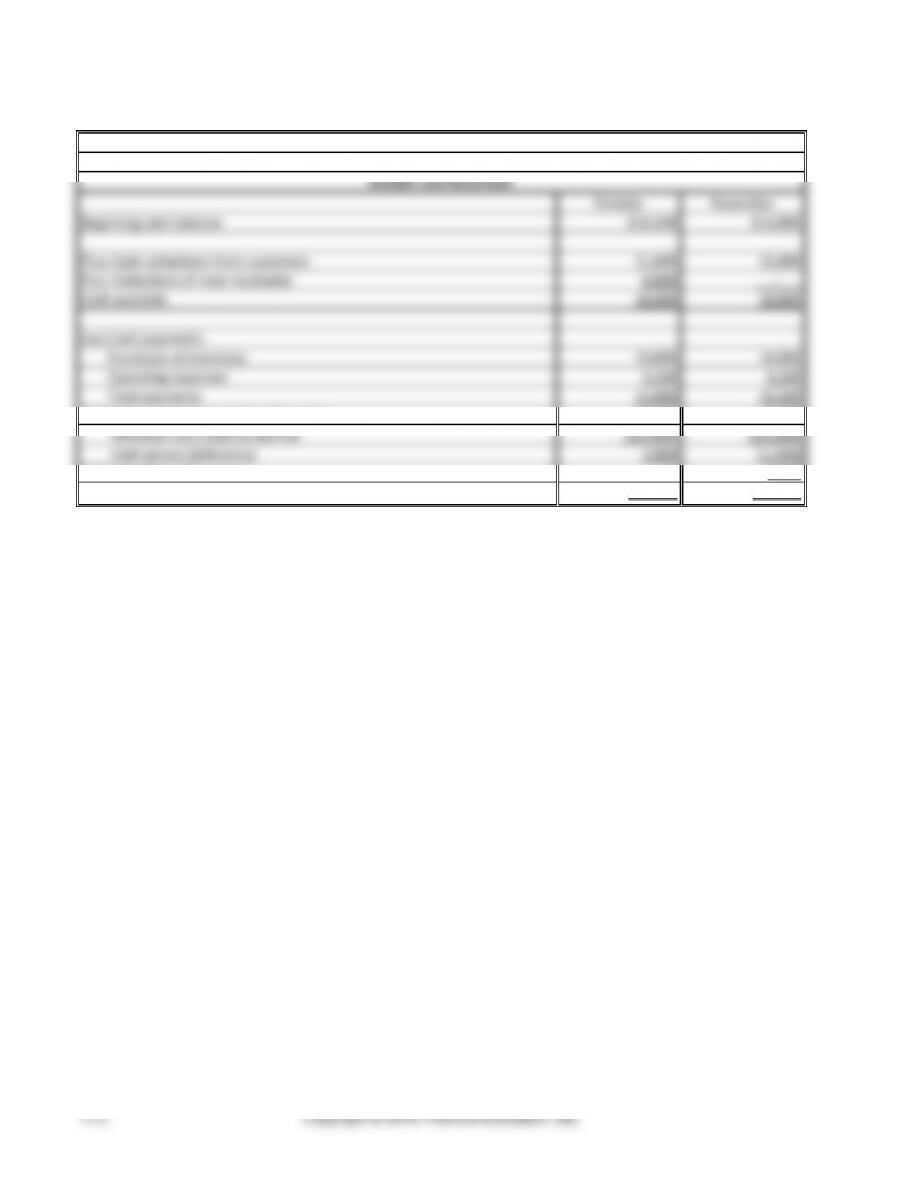

(15−20 min.) E9-32A

Flash Medical Supply

Cash Budget

October and November

October

November

Beginning cash balance

$10,200

$13,000

Plus: Cash collections from customers

11,800

15,800

Plus: Collections of note receivable

6,000

–

Cash available

28,000

28,800

Less Cash payments:

Purchases of inventory

10,800

14,900

Operating expenses

4,200

4,200

Total payments

15,000

19,100

(1) Ending cash balance before financing

13,000

9,700

Minimum cash balance desired

(11,000)

(11,000)

Cash excess (deficiency)

2,000

(1,300)

(2) Total effect of financing

-0-

2,000

Ending cash balance, (1) + (2)

$13,000

$11,700

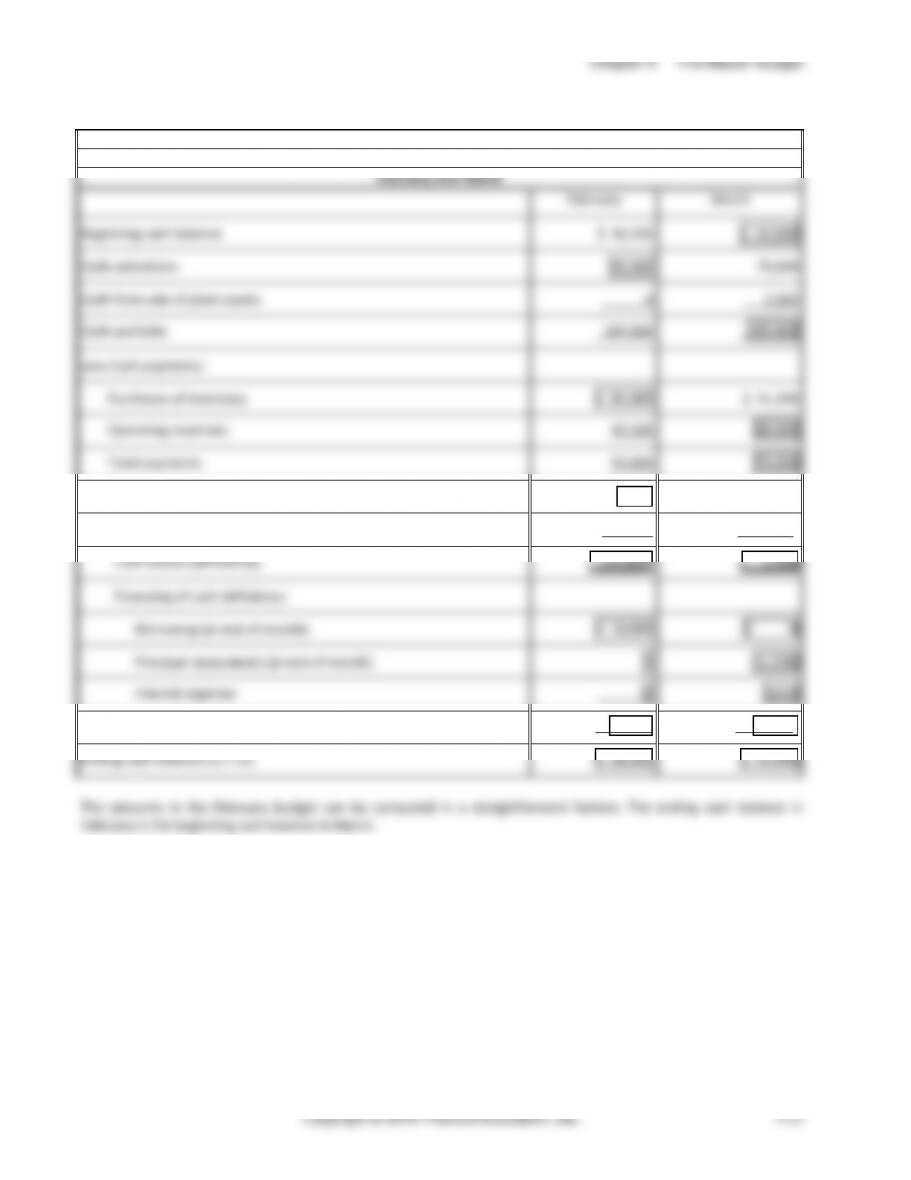

(20 min.) E9-33A

Backyard Adventures

Cash Budget

February and March

February

March

Beginning cash balance

$ 16,500

$ 24,000

Cash collections

90,500

79,600

Cash from sale of plant assets

0

2,000

Cash available

107,000

105,600

Less Cash payments:

Purchases of inventory

$ 50,300

$ 41,200

Operating expenses

47,500

38,000

Total payments

97,800

79,200

(1) Ending cash balance before financing

9,200

26,400

Less: Minimum cash balance desired

(24,000)

(24,000)

Cash excess (deficiency)

(14,800)

2,400

Financing of cash deficiency:

Borrowing (at end of month)

$ 14,800

$ 0

Principal repayments (at end of month)

0

(2,208)

Interest expense

0

(192)

(2) Total effects of financing

14,800

(2,400)

Ending cash balance (1) + (2)

$ 24,000

$ 24,000

The amounts in the February budget can be computed in a straightforward fashion. The ending cash balance in

February is the beginning cash balance in March.

Managerial Accounting 4e Solutions Manual

(15-20 min.) E9-34A

Scannell Readers

Inventory, Purchases, and Cost of Goods Sold Budget

Nine Months Ended September 30

QUARTER ENDED

NINE-MONTH

March 31

June 30

Sept.30

TOTAL

Cost of goods sold:

(0.60 × $130,000)

$ 78,000

(0.60 × $180,000)

$ 108,000

(0.60 × $155,000)

$ 93,000

$279,000

Plus: Desired ending inventory

[$10,000 + (0.10 × $108,000)]

20,800

[$10,000 + (0.10 × $93,000)]

19,300

[$10,000 + (0.10 × 0.60 × $230,000)]

23,800

Total inventory required

98,800

127,300

116,800

Less: Beginning inventory

(18,000)

(20,800)

(19,300)

Amount of inventory to purchase

$ 80,800

$ 106,500

$ 97,500

Quarter 2

Quarter 3

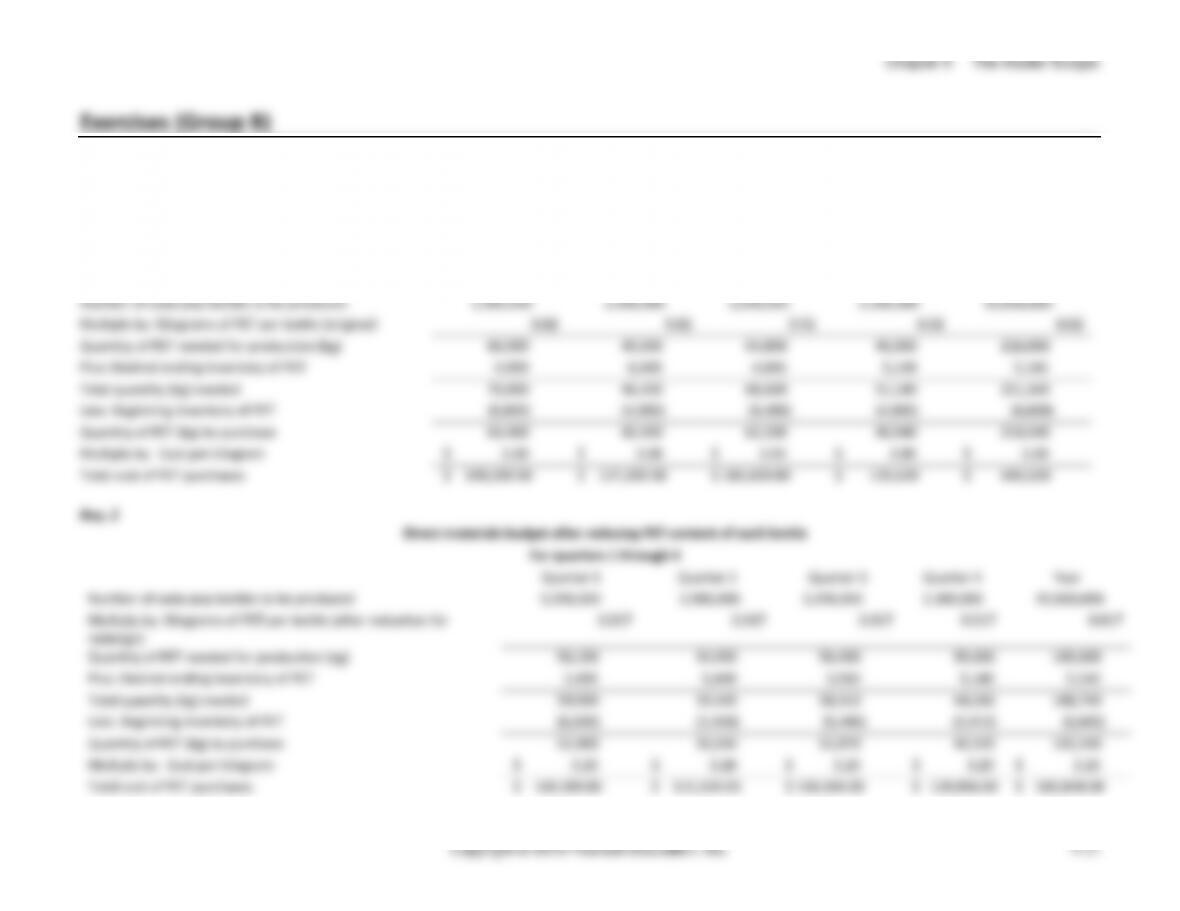

(10-15 min.) E9-35B

Req. 1

Direct materials budget before any changes

For quarters 1 through 4

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Number of soda pop bottles to be produced

3,300,000

2,000,000

3,200,000

2,300,000

10,800,000

Multiply by: Kilograms of PET per bottle (original)

0.02

0.02

0.02

0.02

0.02

Quantity of PET needed for production (kg)

66,000

40,000

64,000

46,000

216,000

Plus: Desired ending inventory of PET

4,000

6,400

4,600

5,140

5,140

Total quantity (kg) needed

70,000

46,400

68,600

51,140

221,140

Less: Beginning inventory of PET

(6,600)

(4,000)

(6,400)

(4,600)

(6,600)

Quantity of PET (kg) to purchase

63,400

42,400

62,200

46,540

214,540

Multiply by: Cost per kilogram

$ 3.00

$ 3.00

$ 3.00

$ 3.00

$ 3.00

Total cost of PET purchases

$ 190,200.00

$ 127,200.00

$ 186,600.00

$ 139,620

$ 643,620

Managerial Accounting 4e Solutions Manual

(continued) E9-35B

Req. 3

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Savings from reducing PET content of each bottle

