Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

(15-20 min.) E6-38A

Req. 1

Wilson’s operating income under variable costing will be lower than its operating income under absorption costing.

This situation is because under absorption costing, some of the fixed MOH remains “trapped” on the balance sheet as

part of the cost of inventory. Under variable costing, all fixed MOH incurred during the period is expensed as a period

cost.

Managerial Accounting 4e Solutions Manual

(continued) E6-39A

Flannery Water Optics

Contribution Margin (Variable Costing) Income Statement

Year Ended December 31

Sales revenue (225,000 × $49)

$11,025,000

Variable expenses:

Variable cost of goods sold

4,500,000

Sales commission expense (225,000 × $8)

1,800,000

(6,300,000)

Contribution margin

4,725,000

Fixed expenses:

Manufacturing overhead

$2,400,000

Operating expenses

245,000

(2,645,000)

Operating income

$ 2,080,000

Req. 2

Absorption costing operating income is higher than variable costing operating income. This situation is because

absorption costing defers $150,000 of fixed manufacturing overhead as an asset in ending inventory. In contrast,

variable costing expenses all of the fixed manufacturing overhead during the year.

Variable costing expenses $150,000 more costs during the year, so variable costing operating income is $150,000 less

than absorption costing income.

Req. 3

Increase in contribution margin

$315,000

Increase in fixed expenses

(165,000)

Increase in operating income

$150,000

The company should go ahead with the promotion because the increase in contribution margin exceeds the increase in

fixed costs.

Chapter 6 Cost Behavior

Exercises (Group B)

(15 min.) E6-40B

Req. 1

6,000

garments

7,500

garments

9,000

garments

Total variable costs

$ 5,100

$ 6,375*

$ 7,650

Total fixed costs

18,000

18,000

18,000

Total operating costs

$23,100

$24,375

$25,650

Variable cost per garment

$0.85

$0.85

$0.85

Fixed cost per garment

3.00

2.40*

2.00

Average cost per garment

$3.85

$3.25

$2.85

*Given

Req. 2

The average cost per garment changes as volume changes, due to the fixed component of the dry cleaner’s costs. The

fixed cost per unit decreases as volume increases, while the variable cost per unit remains constant.

Req. 3

Cost from Requirement 1 for 6,000 garments: $23,100

Estimated cost @ 6,000 garments using $2.85: $17,100

Underestimation total: $6,000

She would underestimate her costs by $6,000.

(15 min.) E6-41B

Peltier Dry Cleaners

Projected Absorption Costing Income Statement

Month Ended March 31

Dry cleaning revenue (4,280 × $6)

$25,680

Less: Operating expenses [$18,000 + (4,280 × $0.85)]

(21,638)

Operating income

$4,042

Peltier Dry Cleaners

Projected Contribution Margin Income Statement

Month Ended March 31

Dry cleaning revenue (4,280 × $6)

$25,680

Less: Variable expenses (4,280 × $0.85)

(3,638)

Contribution margin

22,042

Less: Fixed expenses

(18,000)

Operating income

$4,042

Managerial Accounting 4e Solutions Manual

(15 min.) E6-42B

High point June; Low point March

Req. 1

Change in cost = $4,294 - $3,574 = $720

(15 min.) E6-43B

Average cost per unit

=

Total cost ÷ number of units

$23.43

=

Total cost ÷ 1,400 units

$32,802

=

Total cost

Req. 2

Total cost

=

Variable cost component + fixed cost component

y

=

vx + f

$32,802

=

v (1,400) + $20,202

$12,600

=

v (1,400)

$9.00

=

v

The variable cost per unit is $9.00

Req. 3

y

=

$9.00x + $20,202

where x = number of mailboxes

Req. 4

$37,488

=

1,600 × $23.43 average cost per mailbox

Managerial Accounting 4e Solutions Manual

(10-15 min.) E6-44B

Req. 1

Variable cost:

High

$810,000

750,000

Qtr 3

Low

$689,400

616,000

Qtr 1

Difference

$120,600

134,000

$120,600/134,000 units = $0.90 variable cost per unit

Req. 2

Projected total number of bills

640,000

% of customers using paperless billing

40%

Calculated number of customers

256,000

Variable cost per bill saved

$0.90

Total cost saved

$230,400.00

Less cost of paperless system

$187,800.00

Net savings

$ 42,600.00

Projected total number of bills

640,000

% of customers using paperless billing

30%

Calculated number of customers

192,000

Variable cost per bill saved

$0.90

Total cost saved

$172,800.00

Less cost of paperless system

$187,800.00

Net savings (cost)

$ (15,000.00)

Should the company still offer the paperless billing system? The answer to this question is dependent upon the

student’s value system and is meant to be a discussion point.

(10-15 min.) E6-45B

Req. 1

(10-15 min.) E6-46B

Use the high-low method to determine Posies Unlimited’s operating cost equation.

