Chapter 6 Cost Behavior

Copyright © 2015 Pearson Education, Inc.

6-1

Chapter 6

Cost Behavior

Quick Check

Answers:

QC-1. a

QC-3. c

QC-5. d

QC-7. c

QC-9. b

QC-2. b

QC-4. d

QC-6. b

QC-8. c

QC-10. c

Short Exercises

(5-10 min.) S6-1

(5-10 min.) S6-2

Total fixed cost

÷

Number of basketballs

produced

=

New fixed cost per basketball

$18,000

÷

18,000

=

$1.00

(5-10 min.) S6-3

Total manufacturing costs $120,000 – $50,000 variable expenses = $70,000 fixed expenses

=

$83,250*

=

Managerial Accounting 4e Solutions Manual

(5-10 min.) S6-4

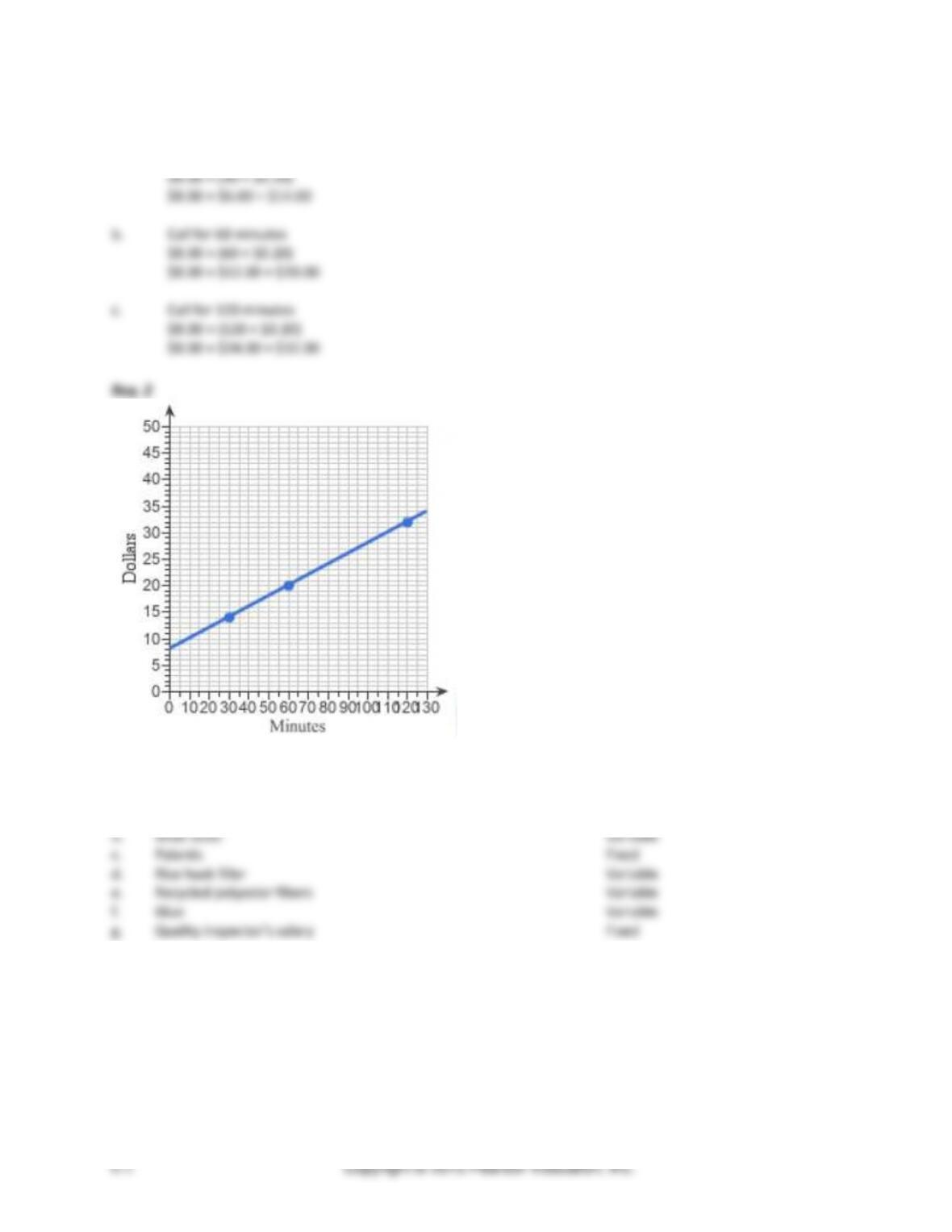

Req. 1

a. Call for 30 minutes

(5-10 min.) S6-5

a.

