Chapter 6 Cost Behavior

(continued) P6-60A

Req. 5

Cost

Activity

Variable cost:

High pt.

$579,000

32,000

Nov

Low pt.

$420,000

20,000

Sep

Difference

$159,000

12,000

Change in cost / change in volume = variable cost

$159,000 / 12,000 = $13.25 (rounded)

Using high point

Total cost

=

Variable cost component + fixed cost component

y

=

vx + f

$579,000

=

32,000 ($13.25) + f

$579,000

=

$424,000 + f

$155,000

=

f

Total fixed costs = $155,000

y = $13.25x + $155,000

Req. 6

January’s estimated manufacturing overhead costs are $499,500.

y = vx + f

y = 26,000 ($13.25) + $155,000

Total costs = $499,500 (some rounding so answers may vary slightly)

Chapter 6 Cost Behavior

(30-45 min.) P6-62A

Req. 1

Gross Profit

Sales ($115.00 x 1,900)

$218,500

Less: Cost of goods sold (1,900* violins × $103**)

195,700

Gross profit

$ 22,800

Sales

$ 218,500

Less: Variable costs

(162,100)

Contribution margin

$ 56,400

*(131,300 + $55,000 + $27,000)/2,700 = $79

$12,000/1,900 = $6.31579

$79.00 + ($6.322x 1,900) = $162,100 (rounded)

Req. 3

Total Expenses Shown Below the Gross Profit Line

Variable selling and administrative expenses

$12,000

+ Fixed selling and administrative expenses

12,900

Total expenses below the gross profit line

$24,900

All fixed expenses:

Fixed manufacturing

$64,800

Fixed selling and administrative

12,900

Total fixed expenses

$77,700

Req. 5

The dollar value of ending inventory under absorption costing is $82,400 ($103 x 800).

Req. 6

The dollar value of ending inventory under variable costing is $63,200 ($79 x 800).

The absorption (traditional) income statement will have a higher operating income by $19,200, [($64,800/2,700) x

800].

Under absorption costing, more fixed manufacturing overhead costs are trapped on the balance sheet when inventory

increases. Under variable costing, these costs are expensed as part of cost of goods sold in the current period.

(25-35 min.) P6-63A

Req. 1

January

February

Absorption

Costing

Variable

Costing

Absorption

Costing

Variable

Costing

Variable manufacturing expense per meal

$5.00

$5.00

$5.00

$5.00

Fixed MOH (Absorption only) ($800/2,000; $800/1,600)

