Chapter 5 Process Costing

(continued) P5-54B

Colorado Furniture Company

Sawing Department

Cost per Equivalent Unit

Month Ended September 30

Cost per Equivalent Unit:

Direct Materials

Conversion Costs

Total

Beginning work in process, Sept. 1

$ 0

$ 0

$ 0

Costs added during September

1,855,000

342,500 a

$2,197,500

Total costs to account for

$1,855,000

$342,500

$2,197,500

Divide by total equivalent units

÷ 17,500

÷ 17,125

Cost per equivalent unit

$ 106

$ 20

a$139,000 + $203,500 = $342,500

Req. 3

Colorado Furniture Company

Sawing Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

16,000

16,000

Multiply by: Cost per equivalent unit

x $ 106

x $ 20

Cost assigned to units completed and transferred out

$ 1,696,000

$ 320,000

$2,016,000

b) Ending work in process inventory:

Equivalent units in ending WIP

1,500

1,125

Multiply by: Cost per equivalent unit

x $ 106

x $ 20

Cost assigned to units in ending WIP

$159,000

$ 22,500

$181,500

Total costs to account for

$2,197,500

Total cost accumulated in the Sawing Department during September are the same as the Total Costs to account for

shown in Req. 2:

Direct materials……………………………

$1,855,000

Direct labor…………………………………

139,000

Manufacturing overhead………………..

203,500

Total costs…………………………………

$2,197,500

Managerial Accounting 4e Solutions Manual

(continued) P5-54B

Req. 4

Journal

DATE

ACCOUNT TITLE AND EXPLANATION

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Sawing

2,197,500

Raw Materials Inventory

1,855,000

Manufacturing Wages

139,000

Manufacturing Overhead

203,500

To journalize the direct materials, direct

labor, and manuf. overhead to the

Sawing Department.

Work in Process Inventory—Assembly

2,016,000

Work in Process Inventory—Sawing

2,016,000

To transfer costs of units completed to

Assembly Department.

Note: Students may prepare three separate journal entry or the one summary journal entry (as shown above) to

record the three manufacturing costs.

(30-40 min.) P5-55B

Req. 1

Chicken and Green

cream peppers and

Chapter 5 Process Costing

(continued) P5-55B

Req. 2

Value World

Mixing Department

Flow of Physical Units and Computation of Equivalent Units

Month Ended November 30

Flow of

Physical Units

Equivalent Units

Flow of Production

Chicken,

Cream

Green Peppers,

Mushrooms

Conversion

Costs

Units to account for:

Beginning work in process, Nov. 1

0

Started in production

13,900

Total physical units to account for

13,900

Units accounted for:

Completed and transferred out

13,300

13,300

13,300

13,300

Ending work in process, Nov. 30

600

600a

0a

330b

Total physical units accounted for

13,900

Total equivalent units

13,900

13,300

13,630

__________

Green Peppers and

Beginning work in process

Costs added during Nov.

Total costs to account for

Divide by total equivalent units

÷ 13,900

Managerial Accounting 4e Solutions Manual

(continued) P5-55B

Req. 4

Value World

Mixing Department

Assignment of Costs

Assign costs

Chicken and

Cream

Green

Peppers &

Mushrooms

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

13,300

13,300

13,300

Multiply by: Cost per equivalent unit

x $1.10

x $0.30

x $1.50

Cost assigned to units completed and transferred out

14,630

$3,990

$19,950

$ 38,570

Ending work in process inventory:

Equivalent units in ending WIP

600

0

330

Multiply by: Cost per equivalent unit

x $1.10

x $0.30

x $1.50

Cost assigned to units in ending WIP

$ 660

$0

$495

$1,155

Total costs accounted for

$39,725

(45-60 min.) P5-56B

Req. 1

Transferred Direct

Chapter 5 Process Costing

(continued) P5-56B

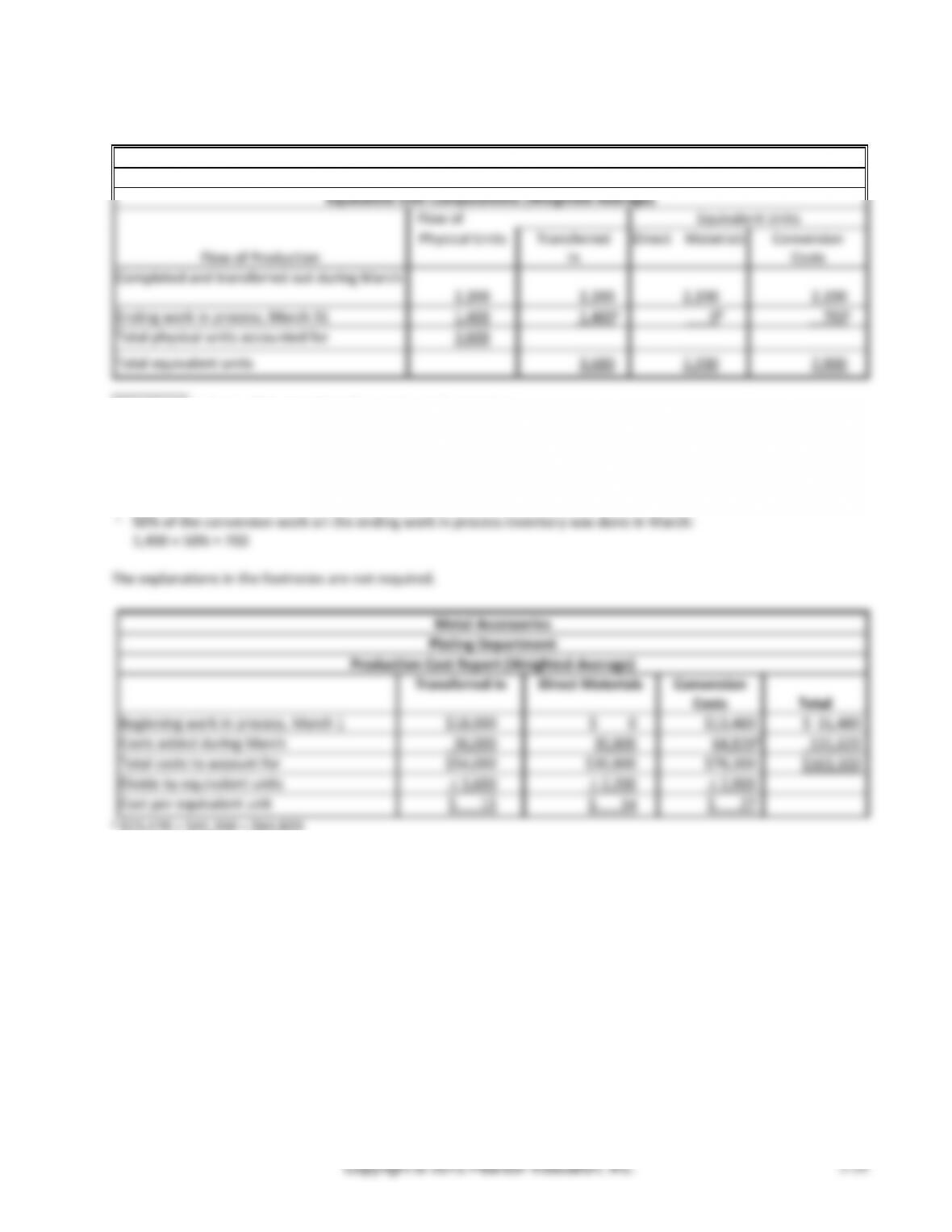

Req. 2

Metal Accessories

Plating Department

Equivalent Unit Computations (Weighted-Average)

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred

In

Direct Materials

Conversion

Costs

Completed and transferred out during March

2,200

2,200

2,200

2,200

Ending work in process, March 31

1,400

1,400a

0b

700c

Total physical units accounted for

3,600

Total equivalent units

3,600

2,200

2,900

__________

a The time line shows that transferred-in costs are incurred at

the beginning of the plating process. Ending inventory was started this period, so it did pass the point where

transferred-in costs are added. The ending inventory is therefore complete with respect to transferred-in costs.

b The time line shows that direct materials are not added until the end of the plating process. The ending inventory is

only 50% of the way through the plating process, so it has not yet incurred any plating direct materials costs.