Depreciation on equipment

Fixed

b.

Shoe laces

Variable

c.

Patents

Fixed

d.

Rice husk filler

Variable

e.

Recycled polyester fibers

Variable

f.

Glue

Variable

g.

Quality inspector’s salary

Fixed

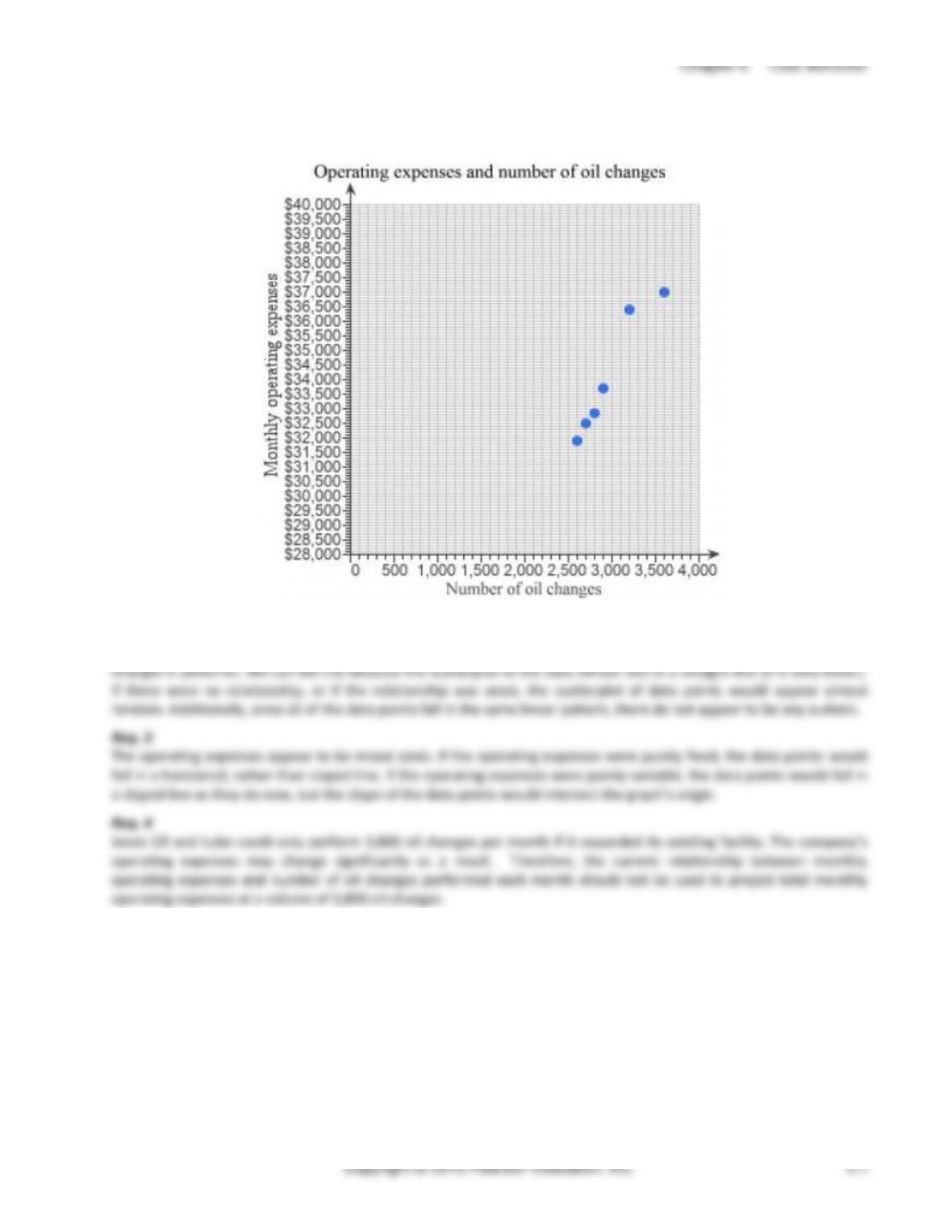

(10-15 min.) S6-6

Req. 1

Req. 2

There appears to be a very strong relationship between the company’s operating expenses and the number of oil

Managerial Accounting 4e Solutions Manual

(5-10 min.) S6-7

First, identify the formula and calculate the variable cost component (slope).

