Chapter 8 Relevant Costs for Short-Term Decisions

Copyright © 2015 Pearson Education, Inc.

8-1

Chapter 8

Relevant Costs for Short-Term Decisions

Quick Check

Answers:

QC-1. c

QC-3. d

QC-5. a

QC-7. b

QC– 9. b

QC-2. c

QC-4. b

QC-6. c

QC-8. d

QC-10. a

(5 min.) S8-1

a. The trade-in value of the old printer is relevant.

b. Paper costs are irrelevant because these costs will be the same with either the old printer or the new printer.

c. The difference between the toner cartridges is relevant.

Managerial Accounting 4e Solutions Manual

(10 min.) S8-3

Req. 1

Mount Snows should emphasize a cost-plus approach to pricing because it has been able to differentiate its ski resort

from others in the area. Because of its favorable reputation, managers will have some control over pricing. Of course,

$ 89

(10-15 min.) S8-4

Req. 1

If Mount Snows is a price-taker, projected income is as follows:

Revenue at market price (775,000 × $66)………………..

$51,150,000

Less: Total costs…………………………………………………….

(49,425,000)a

Operating income……………………………………………

$ 1,725,000

vs. Desired operating income ($115 million × 17%)……

$19,550,000

Expected profit shortfall…………………………………..

$ 17,825,000

a Previous problem

As a percentage of assets, Mount Snows’ projected profit is 1.50% ($1,725,000/$115,000,000). Investors will not be

happy with this profit level, because the expected return on assets is less than the desired return on assets. Stock

prices may decline as a result.

Req. 2

If Mount Snows is able to reduce its fixed costs to $28.5 million, its new target variable cost per skier/snowboarder is:

TOTAL

Revenue at market price ($66 × 775,000)

$51,150,000

Less: Desired profit ($115 million × 17%)

(19,550,000)

Target total cost

$31,600,000

Less: Reduced level of fixed costs

(28,500,000)

Target total variable costs

$ 3,100,000

Divided by number of skiers and snowboarders

÷775,000

Target variable cost per skiers and snowboarders

$ 4.00

This target variable cost is less than 60% of the current variable cost of $7.00. Mount Snows may have a difficult time

achieving this target since it is so much lower than the current variable cost.

(5-10 min.) S8-5

The Men’s and Women’s Departments are earning income. While the Accessories Department appears to be losing

(10 min.) S8-6

Expected decrease in revenues…………….

$98,000

Expected decrease in expenses:

Variable expenses…………………………..

$90,000

Fixed expenses……………………………

25,000

Total expenses………………………………

115,000

Expected increase in operating income……

$ 17,000

Decision: Mila Fashions should drop the Accessories Department.

(10 min.) S8-7

Expected revenues…………………………..

$81,000

Expected expenses:

Variable expenses………………………

$52,000

Fixed expenses ($6,800 x 4)……………

27,200

Total expenses…………………………

79,200

Expected operating income from shoe department………………………………

$1,800

Compare this potential profit with the contribution margins from the other departments:

Department (sales − variable costs)

Contribution margin

Men ‘s ($109,000 − $59,000)………………….

$50,000

Women’s ($56,000 − $30,000)………………

$26,000

Accessories ($98,000 − $90,000)…………

$8,000

The company should not consider replacing the Accessories Department with a Shoe Department because even though

the Shoe Department has a higher contribution margin than the Accessories Department, the Shoe Department will

incur an additional $27,200 in fixed costs.

Managerial Accounting 4e Solutions Manual

(15 min.) S8-8

Req. 1

StoreAway production is constrained by the machine hours available for producing the bins. StoreAway needs to

determine its most profitable product mix by considering each size bin’s contribution margin per machine hour:

Regular

Large

Sales price per unit

$ 8.40

$10.20

Less: Variable cost per unit

(3.00)

(4.40)

Contribution margin per unit

$ 5.40

$ 5.80

× Units per machine hour

× 16

× 12

Contribution margin per machine hour

$86.40

$69.60

Machine hours available………………………………

2,800

Number of regular bins per machine hour…………..

× 16

Maximum production of regular size bins……………

44,800

StoreAway should spend all 2,800 machine hours making regular size bins, resulting in 44,800 regular size bins and 0

machine hours making large size bins.

