Chapter 7 Cost-Volume-Profit Analysis

Copyright © 2015 Pearson Education, Inc.

7-1

Chapter 7

Cost-Volume-Profit Analysis

Quick Check

Answers:

QC-1. d

QC-3. b

QC-5. a

QC-7. b

QC-9. c

QC-2. c

QC-4. c

QC-6. c

QC-8. b

QC-10. d

(5-10 min.) S7-1

a.

Sales price per passenger…………………….

$ 50

Less: Variable cost per passenger…………..

20

Contribution margin per passenger…………

$ 30

b.

Contribution margin per passenger…………

$30

Divided by sales price per passenger……….

÷ 50

Contribution margin ratio……………………..

60%

c.

Total contribution margin (11,000 × $30)……

$330,000

Less: Fixed expenses…………………………..

210,000

Operating income……………………………….

$120,000

d.

Total contribution margin

($490,000 × 60%) …………………………..

$294,000

Less: Fixed expenses…………………………..

210,000

Operating income……………………………….

$84,000

(5 min.) S7-2

The unit contribution margin tells managers how much income is earned on each unit of sales before considering fixed

Managerial Accounting 4e Solutions Manual

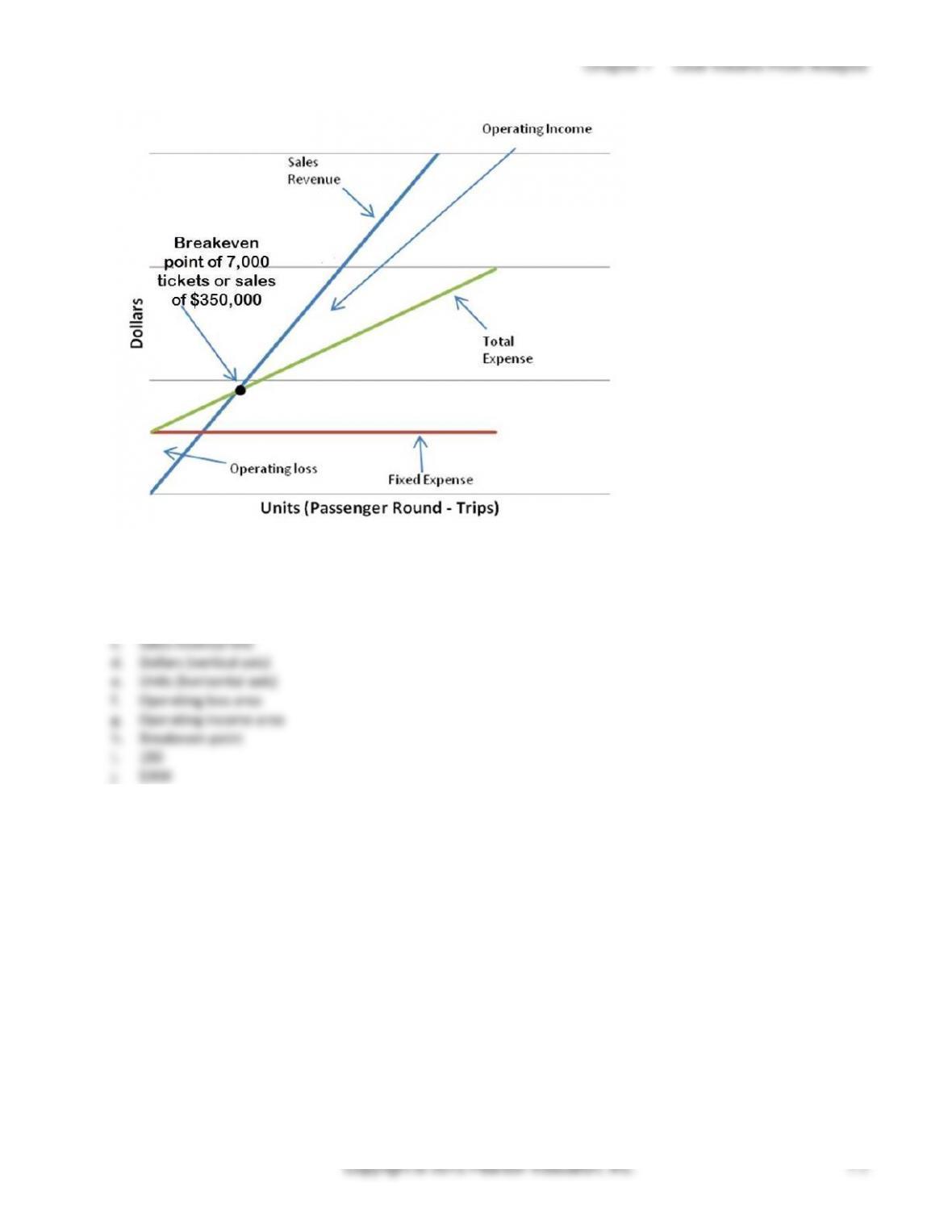

(5-10 min.) S7-3

Units sold

=

Fixed expenses + Operating income

(to break even)

Contribution margin per unit (passenger)

=

$210,000 + 0

$30*

=

7,000 passengers

*Contribution margin

=

$50 sales

−

$20 variable expense

per passenger

price

per passenger

(5 min.) S7-4

Sales in units

=

Fixed expenses + Operating income

Contribution margin per unit

=

$210,000 + $45,000

$30

=

8,500 dinner cruise tickets

Or, using the equation approach:

Sales revenue

−

Variable expenses

−

Fixed

=

Operating

expenses

income

Sale price Units

per unit × sold

−

Variable cost Units

