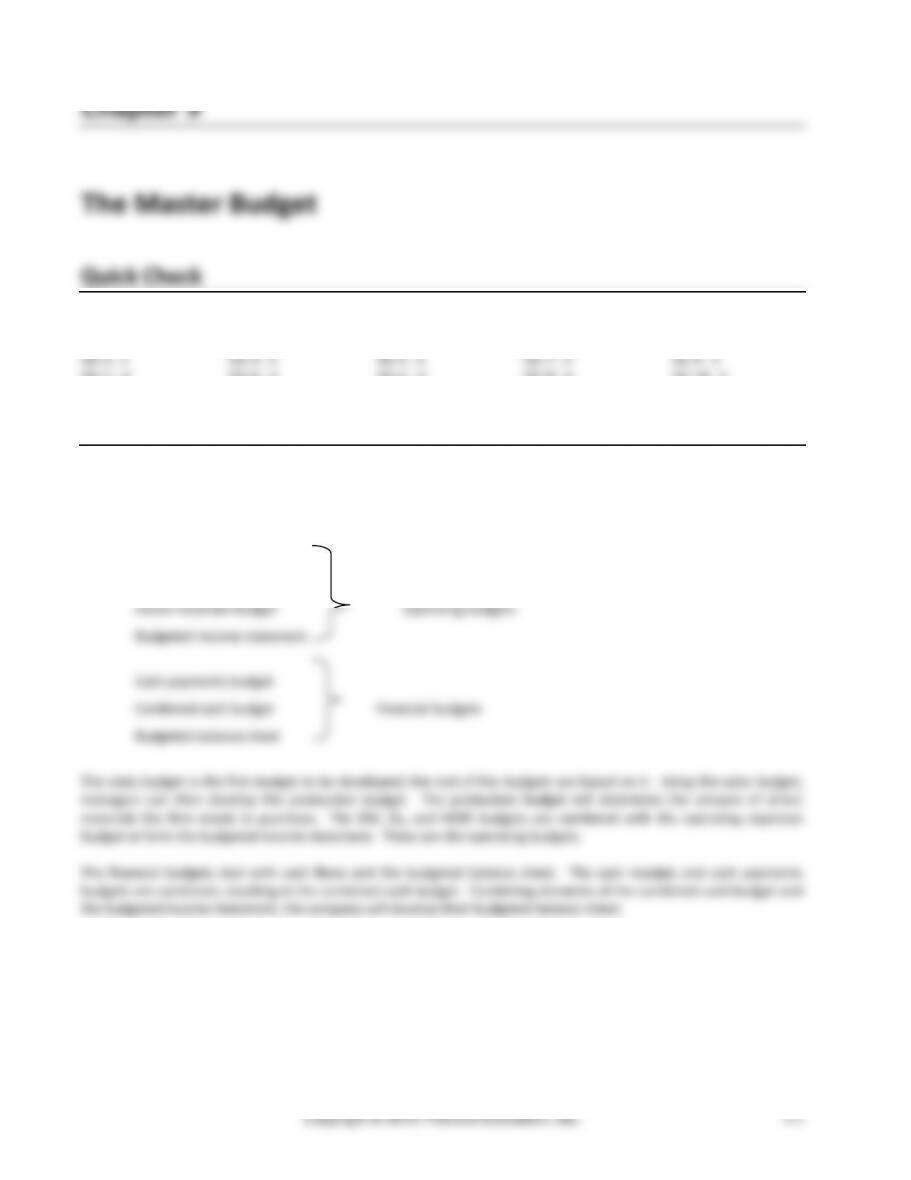

Chapter 9 The Master Budget

Copyright © 2015 Pearson Education, Inc.

9-1

Chapter 9

The Master Budget

Quick Check

Answers:

QC-1. c

QC-3. a

QC-5. b

QC-7. a

QC-9. a

QC-2. d

QC-4. d

QC-6. d

QC-8. b

QC-10. b

Short Exercises

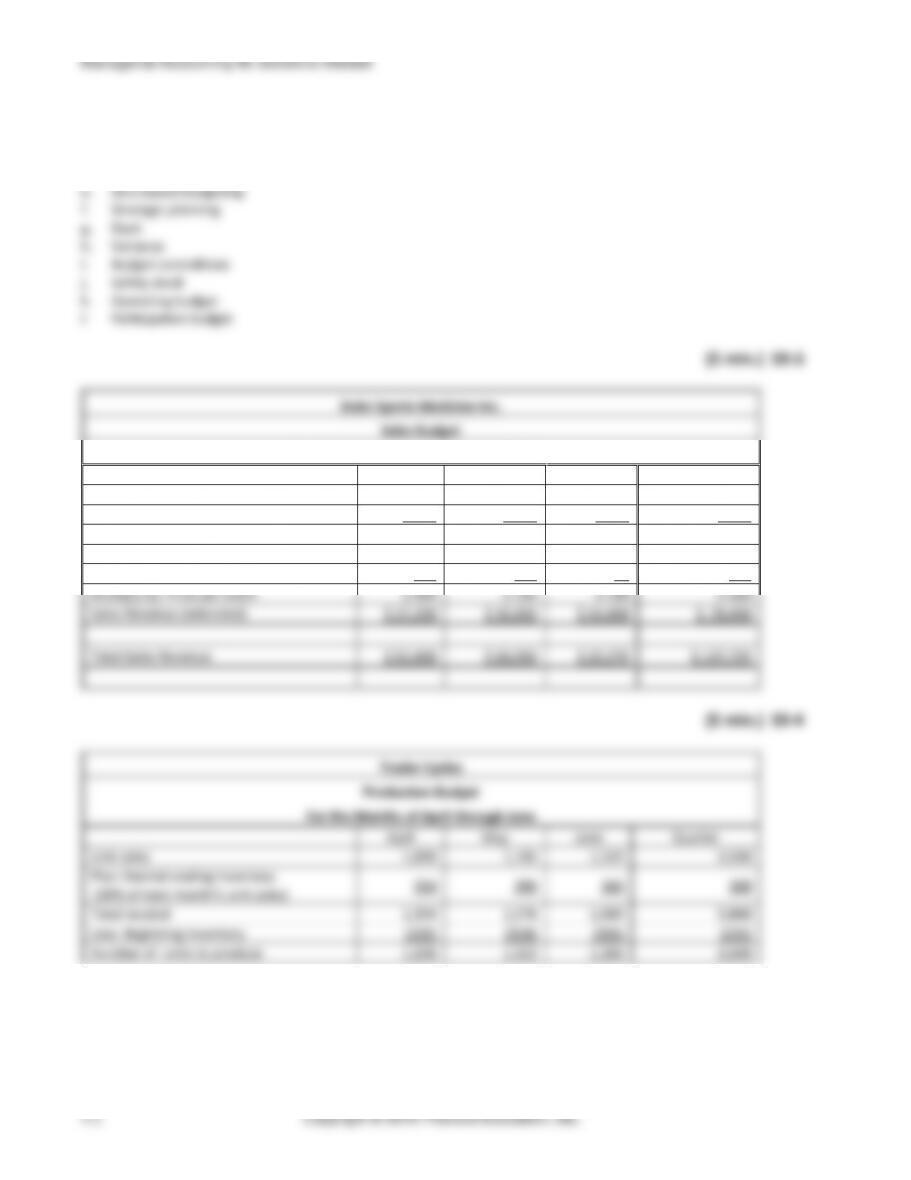

(5-10 min.) S9-1

Prepare the components of the master budget in the following order:

Sales budget

Production budget

(5 min.) S9-2

a. Rolling budget

b. Master budget

c. Financial budgets

d. Production budget

Chapter 9 The Master Budget

(5 min.) S9-5

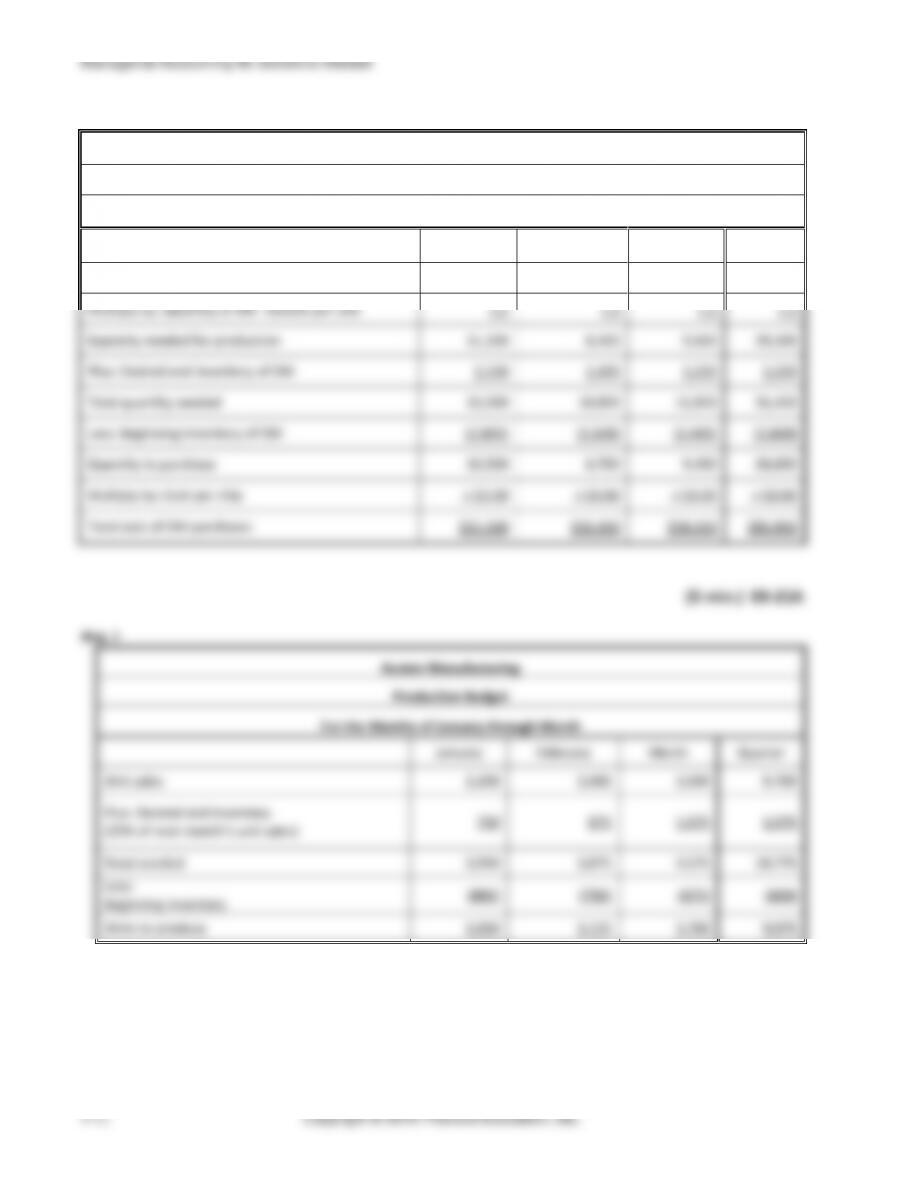

The Bakery by the Bay

Direct Materials Budget

For the Months of July through September

July

August

Sept.

Quarter

Units to be produced

1,460

1,920

1,760

5,140

Multiply by: Pounds of flour

needed per unit

× 0.50

× 0.50

× 0.50

× 0.50

Quantity (lbs.) needed for

production

730

960

880

2,570

Plus: Desired end inventory of DM

(10% of the amount needed

for next month’s production)

96

88

74

74

Total quantity (lbs.) needed

826

1,048

954

2,644

Less: Beginning inventory of DM

(100)

(96)

(88)

(100)

Quantity (lbs.) to purchase

726

952

866

2,544

Multiply by: Cost per pound

× $2.00

× $2.00

× $2.00

× $2.00

Total cost of DM purchases

$1,452

$1,904

$1,732

$5,088

(5 min.) S9-6

Cameron Manufacturing

Direct Labor Budget

For the Months of January through March

January

February

March

Quarter

Units to be produced

560

600

860

2,020

Multiply by: Direct labor hours per unit

× 6.0

× 6.0

× 6.0

× 6.0

Total hours required

3,360

3,600

5,160

12,120

Multiply by: Direct labor cost per hour

× $16

× $16

× $16

× $16

Total direct labor cost

$53,760

$57,600

$82,560

$193,920

(5 min.) S9-7

Total Variable MOH

Plus: Fixed MOH

3,000

Total MOH

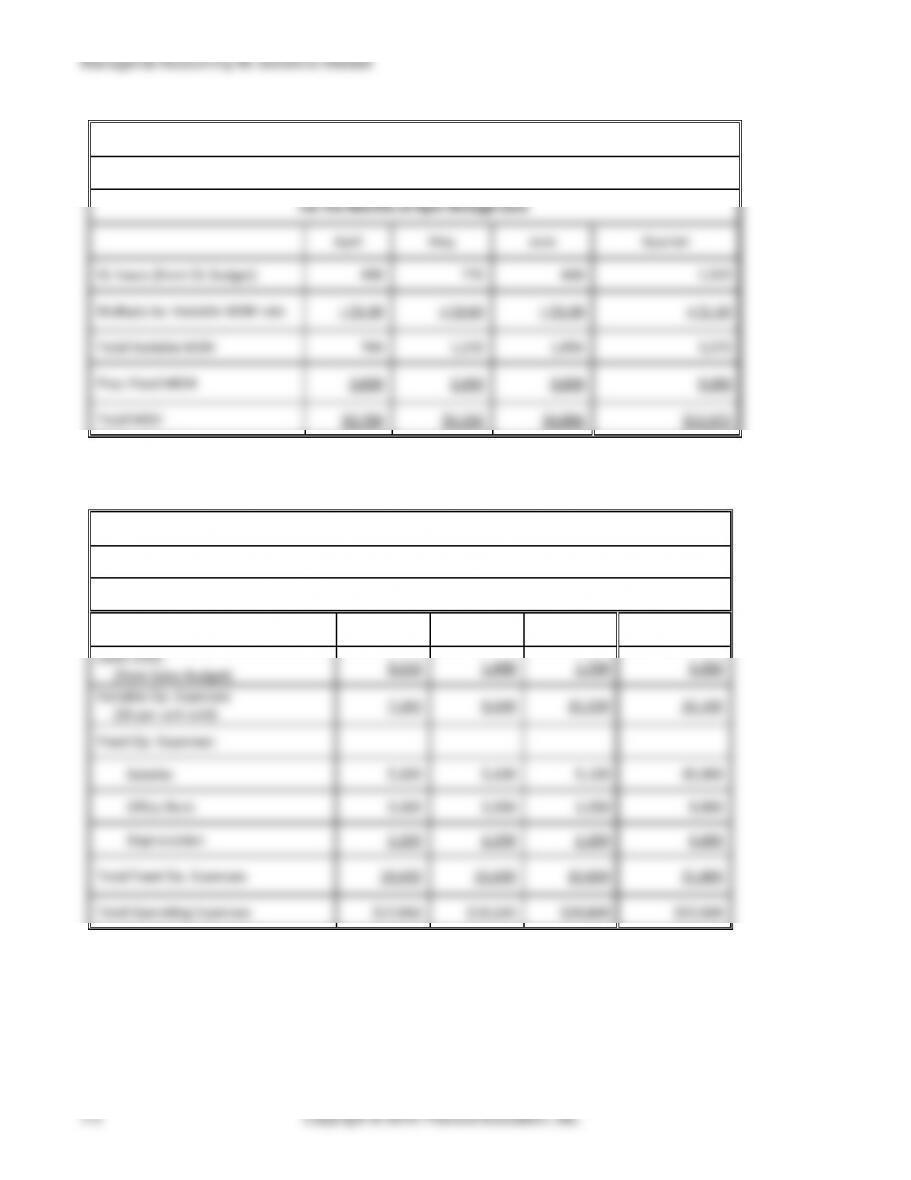

(5 min.) S9-8

Davenport Corporation

Operating Expenses Budget

For the Months of July through September

July

August

Sept.