Change in costs

÷

Change in volume

=

Variable cost per unit

$5,100*

÷

1,000*

=

$5.10

$37,000

=

Change in costs

÷

Change in volume

=

Variable cost per unit

÷

=

$27,700

=

(5-10 min.) S6-9

First, identify the formula and calculate the variable cost component (slope).

Change in costs

÷

Change in volume

=

Variable cost per unit

$9,500a

÷

475b

=

$20

=

Chapter 6 Cost Behavior

(10-15 min.) S6-14

Patricia’s Quilt Shoppe

Income Statement

Month Ended February 28

Sales revenue (100 × $410)

$41,000

Less: Cost of goods sold (100 × $240)

(24,000)

Gross profit

17,000

Less: Operating expenses

Sales commissions (4% × $41,000)

$ (1,640)

Payroll costs

(2,100)

Lease

(1,600)

($5,340)

Operating income

$ 11,660

Patricia’s Quilt Shoppe

Contribution Margin Income Statement

Month Ended February 28

Sales revenue (100 × $410)

$41,000

Less variable expenses:

Cost of goods sold (100 × $240)

($24,000)

Sales commissions (4% × $41,000)

($1,640)

(25,640)

Contribution margin

15,360

Less fixed expenses:

Payroll costs

(2,100)

Lease

(1,600)

(3,700)