−

Fixed

=

Operating

per unit × sold

expenses

income

[($50 × Units sold)

−

($20 × Units sold)]

−

$210,000

=

$45,000

[($50 − $20) × Units sold]

−

$210,000

=

$45,000

Units sold

=

8,500 tickets

To earn target income of $45,000, the cruiseline must sell 8,500 dinner cruise tickets.

Chapter 7 Cost-Volume-Profit Analysis

(continued) S7-7

Req. 2

If the variable cost decreases to $10, then the new unit contribution margin is $40 ($50 − $10). The new breakeven

point in units is:

=

Fixed expenses + Operating income

Sales in units

Contribution margin per unit

=

$210,000 + $0

$40

=

5,250 dinner cruise passengers

To achieve breakeven, sales revenue needs to be $262,500 (5,250 passengers × $50 sales price per ticket).

Or, using the equation approach:

Sales revenue

−

Variable expenses

−

Fixed

=

Operating

expenses

income

Sale price Units

per unit × sold

−

Variable cost Units

−

Fixed

=

Operating

per unit × sold

expenses

income

($50 × Units sold)

−

($10 × Units sold)

−

$210,000

=

$0

[($50 − $10) × Units sold]

−

$210,000

=

$0

Units sold

=

5,250 passengers

5,250 passengers × $50 = $262,500

Contribution

=

Contribution margin per unit

margin ratio

Sale price per unit

=

$50 − 10

$50

=

0.80

Sales

=

Fixed expenses + Operating income

in dollars

Contribution margin ratio

=

$210,000 + $0

0.80

=

$262,500

All else being equal, a decrease in variable costs will increase the contribution margin per unit and the contribution

margin ratio. The breakeven point will therefore decrease. An increase in variable costs will have the opposite effect.