$ 20,920

$ 11,872

$ 17,416

$ 10,564

$ 60,772

Total savings for the year

$ 60,772

Cost of retrofitting the molds

$ 59,862

Net savings (cost) of retrofitting – first year

$ 910

Savings each year AFTER the first year

$ 60,772

Chapter 9 The Master Budget

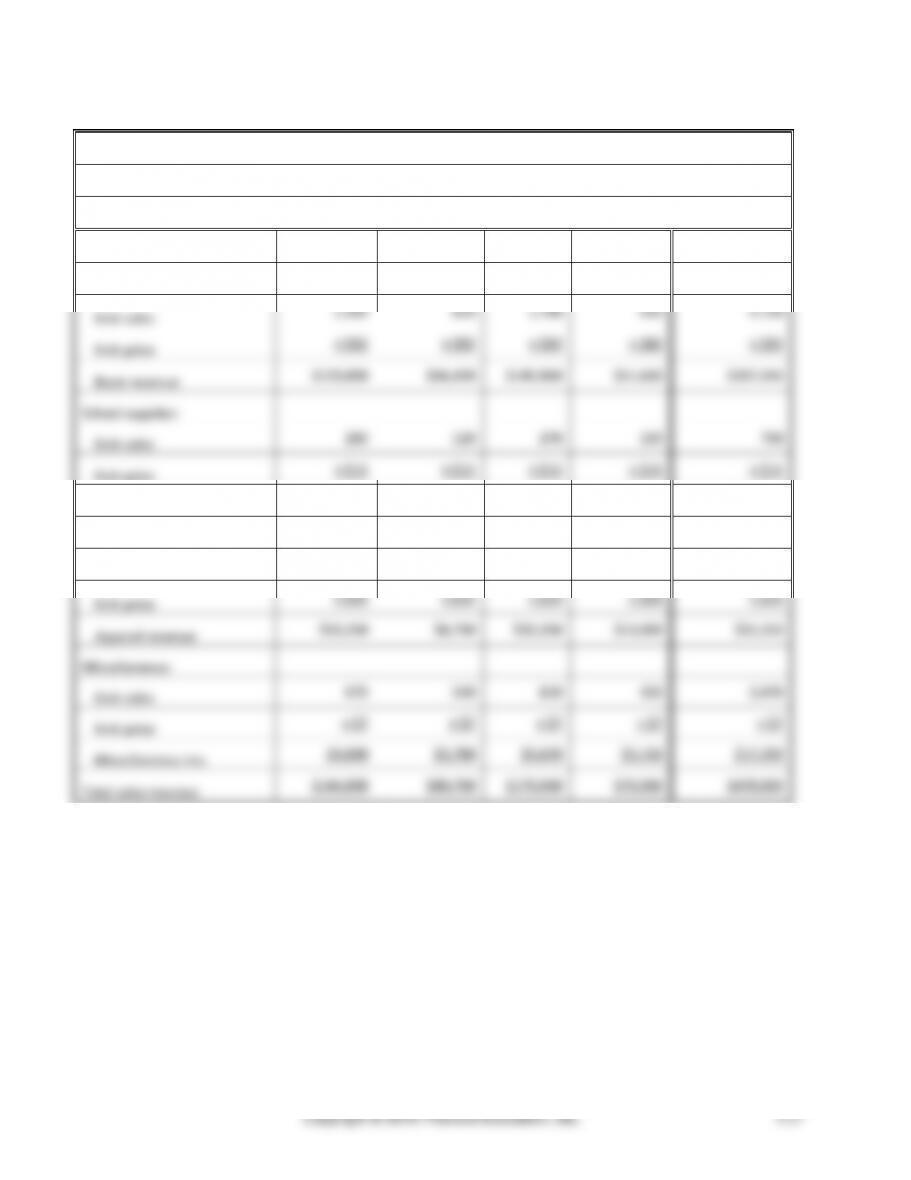

(10 min.) E9-36B

Albany College Bookstore

Sales Budget

For the Upcoming Year

Q1

Q2

Q3

Q4

Year

Books:

Unit sales

1,500

810

1,780

630

4,720

Unit price

× $82

× $82

× $82

× $82

× $82

Book revenue

$123,000

$66,420

$145,960

$51,660

$387,040

School supplies:

Unit sales

210

120

270

150

750

Unit price

× $15

× $15

× $15

× $15

× $15

School supplies rev.

$3,150

$1,800

$4,050

$2,250

$11,250

Apparel:

Unit sales

530

350

810

520

2,210

Unit price

× $25

× $25

× $25

× $25

× $25

Apparel revenue

$13,250

$8,750

$20,250

$13,000

$55,250

Miscellaneous:

Unit sales

670

540

810

450

2,470

Unit price

× $7

× $7

× $7

× $7

× $7

Miscellaneous rev.