Req. 3

Given this product mix, StoreAway’s operating income for the period is projected to be:

Number of regular size bins……………………

44,800

Contribution margin per regular size bin………

× $5.40

Total contribution margin………………………

$ 241,920*

Less: Fixed expenses……………………………

(120,000)

Operating income…………………………………

$ 121,920

*Total contribution margin can also be found by multiplying

2,800 hours by the regular size bin contribution margin per

hour of $86.40 (2,800 hours × $86.40/ hour = $241,920).

(15 min.) S8-9

Req. 1

StoreAway should emphasize the production of regular size bins, since they are more profitable than the large size

bins. StoreAway should make as many regular bins as it can sell and then use the remaining machine hours to produce

large bins:

Number of machine hours available………………………..

2,800 hours

Number of regular bins demanded………………………….

38,400

Divided by number of regular bins produced per hour….

÷ 16

Number of hours used to produce regular bins…………..

2,400 hours

Number of hours still available………………………………

400 hours

Multiplied by number of large bins produced per hour…

× 12

Number of large bins to produce……………………………

4,800

StoreAway should produce 38,400 regular size bins and 4,800 large size bins.

Chapter 8 Relevant Costs for Short-Term Decisions

(continued) S8-9

Req. 2

Given this product mix, StoreAway’s operating income will be:

Regular

Large

Total

Number of bins

38,400

4,800

Contribution margin per bin

×$5.40

×$5.80

Total contribution margin

$207,360*

$27,840**

$235,200

Less: Fixed expenses

(120,000)

Operating income

$115,200

*Regular bin contribution margin can also be found by multiplying 2,400 hours by the regular size bin contribution

margin per hour of $86.40 (2,400 hours × $86.40/ hour = $207,360).

** Large bin contribution margin can also be found by multiplying 400 hours by the large size bin contribution margin

per hour of $69.60 (400 hours × $69.60/ hour = $27,840).

Req. 3

Operating income is less than it was when StoreAway was producing its optimal product mix because the company had

to produce less regular size bins to match demand for these bins. The company had to give up some of the regular bin

contribution margin per machine hour in order to produce large bins.

(10 min.) S8–10

Req. 1

The absorption unit cost of making the bread is $2.39 per loaf:

Direct material………………………………..

$0.46

Direct labor……………………………………

0.75

Variable overhead……………………………

0.22

Variable cost per unit…………………….

$1.43

Plus: Fixed overhead per unit……………….

.96

Full (absorption) cost per unit……………….

$2.39

Req. 2

Decision: The company should bake the bread in-house since the variable cost of making each loaf is less than the cost

of outsourcing each loaf.

Req. 3

The company should consider the following qualitative factors before making a final decision:

Will the local bakery meet its delivery time requirements? If labor and oven time were not devoted to bread making,

could another more profitable product be made in its place? How does the quality and freshness of the local bakery

bread compare to the bread baked in-house?

(5-10 min.) S8–11

The book value of Wheeler Food’s trucks is irrelevant, because it will be the same whether the fleet management is

Managerial Accounting 4e Solutions Manual

(continued) S8–11

Wheeler Food

Outsourcing Decision Analysis

Retain In-House

Outsource to Fleet

Management

Services

Difference

Annual leasing fee for software

$ 8,000

$ –

$ 8,000

Annual maintenance of trucks

154,000

–

154,000

Total annual salaries of five other

fleet management employees

145,000

–

145,000

Fleet Management Services’

–

annual fee

–

276,000

(276,000)

Total cost

$307,000

$276,000

Cost savings from outsourcing

$ 31,000

Operating income for Wheeler Food will increase by $31,000 by outsourcing the fleet-management function.

(5-10 min.) S8–12

In addition to the quantitative analysis, Riley should consider the following qualitative factors before making a final

decision:

(5-10 min.) S8–13

The $78,720 inventoriable cost (book value) of the inventory is a sunk cost that will be the same whether the remote

entry keys are sold as is or processed further. Consequently, the book value of the inventory is not relevant to the

(5-10 min.) S8–14

Sell as Cocoa

Powder

Sell as Chocolate

Syrup

Sell as Boxed Assorted

Chocolates

Revenue

$15,000

$101,000

$200,000

Less: Additional processing costs

0

(69,000)

(180,000)

Net benefit to operating income

$15,000

$ 32,000

$ 20,000

The company president made the wrong decision. First, the cost of processing the cocoa beans is irrelevant since it will

be incurred no matter which of the three products is sold. Second, in addition to the revenues, the additional costs of

transforming the cocoa powder into other products needs to be considered.