Managerial Accounting 4e Solutions Manual

(5-10 min.) S7-8

Req. 1

The decline in fixed costs does not affect the $30 unit contribution margin calculated in S7-1. The new breakeven point

in units is:

=

Fixed expenses + Operating income

Sales in units

Contribution margin per unit

=

$180,000 + $0

$30

=

6,000 dinner cruise passengers

Or, using the equation approach:

Sales revenue

−

Variable expenses

−

Fixed

=

Operating

expenses

income

Sale price Units

per unit × sold

−

Variable cost Units

−

Fixed

=

Operating

per unit × sold

expenses

income

($50 × Units sold)

−

($20 × Units sold)

−

$180,000

=

$0

[($50 − $20) × Units sold]

−

$180,000

=

$0

$30

×

Units sold

=

$180,000

Units sold

=

6,000 passengers

6,000 passengers × $50 = $300,000

Alternatively,

Contribution

=

Contribution margin per unit

margin ratio

Sale price per unit

=

$50 − 20

$50

=

0.60

Sales

=

Fixed expenses + Operating income

in dollars

Contribution margin ratio

=

$180,000 + $0

0.60

=

$300,000

Chapter 7 Cost-Volume-Profit Analysis

(continued) S7-8

(5-10 min.) S7-9

Weighted-Average Contribution Margin per Unit

Regular

Executive

Cruise

Cruise

Total

Sale price per ticket

$ 50

$130

Less: Variable expense per ticket

20

40

Contribution margin per ticket

$ 30

$ 90

Sales mix in units

× 4

× 1

5

Contribution margin

$120

$ 90

$210

Weighted-average contribution

margin per unit ($210 / 5)

$ 42.00

A simple average contribution margin would be $60 [(30 + 90) / 2]. The weighted-average is less than the simple

average because the cruiseline sells more regular cruises (with the lower contribution margin) than executive cruises.

The weighted average contribution margin ($42.00) is higher than the contribution margin of regular cruises ($30)

because the cruiseline sells some executive cruises, and executive cruises have a higher contribution margin ($90) than

regular cruises.

Because the new sales mix creates a higher weighted average contribution margin, the cruiseline will need to sell fewer

cruises, in total, to breakeven than when it just sold regular cruises.

(5-10 min.) S7-10

a.

Sales

=

Fixed expenses + Operating income

in total tickets

Weighted-average contribution margin per unit

=

$210,000 + $0

$42.00*

=

5,000 passengers

Chapter 7 Cost-Volume-Profit Analysis

(5-10 min.) S7-13

a.

Margin of safety

=

Expected sales

−

Breakeven sales

in units

in units

in units

=

1,500 – 750*

=

750 posters

*Breakeven in units = $15,000/($45-$25) = 750 units

b.

Margin of safety

=

Target level

–

Breakeven

in dollars

sales dollars

sales dollars

=

$67,500** – $33,750***

=

$33,750

** Expected sales in dollars = 1,500 x $45 = $67,500

*** Breakeven in dollars = 750 x $45 = $33,750

c.

Margin of safety

=

Margin of safety in dollars

as a percentage

Expected sales in dollars

of expected sales

=

33,750

67,500

=

50%

Chapter 7 Cost-Volume-Profit Analysis

(5-10 min.) S7-15

Req. 1

Product: Cupcakes

Selling price per unit

$ 6.00

Less: Variable cost per unit

$ 4.00

CM

$ 2.00

To find the indifference point, you need to set the costs of Option

1 equal to the costs of Option 2:

$2,600 = $1,700 + [($6 x .05) x CUPCAKES]

Then solve for CUPCAKES:

CUPCAKES = 3,000

Proof:

Lease costs under Option 1:

Fixed costs

$ 2,600

Variable costs (none)

0

Total costs under Option 1

$ 2,600

Lease costs under Option 2:

Fixed costs

$ 1,700

Variable costs per unit ($6 x .05)

$ 0.30

Times # of units at pt of indifference (3,000)

3,000

Total variable costs

900

Total costs under Option 2

$2,600

1. Integrity – Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent

conflicts of interest. Advise all parties of any potential conflicts.

skills.

3. Competence – Perform professional duties in accordance with relevant laws, regulations, and technical standards.

5. Credibility – Disclose all relevant information that could reasonably be expected to influence an intended user’s

understanding of the reports, analyses, or recommendations.

