Copyright © 2015 Pearson Education, Inc.

7-56

(30-45 min.) P7-64B

Req. 1

Cost-Volume-Profit Analysis

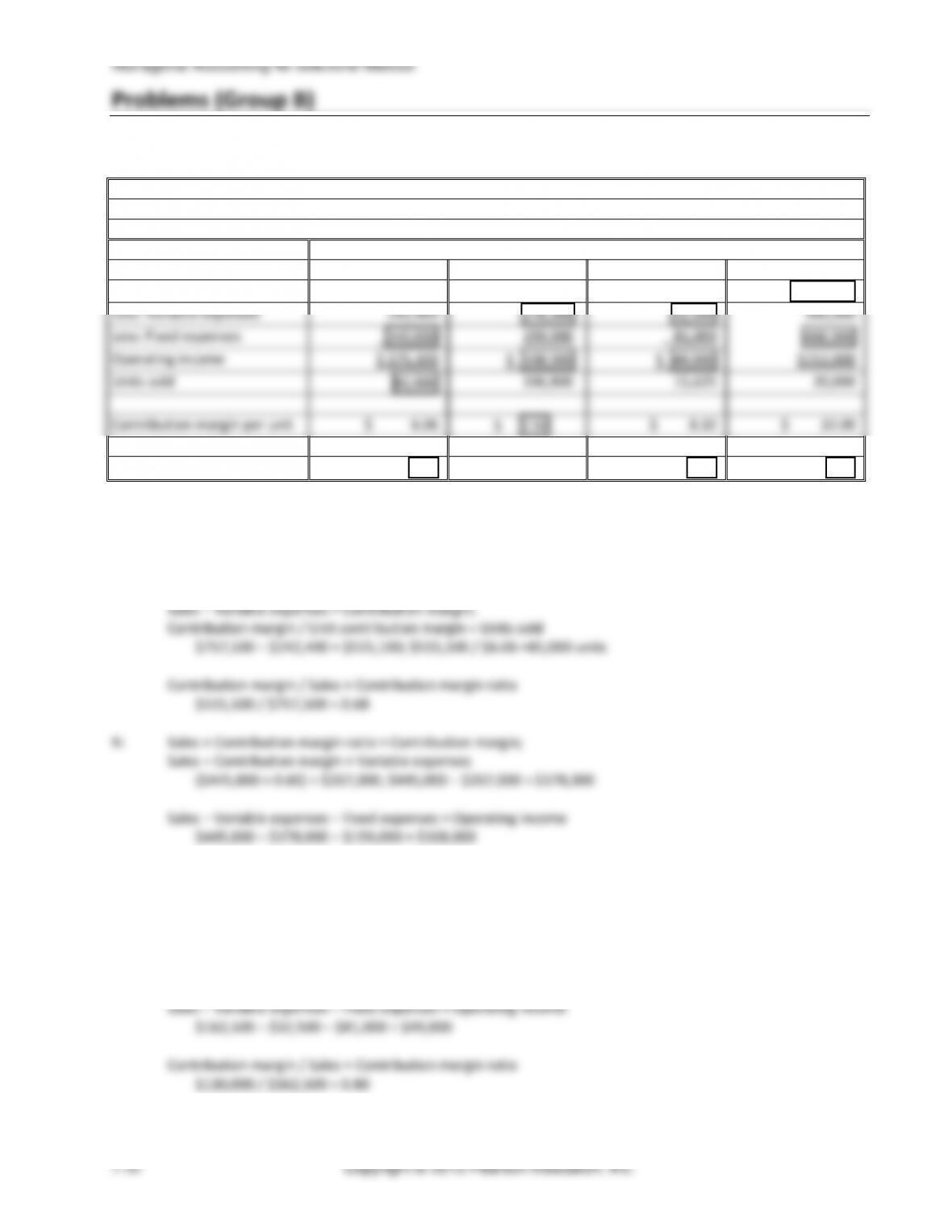

Companies Q, R, S, T

COMPANY

Q

R

S

T

Target sales

$757,500

$445,000

$162,500

$1,000,000

Less: Variable expenses

242,400

178,000

32,500

360,000

Less: Fixed expenses

340,000

159,000

81,000

488,000

Operating income

$ 175,100

$ 108,000

$ 49,000

$152,000

Units sold

85,000

106,800

15,625

20,000

Contribution margin per unit

$ 6.06

$ 2.50

$ 8.32

$ 32.00

Contribution margin ratio

0.68

0.60

0.80

0.64

Computations (top to bottom for each company)