$0.40

$0.00

$0.50

$0.00

Total product cost.……………………

$5.40

$5.00

$5.50

$5.00

Managerial Accounting 4e Solutions Manual

(continued) P6-63A

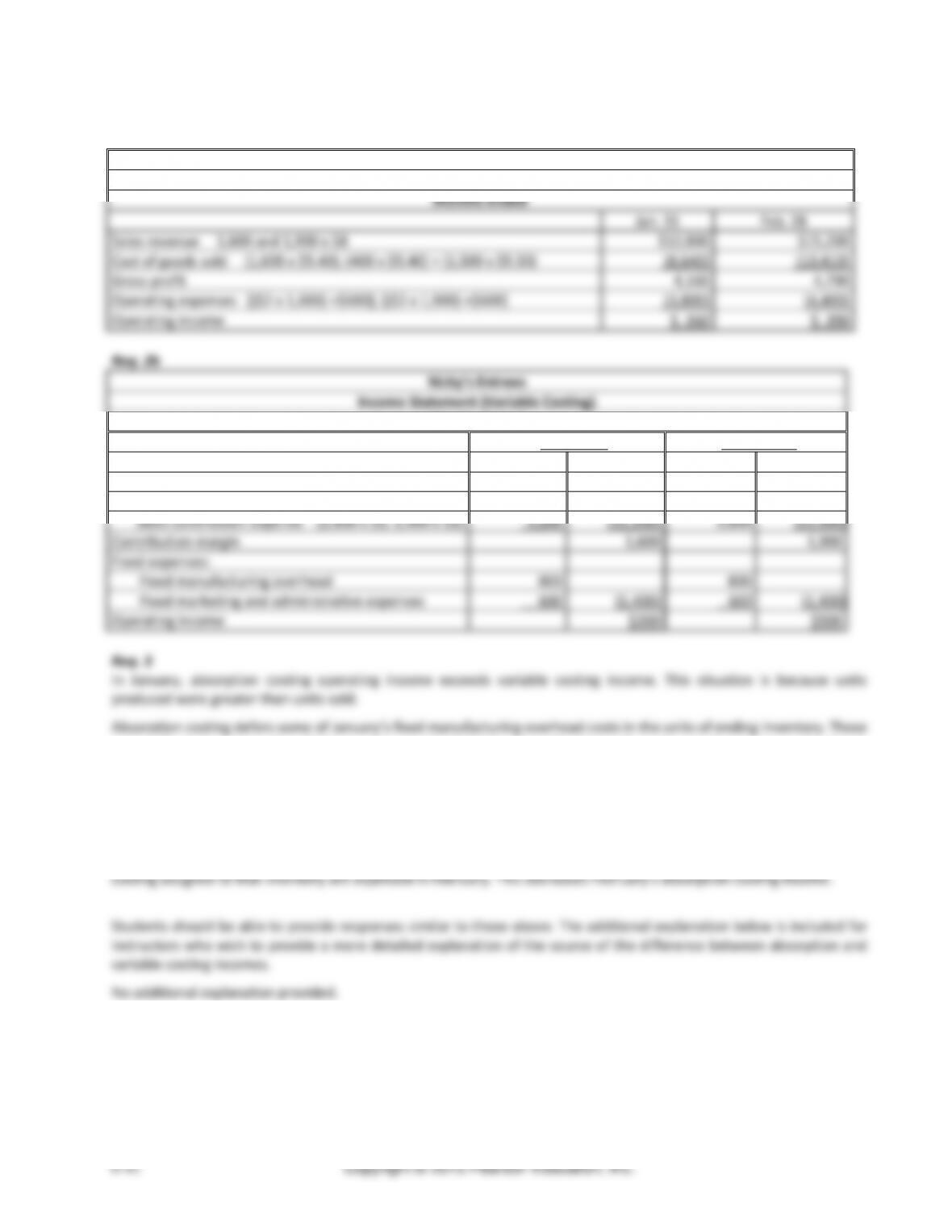

Req. 2a

Nicky’s Entrees

Income Statement (Absorption Costing)

Months Ended

Jan. 31

Feb. 28

Sales revenue 1,600 and 1,900 x $8

$12,800

$15,200

Cost of goods sold (1,600 x $5.40); (400 x $5.40) + (1,500 x $5.50)

(8,640)

(10,410)

Gross profit

4,160

4,790

Operating expenses [($2 x 1,600) +$600]; [($2 x 1,900) +$600]

(3,800)

(4,400)

Operating income

$ 360

$ 390

Req. 2b

Nicky’s Entrees

Income Statement (Variable Costing)

Months Ended

January 31

February 28

Sales revenue

$12,800

$15,200

Variable expenses:

Variable cost of goods sold (1,600 and 1,900 x $5)

8,000

9,500

Sales commission expense (1,600 x $2; 1,900 x $2)

3,200

(11,200)

3,800

(13,300)

Contribution margin

1,600

1,900

Fixed expenses:

Fixed manufacturing overhead

800

800

Fixed marketing and administrative expenses

600

(1,400)

600

(1,400)

Operating income

$200

$500

Req. 3

In January, absorption costing operating income exceeds variable costing income. This situation is because units

produced were greater than units sold.

Absorption costing defers some of January’s fixed manufacturing overhead costs in the units of ending inventory. These

costs will not be expensed until those units are sold. Deferring these fixed manufacturing overhead costs to the future

increases January’s absorption costing income.

In February, absorption costing operating income is less than variable costing operating income. This is because units

produced were less than units sold for the month.

As inventory declines, as was the case this February, January’s fixed manufacturing overhead costs that absorption

Copyright © 2015 Pearson Education, Inc.

6-43

(45-60 min.) P6-64B

Req. 1

The hospital’s overhead appears to be a mixed cost. If it were a fixed cost, it would remain constant each month. If it

Managerial Accounting 4e Solutions Manual

(continued) P6-64B

Req. 5

Cost

Activity

Variable cost:

High pt.

$574,000

31,500

Nov

Low pt.

$412,000

19,500

Sep

Difference

$162,000

12,000

Change in cost / change in volume = variable cost

$162,000 / 12,000 = $13.50

Using high point

Total cost

=

Variable cost component + fixed cost component

y

=

vx + f

$574,000

=

31,500 ($13.50) + f

$574,000

=

$425,250 + f

$148,750

=

f

Total fixed costs = $148,750

Total costs = Variable costs + fixed costs

y = vx + f

y = 24,500 ($13.50) + $148,750

Total costs = $479,500

Req. 6

y = $13.12x + $173,670.16

y = $13.12(24,500) + $173,670.16

y = $495,110.16

Req. 7

y = $51.37x + $270,606.28

y = $51.37(3,640) + $270,606.28

y = $457,593. 08

Req. 8

We have the most confidence in the cost equation using nursing hours. The R-square value for that equation was the

highest.