Quarter

Sales Units

(from Sales Budget)

1,210

1,440

1,700

4,350

Variable Op. Expenses

($6 per unit sold)

7,260

8,640

10,200

26,100

Fixed Op. Expenses:

Salaries

5,100

5,100

5,100

15,300

Office Rent

3,300

3,300

3,300

9,900

Depreciation

2,200

2,200

2,200

6,600

Total Fixed Op. Expenses

10,600

10,600

10,600

31,800

Total Operating Expenses

$17,860

$19,240

$20,800

$57,900

Probe Corporation

Manufacturing Overhead Budget

For the Months of April through June

Chapter 9 The Master Budget

(5 min.) S9-9

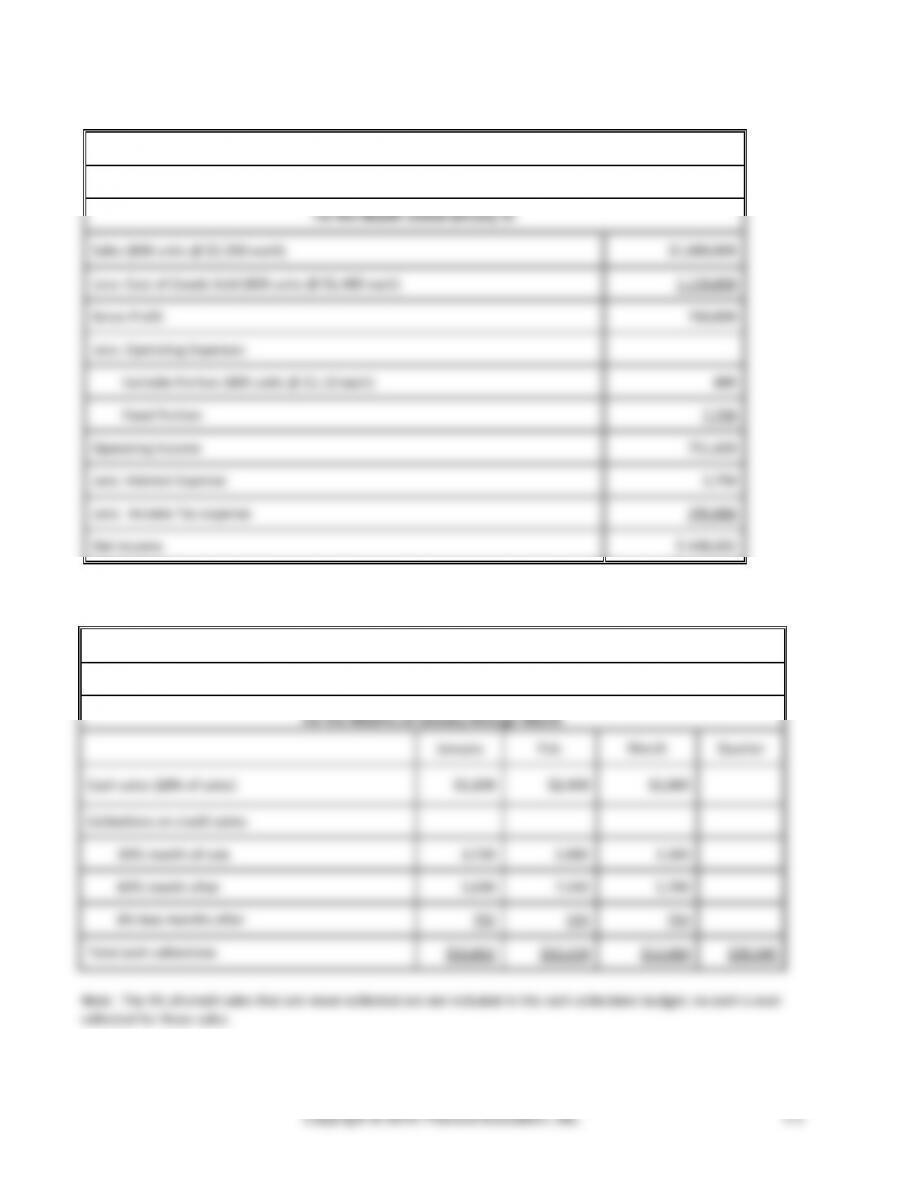

Bell Simpson

Budgeted Income Statement

For the Month ended January 31

Sales (800 units @ $2,350 each)

$1,880,000

Less: Cost of Goods Sold (800 units @ $1,400 each)

1,120,000

Gross Profit

760,000

Less: Operating Expenses

Variable Portion (800 units @ $1.10 each)

880

Fixed Portion

7,700

Operating Income

751,420

Less: Interest Expense

3,700

Less: Income Tax expense

299,088

Net Income

$ 448,632

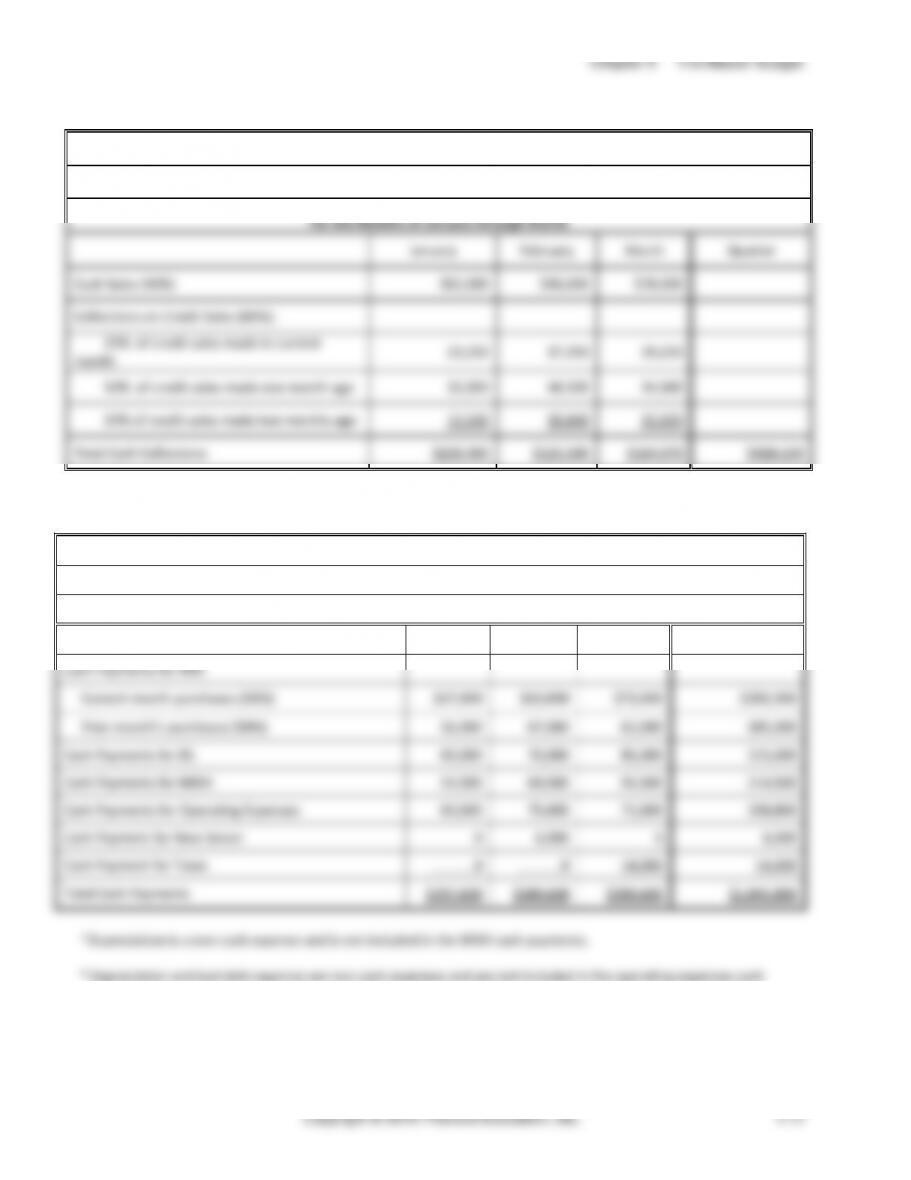

(5 min.) S9-10

Emerald Service

Cash Collections Budget

For the Months of January through March

January

Feb.

March

Quarter

Cash sales (20% of sales)

$3,100

$2,400

$2,800

Collections on credit sales:

30% month of sale

3,720

2,880

3,360

60% month after

5,040

7,440

5,760

6% two months after

792

504

744

Total cash collections

$12,652

$13,224

$12,664

$38,540

Note: The 4% of credit sales that are never collected are not included in the cash collections budget; no cash is ever

collected for these sales.

Managerial Accounting 4e Solutions Manual

(5 min.) S9-11

Stately Corporation

Cash Payments Budget

Cash Payments for DM:

Last month’s purchases (45%)

$35,550

This month’s purchases (55%)

48,400

Cash Payments for DL

35,000

Cash Payments for MOH

38,000

Cash Payments for Operating Expenses

42,600

Cash Payment for Taxes

7,600

Total Cash Payments

$207,150

(5-10 min.) S9-12

George Services, Inc.