Operating income

$ 11,660

(10-15 min.) S6-15

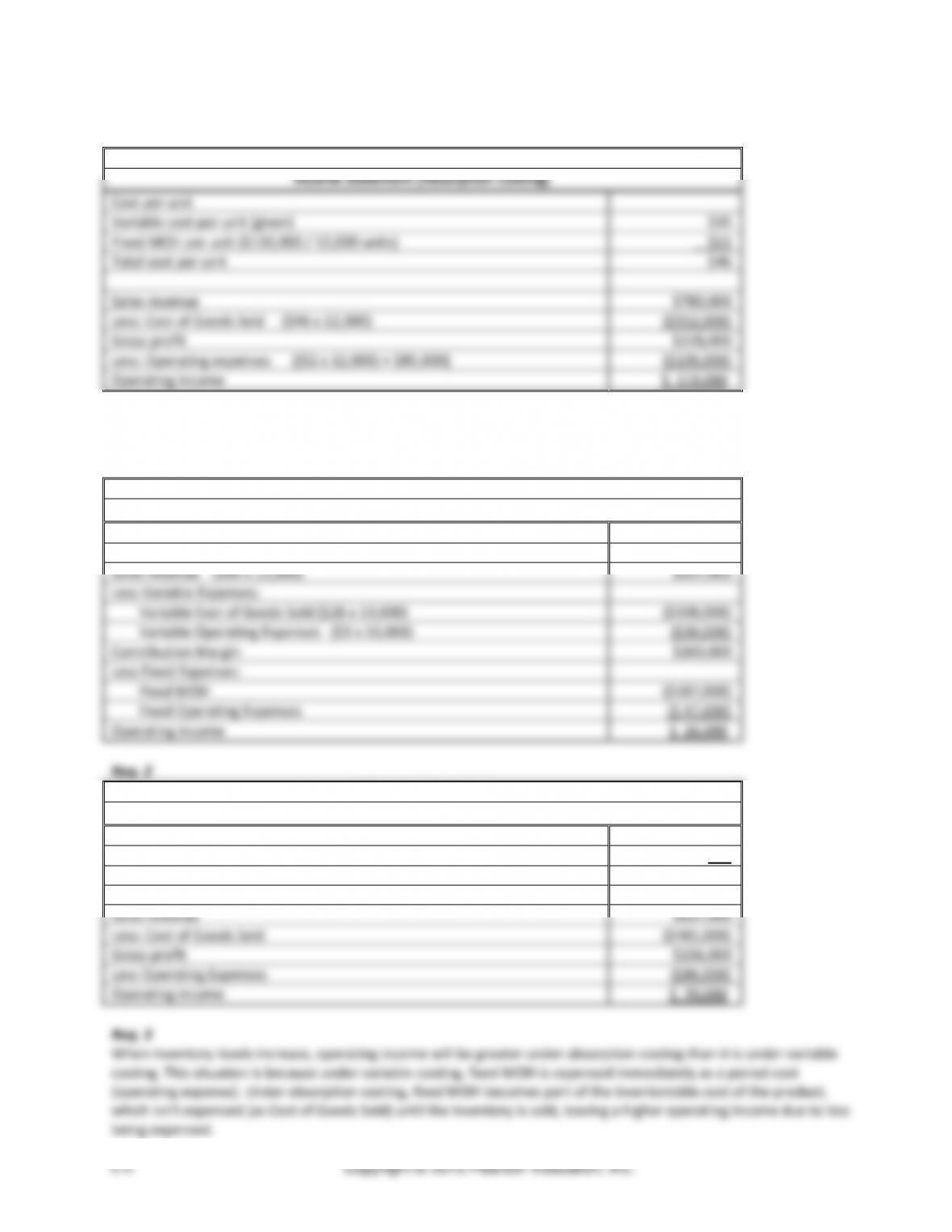

Req. 1

O’Neill’s Products

Income Statement (Variable Costing)

Variable cost per unit (given)

$ 35

Sales revenue ($65 x 12,000)

$780,000

Less Variable Expenses:

Variable Cost of Goods Sold ($35 x 12,000)

$420,000

Variable Operating Expenses ($2 x 12,000)

$ 24,000

Contribution Margin

$336,000

Less Fixed Expenses:

Fixed MOH

$132,000

Fixed Operating Expenses

$ 85,000

Operating Income

$ 119,000

Managerial Accounting 4e Solutions Manual

(continued) S6-15

Req. 2

O’Neill’s Products

Income Statement (Absorption Costing)

Cost per unit

Variable cost per unit (given)

$35

Fixed MOH per unit ($132,000 / 12,000 units)

$11

Total cost per unit

$46

Sales revenue

$780,000

Less: Cost of Goods Sold ($46 x 12,000)

($552,000)

Gross profit

$228,000

Less: Operating expenses [($2 x 12,000) + $85,000]

($109,000)

Operating income

$ 119,000

(15 min.) S6-16

Req. 1

Allen Manufacturing

Income Statement (Variable Costing)

Variable cost per unit

$26

Sales revenue ($49 x 13,000)

$637,000

Less Variable Expenses:

Variable Cost of Goods Sold ($26 x 13,000)

($338,000)

Variable Operating Expenses ($3 x 13,000)

($39,000)

Contribution Margin

$260,000

Less Fixed Expenses:

Fixed MOH

($187,000)

Fixed Operating Expenses

($ 47,000)

Operating income

$ 26,000

Req. 2

Allen Manufacturing

Income Statement (Absorption Costing)

Variable cost per unit (given)

$26

Fixed MOH per unit ($187,000/17,000 units)

$11

Total cost per unit

$37

Sales revenue

$637,000

Less: Cost of Goods Sold

($481,000)

Gross profit

$156,000

Less Operating Expenses

($86,000)

Operating income

$ 70,000

Req. 3

When inventory levels increase, operating income will be greater under absorption costing than it is under variable

costing. This situation is because under variable costing, fixed MOH is expensed immediately as a period cost

(operating expense). Under absorption costing, fixed MOH becomes part of the inventoriable cost of the product,

which isn’t expensed (as Cost of Goods Sold) until the inventory is sold, leaving a higher operating income due to less

being expensed.

(15 min.) S6-17

(a)

(b)

(c)

Variable Expenses

Mixed Expenses

Fixed Expenses

$50

Cost

(thou-

sands)

$100

Cost

(thou-

sands)

$40

Cost

(thou-

sands)

$40

$ 80

$30

$30

$ 60

$20

$20

$ 40

$10

$10

$ 20

0 2 4 6 8 10

0 2 4 6 8 10

0 2 4 6 8 10

Volume

(thousands of

units)

Volume

(thousands of

units)

Volume

(thousands of

units)

(5-10 min.) S6-18

a. Graph 2

b. Graph 2

c. Graph 9

d. Graph 2

Managerial Accounting 4e Solutions Manual

(5 min.) S6-20

1.