High point – February; Low point - July

Managerial Accounting 4e Solutions Manual

(20-30 min.) E6-47B

Req. 1

y = $0.20x + $1,964.29

(5-10 min.) E6-48B

Req. 1

y = $0.21x + $1,810.75

(10-15 min.) E6-49B

Req. 1

(10-15 min.) E6-50B

Cost

Activity

Variable cost:

High pt.

$26,500

4,100

May

Low pt.

$19,100

2,100

June

Difference

$7,400

2,000

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

6-30

(10-15 min.) E6-51B

Req. 1

y

=

$6.21x

+

$5,627.61

Req. 2

The R-square is 0.70373.

(15-20 min.) E6-52B

y

=

$4.16x

+

$10,604.32

Req. 3

The R-square is 0.923756.

(15 min.) E6-53B

High point: 90% x 750 units = 675 units, $217,150

Low point: 80% x 750 units = 600 units, $212,800

Determine the formula that is used to calculate the variable cost (slope).

Change in cost

÷

Change in volume

=

Variable cost (slope)

($217,150 - $212,800) / (675 – 600) = $58

Now determine the formula that is used to calculate the fixed cost component.

Total operating cost

÷

Total variable cost

=

Fixed cost

Choosing the high point here:

$217,150 = ($58 x 675) + FC

FC = $178,000

Cost equation: y = $58x + $178,0000

The owner should expect his operating costs to be $208,450 if occupancy falls to 70% [($58 x (70% x 750)) + $178,000].

Chapter 6 Cost Behavior

(10-20 min.) E6-54B

Fabulous Flamingos

Contribution Margin Income Statement

For the Year Ended December 31

Sales revenue

$ 1,005,000

Variable expenses:

Cost of goods sold

669,000

Variable selling and marketing expenses

27,720

Variable web site maintenance expenses

14,125

Other variable operating expenses

1,700

Total variable expenses

712,545

Contribution margin

292,455

Fixed expenses:

Fixed selling and marketing expenses

33,280

Fixed web site maintenance expenses

42,375

Other fixed operating

expenses

15,300

Total fixed expenses

90,955

Operating income

$ 201,500

Calculations for selling and marketing expenses:

Total selling and marketing expenses

$ 61,000

Variable freight-out

(19,400)

Remaining selling and marketing expenses

$ 41,600

Chapter 6 Cost Behavior

(continued) E6-56B

Req. 2

Year 1

Year 2

Fixed MOH cost per unit

$13

$13

Managerial Accounting 4e Solutions Manual

(15-20 min.) E6-57B

Req. 1

Wentworth’s operating income under variable costing will be lower than its operating income under absorption

costing. This situation is because under absorption costing, some of the fixed MOH remains “trapped” on the balance

sheet as part of the cost of inventory. Under variable costing, all fixed MOH incurred during the period is expensed as

Reconciling between two methods

Fixed MOH cost per unit $161,000/7,000

$23

Change in inventory (in units) (0+7,000 – 6,500)

500

Difference between methods

11,500

Absorption income – difference = Variable income

$32,500 – 11,500 = $21,000

Req. 3

The figures below can be calculated using the percentage of

produced units sold without the costs per unit, but you need

to change the formula for Variable Cost of Goods Sold since

the costs per unit are not provided in the problem.

Sales revenue (6,500 x $76)

$494,000

Less Variable Expenses:

Variable Cost of Goods Sold

$396,500 / 6,500 = $61 - $23 = $38

6,500 x $38

$247,000

Variable Operating Expenses (6,500 x $1.538 rounded)

$10,000

Contribution Margin

$237,000

Less Fixed Expenses:

Fixed MOH

$161,000

Fixed Operating Expenses

$55,000

Operating Income

$21,000

*Total operating expenses $65,000

Less fixed portion 55,000

Variable $10,000

# of units ÷6,500

(15 min.) E6-58B

Req. 1

Goggle Water optics

Conventional (Absorption Costing) Income Statement

Year Ended December 31

Sales revenue (200,000 × $45)

$9,000,000

Cost of goods sold (200,000 x $27*)

(5,400,000)

Gross profit

3,600,000

Operating expenses [(200,000 × $14) + $235,000]

(3,035,000)

Operating income

$ 565,000

__________

*Variable manufacturing expense per unit of $18 plus $9 fixed manufacturing expense per unit ($1,980,000 fixed

manufacturing overhead / 220,000 units produced.)

Goggle Water Optics

Contribution Margin (Variable Costing) Income Statement

Year Ended December 31

Sales revenue (200,000 × $45)

$9,000,000

Variable expenses:

Variable cost of goods sold (200,000 x $18)

3,600,000

Sales commission expense (200,000 × $14)

2,800,000

(6,400,000)

Contribution margin

2,600,000

Fixed expenses:

Manufacturing overhead

$1,980,000

Operating expenses

235,000

(2,215,000)

Operating income

$ 385,000

Req. 2

Absorption costing operating income is higher than variable costing operating income. This situation is because

absorption costing defers $180,000 of fixed manufacturing overhead as an asset in ending inventory. In contrast,

variable costing expenses all the fixed manufacturing overhead during the year.