Copyright © 2015 Pearson Education, Inc.

7-12

(15 min.) E7-17A

Req. 1

Global Travel

Contribution Margin Income Statements

Sales revenue

$270,000

$410,000

Less: Variable expenses (30% of sales revenue*)

81,000

123,000

Contribution margin (70% of sales revenue**)

189,000

287,000

Fixed expenses

170,800

170,800

Operating income (loss)

$ 18,200

$ 116,200

__________

*$120,000 / $400,000 = 0.30

**$280,000 / $400,000 = 0.70 (CM ratio)

Req. 2

Breakeven sales

=

$170,800 + $0

1 − 0.30

=

$170,800 + $0

0.70

=

$244,000

(10-15 min.) E7-18A

This problem involves working backwards through the shortcut contribution margin formula and then working

backwards through the contribution margin income statement to find the missing data.

First, fill in the given data in the short cut contribution margin formula, and solve for the contribution margin ratio:

Sales needed to breakeven

=

Fixed expenses

Contribution margin ratio

$48,000

=

$24,000

Contribution margin ratio

Contribution margin ratio

=

$24,000

$48,000

Contribution margin ratio

=

.50

Next, fill in the given data in the contribution margin income statement:

Sales………………………….

$ ?

Less: Variable expenses….

42,000

Contribution margin……….

?

Less: Fixed expenses……..

24,000

Operating income…………..

$ ?

Chapter 7 Cost-Volume-Profit Analysis

(continued) E7-18A

Because the contribution margin ratio is 50% of sales revenue, the variable expenses must be 50% of sales revenue.

Therefore:

Variable expenses

=

50% × Sales revenue

$ 42,000

=

50% × Sales revenue

$ 84,000

=

Sales revenue

Sales − $42,000

=

50% Sales

Sales − 50% Sales

=

$42,000

50% Sales

=

$42,000

Sales

=

$42,000

50%

Sales

=

$84,000

Sales……………………………….

$ 84,000

Less: Variable expenses……….

42,000

Contribution margin…………….

$ 42,000

Less: Fixed expenses…………..

24,000

Operating income……………….

$ 18,000

Sale price………………….………..……………..

$1.80

Less: Variable expenses………………….………..….

0.90

Contribution margin per unit…………..……

$0.90

Contribution margin ratio:

Contribution margin per unit

=

$0.90

Sale price per unit

$1.80

=

0.50

Req. 2

Breakeven sales in units

=

Fixed expenses + Operating income

Contribution margin per unit

=

$90,000 + $0

$0.90

=

100,000 packages

Breakeven sales in dollars

=

Fixed expenses + Operating income

Contribution margin ratio

=

$90,000 + $0

0.50

=

$180,000

Managerial Accounting 4e Solutions Manual

(continued) E7-19A

Req. 3

Sales in units

=

Fixed expenses + Operating income

Contribution margin per unit

=

$90,000 + $18,000

$0.90

=

120,000 packages

(5-10 min.) E7-20A

New contribution margin per unit:

Sales price……………………………...…………..

$1.80

Less: Variable expenses………………….………..….

0.80

Contribution margin per unit…..……………

$1.00

Sales in units

=

Fixed expenses + Operating income

Contribution margin per unit

=

$1.00

=

123,000 packages

level.

Chapter 7 Cost-Volume-Profit Analysis

(10-15 min.) E7-21A

Req. 1

Contribution

=

Contribution margin per unit

margin ratio

Sales price per unit

=

$5.25 − $2.10

$5.25

=

0.60

Breakeven sales

=

Fixed expenses + Operating income

in dollars

Contribution margin ratio

=

$7,500 + $0

0.60

=

$12,500

Target sales

=

Fixed expenses + Operating income

in dollars

Contribution margin ratio

=

$7,500 + $7,050

0.60

=

$24,250

Yes, the franchising concept is a good idea. Most locations are expected to sell more ($25,000) than the sales required

Contribution margin per unit ($5.25 – $2.10)

$ 3.15

Average sales volume units…………………

× 6,500

Contribution margin…………………………..