The CEO of a small company visits a competitor’s dumpster and

takes several trash bags containing discarded papers and reports.

The CEO directs Ivan to go through the competitor’s trash to find

any information about the competitor’s costs for a contract coming

up for bid. Ivan goes through the papers to find the information

because he does not want to lose his job.

Integrity – Abstain from engaging in

or supporting any activity that might

discredit the profession.

2.

Blue Heron Mobile operates in a highly competitive environment.

Cost information is highly confidential since most jobs are obtained

through a bidding process based on variable costing, or in some

cases absorption costing. Steve Nunez is the manager of the

Accounting Department of Blue Heron Mobile. He neglects to talk

with his new hires about the confidentiality of data, nor is there a

formal policy in place about non-disclosure.

Confidentiality – Inform all relevant

parties regarding appropriate use of

confidential information. Monitor

subordinates’ activities to ensure

compliance.

3.

Natasha is an accountant for Red Box Consulting. At a party, she

overhears a man about an upcoming contract his company will be

bidding on. She listens closer and hears specific variable cost

information that the man shares. She returns to work the next day

and shares this competitor’s cost information with her friend who

is working on preparing Red Box Consulting’s bid.

Confidentiality – Refrain from using

confidential information for

unethical or illegal advantage.

4.

Curtis struggled through regression analysis in his college courses.

Now his manager has asked him to run a regression analysis to

create a model for predicting overhead costs. He runs the

regression and creates the model. He gives his manager the cost

equation for overhead costs, even though he does not really

understand it or have any way of checking to see if he did it

correctly. He is hesitant to ask for help because he just started this

job and he wants to look impressive.

Competence – Recognize and

communicate professional

limitations or other constraints that

would preclude responsible

judgment or successful

performance of an activity.

5.

Alyssa does not disclose on the financial statements that variable

costing, rather than absorptions costing, was used.

Credibility – Disclose all relevant

information that could reasonably

be expected to influence an

intended user’s understanding of

the reports, analyses, or

recommendations.

Chapter 6 Cost Behavior

Exercises (Group A)

(15 min.) E6-21A

Req. 1

2,000

Garments

3,500

Garments

5,000

Garments

Total variable costs

$1,200

$2,100*

$ 3,000

Total fixed costs

7,000

7,000

7,000

Total operating costs

$8,200

$9,100

$10,000

Variable cost per garment

$0.60

$0.60

$0.60

Fixed cost per garment

3.50

2.00*

1.40

Average cost per garment

$4.10

$2.60

$2.00

*given

Req. 2

The average cost per garment changes as volume changes, due to the fixed component of the dry cleaner’s costs. The

fixed cost per unit decreases as volume increases, while the variable cost per unit remains constant.

Req. 3

He would underestimate his costs by $4,200*.

Cost from Req. 1 for 2,000 units: $8,200

Estimated costs @2,000 using $2.00: $4,000

Underestimation of costs $4,200

(15 min.) E6-22A

Princeton Drycleaners

Projected Income Statement

Month Ended March 31

Dry cleaning revenue (4,300 × $8)

$34,400

Less: Operating expenses [$7,000 + (4,300 × $0.60)]

(9,580)

Operating income (loss)

$24,820

Princeton Drycleaners

Projected Contribution Margin Income Statement

Month Ended March 31

Dry cleaning revenue (4,300 × $8)

$34,400

Less: Variable expenses (4,300 × $0.60)

(2,580)

Contribution margin

31,820

Less: Fixed expenses

(7,000)

Operating income (loss)

$24,820

Managerial Accounting 4e Solutions Manual

(15 min.) E6-23A

Req. 1

High – June; Low – March

(15 min.) E6-24A

Req. 1

Average cost per unit = Total cost ÷ number of units

$20.43 = Total cost ÷ 1,000 units

($10.00 x 1,100) + $10,430 = $21,430

Req. 6

Chapter 6 Cost Behavior

(10-15 min.) E6-25A

Req. 1

Cost

Activity

Variable cost:

High pt.