(5-10 min.) S8-15

1.

Stanley does not know how to categorize fixed costs as

unavoidable or avoidable so he guesses on the

categorization of each fixed cost.

Competence – Perform professional duties in

accordance with relevant laws, regulations, and

technical standards.

2.

Connor Advertising Agency is looking at whether to

continue to do its own payroll in-house or to outsource

it to a payroll firm (a classic “make or buy” decision.)

Elsie, an accountant at Connor, does not tell

management that the payroll firm bidding on the work

is owned and managed by her mother.

Integrity – Mitigate actual conflicts of interest,

regularly communicate with business associates

to avoid apparent conflicts of interest. Advise all

parties of any potential conflicts.

3.

Sarah is a management accountant at a large

electronics firm. She is instructed to prepare an analysis

of the performance of an underperforming company

division. Since Sarah is afraid that many employees

could lose their jobs if that division appears to be

underperforming, Sarah underestimates the amount of

expenses generated by that division. Sarah hopes that

the division is not discontinued.

Credibility – Disclose all relevant information

that could reasonably be expected to influence

an intended user’s understanding of the

reports, analyses, or recommendations.

4.

Latoya, a CPA and a CMA, makes a YouTube video

bragging about loopholes she has found to avoid taxes.

These loopholes are questionable at best.

Integrity – Abstain from engaging in or

supporting any activity that might discredit the

profession.

5.

Seymour is the controller for a small manufacturer. He

mentions to a close friend that his company is going to

start offshoring production to decrease labor costs.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

(5-10 min.) E8-16A

Item

Relevant

Irrelevant

a.

Book value of old machine

X

b.

Maintenance cost of new machine

X

c.

Maintenance cost of old machine

X

d.

Installation cost of new machine

X

e.

Accumulated depreciation on old machine

X

f.

Cost per pound of food to be processed

X

g.

Installation cost of old machine

X

h.

Cost of the new machine

X

i.

Cost of the old machine

X

j.

Added profits from the increase in production resulting

from the new machine

X

k.

Fixed selling costs

X

l.

Variable selling costs

X

m.

Trade-in value of old machine

X

n.

Interest expense on new machine

X

o.