Q: Sales − Variable expenses − Operating income = Fixed expenses

$757,500 − $242,400 − $175,100 = $340,000

Contribution margin / Units sold = Contribution margin per unit

$267,000 / 106,800 = $2.50

S: Units sold × Unit contribution margin = Contribution margin;

Sales − Contribution margin = Variable expenses

15,625 × $8.32 = $130,000; $162,500 − $130,000 = $32,500

Chapter 7 Cost-Volume-Profit Analysis

(continued) P7-64B

T: Units sold × Unit contribution margin = Contribution margin;

Contribution margin + Variable expenses = Sales

20,000 × $32.00 = $640,000; $640,000 + $360,000 = $1,000,000

(30-45 min.) P7-65B

Req. 1

Revenue per show:

1,400 tickets × $65 / ticket…..……………….…………

$91,000

Variable expenses per show:

Programs: 1,400 guests × $6 / guest……….……….…

$ 8,400

Cast: 65 cast members × $320 / cast member………

20,800

Total variable expenses per show…………………..…..

$29,200

Managerial Accounting 4e Solutions Manual

(continued) P7-65B

Req. 2

Sales revenue

−

Variable expenses

−

Fixed expenses

=

Operating income

Revenue

Number

Variable

Number

per

×

of

−

exp. per

×

of

−

Fixed expenses

=

Operating income

show

shows

show

shows

Number

Number

$91,000

×

of

−

$29,200

×

of

−

$2,163,000

=

$0

shows

shows

($91,000 – $29,200) × Number of shows

=

$2,163,000

$61,800 × Number of shows

=

$2,163,500

Number of shows

=

$2,163,500

$61,800

Breakeven number of shows

=

35 shows

Req. 3

Contribution margin

=

$91,000 − $29,200

=

$61,800

Target number of shows

=

Fixed expenses + Target operating income

Contribution margin per unit

Target number of shows

=

$2,163,000 + $3,708,000

$61,800

Target number of shows

=

$5,871,000

$61,800

Target number of shows

=

95 shows

Chapter 7 Cost-Volume-Profit Analysis

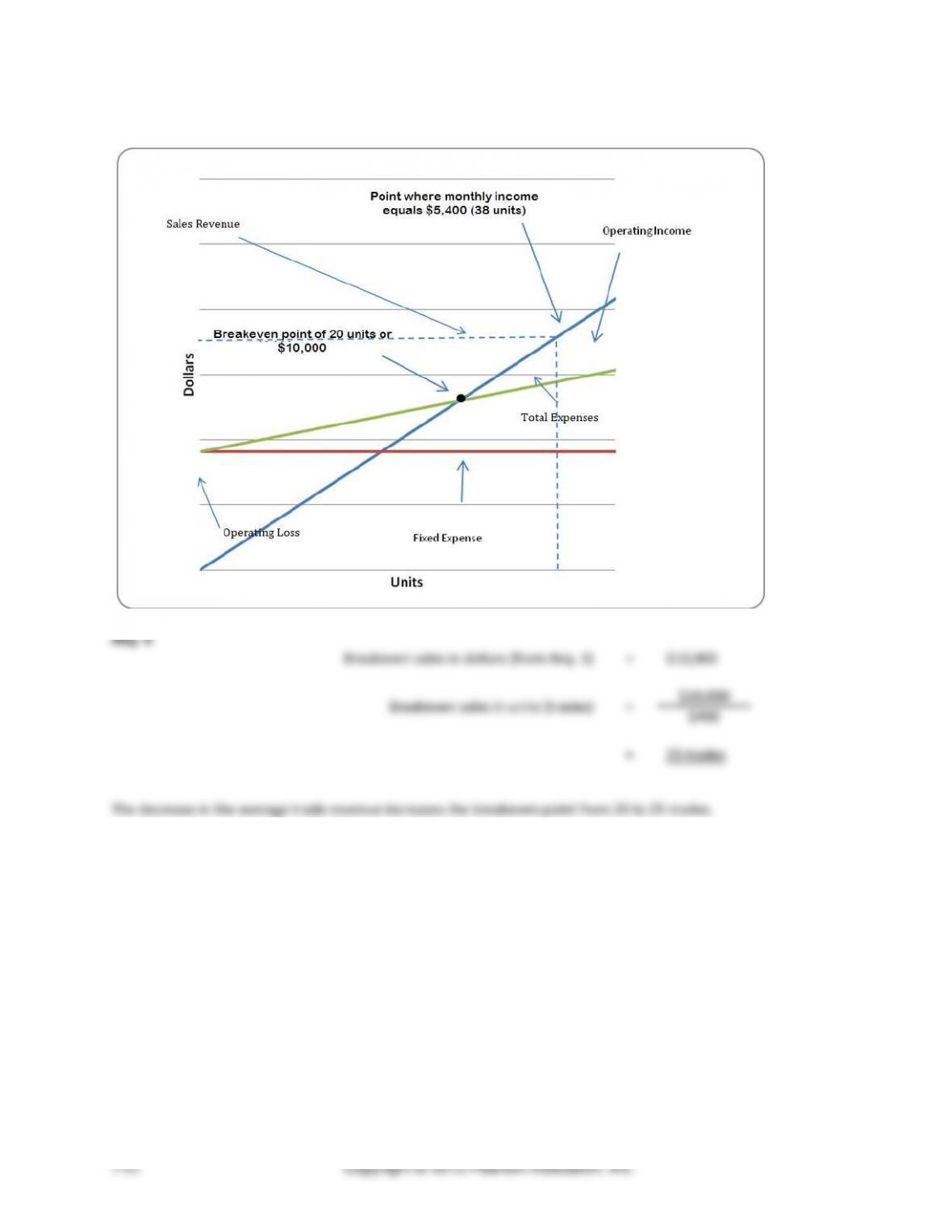

(30-45 min.) P7-66B

Managerial Accounting 4e Solutions Manual

(continued) P7-66B

Req. 4

Margin of safety

=

Sales − Sales at breakeven

Margin of safety

=

$9,262,500− (75,000 cartons × $19.50 per carton)

Margin of safety

=

$9,262,500− $1,462,500

Margin of safety

=

$7,800,000

Operating leverage factor

$7,125,000 / $6,000,000

Operating leverage factor

1.188 (rounded)