Cash Budget

Month Ended October 31

Beginning cash balance

$ 8,200

Plus: Cash collections from customers

548,410

Cash available

556,610

Less: Total cash payments

(573,870)

Ending cash balance before financing

(17,260)

Minimum cash balance desired

(7,600)

Amount to borrow

$ (24,860)

George must borrow $24,860 by the end of October.

(5 min.) S9-13

Transaction fee = ($0.45 × number of transactions) + (1% × sales made with credit and debit cards)

Chapter 9 The Master Budget

(15 min.) S9-14

Req. 1

Techworks Company

Sales Budget

January

February

Total

Sales price per phone

$ 170.00

$ 200.00

Multiply by: Number of phones

× 4,200

× 3,800

Total sales

$714,000

$760,000

$1,474,000

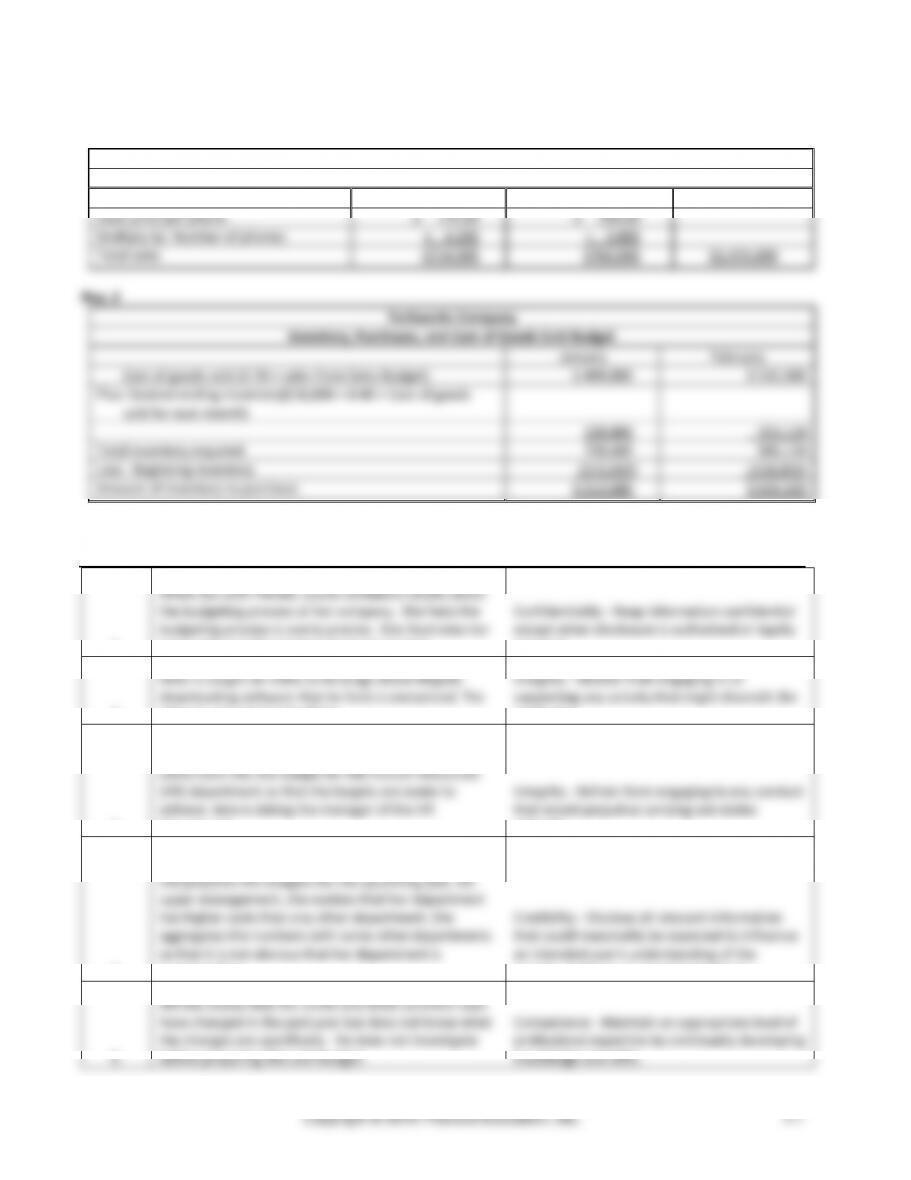

Req. 2

Techworks Company

Inventory, Purchases, and Cost of Goods Sold Budget

January

February

Cost of goods sold (0.70 × sales from Sales Budget)

$ 499,800

$ 532,000

Plus: Desired ending inventory($16,000 + 0.40 × Cost of goods

sold for next month)

228,800

353,120

Total inventory required

728,600

885,120

Less: Beginning inventory

(215,920)

(228,800)

Amount of inventory to purchase

$ 512,680

$ 656,320

(5-10 min.) S9-15

1.

When out with friends, Louise complains loudly about

the budgeting process at her company. She feels the

budgeting process is overly precise. She illustrates her

point with specific numbers from the budget.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

2.

Allan is caught on video as he brags about illegally

downloading software that he feels is overpriced. The

video is uploaded to YouTube.

Integrity – Abstain from engaging in or

supporting any activity that might discredit the

profession.

3.

Jake, an accountant for Snow Films Company, builds

some slack into the budget for the Human Resources

(HR) department so that the targets are easier to

achieve. Jake is dating the manager of the HR

department.

Integrity – Refrain from engaging in any conduct

that would prejudice carrying out duties

ethically.

4.

Pearl is the controller for Cloudy Fork Gardens. When

she prepares the budgets for the upcoming year, for

upper management, she realizes that her department

has higher costs than any other department. She

aggregates the numbers with some other departments

so that it is not obvious that her department is

overspending.

Credibility – Disclose all relevant information

that could reasonably be expected to influence

an intended user’s understanding of the

reports, analyses, or recommendations.

5.

Alfredo knows that the credit and debit card fees laws

have changed in the past year but does not know what

the changes are specifically. He does not investigate

before preparing the cash budget.

Competence – Maintain an appropriate level of

professional expertise by continually developing

knowledge and skills.

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(15 min.) E9-16A

Req. 1

Direct materials budget before any changes

For quarters 1 through 4

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Number of soda pop bottles to be produced

2,800,000

3,100,000

2,600,000

2,500,000

11,000,000

Multiply by:Kilograms of PET per bottle (original)

0.01

0.01

0.01

0.01

0.01

Quantity of PET needed for production (kg)

28,000

31,000

26,000

25,000

110,000

Plus: Desired ending inventory of PET

9,300

7,800

7,500

8,040

8,040

Total quantity (kg) needed

37,300

38,800

33,500

33,040

118,040

Less: Beginning inventory of PET

(8,400)

(9,300)

(7,800)

(7,500)

(8,400)

Quantity of PET (kg) to purchase

28,900

29,500

25,700

25,540

109,640

Multiply by: Cost per kilogram

$ 5.00

$ 5.00

$ 5.00

$ 5.00

$ 5.00

Total cost of PET purchases

$ 144,500.00

$ 147,500.00

$ 128,500.00

$ 127,700

$ 548,200

Req. 2

Direct materials budget after reducing PET content of each bottle

For quarters 1 through 4

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Number of soda pop bottles to be produced

2,800,000

3,100,000

2,600,000

2,500,000

11,000,000

Multiply by: Kilograms of PET per bottle (after reduction for

redesign)

0.009

0.009

0.009

0.009

0.009

Quantity of PET needed for production (kg)

25,200

27,900

23,400

22,500

99,000

Plus: Desired ending inventory of PET

8,370

7,020

6,750

8,040

8,040

Total quantity (kg) needed

33,570

34,920

30,150

30,540

107,040

Less: Beginning inventory of PET

(8,400)

(8,370)

(7,020)

(6,750)

(8,400)

Quantity of PET (kg) to purchase

25,170

26,550

23,130

23,790

98,640

Multiply by: Cost per kilogram

$ 5.30

$ 5.30

$ 5.30

$ 5.30

$ 5.30

Total cost of PET purchases

$ 133,401.00

$ 140,715.00

$ 122,589.00

$ 126,087.00

$ 522,792.00

Chapter 9 The Master Budget

(continued) E9-16A

Req. 3

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Savings from reducing PET content of each bottle

$ 11,099

$ 6,785

$ 5,911

$ 1,613

$ 25,408

Total savings for the year

$ 25,408

Cost of retrofitting the molds

$ 24,478

Net savings (cost) of retrofitting – first year

$ 930

Savings each year AFTER the first year

$ 25,408

The company should make the change (retrofitting); even though the first year results in a net outflow, later years will realize savings.