Sales tax paid on old machine

X

Chapter 8 Relevant Costs for Short-Term Decisions

(10-15 min.) E8-17A

Req. 1

Hobby Memorabilia & More

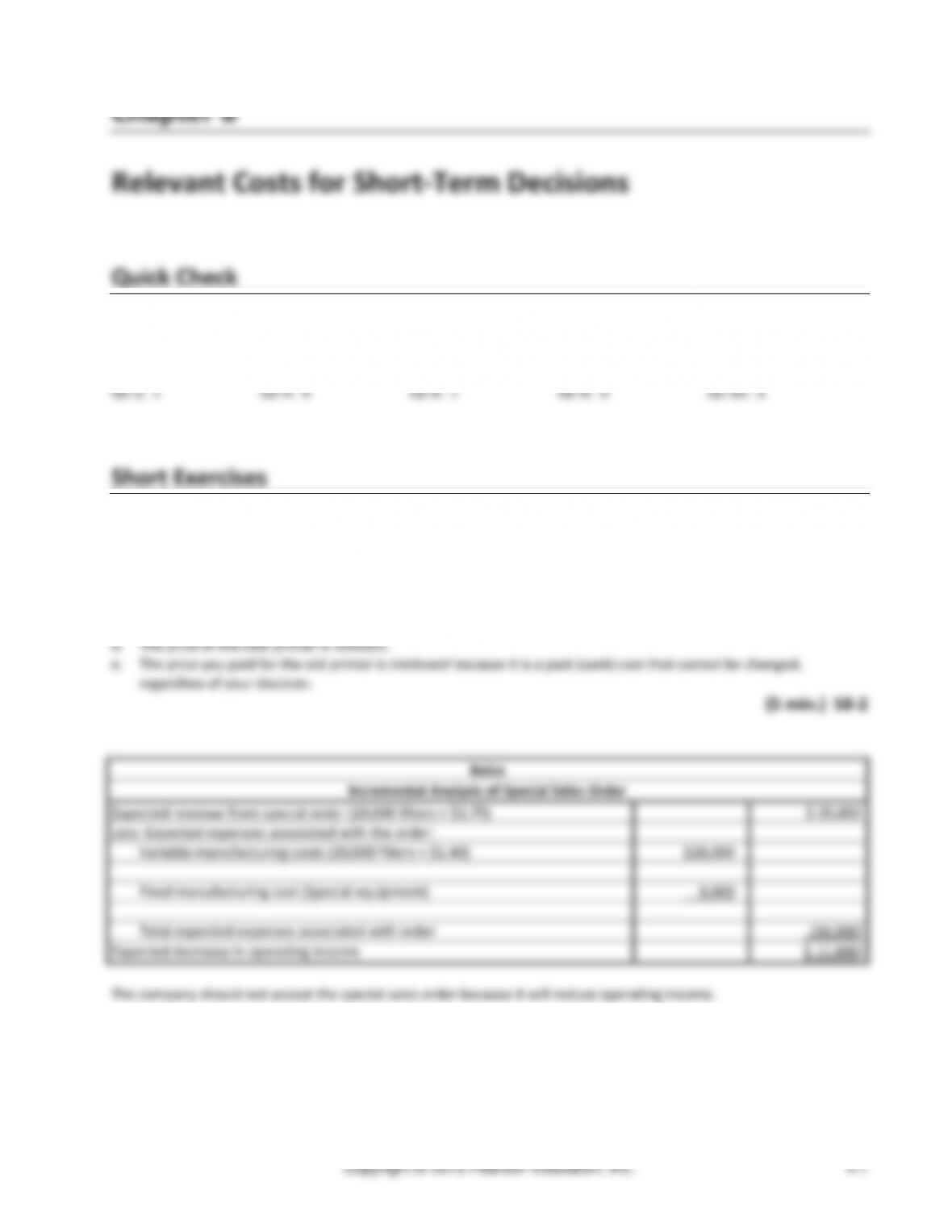

Incremental Analysis of Special Sales Order

Revenue from special order:

Sale of 58,000 packs × $0.43 each

$ 24,940

Less expenses associated with the order:

Variable manufacturing cost: 58,000 packs × $0.33 each ($0.14 + $0.08 + $0.11)

(19,140)

Increase in operating income from the order

$ 5,800

__________

Decision: Accept the special sales order.

Req. 2

Hobby Memorabilia & More

Incremental Analysis of Special Sales Order

Revenue from special order

(Sale of 58,000 packs × $0.43 each)

$ 24,940

Less variable expenses associated with the order:

Variable manufacturing cost: (58,000 × $0.33)

19,140

Contribution margin

5,800

Less: Additional fixed manufacturing costs associated with order

5,500

Increase in operating income from order

$ 300

Decision: Accept the special sales order.

(10-15 min.) E8-18A

Req. 1

(000s omitted)

Bid price

$ 34,500

Less scrap value

$ 32,800

Net cost of recycling

$ 1,700

Versus: Cost to sink

$ 700

Net difference in favor of sinking

$ 1,000

Financially, it is $1,000,000 more advantageous to sink the ship rather than recycle it.

Req. 2

From a sustainability standpoint, the decommissioned aircraft carrier should be dismantled and recycled.

The following qualitative factors should be considered into this analysis:

1. Jobs creation in record-high unemployment rates geographic region.

2. Materials are recycled and used for a different purpose

3. Toxins are not released into the ocean.

Chapter 8 Relevant Costs for Short-Term Decisions

(10-15 min) E8-20A

Req. 1

Preston will need to emphasize a target-costing approach to pricing. Because the tract homes are not unique and face

stiff competition, Preston will not have much control over pricing.

Managerial Accounting 4e Solutions Manual

(continued) E8-21A

Req. 3

Family Tyme Movies

Analysis of Dropping the DVD Product Line

Expected decrease in DVD revenue

$126,000

Expected decrease in DVD expenses:

Variable expenses

$80,000

Fixed expenses

74,000

154,000

Expected increase in operating income

28,000

Lost contribution margin on Blu-ray Discs (10% × $146,000)

(14,600)

Net expected increase in operating income

$ 13,400

Decision: Consider dropping DVDs because, assuming that all $74,000 of fixed costs assigned to the DVD product line

can be avoided but that Blu-ray production and sales would decline 10%, the product’s incremental revenues is now

less than its incremental costs.