$20,475

Less: Fixed expenses……………………….

(7,500)

Operating income………………………………

$12,975

Req. 2

After the price cut and advertising fees, the average restaurant location will have the following operating income:

New contribution margin per unit ($4.75 sales price – $2.10

variable cost…………………………………….

$ 2.65

New sales volume (units)………….

× 7,000

Contribution margin…………………

$18,550

Less: New fixed expenses

($7,500 + $600 advertising fee)……

(8,100)

New operating income……………..

$ 10,450

Assuming volume increases according to plan, cutting the sales price and advertising will allow the franchise owners to

continue to reach their target profits of $7,050 per month. However, their operating income will not be as high as

before the changes.

Chapter 7 Cost-Volume-Profit Analysis

(15-20 min.) E7-25A

Req. 1

(Fixed expenses + Operating income) / CM per unit = Breakeven in units

($240,000 + $0) / ($2,400 – $1,000 – $200) = 200 units

(Fixed expenses + Operating income) / CM ratio = Breakeven in sales dollars

Chapter 7 Cost-Volume-Profit Analysis

(15-20 min.) E7-28A

Weighted-Average Contribution Margin per Unit

Twig

Oak

Total

Sale price per unit

$15.00

$35.00

Less: Variable cost per unit

2.50

10.00

Contribution margin per unit

$12.50

$25.00

Multiply by: Sales mix in units

× 4

× 1

5

Contribution margin

$50.00

$25.00

$75.00

Weighted-average contribution margin per unit ($75 / 5 units)

$15.00

Fixed expenses + Operating income

Weighted-average contribution margin per unit

=

$15

=

20 units

Breakeven sales of twig stands (20 × 4/5)………………

Breakeven sales of oak stands (20 × 1/5).………………

(15-20 min.) E7-29A

Weighted-Average Contribution Margin per Unit

Standard

Chrome

Total

Sales price per unit

$60

$75

Less: Variable cost per unit

45

55

Contribution margin per unit

$15

$20

Multiply by: Sales mix in units

× 3

× 2

5

Contribution margin

$45

$40

$ 85

Weighted-average contribution margin per unit ($110 / 5 units)

$ 17

Sales in total units:

=

Fixed expenses + Operating income

Weighted-average contribution margin per unit

=

$18,700 + $0

$17

=

1,100 units

Breakeven sales of standard scooters (1,100 × 3/5)………………

660 units

Breakeven sales of chrome scooters (1,100 × 2/5).………………..

440 units

Managerial Accounting 4e Solutions Manual

(continued) E7-29A

Sales in total units:

=

Fixed expenses + Operating income

Weighted-average contribution margin per unit

=

$18,700 + $13,600

$17

=

1,900 units

Target sales of standard scooters (1,900 × 3/5)……..………………

1,140 units

Target sales of chrome scooters (1,900 × 2/5)………...……………….

760 units

(20-30 min.) E7-30A

This is a challenging exercise that requires students to work backwards. Use the weighted-average contribution margin

per unit chart, in conjunction with the shortcut formula, to work backwards to find the contribution margin of the

Classic.

Digital

Classic

Total

Sales price per unit……..……..………..

$225

Less: Variable expense per unit. ($125 + $35)

160

Contribution margin per unit..……..

65

215

Multiply by: Sales mix in units……….……………..

x 7

× 3

10

Contribution margin……….………….

$455

645

1,100

Weighted-average contribution

margin per unit……….……………..

$ 110

aSales in

=

Fixed expenses + Operating income

total units

Weighted-average contribution margin per unit

2,100

=

$195,000 + $36,000

Weighted-average contribution margin per unit

Weighted-average

=

$231,000

2,100

contribution

margin per unit

=

$110 / unit