(5 min.) E9-17A

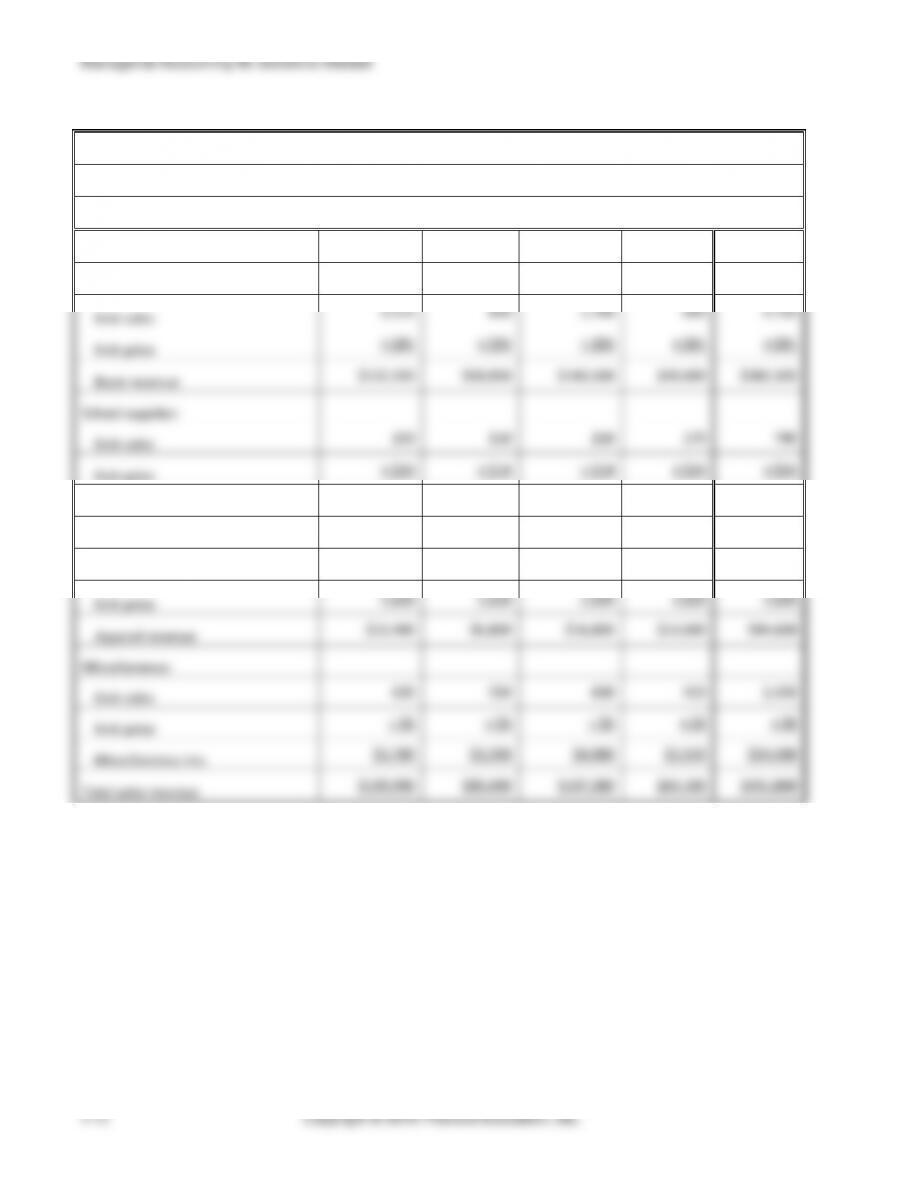

Miami College Bookstore

Sales Budget

For the Upcoming Year

Q1

Q2

Q3

Q4

Year

Books:

Unit sales

1,510

850

1,760

600

4,720

Unit price

× $81

× $81

× $81

× $81

× $81

Book revenue

$122,310

$68,850

$142,560

$48,600

$382,320

School supplies:

Unit sales

250

110

210

170

740

Unit price

× $14

× $14

× $14

× $14

× $14

School supplies rev.

$3,500

$1,540

$2,940

$2,380

$10,360

Apparel:

Unit sales

520

340

840

530

2,230

Unit price

× $20

× $20

× $20

× $20

× $20

Apparel revenue

$10,400

$6,800

$16,800

$10,600

$44,600

Miscellaneous:

Unit sales

630

550

830

420

2,430

Unit price

× $6

× $6

× $6

× $6

× $6

Miscellaneous rev.

$3,780

$3,300

$4,980

$2,520

$14,580

Total sales revenue

$139,990

$80,490

$167,280

$64,100

$451,860

Chapter 9 The Master Budget

(10-20 min.) E9-18A

Hinckley Preschool

Budgeted Revenue

For Year Ended XXXX

Monthly tuition revenue:

2-day program

86 kids × $115

$ 9,890

3-day program

34 kids × $140

4,760

4-day program

68 kids × $155

10,540

5-day program

26 kids × $180

4,680

Total monthly tuition

$29,870

Months of operations

× 8 months

Total tuition revenue

$238,960

Registration fee revenue

214 kids × $135

28,890

Lunch bunch revenue

(214 kids × 50%) × $4 × 12

times

per month × 8 months

41,088

Total Revenue

$308,938

Note: Students may have shown yearly tuition by age group, rather than finding monthly tuition and then multiplying

it by the nine months of operations. Nonetheless, total tuition revenue for the year should be the same as that shown.

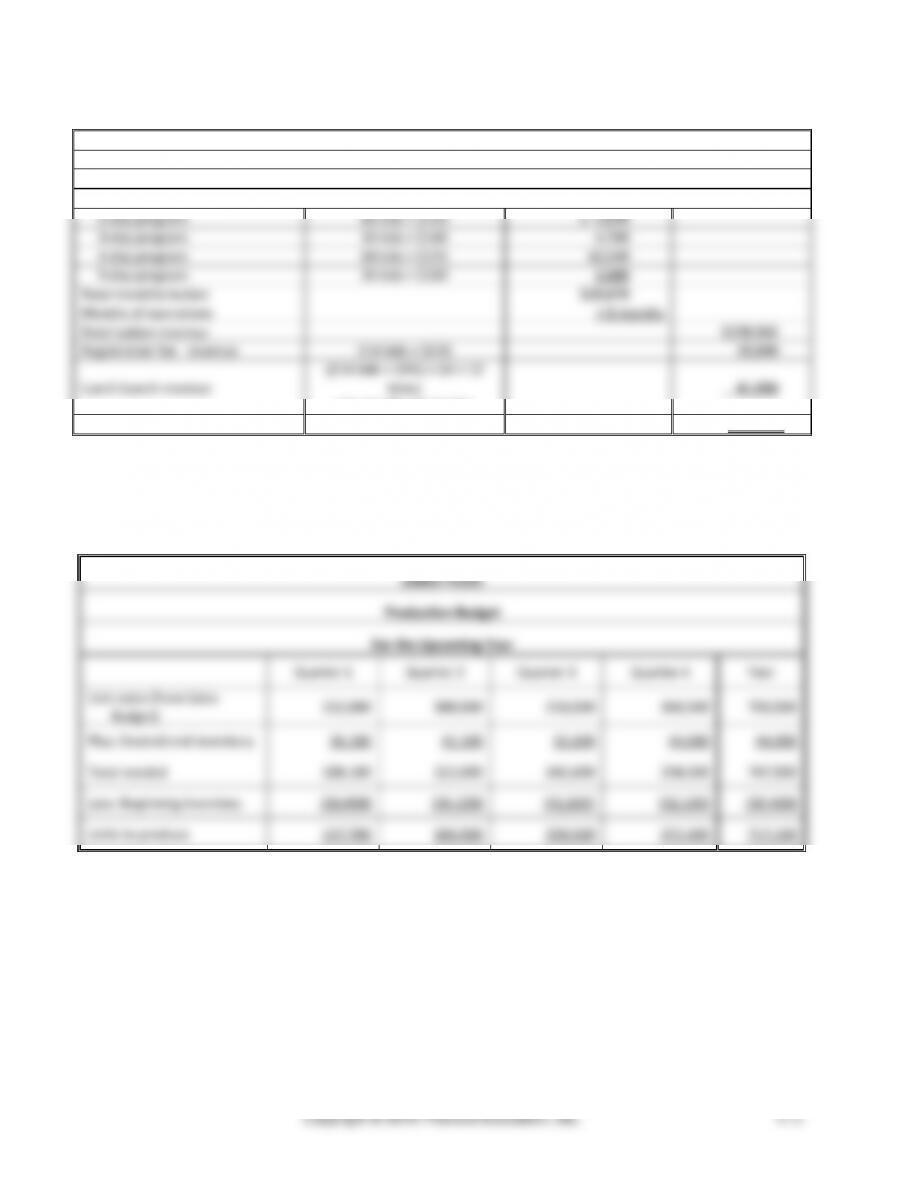

(5 min.) E9-19A

Jabber Foods

Production Budget

For the Upcoming Year

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Unit sales (from Sales

Budget)