(10-15 min.) E8-22A

First, we need to separate the fixed and variable costs:

Cost of goods sold:

$6,450,000 × 40% = $2,580,000 fixed manufacturing costs

Expected decrease in revenue

Expected decrease in expenses:

4,920,000

Expected decrease in total expenses

Expected increase (decrease) in operating income

Chapter 8 Relevant Costs for Short-Term Decisions

(15 min.) E8-23A

TreadLight

Product Mix Analysis

Deluxe

Regular

Sale price per unit

$1,020

$580

Less: Variable costs per unit

689a

449b

Contribution margin per unit

331

131

Units produced with equivalent number of machine hours

× 1

× 2

Contribution margin for equivalent number of machine hours

$ 331

$262

a ($320 + $ 88 + $168 + $113)

b ($110 + $186 + $ 84 + $ 69)

This is a product mix decision. TreadLight should produce the product with the highest contribution margin per unit of

the constraint.

Two times as much overhead cost is allocated to each Deluxe model as to each Regular model. Thus, it takes two times

as many machine hours to produce a Deluxe model.

For each unit of the Deluxe model produced (contributing $331 to operating income), TreadLight can produce two units

of the Regular model (contributing $262 to operating income).

Therefore, TreadLight should produce only the Deluxe model (if it has unlimited demand for the Deluxe model).