Managerial Accounting 4e Solutions Manual

(continued) P7-67B

Req. 3

Chapter 7 Cost-Volume-Profit Analysis

(25-35 min.) P7-68B

Req. 1

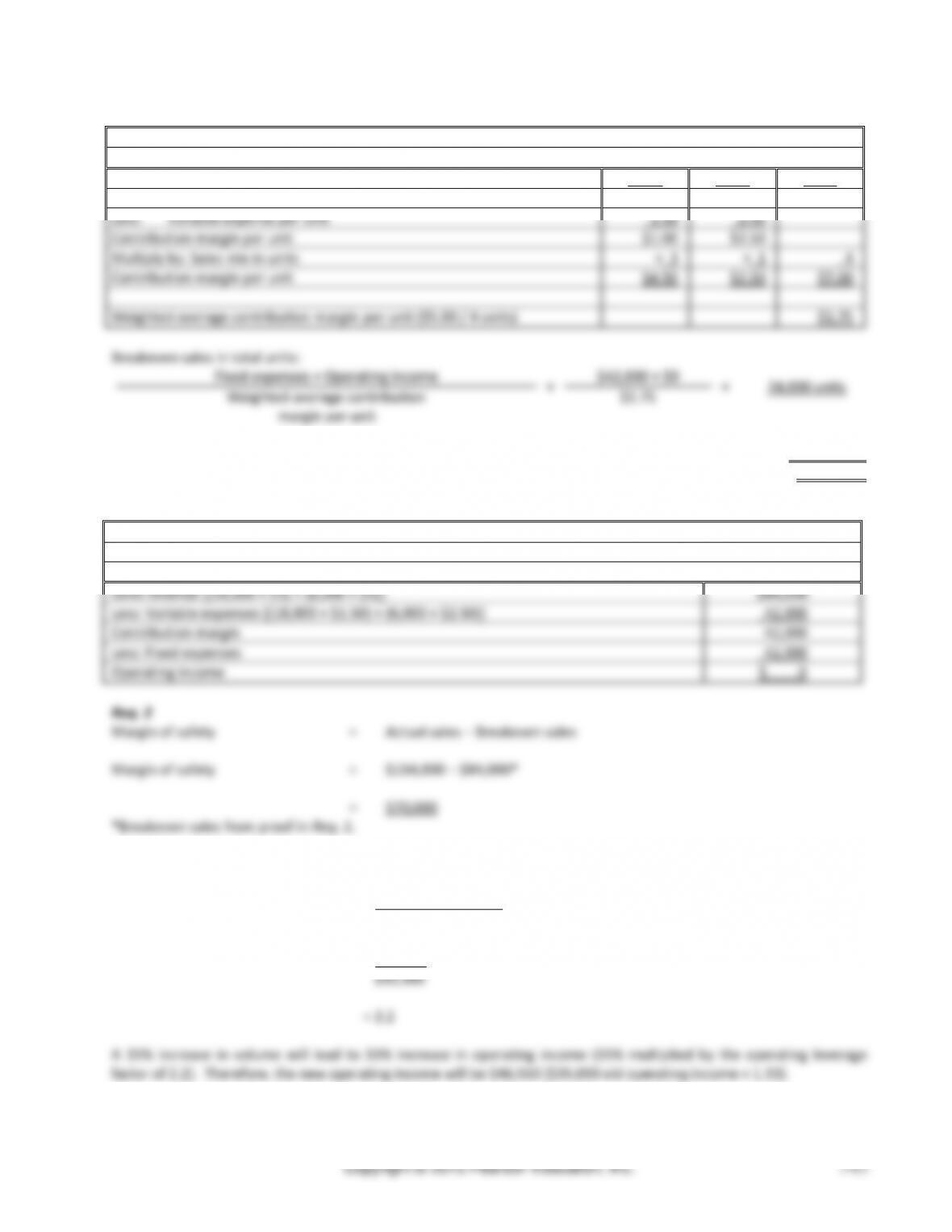

Margot Coffee

Weighted-Average Contribution Margin per Unit

Small

Large

Total

Sale price per unit

$3.00

$5.00

Less: Variable expense per unit

1.50

2.50

Contribution margin per unit

$1.00

$2.50

Multiply by: Sales mix in units

× 3

× 1

4

Contribution margin per unit

$4.50

$2.50

$7.00

Weighted-average contribution margin per unit ($5.00 / 4 units)

$1.75

Breakeven sales in total units:

Fixed expenses + Operating income

=

$42,000 + $0

=

24,000 units

Weighted-average contribution

$1.75

margin per unit

Breakeven sales of small coffees (24,000 × ¾)……..

18,000 units

Breakeven sales of large coffees (24,000 × ¼)……..

6,000 units

Proof:

Margot Coffee

Contribution Margin Income Statement

Month Ended February 29

Sales revenue [(18,000 × $3) + (6,000 × $5)]

$84,000

Less: Variable expenses [(18,000 × $1.50) + (6,000 × $2.50)]

42,000

Contribution margin

42,000

Less: Fixed expenses

42,000

Operating income

$ 0

Req. 2

Margin of safety

=

Actual sales − Breakeven sales

Margin of safety

=

$154,000 − $84,000*

=

$70,000

*Breakeven sales from proof in Req. 1.

Req. 3

Operating leverage factor:

= Contribution margin

Operating income

= $77,000

Managerial Accounting 4e Solutions Manual

(continued) P7-68B

Proof:

Margot Coffee

