Chapter 7 Cost-Volume-Profit Analysis

(15 min.) E7-53B

Req. 1

Contribution margin ratio

=

1.00 − 0.40

=

0.60

Breakeven sales in dollars

=

Fixed expenses + Operating income

Contribution margin ratio

=

$7,500 + $0

0.60

=

$12,500

$7,500 + $30,000

$62,500

$62,500 − $12,500

$50,000

=

Managerial Accounting 4e Solutions Manual

(10 min.) E7-54B

First, find the contribution margin:

Sales………………………………

$45,000

Contribution margin ratio……..

× .20

Contribution margin……………

$ 9,000

Contribution margin……..

$9,000

Less: Fixed expenses….

Unknown

Operating income………..

$ 5,625

(10-15 min.) E7-55B

Req. 1

Selling price $45

Less: Variable costs ($10 + $4 + $2) 16

CM per unit $29

Lease costs under Option A:

Fixed costs

$ 3,600

Variable costs (none)

0

Total costs under Option A

$ 3,600

Lease costs under Option B:

Fixed costs

$ 990

Total variable costs (20% x $45 x 190)

1,710

Total costs under Option B

$2,700

The more attractive lease option is Option B because it results in the lowest total lease costs.

Req. 2

To solve the question, you need to set the costs of Option A equal to the costs of Option B:

$3,600 = $990 + (20% x $45 x CANDLES)

Then solve for CANDLES:

CANDLES = 290

Req. 3

The lease option that is more attractive for the company if the company plans to sell 490 candles a month is option A,

the fixed lease payment because the sales volume is more than the indifference point.