Chapter 8 Relevant Costs for Short-Term Decisions

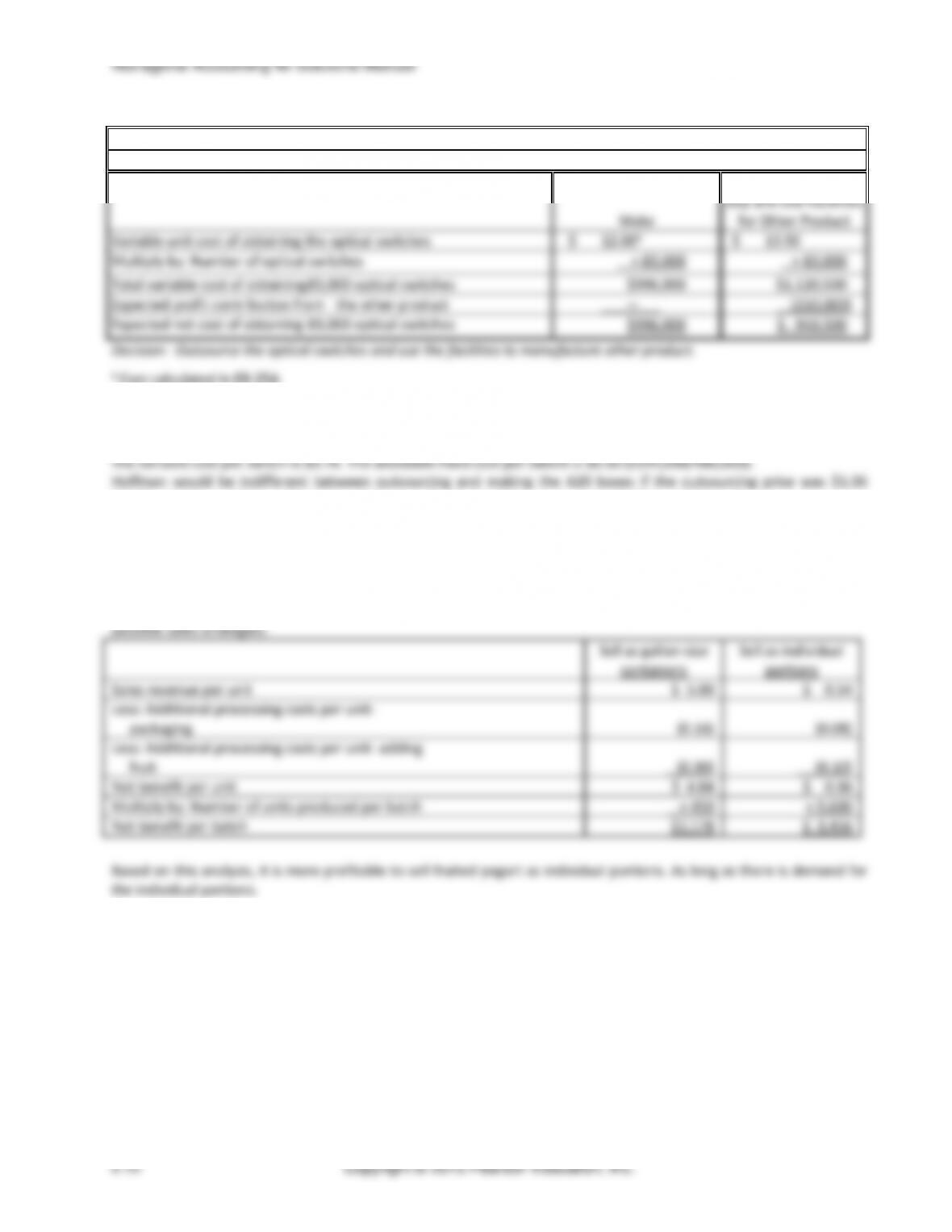

(10-15 min.) E8-25A

Req. 1

TechSystems

Incremental Analysis for Outsourcing Decision

Make Unit

Buy Unit

Difference

Variable cost per unit:

Direct materials

$ 9.00a

$ —

$ 9.00

Direct labor

2.00b

—

2.00

Variable overhead

1.00c

—

1.00

Purchase price from outsider

—

13.50

(13.50)

Variable cost per unit

$12.00

$13.50

$ (1.50)

a $612,000 / 68,000 = $9.00/unit

b $136,000 / 68,000 = $2.00/unit

c $68,000 / 68,000 = $1.00/unit

Decision: Make the optical switch because the cost per unit to make the switch is less than the variable cost per unit to

buy the switch.

Req. 2

Make switches

Buy switches

Variable cost per unit (from part 1)

$ 12.00

$ 13.50

Multiply by: Units needed

73,000

73,000

Total variable costs

$ 876,000

985,500

Plus: Fixed costs

408,000

311,000*

Total relevant costs

$1,284,000

$1,296,500

*($408,000 − $97,000 avoidable)

Decision: Make the optical switch because the total relevant costs to make the switches are less than the total relevant

costs to buy the switches.

Req. 3

Cost if making switches

=

Cost of outsourcing switches

Variable costs + fixed costs

=

Variable costs + fixed costs

($12.00 × 73,000) + $408,000

=

(x)* (73,000) + $311,000

$876,000 + $408,000

=

73,000x + $311,000

$973,000

=

73,000x

$13.33 (rounded)

=

x

* Where x = outsourcing cost per switch

Chapter 8 Relevant Costs for Short-Term Decisions

Exercises (Group B)

(5-10 min.) E8–29B

Item

Relevant

Not Relevant

a.

Cost of the new machine

X

b.

Cost of the old machine

X

c.

Added profits from increase in production resulting

from the new machine

X

d.

Fixed selling costs

X

e.

Variable selling costs

X

f.

Sales value of old machine

X

g.

Interest expense on new machine

X

h.

Interest expense on old machine

X

i.

Book value of old machine

X

j.

Maintenance cost of new machine

X

k.

Repairs and maintenance costs of old machine

X*

l.

Installation costs of new machine

X

m.

Accumulated depreciation on old machine

X

n.

Cost per pound of hamburger

X

o.

Installation cost of old machine

X

*Considered as future repairs and maintenance costs of the old machine.