Chapter 6 Cost Behavior

(45-60 min.) P6-65B

Req. 1

Carmichael’s manufacturing overhead appears to be a mixed cost. If it were a fixed cost, it would remain constant each

Managerial Accounting 4e Solutions Manual

Req. 5

Cost

Activity

Variable cost:

High pt.

$527,000

27,000

Nov

Low pt.

$425,000

19,000

Sep

Difference

$102,000

8,000

Change in cost / change in volume = variable cost

$102,000 / 8,000 = $12.75

Using high point

Total cost

=

Variable cost component + fixed cost component

y

=

vx + f

$527,000

=

27,000 ($12.75) + f

$527,000

=

$344,250 + f

$182,750

=

f

Total fixed costs = $182,750

y = $12.75x + $182,750

Req. 6

January’s estimated manufacturing overhead costs are $495,125.

y = vx + f

y = 24,500 ($12.75) + $182,750

y = $495,125

(15-20 min.) P6-66B

Req. 1

Darla’s Ice Cream Shoppe

Income Statement

For the Month Ended June 30

Sales revenue (9,400 × $5.00)

$47,000

Cost of goods sold (9,400 × $0.60*)

(5,640)

Gross profit

41,360

Operating expenses:

Lease expense

$ 2,000

Depreciation expense

240

Other operating expenses

2,600

Total operating expenses

(4,840)

Operating income

$ 36,520

*$14 per tub ÷ 35 servings = $0.40 for ice cream + $0.20 per ice cream cone = $0.60

Req. 2

Darla’s Ice Cream Shoppe

Contribution Margin Income Statement

For the Month Ended June 30

Sales revenue (9,400 × $5.00)

$47,000

Variable expenses:

Cost of goods sold (9,400 × 0.60*)

$5,640

Other variable operating expenses

650a

(6,290)

Contribution margin

$40,710

Fixed expenses:

Lease expense

$2,000

Depreciation expense

240

Other fixed operating expenses

1,950b

(4,190)

Operating income

$ 36,520

a $2,600 × 25% variable = $650

b $2,600 × 75% fixed = $1,950

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

6-48

(30-45 min.) P6-67B

1. Gross Profit

Sales

$198,000

Less: Cost of goods sold (1,650* violins × $103**)

169,950

Gross profit

$ 28,050

2. Contribution Margin

Sales

$ 198,000

Less: Variable expenses *

(147,250)

Contribution margin

$ 50,750

*($104,500 + $60,000 +$31,000)/2,300 = $85

$7,000/1,650 = $4.242

($85 + $4.242) x 1,650 = $147,250

3. Total Expenses Shown Below the Gross Profit Line

Variable selling and administrative expenses

$7,000

+ Fixed selling and administrative expenses

13,100

Total expenses below the gross profit line

$20,100

4. Total Expenses Shown Below the Contribution Margin Line

Fixed manufacturing overhead

$41,400

+ Fixed selling and administrative expenses

13,100

Total expenses below the contribution margin line

$54,500

5. The dollar value of ending inventory under absorption costing is $66,950 ($103 x 650).

6. The dollar value of ending inventory under variable costing is $55,250 ($85 x 650).

(25-35 min.) P6-68B

Req. 1

January

February

Absorption

Costing

Variable

Costing

Absorption

Costing

Variable

Costing

Variable manufacturing expense per meal

$3.00

$3.00

$3.00

$3.00

Fixed MOH (Absorption only) $1,200/1,600; $1,200/1,500

0.75

0.00

0.80

0.00

Total product cost……….……………

$3.75

$3.00

$3.80

$3.00

Chapter 6 Cost Behavior

(continued) P6-68B

Req. 2a

Marty’s Entrees

Income Statement (Absorption Costing)

Month Ended January 31

Jan. 31

Feb. 28

Sales revenue (1,300 and 1,700 × $9)

$11,700

$15,300

Cost of goods sold*

(4,875)

(6,445)

Gross profit

6,825

8,855

Operating expenses

(3,000)

(3,800)

Operating income

$ 3,825

$ 5,055

Jan: 1,300 x $3.75 = $4,875

Feb: (300 x $3.75) + (1,400 x $3.80) = $6,445

Req. 2b

Marty’s Entrees

Income Statement (Variable Costing)

Months Ended

January 31

February 28

Sales revenue

$11,700

$15,300

Variable expenses:

Variable cost of goods sold

3,900

5,100

Sales commission expense

2,600

(6,500)

3,400

(8,500)

Contribution margin

5,200

6,800

Fixed expenses:

Fixed manufacturing overhead

1,200

1,200

Fixed marketing and administrative expenses

400

(1,600)

400

(1,600)

Operating income

$3,600

$5,200

Req. 3

In January, absorption costing operating income exceeds variable costing income. This situation is because the units

produced were greater than the units sold.