Lease costs under option A: #3,600

Lease costs under option B: $990 + (20% x $45 x 490) = $5,400

Managerial Accounting 4e Solutions Manual

(continued) E7-56B

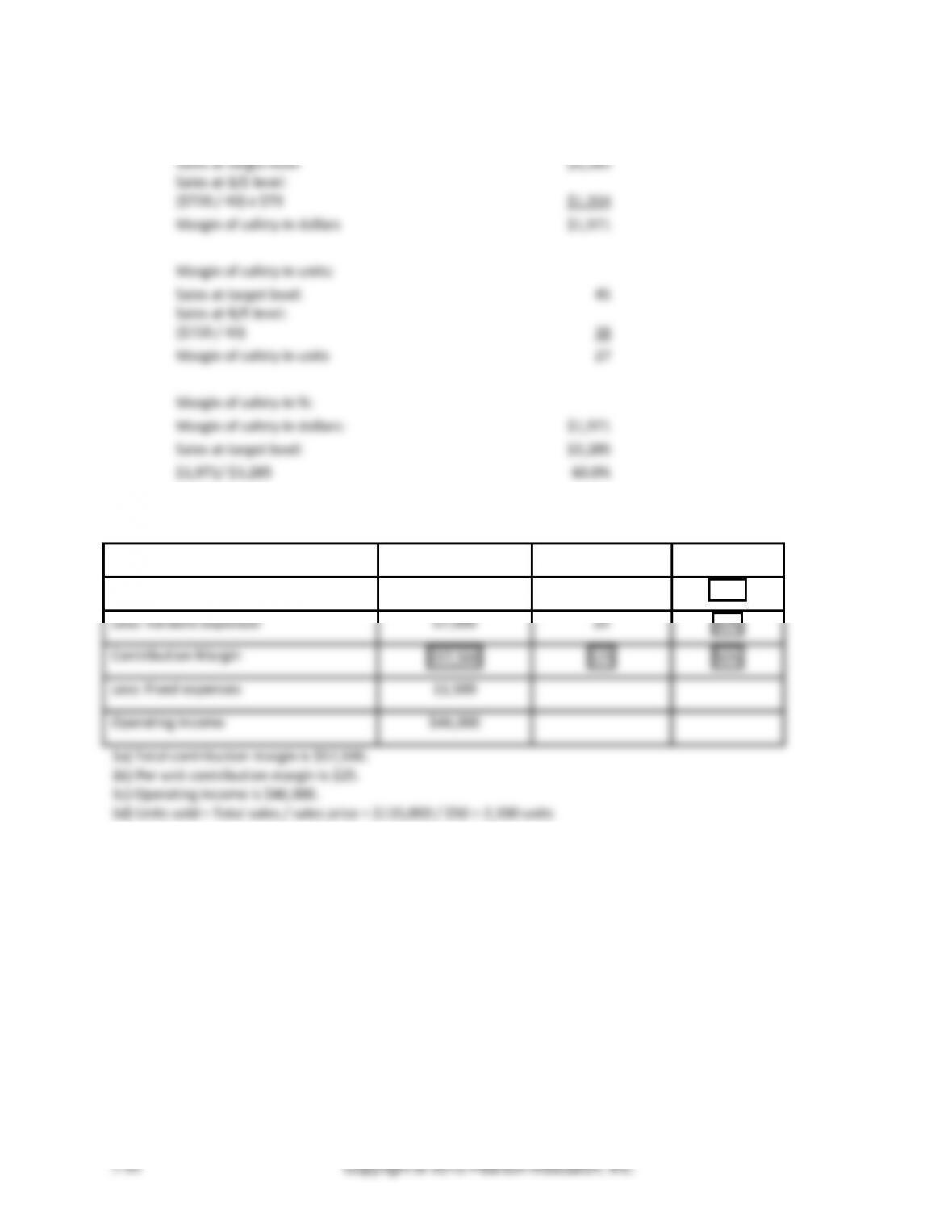

Req. 3

Margin of safety in dollars:

Sales at target level

$3,285

Sales at B/E level:

($720 / 40) x $73

$1,314

Margin of safety in dollars

$1,971

Margin of safety in units:

Sales at target level:

45

Sales at B/E level:

($720 / 40)

18

Margin of safety in units

27

Margin of safety in %:

Margin of safety in dollars:

$1,971

Sales at target level:

$3,285

$1,971/ $3,285

60.0%

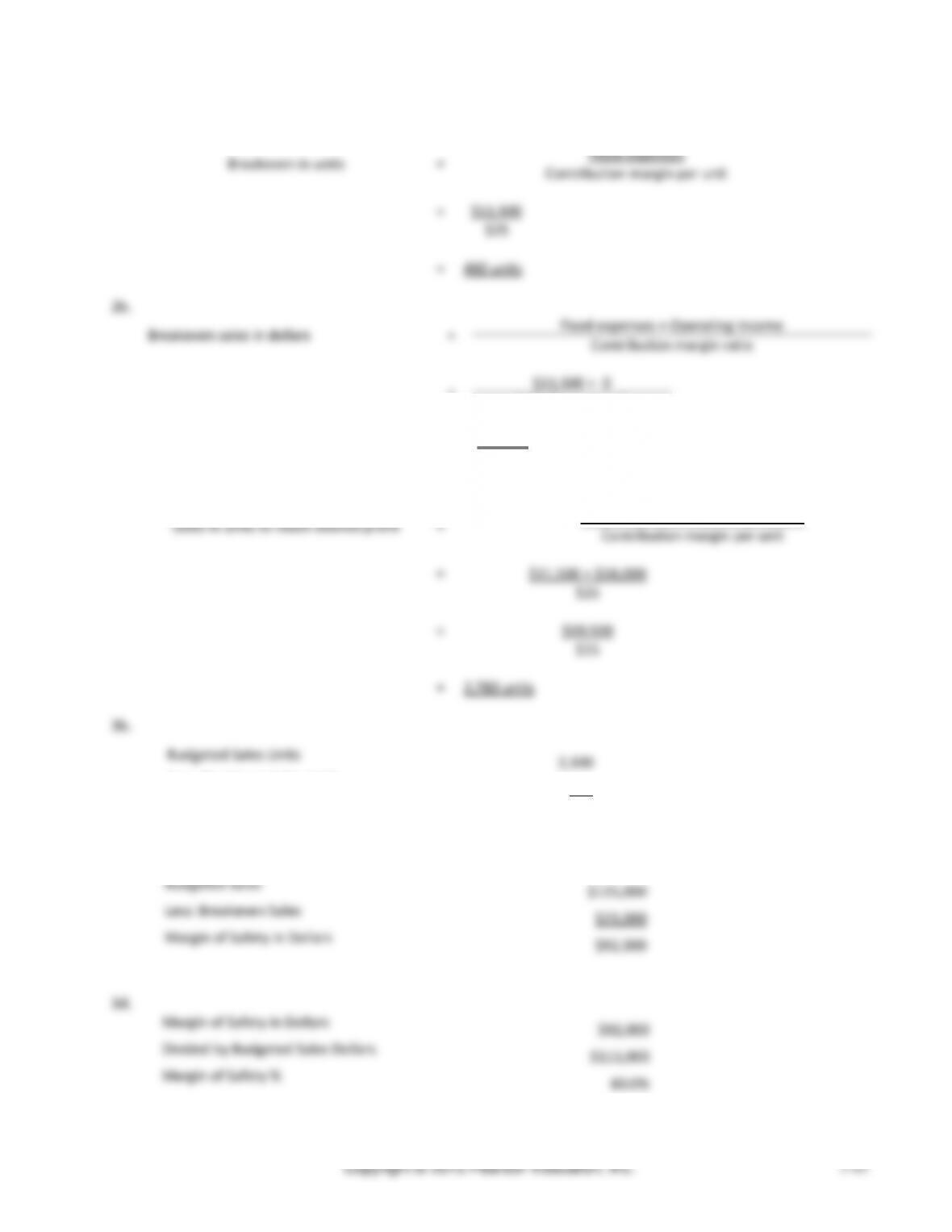

(20-25 min.) E7-57B

Req. 1

Total

Per Unit

%

Sales

$115,000

$50

100%

Less: Variable expenses

57,500

25

50%

Contribution Margin

$57,500

$25

50%

Less: Fixed expenses

11,500

Operating income

$46,000

1a) Total contribution margin is $57,500.

1b) Per unit contribution margin is $25.

1c) Operating income is $46,000.

1d) Units sold = Total sales / sales price = $115,000 / $50 = 2,300 units

Chapter 7 Cost-Volume-Profit Analysis

(continued) E7-57B

Req. 2

2a.

Breakeven in units

=

Fixed expenses

Contribution margin per unit

=

$11,500

$25

=

460 units

2b.

Breakeven sales in dollars

=

Fixed expenses + Operating income

Contribution margin ratio

=

$11,500 + 0

0.50 (from req. 1)

=

$23,000

Req. 3

3a.

Sales in units to reach desired profit

=

Fixed expenses + Operating Income

Contribution margin per unit

=

$11,500 + $58,000

$25

=

$69,500

$25

=

2,780 units

3b.

3c.

Less: Breakeven Sales

Margin of Safety in Dollars

Margin of Safety in Dollars

$92,000

Divided by Budgeted Sales Dollars

$115,000

Margin of Safety %

80.0%

Budgeted Sales Units

2,300

Less: Breakeven Sales Units

460

Margin of Safety in Units

1,840

Budgeted Sales

$115,000

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

7-46

(20-25 min.) E7-58B

1.

Sales price per unit……..………………………….

$25.00

Less: Variable cost per unit ($8.40+$8+$3.70+$1.90)……………………………..

$22.00

Contribution margin per unit…………..……………

$ 3.00

Contribution margin ratio

=

$3.00

=

.12

$25.00

=

12%

Sales Revenue (100,000 × $25.00)…………

$ 2,500,000

Less: Variable exp. (100,000 × $22.00)

(2,200,000)

Contribution margin……………….………..

$ 300,000

2.

Sales volume (units)…………………………

130,000

Unit contribution margin……………………

x $25.00

Contribution margin…………………………

$390,000

Less: Fixed expenses ($121,800+$167,100)………………………

(288,900)

Operating income……………………………

$101,100

3.

Sales revenue…………………………………

$4,000,000

Contribution margin ratio…………………..

x 12%

Contribution margin…………………………

$480,000

Less: Fixed expenses ($121,800+$167,100)………………………

(288,900)

Operating income……………………………

$ 191,100

4.

B/E sales in units

=

$288,900

=

96,300

$3.00

units

B/E sales in dollars

=

$288,900

=

$2,407,500

12%

5.

$288,900 + $260,100

=

183,000 units

$3.00

Chapter 7 Cost-Volume-Profit Analysis

(continued) E7-58B

6.

Original contribution margin per unit………………

$3.00

Less: Increase in Direct labor cost per unit ($8.00 x

10%)………………………………….………..…….

$0.80

New contribution margin per unit…………………

$2.20

Original fixed expenses…………………………….

$288,900

Plus: Increase in fixed expenses……………….

23,500

New fixed expenses…………………………………

$312,400

New breakeven in units

=

$312,400

=

142,000

$2.20

Units

7.

Contribution margin (from part 1)…………………

$300,000

Less: Fixed expenses……………………………..