$800,000

740,000

Q3

Low pt.

$672,700

550,000

Q1

Difference

$127,300

190,000

Chapter 6 Cost Behavior

Copyright © 2015 Pearson Education, Inc.

6-15

(20-30 min.) E6-28A

Req. 1 and 2

y

=

$0.28x

+

$908.93

Req. 3

(5-10 min.) E6-29A

Req. 1

y

=

$0.19x

+

$2,250.74

Req. 2

(10-15 min.) E6-30A

Req. 1

Managerial Accounting 4e Solutions Manual

(10-15min.) E6-31A

Req. 1

Cost

Activity

Variable cost:

High pt.

$31,100

4,600

April

Low pt.

$22,000

2,000

June

Difference

$9,100

2,600

Change in cost / change in volume = variable costs

$9,100 / 2,600 = $3.50

Req. 2

Using high point

Total cost

=

Variable cost component + fixed cost component

y

=

vx + f

$31,100

=

4,600 ($3.50) + f

$31,100

=

$16,100 + f

$15,000

=

f

Total fixed costs = $15,000

Req. 3

Total costs = Variable costs + fixed costs

y = vx + f

y = 2,800 ($3.50) + $15,000

Total costs = $24,800

(5-10 min.) E6-32A

Req. 1

y = $4.94x + $10,637.34

(15-20 min.) E6-33A

Req. 1

Student prepares regression using Excel. Answers shown below under related requirements.

Req. 2

y = $6.57x + $1,626.72

Managerial Accounting 4e Solutions Manual

(10-20 min.) E6-35A

Two Lizards

Contribution Margin Income Statement

For the Year Ended December 31

Sales revenue

$1,014,000

Variable expenses:

Cost of goods sold

665,000

Variable selling and marketing expenses

28,520

Variable web site maintenance expenses

14,875

Other variable operating expenses

1,840

Total variable expenses

710,235

Contribution margin

303,765

Fixed expenses:

Fixed selling and marketing expenses

32,480

Fixed web site maintenances expenses

44,625

Other fixed operating expenses

16,560

Total fixed expenses

93,665

Operating income

$210,100

Calculations for selling and marketing expenses:

Total selling and marketing expenses

$ 61,000

Variable freight-out

(20,400)

Remaining selling and marketing expenses

$ 40,600

(15-20 min.) E6-36A

Req. 1

Hatcher Carriage Company

Contribution Margin Income Statement

For the Month Ended May 31

Sales revenue (13,050 × 85% × $21.00) +

(13,050 × 15% × $13.00)

$258,390

Variable expenses:

Fee paid to city (15% × $258,390)

$38,759

Complimentary postcards (13,050 × $0.85)

11,093

Brokerage fee (13,050 × 60% × $1.50)

11,745

Carriage driver wages (13,050 × $3.80)

49,590

Total variable expenses

111,187

Contribution margin

$147,203

Fixed expenses:

Leasing and boarding horses

$48,000

Non-carriage driver payroll expense

7,500

Depreciation expense

2,100

Other fixed operating expenses

7,400

Total fixed expenses

65,000

Operating income

$82,203

Req. 2

If passenger volume increases by 10% in May, we would expect all variable expenses to increase by 10%. This is

because revenues and variable costs change in direct proportion to changes in volume. As a result, the contribution

margin would also increase by 10%.

Assuming that a 10% increase in volume is still in the same relevant range, we would expect all fixed costs to remain at

their present level.