Absorption costing defers some of January’s fixed manufacturing overhead costs in the units of ending inventory. These

costs will not be expensed until those units are sold. Deferring some of these fixed manufacturing overhead costs to

the future increases January’s absorption costing income.

In February, absorption costing operating income is less than variable costing operating income. This situation is

Copyright © 2015 Pearson Education, Inc.

6-50

A6–69

1. Briefly describe an organization with which you are familiar. Describe a situation when a manager in that

organization could use cost behavior information and how the manager could use the information.

2. How are fixed costs similar to step fixed costs? How are fixed costs different from step fixed costs? Give an

example of a step fixed cost and describe why that cost is not considered to be a fixed cost.

3. Describe a specific situation when a scatter plot could be useful to a manager.

The manager of a printing firm could use a scatter plot to analyze the monthly telephone expenses for a year to

4. What is a mixed cost? Give an example of a mixed cost. Sketch a graph of this example.

5. Compare discretionary fixed costs to committed fixed costs. Think of an organization with which you are

familiar. Give two examples of discretionary fixed costs and two examples of committed fixed costs that

Chapter 6 Cost Behavior

Copyright © 2015 Pearson Education, Inc.

6-51

increased or decreased in the short run by managers. Rent and depreciation are examples of committed fixed

costs because they can only be changed in the long run.

6. Define the terms “independent variable” and “dependent variable,” as used in regression analysis. Illustrate the

concepts of independent variables and dependent variables by selecting a cost a company would want to

7. Define the term “relevant range.” Why is it important to managers?

8. Describe the term “R–square.” If a regression analysis for predicting manufacturing overhead using direct labor

hours as the dependent variable has an R-square of .40, why might this be a problem? Given the low R-square

value, describe the options a manager has for predicting manufacturing overhead costs. Which option do you

9. Over the past year, a company’s inventory has increased significantly. The company uses absorption costing for

financial statements, but internally, the company uses variable costing for financial statements. Which set of

10. A company has adopted a lean production philosophy and, as a result, has cut its inventory levels significantly.

Describe the impact on the company’s external financial statements as a result of this inventory reduction. Also

11. What costs might a business incur by not adopting e-billing (paperless) services? Is e-billing only profitable to

large businesses or is it applicable to small business? Explain what might be involved in changing over to

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

6-52

over to a paperless billing system requires developing a secure banking website as well as convincing customers to

adopt the new system.

12. How might the principles of sustainability (such as increased efficiency) affect cost behavior overall? Think of an

example of a sustainable change in process or material that could impact the cost equation of that cost (i.e., the

Copyright © 2015 Pearson Education, Inc.

6-53

A6–70

1. Describe the company you selected and the products or services it provides.

2. List ten costs that this company would incur. Include costs from a variety of departments within the company,

including human resources, sales, accounting, production (if a manufacturer), service (if a service company), and

others. Make sure that you have at least one cost from each of the following categories: fixed, variable, and

mixed.

Development of new texts/editions

3. Classify each of the costs you listed as either fixed, variable, or mixed. Justify why you classified each cost as you

did.

Mixed – includes salaried editors (fixed) and authors’ advances

Fixed – scheduled training sessions

4. Describe a potential cost driver for each of the variable and mixed costs you listed. Explain why each cost driver

would be appropriate for its associated cost.

Revision/new book projects

Chapter 6 Cost Behavior

3. Categorized each cost in your list as fixed, variable, or mixed.

4. The number of trips taken by the president in any given year fluctuates and is dependent upon the political

climate, crises, economics, and the like. How useful to you think this cost per hour is?

5. What purpose(s) can the $179,750 cost per hour be used for? Are there any purposes for which that cost is not

representative of the “true” cost?

6. Can you think of a better way to represent/ communicate the cost of Air Force One?

7. Do you think the reimbursement policy is fair to the president? Why or why not?

8. Do you think the reimbursement policy is fair to the taxpayers? Why or why not?