(288,900)

Operating income……………………………………

$11,100

Operating leverage factor

=

$300,000

=

27.03 (rounded)

$11,100

8.

Increase in volume……………………..

3%

× Operating leverage factor…………..

27.03

New fixed expenses……………………

81.1% (rounded)

9.

Margin of safety

=

Sales − Sales at breakeven

=

$2,500,000 − $2,407,500

(from part 1) (from part 4)

=

$92,500

Margin of safety as a percentage

=

92,500

2,500,000

=

.037

=

3.7%

10.

16 GB

32 GB

Total

Sales price……………..

$25

$50

Less: Variable cost…………..

22

27

Contribution margin….

$ 3

$23

Multiply by: Sales mix……………….

× 9

× 1

10

Contribution margin….

$27

$23

$50

Weighted-average contribution margin per unit

$5.00

Sales in units

=

$121,800 + $167,100 + $260,100

=

109,800 units

$5.00

Smaller 16 GB: 109,800 × 9/10…………………

98,820 units

Larger 32 GB: 109,800 × 1/10….………………

10,980 units

Copyright © 2015 Pearson Education, Inc.

7-48

(30-45 min.) P7-59A

Req. 1

Cost-Volume-Profit Analysis

Companies Q, R, S, T

COMPANY

Q

R

S

T

Target sales

$625,000

$445,000

$236,000

$780,000

Less: Variable expenses

125,000

178,000

118,000

156,000

Less: Fixed expenses

370,000

159,000

94,000

493,000

Operating income

$130,000

$ 108,000

$ 24,000

$131,000

Units sold

80,000

106,800

12,500

16,000

Contribution margin per unit

$ 6.25

$ 2.50

$ 9.44

$ 39.00

Contribution margin ratio

0.80

0.60

0.50

0.80

Computations (top to bottom for each company)

Q: Sales − Variable expenses − Operating income = Fixed expenses

$625,000 − $125,000 − $370,000 = $130,000

Sales − Variable expenses = Contribution margin;

Chapter 7 Cost-Volume-Profit Analysis

(continued) P7-59A

T: Units sold × Unit contribution margin = Contribution margin;