$4,690

$3,780

$5,670

$3,150

$17,290

Total sales revenue

$144,090

$80,750

$175,930

$70,060

$470,830

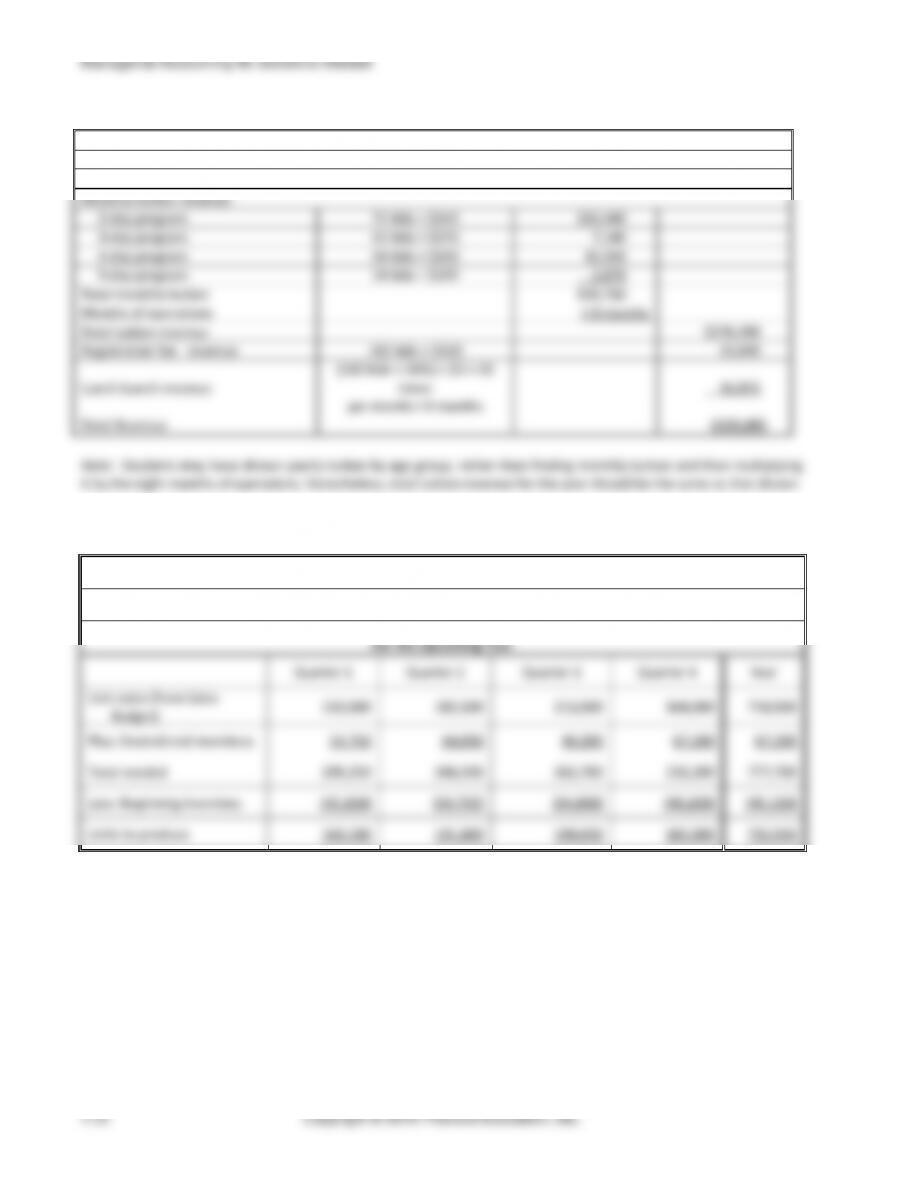

(10-20 min.) E9-37B

Geary Preschool

Budgeted Revenue

For Year Ended XXXX

Monthly tuition revenue:

2-day program

72 kids × $145

$10,440

3-day program

42 kids × $170

7,140

4-day program

54 kids × $190

10,260

5-day program

14 kids × $205

2,870

Total monthly tuition

$30,710

Months of operations

× 9 months

Total tuition revenue

$276,390

Registration fee revenue

182 kids × $120

21,840

Lunch bunch revenue

(182 kids × 50%) × $3 × 15

times

per month × 9 months

36,855

Total Revenue

$335,085

Note: Students may have shown yearly tuition by age group, rather than finding monthly tuition and then multiplying

it by the eight months of operations. Nonetheless, total tuition revenue for the year should be the same as that shown.

(10-15 min.) E9-38B

Ringer Foods

Production Budget

For the Upcoming Year

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Unit sales (from Sales

Budget)

150,500

182,500

213,500

164,000

710,500

Plus: Desired end inventory

54,750

64,050

49,200

67,200

67,200

Total needed

205,250

246,550

262,700

231,200

777,700

Less: Beginning inventory

(45,150)

(54,750)

(64,050)

(49,200)

(45,150)

Units to produce

160,100

191,800

198,650

182,000

732,550

Chapter 9 The Master Budget

(5 min.) E9-39B

Gable Industries

Direct Materials Budget

For the Months of January through March

January

February

March

Quarter

Units to be produced (from Production Budget)

5,300

4,100

4,200

13,600

Multiply by: Quantity of DM needed per unit

× 2

× 2

× 2

× 2

Quantity needed for production

10,600

8,200

8,400

27,200

Plus: Desired end inventory of DM

1,640

1,680

1,680

2,120

Total quantity needed

12,240

9,880

10,240

29,040

Less: Beginning Inventory of DM

(2,120)

(1,640)

(1,680)

(2,120)

Quantity to purchase

10,120

8,240

8,560

26,920

Multiply by: Cost per unit

× $1.00

× $1.00

× $1.00

× $1.00

Total cost of DM purchases

$10,120

$8,240

$8,560

$26,920

Managerial Accounting 4e Solutions Manual

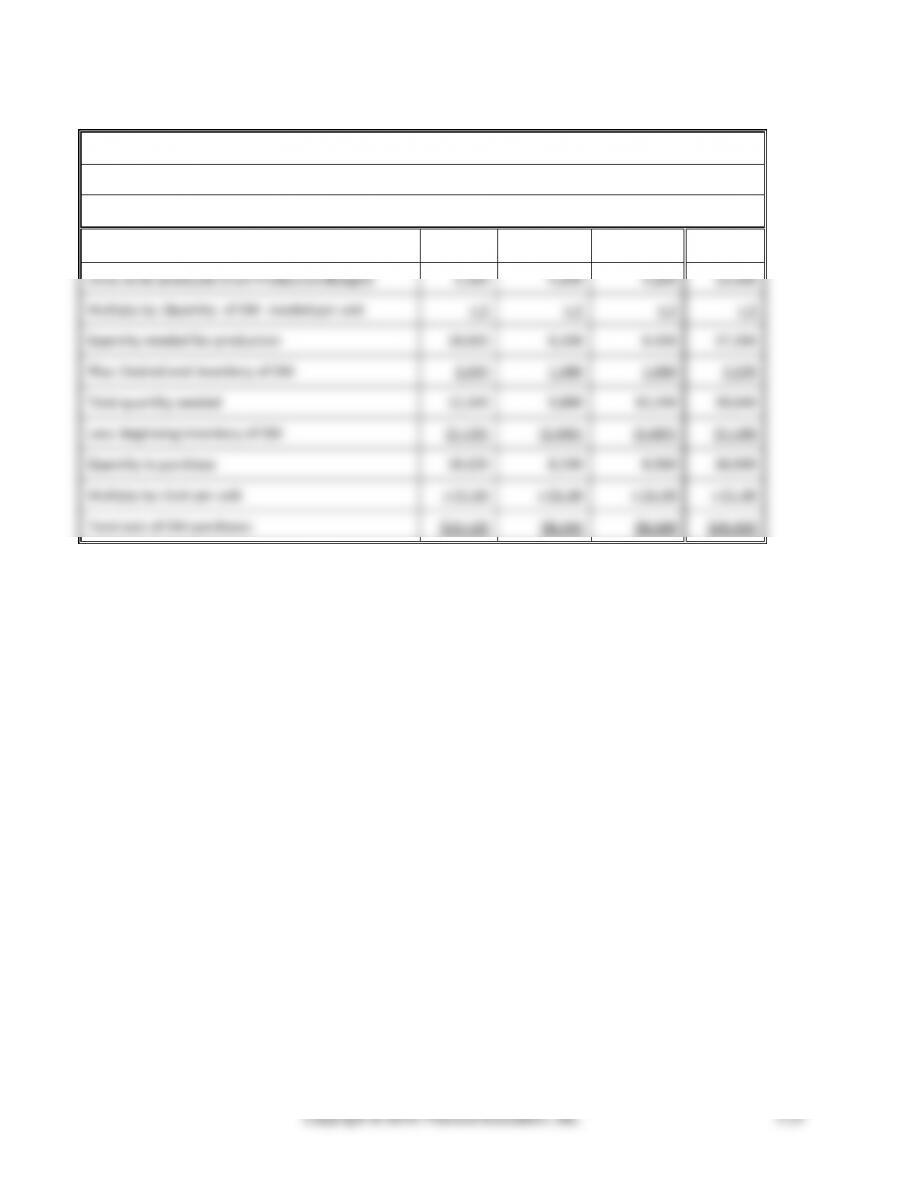

(5 min.) E9-40B

Req. 1

Hoffman Manufacturing

Production Budget

For the Months of January through March

January

February

March

Quarter

Unit sales

3,000

3,200

3,100

9,300

Plus: Desired end inventory

(25% of next month’s unit sales)

800

775

1,050

1,050

Total needed

3,800

3,975

4,150

10,350

Less: Beginning inventory

(750)

(800)

(775)

(750)

Units to produce

3,050

3,175

3,375

9,600

Req. 2

Hoffman Manufacturing

Direct Materials Budget

For the Months of January through March

January

February

March

Quarter

Units to be produced

(from Production Budget)