152,000

180,500

210,500

160,500

703,500

Plus: Desired end inventory

36,100

42,100

32,100

44,000

44,000

Total needed

188,100

222,600

242,600

204,500

747,500

Less: Beginning inventory

(30,400)

(36,100)

(42,100)

(32,100)

(30,400)

Units to produce

157,700

186,500

200,500

172,400

717,100

(5 min.) E9-20A

Beckett Industries

Direct Materials Budget

For the Months of January through March

January

February

March

Quarter

Units to be produced (from Production Budget)

5,600

4,200

4,800

14,600

Multiply by: Quantity of DM needed per unit

× 2

× 2

× 2

× 2

Quantity needed for production

11,200

8,400

9,600

29,200

Plus: Desired end inventory of DM

2,100

2,400

2,250

2,250

Total quantity needed

13,300

10,800

11,850

31,450

Less: Beginning Inventory of DM

(2,800)

(2,100)

(2,400)

(2,800)

Quantity to purchase

10,500

8,700

9,450

28,650

Multiply by: Cost per chip

× $3.00

× $3.00

× $3.00

× $3.00

Total cost of DM purchases

$31,500

$26,100

$28,350

$85,950

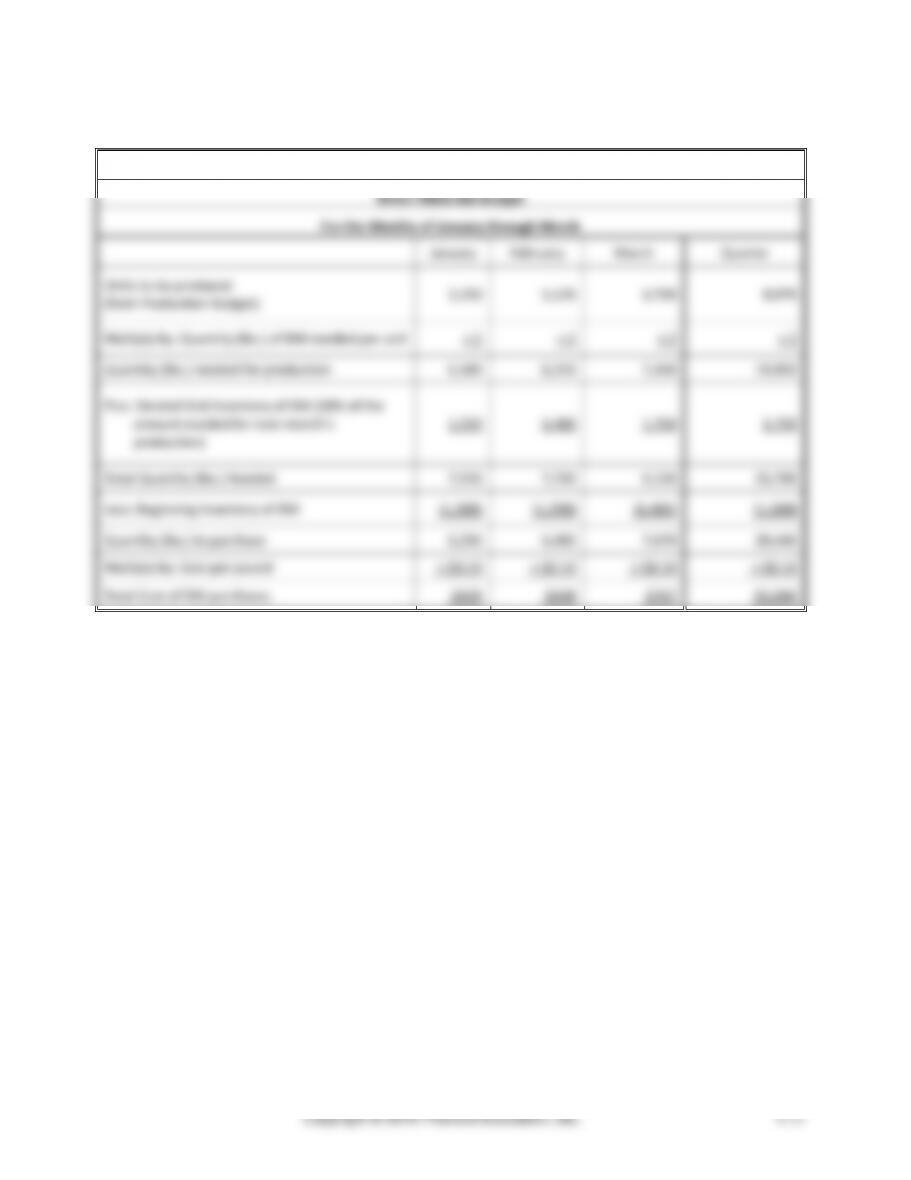

(5 min.) E9-21A

Req. 1

Austen Manufacturing

Production Budget

For the Months of January through March

January

February

March

Quarter

Unit sales

3,200

3,000

3,500

9,700

Plus: Desired end inventory

(25% of next month’s unit sales)

750

875

1,075

1,075

Total needed

3,950

3,875

4,575

10,775

Less:

Beginning inventory

(800)

(750)

(875)

(800)

Units to produce

3,150

3,125

3,700

9,975

Chapter 9 The Master Budget

(continued) E9-21A

Req. 2

Austen Manufacturing

Direct Materials Budget

For the Months of January through March

January

February

March

Quarter

Units to be produced

(from Production Budget)

3,150

3,125

3,700

9,975

Multiply by: Quantity (lbs.) of DM needed per unit

× 2

× 2

× 2

× 2

Quantity (lbs.) needed for production

6,300

6,250

7,400

19,950

Plus: Desired End Inventory of DM (20% of the

amount needed for next month’s

production)

1,250

1,480

1,750

1,750

Total Quantity (lbs.) Needed

7,550

7,730

9,150

21,700

Less: Beginning Inventory of DM

(1,260)

(1,250)

(1,480)

(1,260)