Effect on Operating Income of 15% Increase in Sales Volume

Increase in sales revenue ($154,000 × 0.15)

$23,100

Increase in variable expenses ($77,000 × 0.15)

11,550

Increase in contribution margin

11,550

Change in fixed expenses

0

Operating income before sales increase

35,000

Operating income after sales increase

$46,550

Effect on Operating Income of 15% Increase in Sales Volume

Sales revenue ($154,000 × 1.15)

Variable expenses ($77,000 × 1.15)

88,550

Contribution margin

88,550

Fixed expenses

42,000

Operating income

Copyright © 2015 Pearson Education, Inc.

7-65

A7–69

1. Define breakeven point. Why is the breakeven point important to managers?

1. the breakeven point

3. how changes in costs, sales price, and volume affect the company’s profit and

3. The purchasing manager for Rockwell Fashion Bags has been able to purchase the material for its signature

handbags for $2 less per bag. Keeping everything else the same, what effect would this reduction in material

cost have on the breakeven point for Rockwell Fashion Bags? Now assume that the sales manager decides to

4. Describe three ways that cost-volume-profit concepts could be used by a service organization.

C-V-P can be used by a service organization to help them determine:

2. the volume needed to reach target profit and

5. “Breakeven analysis isn’t very useful to a company because companies need to do more than break even to

survive in the long run.” Explain why you agree or disagree with this statement.