3,050

3,175

3,375

9,600

Multiply by: Quantity (lbs.) of DM needed

per unit

× 2

× 2

× 2

× 2

Quantity (lbs.) needed for production

6,100

6,350

6,750

19,200

Desired End Inventory of DM (20% of the

amount needed for next month’s

production)

1,270

1,350

1,660

1,660

Total Quantity (lbs.) Needed

7,370

7,700

8,410

20,860

Less: Beginning Inventory of DM

(1,220)

(1,270)

(1,350)

(1,220)

Quantity (lbs.) to purchase

6,150

6,430

7,060

19,640

Multiply by: Cost per pound

× $0.20

× $0.20

× $0.20

× $0.20

Total Cost of DM purchases

$1,230

$1,286

$1,412

$3,928

Chapter 9 The Master Budget

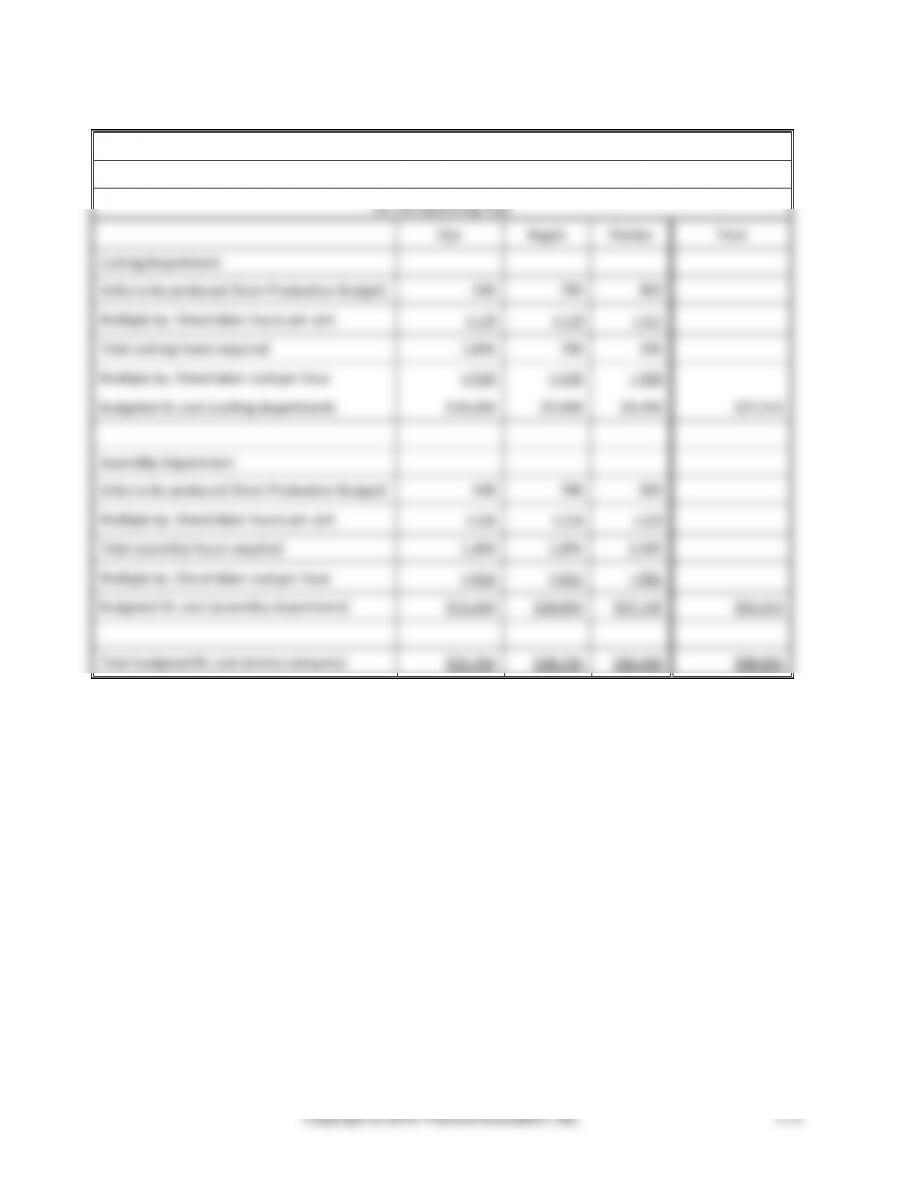

(15 min.) E9-41B

Cleary Industries

Direct Labor Budget

For the Upcoming Year

Zips

Regals

Flashes

Total

Cutting Department

Units to be produced (from Production Budget)

540

790

850

Multiply by: Direct labor hours per unit

× 1.9

× 1.0

× 1.1

Total cutting hours required

1,026

790

935

Multiply by: Direct labor cost per hour

× $10

× $10

× $10

Budgeted DL cost (cutting department)

$10,260

$7,900

$9,350

$27,510

Assembly Department

Units to be produced (from Production Budget)

540

790

850

Multiply by: Direct labor hours per unit

× 2.6

× 2.4

× 2.9

Total assembly hours required

1,404

1,896

2,465

Multiply by: Direct labor cost per hour

× $11

× $11

× $11

Budgeted DL cost (assembly department)

$15,444

$20,856

$27,115

$63,415

Total budgeted DL cost (entire company)

$25,704

$28,756

$36,465

$90,925

(5 min.) E9-42B

The Henry Company

Manufacturing Overhead Budget

For the Upcoming Year

Projected Sales (from Sales Budget)

45,000

Variable MOH costs:

Indirect materials ($1.00 per unit)

$ 45,000

Supplies ($0.80 per unit)

36,000

Indirect labor ($0.40 per unit)

18,000

Plant utilities ($0.10 per unit)

4,500

Repairs and maintenance ($0.50 per unit)

22,500

Total Variable MOH

$ 126,000

Fixed MOH costs:

Indirect labor

64,000

Plant utilities

34,000

Repairs and maintenance

11,000

Depreciation on plant and equipment

48,000

Insurance on plant and equipment

27,000

Plant supervision

60,000

Total Fixed MOH

$ 244,000

Total MOH

$ 370,000

Chapter 9 The Master Budget

(20-30 min.) E9-43B

Req. 1

Greatland Preschool

Budgeted Monthly Operating Expenses

Teachers’ salary:

2-day program

9 teachers × $430 per month

$3,870

3-day program

2 teachers × $654 per month

1,308

4-day program

7 teachers × $868 per month

6,076

5-day program

3 teachers × $1,060 per month

3,180

Director salary

1,350

Total salary expense

$15,784

Payroll tax expense

$15,784 × 7.65%

1,207

Lease expense

4,040

Fixed operating expenses

940

Variable operating expenses

160 * 11

1,760

Total monthly operating

expenses

$23,731

Req. 2

Greatland Preschool

Budgeted Income Statement

For Year Ended XXXX

Tuition, registration fees, and lunch bunch revenue

$ 246,400

Less: Operating expenses ($23,731a × 9 months)

(213,579)

Operating income

$ 32,821

__________

a from Req. 1

Req. 3

From the budgeted income statement, Greatland learns that it has projected operating income for the year. Since

Greatland is a not-for-profit preschool, it is not in business to generate income for its owners. Rather, Greatland may

be able to further its organizational goals with the projected income. For example, it may decide to use the income for

any of the following purposes:

• Invest in additional (or better) classroom equipment

• Invest in additional (or better) playground equipment

• Improve the current program (more crafts, books, better curriculum, special guest visitors, special programs,

field trips, etc.)