Variable costing expenses $180,000 more costs during the year, so variable costing operating income is $180,000 less

than absorption costing income during the year.

Req. 3

Increase in contribution margin (20,000 × $13)*....

$260,000

Increase in fixed expenses.......................…………

(140,000)

Increase in operating income...........................…...

$ 120,000

Managerial Accounting 4e Solutions Manual

Problems (Group A)

(45-60 min.) P6-59A

Req. 1

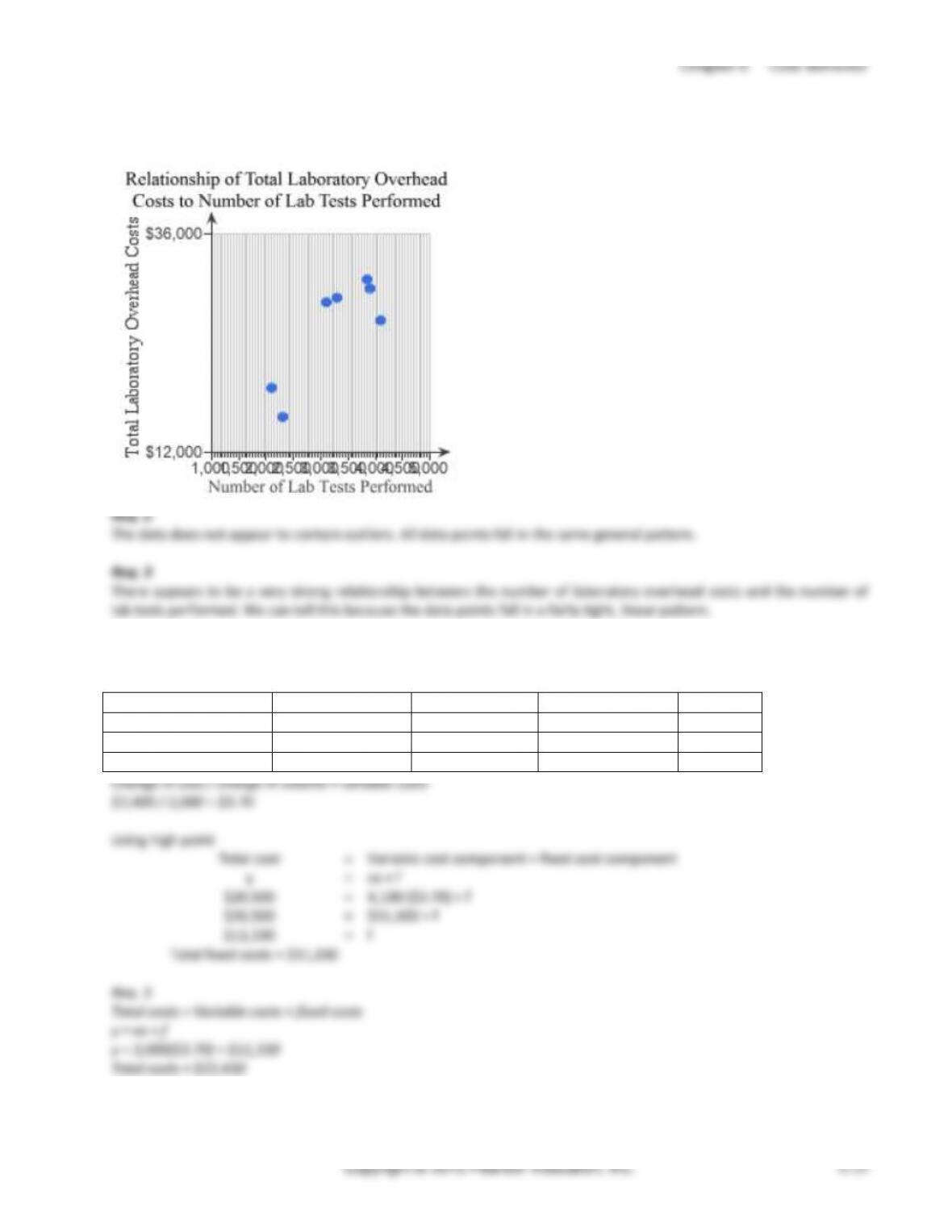

The hospital’s overhead appears to be a mixed cost. If it were a fixed cost, it would remain constant each month. If it

Chapter 6 Cost Behavior

Req. 5

Cost

Activity

Variable cost:

High pt.

$555,000

30,000

Nov

Low pt.

$424,000

20,000

Sep

Difference

$131,000

10,000

highest.