6. What conditions must be met for cost-volume-profit analysis to be accurate?

The following conditions must be met for C-V-P analysis to be accurate:

• A change in volume is the only factor that affects costs.

Managerial Accounting 4e Solutions Manual

7. Why is it necessary to calculate a weighted-average contribution margin ratio for a multiproduct company when

calculating the breakeven point for that company? Why can’t all of the products’ contribution margin ratios just

8. Is the contribution margin ratio of a grocery store likely to be higher or lower than that of a plastics

manufacturer? Explain the difference in cost structure between a grocery store and a plastics manufacturer.

9. Alston Jewelry had sales revenues last year of $2.4 million, while its breakeven point (in dollars) was $2.2

million. What was Alston Jewelry’s margin of safety in dollars? What does the term margin of safety mean?

10. Rondell Pharmacy is considering switching to the use of robots to fill prescriptions that consist of oral solids or

medications in pill form. The robots will assist the human pharmacists and will reduce the number of human

pharmacy workers needed. This change is expected to reduce the number of prescription filling errors, to reduce

11. Suppose a company can replace the packing material it currently uses with a biodegradable packing material.

The company believes this move to biodegradable packing materials will be well received by the general public.

12. How can CVP techniques be used in supporting a company’s sustainability efforts? Conversely, how might CVP

be a barrier to sustainability efforts?

savings.

A7-70

Select one product that you could make yourself. Examples of possible products could be cookies, birdhouses, jewelry,

1. Describe your product. What market are you targeting this product for? What price will you sell your product

for? Make projections of your sales in units over each of the upcoming five years.

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

7-68

5. Now classify all of the expenses you have listed as being either fixed or variable. For mixed expenses, separate

the expense into the fixed component and the variable component.

Rent

Fixed

Utilities

Fixed

Insurance

Fixed

6. Calculate how many units of your product you will need to sell to breakeven in each of the five years you have

7. Calculate the margin of safety in units for each of the five years in your projection.

Margin of Safety = Projected Sales – Breakeven Sales

2012

2013

2014

2015

2016

150-26=124

175-26=149

200-26=174

225-26=199

250-26=224

$15,000-$2,600

$17,500 – $2,600

$20,000 – $2,600

$22,500 – $2,600

$25,000 –

$2,600

$12,400

$14,900

$17,400

$19,900

$22,400

8. Now decide how much you would like to make in before-tax operating income (target profit) in each of the

upcoming five years. Calculate how many units you would need to sell in each of the upcoming years to meet

9. How realistic is your potential venture? Do you think you would be able to break even in each of the projected

five years? How risky is your venture (use the margin of safety to help answer this question). Do you think your

Chapter 7 Cost-Volume-Profit Analysis

(30 min.) A7-71

Ethics Mini-Case

1.

a. The ethical issues in this situation are:

Competence: “Provide decision support information and recommendations that are accurate, clear, concise,

2. By omitting the fixed monthly sales staff salaries from the report, breakeven sales are reported as lower than they

3. First, Greg should report the mistake with his immediate supervisor. If he has concerns about his employment with

1. Is the cost of down a fixed cost or a variable cost for a jacket manufacturer such as Lands’ End?

Down is a variable cost to jacket manufacturers because more down is required for each additional unit (jacket)

produced.

2. If the cost of down increases, what happens to the breakeven point for a down-filled jacket product line at

3. What is the percentage increase in the cost of down per pound from 2010 to 2012 at Land’s End? Would you

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

7-70

costs are assumed to have stayed the same, the actual total cost of making the jacket will increase by a smaller

total percentage. Therefore, the breakeven in units will increase by a smaller amount than 77%.

4. If down increases by a certain percentage, will the selling price of a down-filled jacket need to change by that

same percentage to maintain the same profit margin? Explain.

5. Assume that a Land’s End down jacket selling for $100 uses 12 ounces of down. Further assume that Lands’ End

has $250,000 of fixed costs related to the down jacket line and its other variable manufacturing costs total $60

6. Assume now the same set of facts as in Question 5 but that Lands’ End raises the selling price of each jacket by

$10 in October 2013. Does the contribution margin percentage remain the same?

No, the contribution margin would increase, this is because Lands’ End only uses 12 ounces of down in each jacket