Quantity (lbs.) to purchase

6,290

6,480

7,670

20,440

Multiply by: Cost per pound

× $0.10

× $0.10

× $0.10

× $0.10

Total Cost of DM purchases

$629

$648

$767

$2,044

Managerial Accounting 4e Solutions Manual

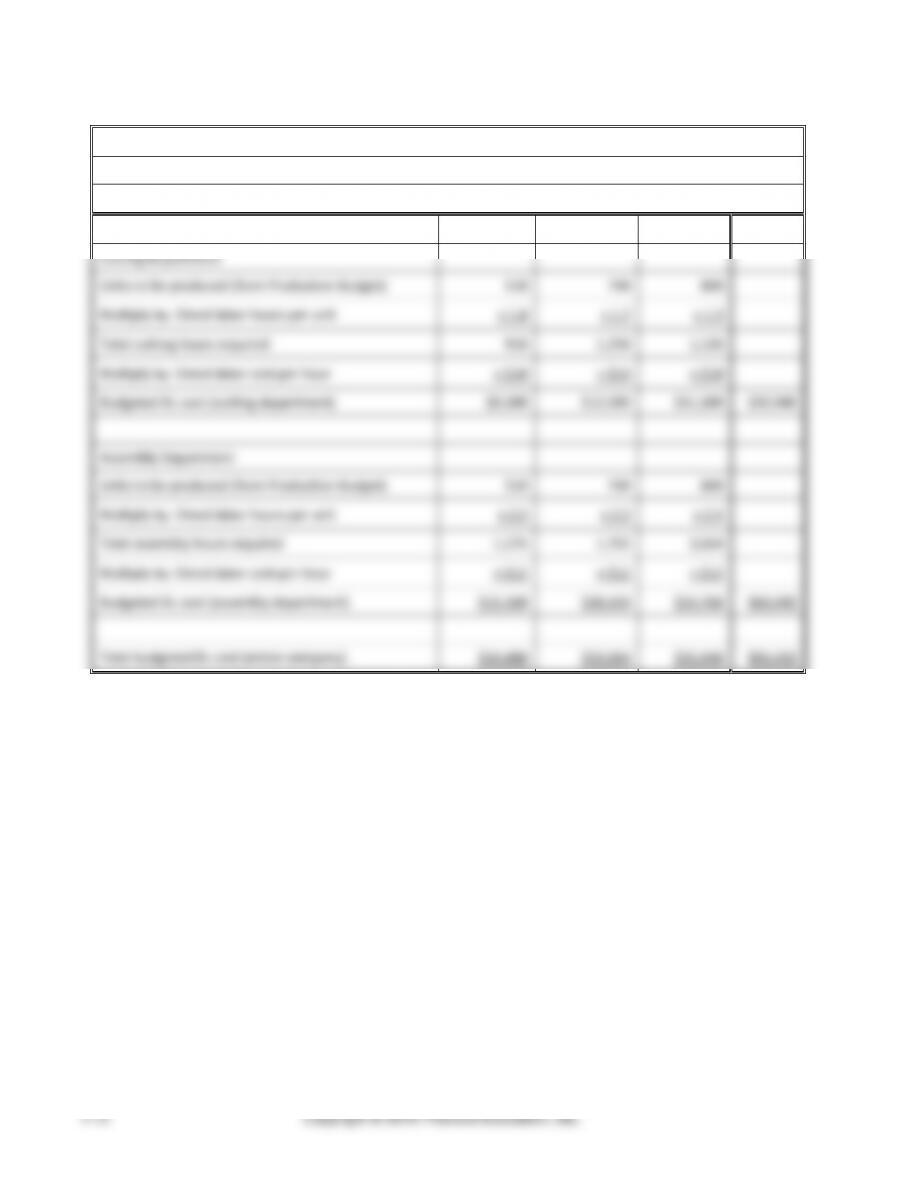

(5 min.) E9-22A

Anderson Industries

Direct Labor Budget

For the Upcoming Year

Rockets

Imperials

Zooms

Total

Cutting Department

Units to be produced (from Production Budget)

510

740

860

Multiply by: Direct labor hours per unit

× 1.8

× 1.7

× 1.3

Total cutting hours required

918

1,258

1,118

Multiply by: Direct labor cost per hour

× $10

× $10

× $10

Budgeted DL cost (cutting department)

$9,180

$12,580

$11,180

$32,940

Assembly Department

Units to be produced (from Production Budget)

510

740

860

Multiply by: Direct labor hours per unit

× 2.5

× 2.3

× 2.4

Total assembly hours required

1,275

1,702

2,064

Multiply by: Direct labor cost per hour

× $12

× $12

× $12

Budgeted DL cost (assembly department)

$15,300

$20,424

$24,768

$60,492

Total budgeted DL cost (entire company)

$24,480

$33,004

$35,948

$93,432

(15 min.) E9-23A

The Mcknight Company

Manufacturing Overhead Budget

For the Upcoming Year

Projected Sales (from Sales Budget)

42,000

Variable MOH costs:

Indirect materials ($1.00 per unit)

$ 42,000

Supplies ($.70 per unit)

29,400

Indirect labor ($0.30 per unit)

12,600

Plant utilities ($0.20 per unit)

8,400

Repairs and maintenance ($0.40 per unit)

16,800

Total Variable MOH

$ 109,200

Fixed MOH costs:

Indirect labor

$ 62,000

Plant utilities

39,000

Repairs and maintenance

10,000

Depreciation on plant and equipment

48,000

Insurance on plant and equipment

27,000

Plant supervision

65,000

Total Fixed MOH

$ 251,000

Total MOH

$ 360,200

Managerial Accounting 4e Solutions Manual

(20-30 min.) E9-24A

Req. 1

Start Smart Preschool

Budgeted Monthly Operating Expenses

Teachers’ salary:

2-day program

7 teachers × $434 per month

$3,038

3-day program

2 teachers × $648 per month

1,296

4-day program

5 teachers × $884 per month

4,420

5-day program

4 teachers × $1,060 per month

4,240

Director salary

1,500

Total salary expense

$14,494

Payroll tax expense

$14,494 × 7.65%

1,109

Lease expense

4,012

Fixed operating expenses

890

Variable operating expenses

960

Total monthly operating

expenses

$21,465

Req. 2

Start Smart Preschool

Budgeted Income Statement

For Year Ended XXXX

Tuition, registration fees, and lunch bunch revenue

$ 241,200

Less: Operating expenses ($21,465* × 9 months)

(193,185)

Operating income

$ 48,015

__________

a from Req. 1

Req. 3

From the budgeted income statement, Start Smart learns that it has projected operating income for the year. Since

Start Smart is a not-for-profit preschool, it is not in business to generate income for its owners. Rather, Start Smart may

be able to further its organizational goals with the projected income. For example, it may decide to use the income for

any of the following purposes:

• Invest in additional (or better) classroom equipment

• Invest in additional (or better) playground equipment

• Improve the current program (more crafts, books, better curriculum, special guest visitors, special programs,

field trips, etc.)

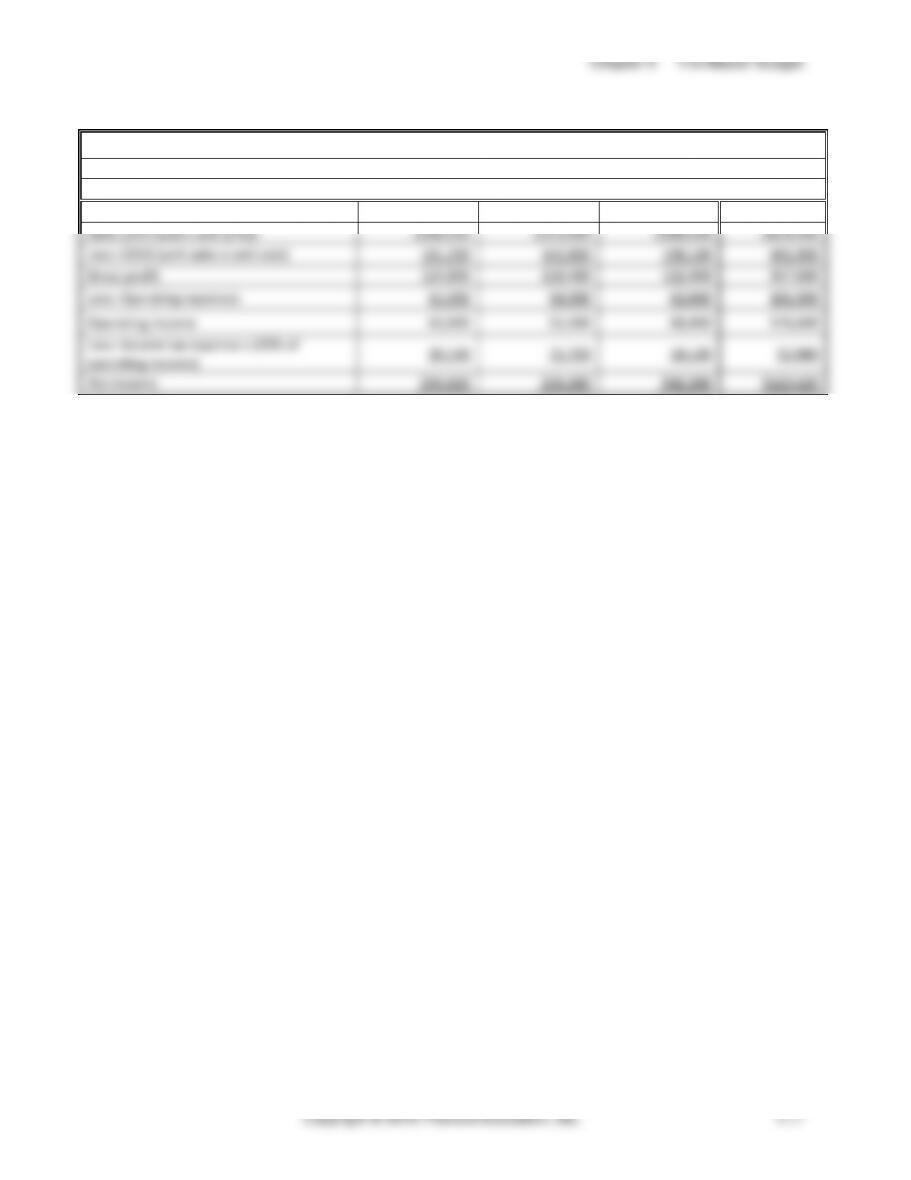

(5 min.) E9-25A

Germaine Labs

Budgeted Income Statement

For the Quarter Ended March 31

Jan.

Feb.