Contribution margin + Variable expenses = Sales

16,000 × $39 = $624,000; $624,000 + $156,000 = $780,000

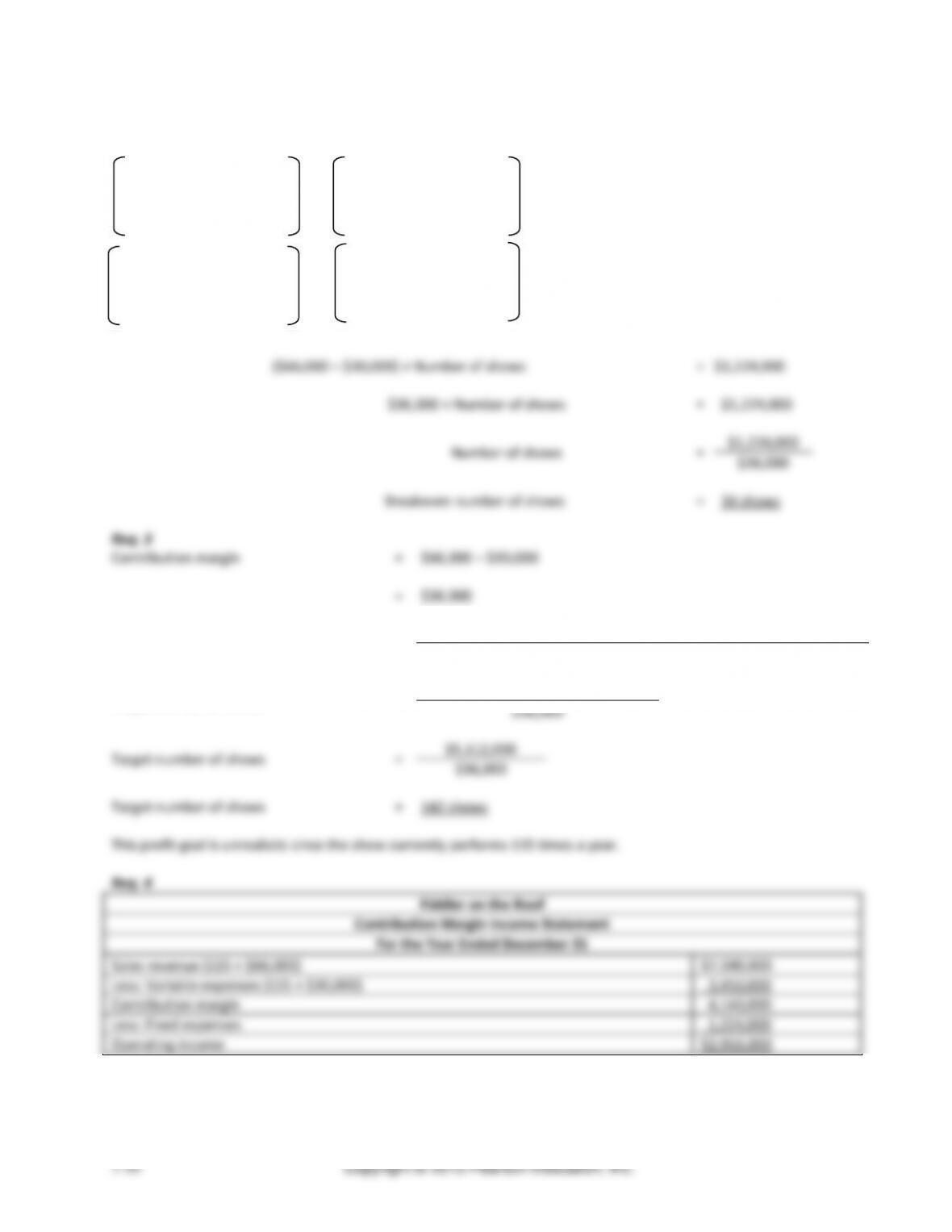

(30-45 min.) P7-60A

Req. 1

Revenue per show:

1,200 tickets × $55 / ticket…..……………….……………

$66,000

Variable expenses per show:

Programs: 1,200 guests × $9 / guest……….……….…

$ 10,800

Cast: 60 cast members × $320 / cast member………

19,200

Total variable expenses per show…………………..…..

$30,000

Managerial Accounting 4e Solutions Manual

(continued) P7-60

Sales revenue

−

Variable expenses

−

Fixed expenses

=

Operating income

Revenue

Number

Variable

Number

per

×

of

−

exp. per

×

of

−

Fixed expenses

=

Operating income

show

shows

show

shows

Number

Number

$66,000

×

of

−

$30,000

×

of

−

$969,000

=

$0

shows

shows

($66,000 – $30,000) × Number of shows

=

$1,224,000

$36,000 × Number of shows

=

$1,224,000

Number of shows

=

$1,224,000

$36,000

Breakeven number of shows

=

34 shows

Req. 3

Contribution margin

=

$66,000 − $30,000

=

$36,000

Target number of shows

=

Fixed expenses + Target operating income

Contribution margin per unit

Target number of shows

=

$1,224,000 + $3,888,000

$36,000

Target number of shows

=

$5,112,000

$36,000

Target number of shows

=

142 shows

Chapter 7 Cost-Volume-Profit Analysis

(30-45 min.) P7-61A

Managerial Accounting 4e Solutions Manual

(continued) P7-61A

Req. 4

Margin of safety

=

Sales − Sales at breakeven

Margin of safety

=

$7,425,000 − (109,500 cartons × $16.50 per carton)

Margin of safety

=

$7,425,000 − $1,806,750

Margin of safety

=

$5,618,250

Operating leverage factor

=

Contribution margin

Operating income

Operating leverage factor

=

$4,500,000

$3,405,000

Operating leverage factor

=

1.322 (rounded)

Req. 5

If volume increases 16%, then operating income will increase 21.15% (operating leverage factor of 1.322 multiplied by

16%).

Proof:

Original volume (cartons)…..……………………

450,000

Add: Increase in volume (16% × 450,000)…

72,000

New volume (cartons)…………………………

522,000

Multiplied by: Unit contribution margin………

$10.00

New total contribution margin………………

$5,220,000

Less: Fixed expenses……………………….

(1,095,000)

New operating income……………………….

$4,125,000

vs. Operating income before change in

volume……………………………………..

3,405,000

Increase in operating income……………….