(5 min.) E9-44B

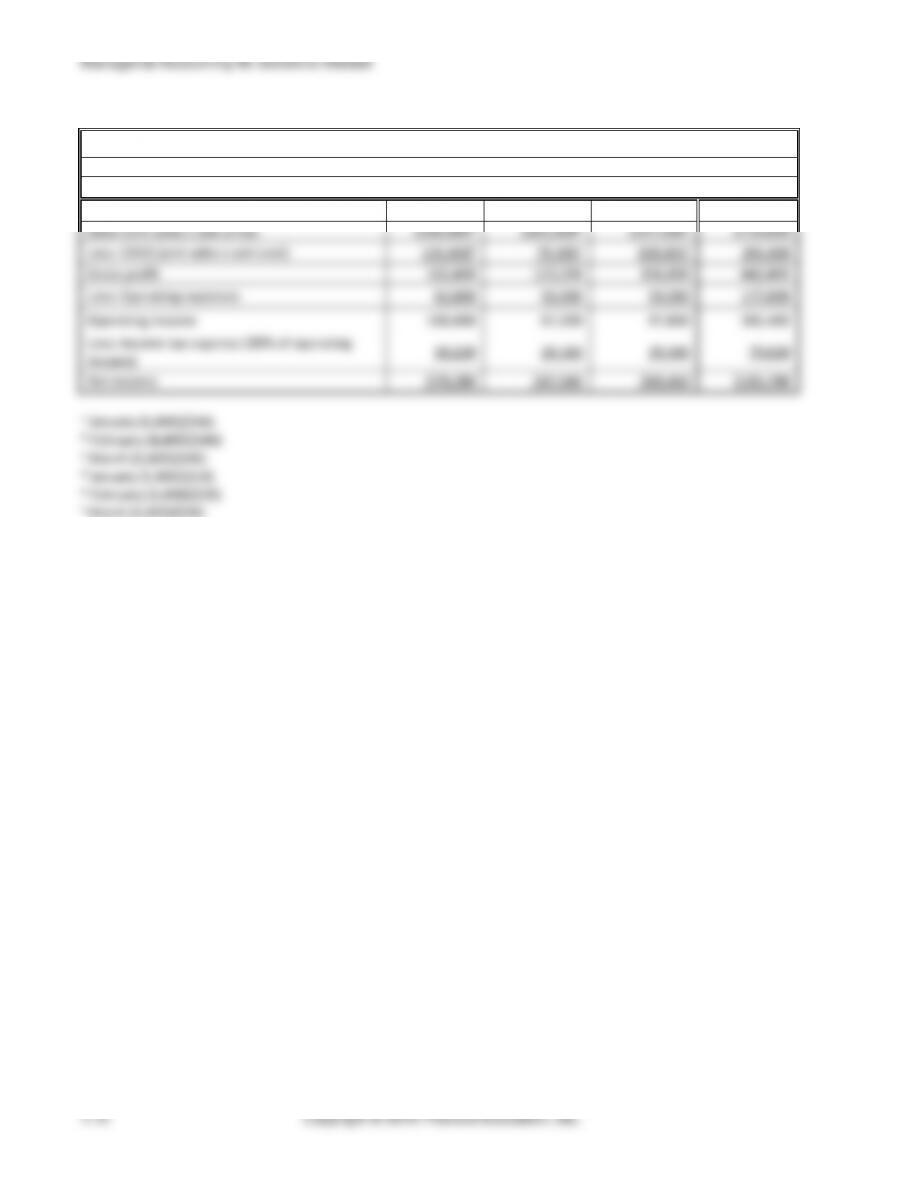

Rossdale Labs

Budgeted Income Statement

For the Quarter Ended March 31

Jan.

Feb.

March

Quarter

Sales (unit sales x sale price)

$266,800a

$202,400b

$257,600c

$726,800

Less: COGS (unit sales x unit cost)

104,400d

79,200e

100,800f

284,400

Gross profit

162,400

123,200

156,800

442,400

Less: Operating expenses

62,000

56,000

59,000

177,000

Operating income

100,400

67,200

97,800

265,400

Less: Income tax expense (30% of operating

income)

30,120

20,160

29,340

79,620

Net income

$70,280

$47,040

$68,460

$185,780

a January (5,800)($46)

b February (4,400)($46)

c March (5,600)($46)

d January (5,800)($18)

e February (4,400)($18)

f March (5,600)($18)

Chapter 9 The Master Budget

(5 min.) E9-45B

Samson Motors

Budgeted Income Statement

For the Upcoming Year

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Sales

$ 4,494,000

$ 4,583,880

$ 4,721,396

$ 5,004,680

$ 18,803,957

Less: Cost of goods sold

2,022,300

2,062,746

2,124,628

2,252,106

8,461,780

Gross profit

$ 2,471,700

$ 2,521,134

$ 2,596,768

$ 2,752,574

$ 10,342,176

Less: Operating expenses

898,800

916,776

1,416,419

1,751,638

4,983,633

Operating income

$ 1,572,900

$ 1,604,358

$ 1,180,349

$ 1,000,936

$ 5,358,543

Calculations:

Given in exercise

$ of amount of

increase (% x Total

sales prior period)

Total Sales

Base sales

$ 4,200,000

% increase Quarter 1

7%

$ 294,000

$ 4,494,000

% increase Quarter 2

2%

$ 89,880

$ 4,583,880

% increase Quarter 3

3%

$ 137,516

$ 4,721,396

% increase Quarter 4

6%

$ 283,284

$ 5,004,680

Given in exercise

Sales in Quarter

Operating

Expenses

% operating expenses in Qtr 1

20%

$ 4,494,000

$ 898,800

% operating expenses in Qtr 2

20%

$ 4,583,880

$ 916,776

% operating expenses in Qtr 3

30%

$ 4,721,396

$ 1,416,419

% operating expenses in Qtr 4

35%

$ 5,004,680

$ 1,751,638

Managerial Accounting 4e Solutions Manual

(5 min.) E9-46B

General Corporation

Cash Collections Budget

For the Months of January through March

January

February

March

Quarter

Cash Sales (40%)

$58,000

$46,000

$70,000

Collections on Credit Sales (60%):

25% of credit sales made in current

month

21,750a

17,250b

26,250c

50% of credit sales made one month

ago

33,000d

43,500e

34,500f

15% of credit sales made two

months ago

7,650g

9,900h

13,050i

Total Cash Collections

$120,400

$116,650

$143,800

$380,850

a 145,000 x 60% x 25%

b 115,000 x 60% x 25%

c 175,000 x 60% x 25%

d 110,000 x 60% x 50%

e 145,000 x 60% x 50%

f 115,000 x 60% x 50%

g 85,000 x 60% x 15%

h 110,000 x 60% x 15%

I 145,000 x 60% x 15%

(5 min.) E9-47B

Bauer Corporation

Cash Payments Budget

For the Months of April through June

April

May

June

Quarter

Cash Payments for DM:

Current month purchases (50%)

$65,000

$63,000

$72,000

$200,000

Prior month’s purchases (50%)

59,500

65,000

63,000

187,500

Cash Payments for DL

52,000

62,000

77,000

191,000

Cash Payments for MOHa

44,200

60,200

84,200

188,600

Cash Payments for Operating Expensesb

57,100

71,100

74,100

202,300

Cash Payment for New Server

0

7,000

0

7,000

Cash Payment for Taxes

0

0

13,500

13,500

Total Cash Payments

$277,800

$328,300

$383,800

$989,900

a Depreciation is a non-cash expense and is not included in the MOH cash payments.

b Depreciation and bad debt expense are non-cash expenses and are not included in the operating expenses cash

payments.