Chapter 8 Relevant Costs for Short-Term Decisions

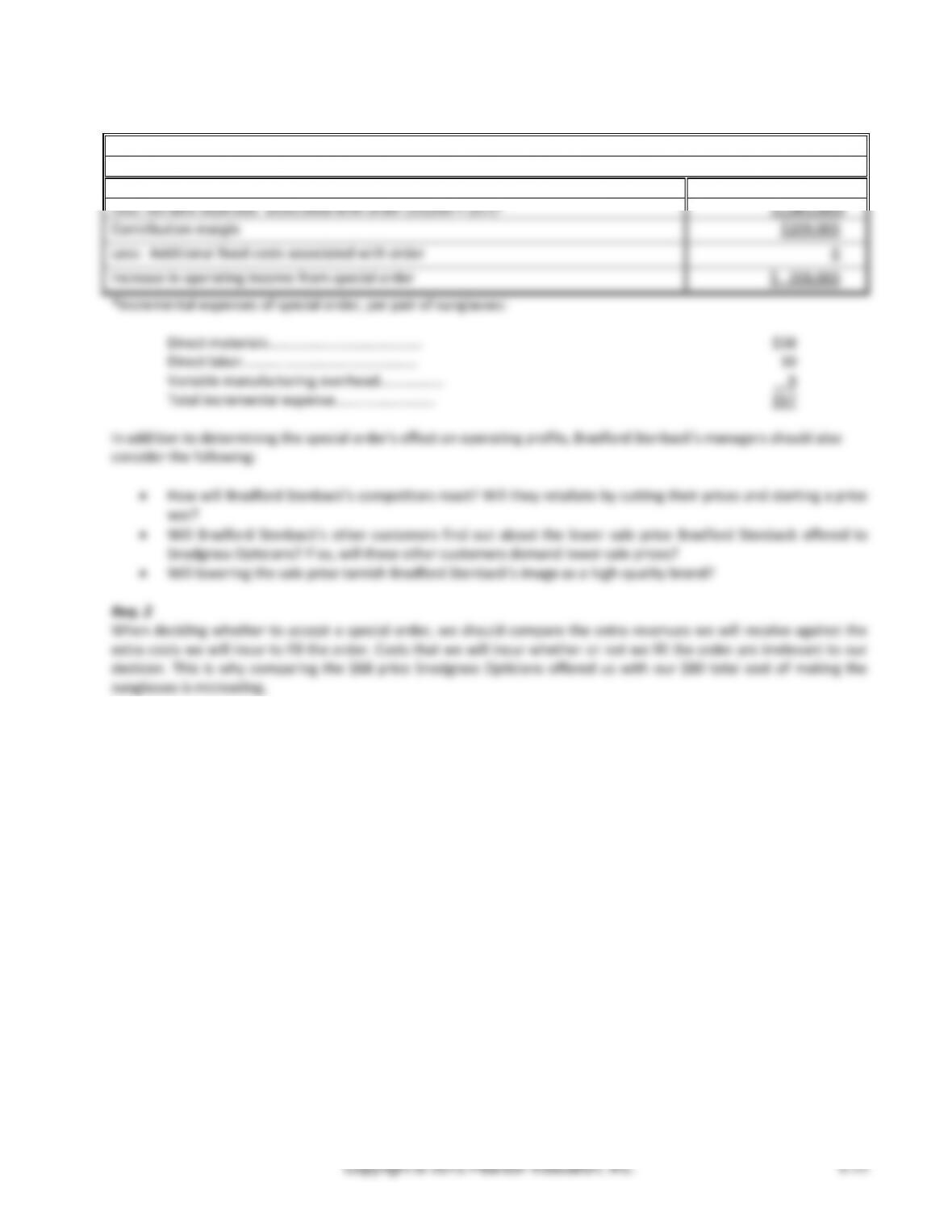

(20-25 min.) E8-32B

Req. 1

Bradford Stenback

Incremental Analysis of Special Sales Order

Revenue from special order (19,000 × $68)

$1,292,000

Less: variable expenses associated with order (19,000 × $57)*

(1,083,000)

Contribution margin

$209,000

Less: Additional fixed costs associated with order

0

Increase in operating income from special order

$ 209,000

*Incremental expenses of special order, per pair of sunglasses:

Direct materials…………………………………….

$38

Direct labor………………………………………….

10

Variable manufacturing overhead………………

9

Total incremental expense……………………….

$57

In addition to determining the special order’s effect on operating profits, Bradford Stenback’s managers should also

consider the following:

• How will Bradford Stenback’s competitors react? Will they retaliate by cutting their prices and starting a price

war?

• Will Bradford Stenback’s other customers find out about the lower sale price Bradford Stenback offered to

Snodgrass Opticians? If so, will these other customers demand lower sale prices?

• Will lowering the sale price tarnish Bradford Stenback’s image as a high-quality brand?

Req. 2

When deciding whether to accept a special order, we should compare the extra revenues we will receive against the

extra costs we will incur to fill the order. Costs that we will incur whether or not we fill the order are irrelevant to our

decision. This is why comparing the $68 price Snodgrass Opticians offered us with our $80 total cost of making the

sunglasses is misleading.

Managerial Accounting 4e Solutions Manual

(10-15 min) E8–33B

Req. 1

Bennett will need to emphasize a target-costing approach to pricing. Because the tract homes are not unique and face

stiff competition, Bennett will not have much control over pricing.