(15-20 min.) E6-37A

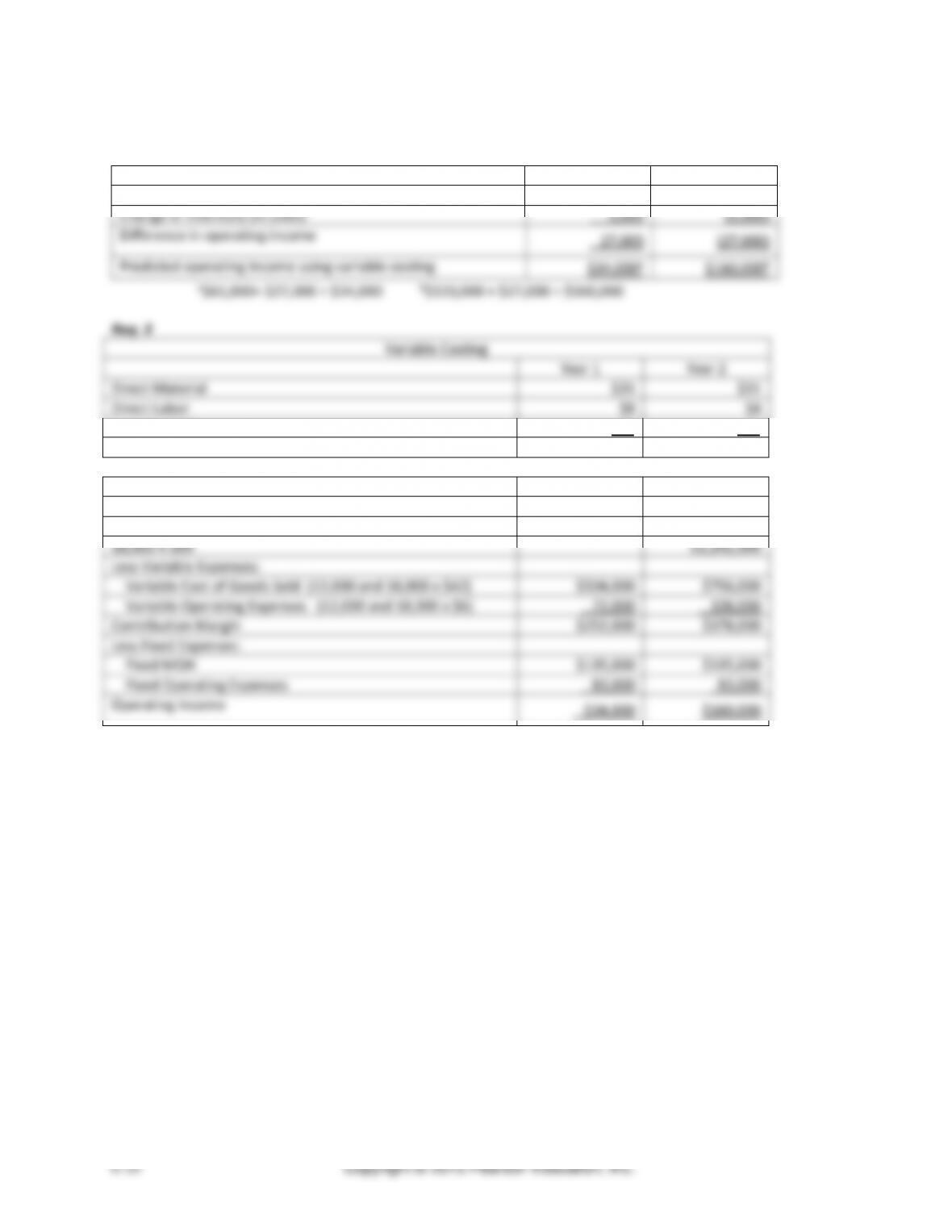

Req. 1

Absorption Costing

Year 1

Year 2

Units sold

12,000

18,000

Direct material

$31

$31

Direct labor

$8

$8

Variable MOH

$3

$3

Fixed MOH per unit ($135,000 ÷15,000 units produced)

$9

$9

Cost per unit

$51

$51

Year 1

Year 2

Sales revenue

12,000 X $69

$828,000

18,000 X $69

$1,242,000

Less: Cost of Goods Sold (12,000 and 18,000 x $51)

$612,000

$918,000

Gross profit

$216,000

$324,000

Less: Operating expenses [$83,000 + (12,000 x $6)]; [$83,000 +

(18,000 x $6)]

$155,000

$191,000

Operating income

$61,000

$133,000

Managerial Accounting 4e Solutions Manual

(continued) E6-37A

Req. 2

Year 1

Year 2

Direct Material

Direct Labor

$8

$8

Variable MOH

Cost per unit

Year 1

Year 2

Sales revenue

12,000 X $69

18,000 X $69

Less Variable Expenses:

Contribution Margin

Less Fixed Expenses:

Change in inventory (in units)

Year 1

Year 2

Fixed MOH cost per unit

$9

$9