March

Quarter

Sales (unit sales x sale price)

$286,000

$253,000

$280,500

$819,500

Less: COGS (unit sales x unit cost)

161,200

142,600

158,100

461,900

Gross profit

124,800

110,400

122,400

357,600

Less: Operating expenses

61,000

58,000

62,000

181,000

Operating income

63,800

52,400

60,400

176,600

Less: Income tax expense s (30% of

operating income)

19,140

15,720

18,120

52,980

Net income

$44,660

$36,680

$42,280

$123,620

Managerial Accounting 4e Solutions Manual

(15 min.) E9-26A

Berkner Motors

Budgeted Income Statement

For the Upcoming Year

Quarter 1

Quarter 2

Quarter 3

Quarter 4

Year

Sales

$ 3,774,000

$ 3,924,960

$ 4,042,709

$ 4,244,844

$ 15,986,513

Less: Cost of goods sold

2,075,700

2,158,728

2,223,490

2,334,664

8,792,582

Gross profit

$ 1,698,300

$ 1,766,232

$ 1,819,219

$ 1,910,180

$ 7,193,931

Less: Operating expenses

1,320,900

1,373,736

1,010,677

848,969

4,554,282

Operating Income

$ 377,400

$ 392,496

$ 808,542

$ 1,061,211

$ 2,639,649

Calculations:

Given in exercise

$ of amount of

increase (% x Total

sales prior period)

Total Sales

Base sales

$ 3,700,000

% increase Quarter 1

2%

$ 74,000

$ 3,774,000

% increase Quarter 2

4%

$ 150,960

$ 3,924,960

% increase Quarter 3

3%

$ 117,749

$ 4,042,709

% increase Quarter 4

5%

$ 202,135

$ 4,244,844

Given in exercise

Sales in Quarter

Operating

Expenses

% operating expenses in Qtr 1

35%

$ 3,774,000

$ 1,320,900

% operating expenses in Qtr 2

35%

$ 3,924,960

$ 1,373,736

% operating expenses in Qtr 3

25%

$ 4,042,709

$ 1,010,677

% operating expenses in Qtr 4

20%

$ 4,244,844

$ 848,969

(5 min.) E9-27A

Bentfield Corporation

Cash Collections Budget

For the Months of January through March

January

February

March

Quarter

Cash Sales (40%)

$62,000

$46,000

$78,000

Collections on Credit Sales (60%):

25% of credit sales made in current

month

23,250

17,250

29,250

50% of credit sales made one month ago

33,000

46,500

34,500

24% of credit sales made two months ago

12,240

15,840

22,320

Total Cash Collections

$130,490

$125,590

$164,070

$420,150

(5 min.) E9-28A

The Smith Company

Cash Payments Budget

For the Months of April through June

April

May

June

Quarter

Cash Payments for DM:

Current month purchases (50%)

$67,000

$62,000

$73,500

$202,500

Prior month’s purchases (50%)

56,000

67,000

62,000

185,000

Cash Payments for DL

60,000

70,000

85,000

215,000

Cash Payments for MOH

54,000

69,000

91,500

214,500

Cash Payments for Operating Expenses

60,600

75,600

72,600

208,800

Cash Payment for New Server

0

6,000

0

6,000

Cash Payment for Taxes

0

0

14,000

14,000

Total Cash Payments

$297,600

$349,600

$398,600

$1,045,800

a Depreciation is a non-cash expense and is not included in the MOH cash payments.

b Depreciation and bad debt expense are non-cash expenses and are not included in the operating expenses cash

payments.

Managerial Accounting 4e Solutions Manual

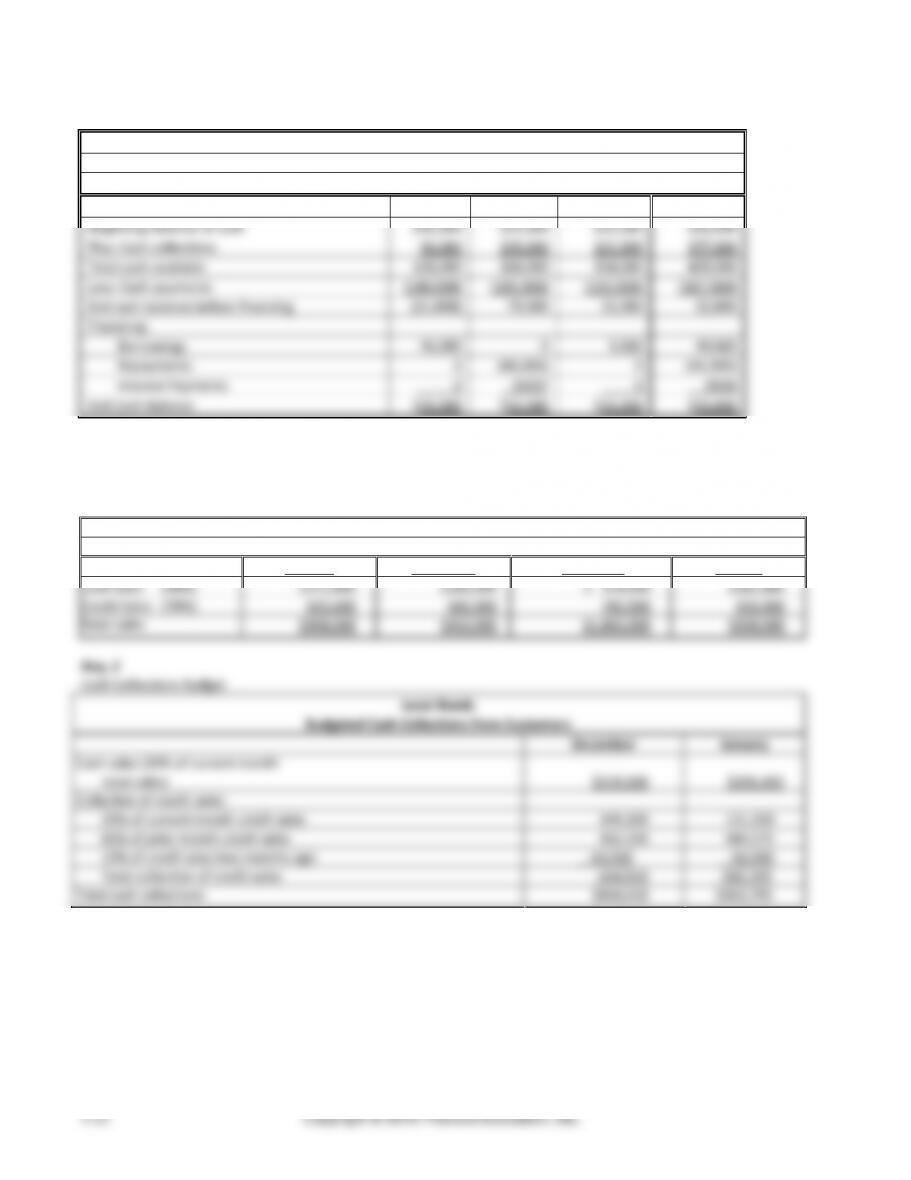

(5 min.) E9-29A

Monette Health Center

Combined Cash Budget

For the Months of July through September

July

August

Sept.

Quarter

Beginning balance of cash

$32,000

$25,000

$32,080

$32,000

Plus: Cash collections

96,000

159,000

122,000

377,000

Total cash available

128,000

184,000

154,080

409,000

Less: Cash payments

(149,000)

(105,000)

(133,000)

(387,000)

End cash balance before financing

(21,000)

79,000

21,080

22,000

Financing:

Borrowings

46,000

0

3,920

49,920

Repayments

0

(46,000)

0

(46,000)

Interest Payments

0

(920)a

0

(920)

End Cash Balance

$25,000

$32,080

$25,000

$25,000

(20-30 min.) E9-30A

Req. 1

Sales Budget

Leret Reeds

Sales Budget

October

November

December

January

Cash Sales (30%)

$272,400

$285,000

$ 319,500

$281,400

Credit Sales (70%)

635,600

665,000

745,500

656,600

Total sales

$908,000

$950,000

$1,065,000

$938,000

Req. 2

Cash Collections Budget

Leret Reeds

Budgeted Cash Collections from Customers

December

January

Cash sales (30% of current month

total sales)

$319,500

$281,400

Collection of credit sales:

20% of current month credit sales

149,100

131,320

65% of prior month credit sales

432,250

484,575

10% of credit sales two months ago

63,560

66,500

Total collection of credit sales

644,910

682,395

Total cash collections

$964,410

$963,795