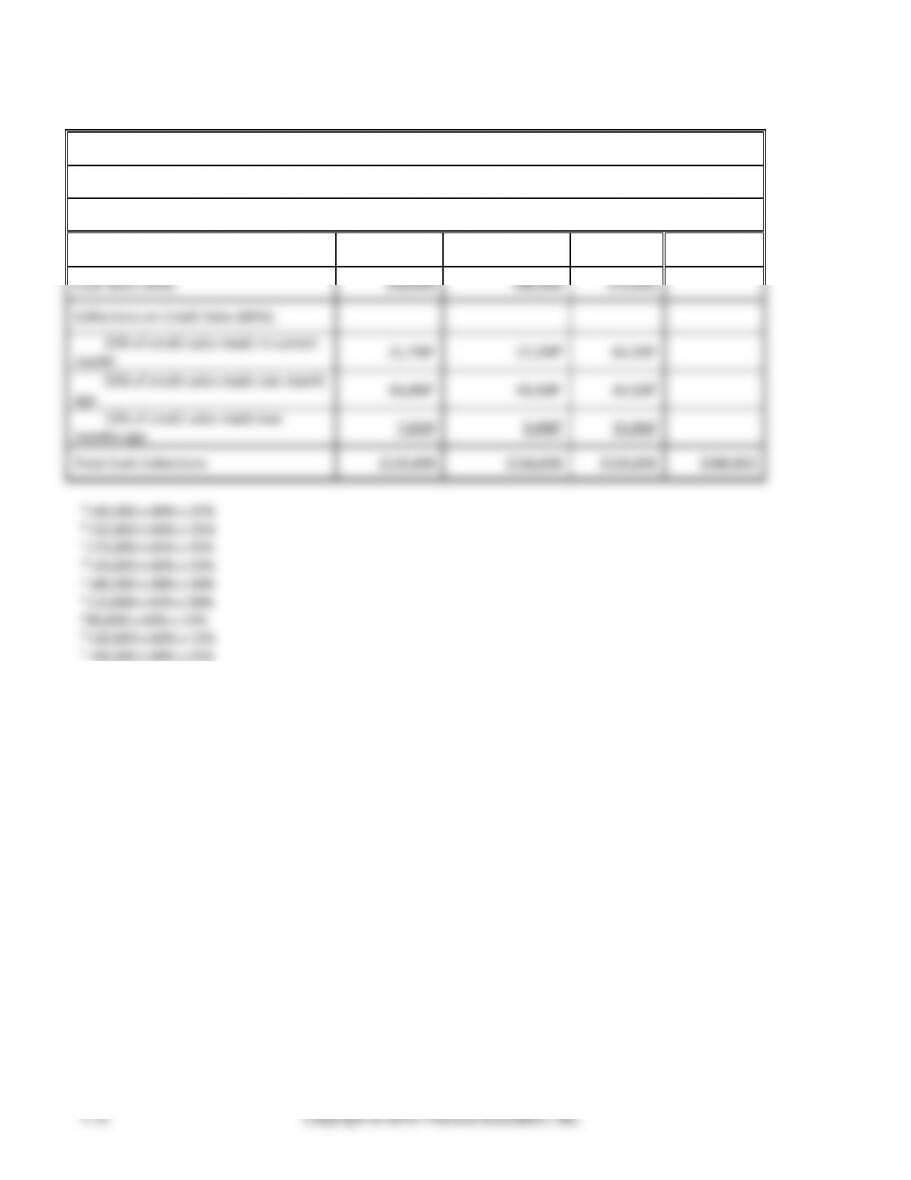

(5 min.) E9-48B

Mission Health Center

Combined Cash Budget

For the Months of July through September

July

August

Sept.

Quarter

Beginning balance of cash

$30,000

$22,000

$30,890

$30,000

Plus: Cash collections

96,000

150,000

127,000

373,000

Total cash available

126,000

172,000

157,890

403,000

Less: Cash payments

(141,000)

(103,000)

(138,000)

(382,000)

End cash balance before financing

(15,000)

69,000

19,890

21,000

Financing:

Borrowings

37,000

0

2,110

39,110

Repayments

0

(37,000)

0

(37,000)

Interest Payments

0

(1,110)a

0

(1,110)

End Cash Balance

$22,000

$30,890

$22,000

$22,000

a 37,000 x 3% x 3 months = $1,110

Managerial Accounting 4e Solutions Manual

(20-30 min.) E9-49B

Req. 1

Sales Budget

Serdnic Reeds

Sales Budget

October

November

December

January

Cash Sales (20%)

$179,200

$193,200

$ 213,000

$186,800

Credit Sales (80%)

716,800

772,800

852,000

747,200

Total sales

$896,000

$966,000

$1,065,000

$934,000

Req. 2

Cash Collections Budget

Serdnic Reeds

Budgeted Cash Collections from Customers

December

January

Cash sales (20% of current month

total sales)

$213,000

$186,800

Collection of credit sales:

25% of current month credit sales

213,000a

186,800d

60% of prior month credit sales

463,680b

511,200e

14% of credit sales two months ago

100,352c

108,192f

Total collection of credit sales

777,032

806,192

Total cash collections

$990,032

$992,992

__________

a December credit sales: $852,000 × 0.25

b November credit sales: $772,800 × 0.60

cOctober credit sales: $716,800 × 0.14

dJanuary credit sales: $747,200 × 0.25

eDecember credit sales: $852,000 × 0.60

f November credit sales: $772,800 × 0.14

Chapter 9 The Master Budget

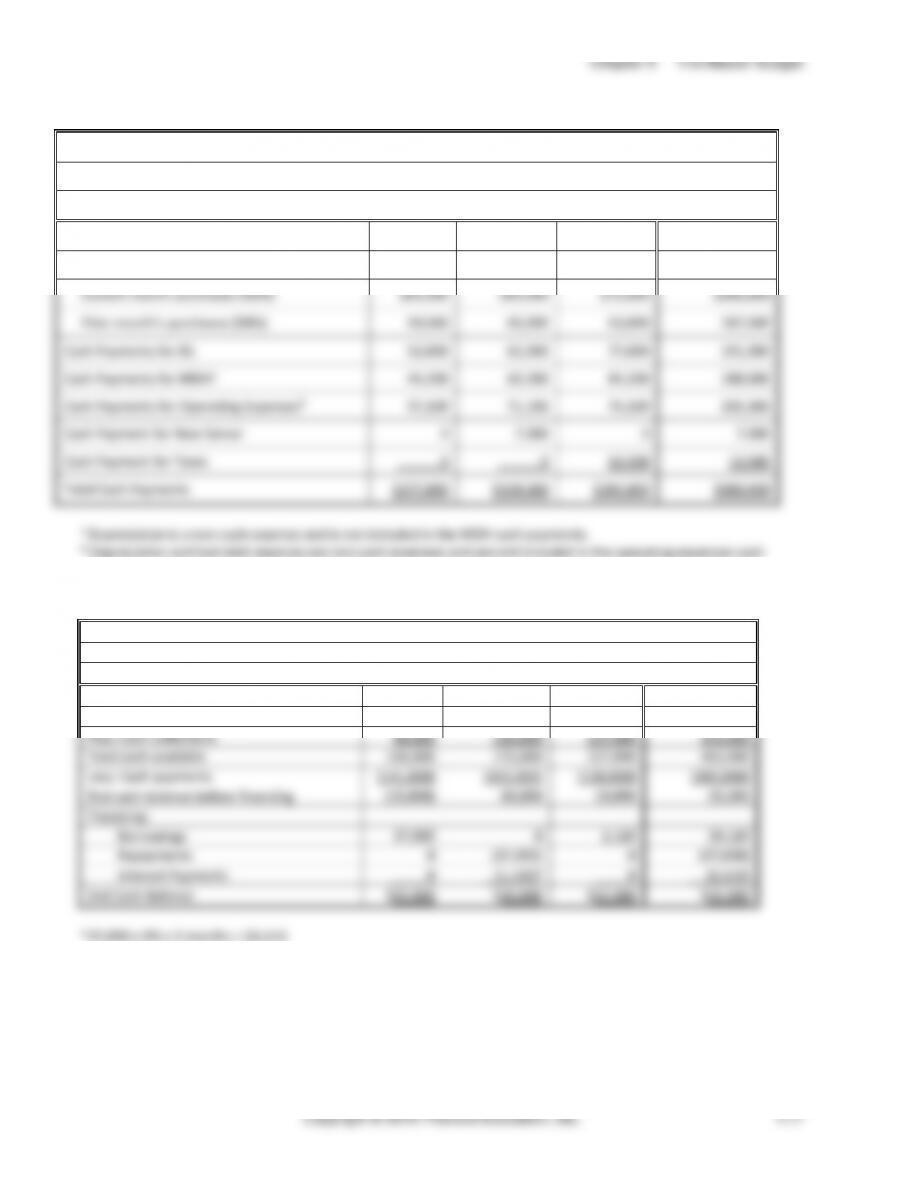

(25−30 min.) E9-50B

Marine Corporation

Budgeted Balance Sheet

March 31

ASSETS

Current Assets:

Casha

$ 9,500

Accounts receivable (0.25 × $12,500)

3,125

Inventory

15,085

$27,710

Plant assets:

Furniture and fixtures

34,500

Accumulated depreciation ($29,880 + $500)

(30,380)

4,120

Total assets

$31,830

LIABILITIES

Current liabilities:

Accounts payable

$ 1,700

Total liabilities

$ 1,700

OWNERS’ EQUITY

Owners’ equityb

30,130

Total liabilities and owners’ equity

$31,830

$28,630

14,300

Managerial Accounting 4e Solutions Manual

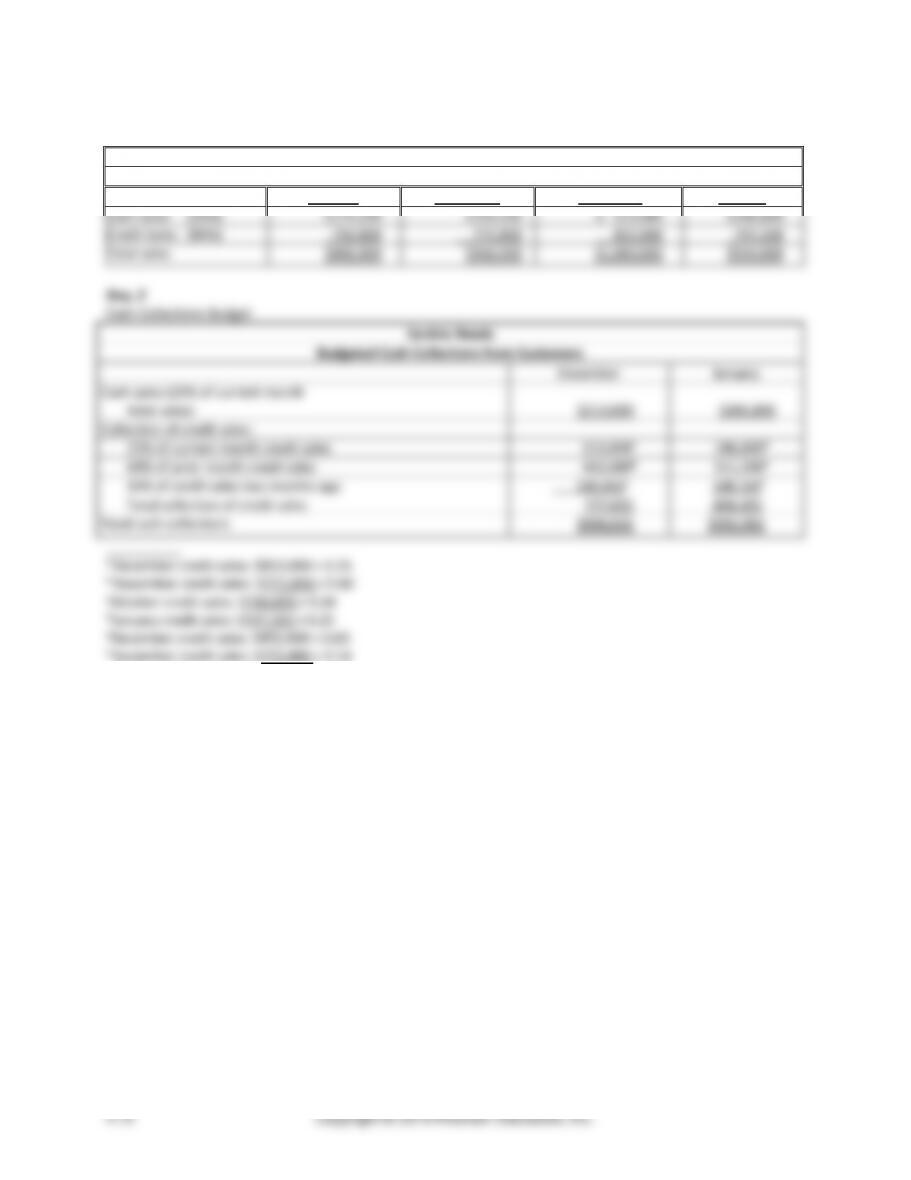

(15−20 min.) E9-51B

Speedy Medical Supply

Cash Budget

October and November

October

November

Beginning cash balance

$10,600

$13,000

Plus: Cash collections from customers

11,400

14,200

Plus: Collections of note receivable

7,000

–

Cash available

29,000

27,200

Less Cash payments:

Purchases of inventory

11,800

13,200

Operating expenses

4,200

4,200

Total payments

16,000

17,400

(1) Ending cash balance before financing

13,000

9,800

Minimum cash balance desired

(10,000)

(10,000)

Cash excess (deficiency)

3,000

(200)

(2) Total effect of financing

-0-

1,000

Ending cash balance, (1) + (2)

$13,000

$10,800