$ 720,000

Percentage change ($720,000 / $3,405,000)

21.15% (rounded)

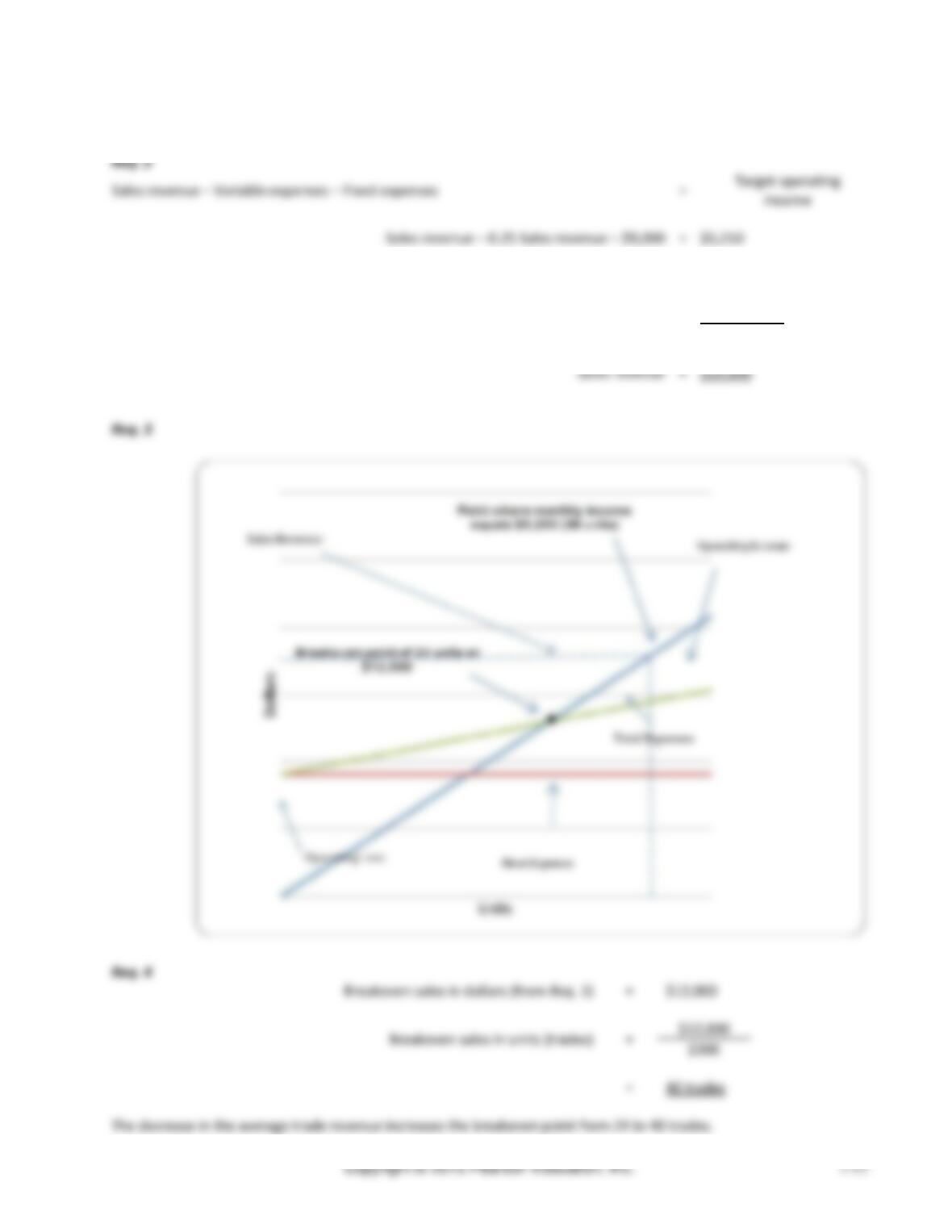

(30-45 min.) P7-62A

Req. 1

Contribution margin ratio

=

0.75 (computed as 1.00 − 0.12 − 0.04 − 0.03 − 0.06)

Monthly fixed expenses

=

$9,000 (computed as $2,700 + $280 + $250 + $600 + $650 +

$4,520)

Breakeven sales in dollars

=

Fixed expenses + Operating income

Contribution margin ratio

=

$9,000 + $0

0.75

=

$12,000

Breakeven sales in units

=

$12,000

(trades)

$500

=

24 trades

Chapter 7 Cost-Volume-Profit Analysis

(continued) P7-62A

Chapter 7 Cost-Volume-Profit Analysis

(continued) P7-63A

Req. 3

Operating leverage factor

= Contribution Margin