Beginning work in process, March 1

$13,480

Costs added during March

Total costs to account for

$78,300

Divide by equivalent units

Cost per equivalent unit

Managerial Accounting 4e Solutions Manual

(continued) P5-56B

Metal Accessories

Plating Department

Production Cost Report

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

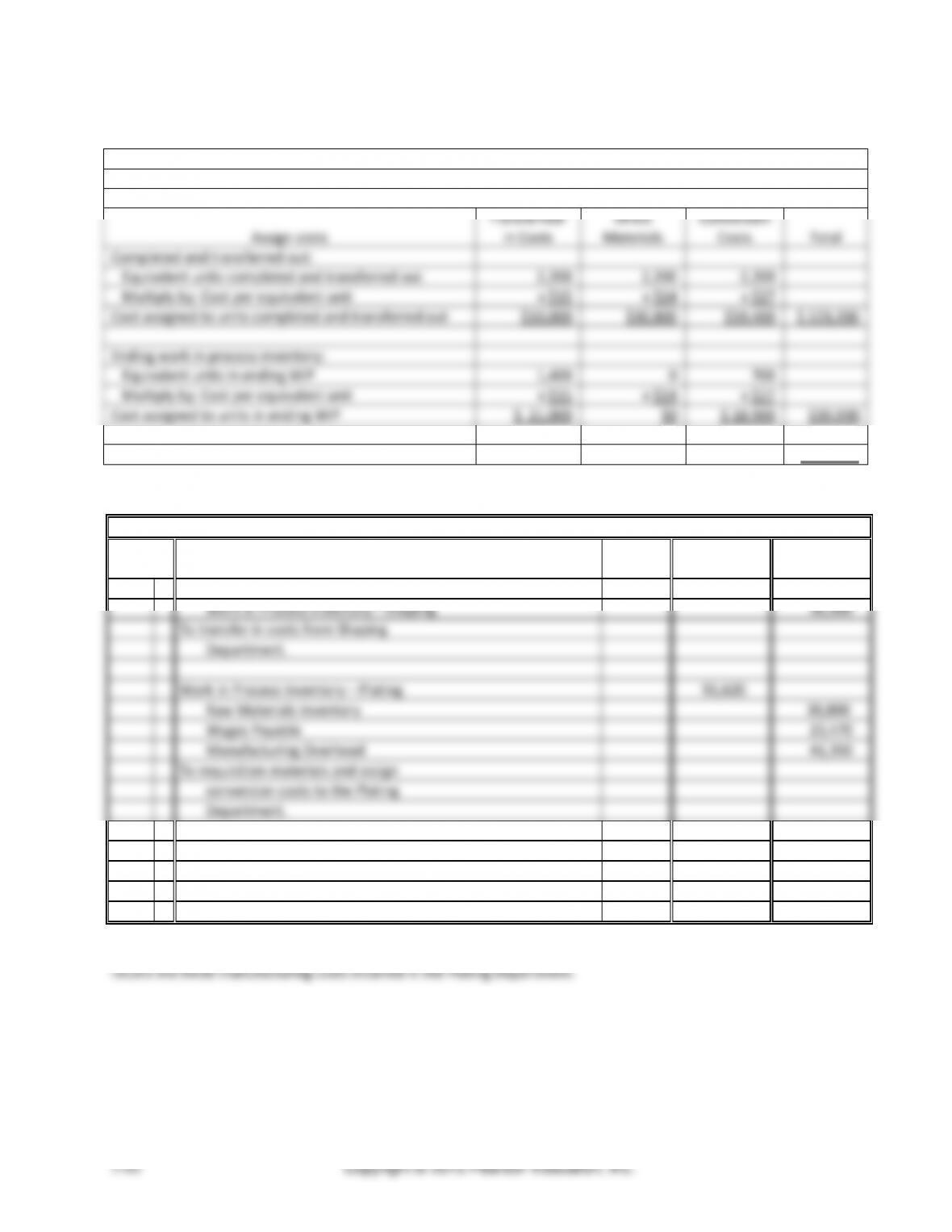

Completed and transferred out:

Equivalent units completed and transferred out

2,200

2,200

2,200

Multiply by: Cost per equivalent unit

x $15

x $14

x $27

Cost assigned to units completed and transferred out

$33,000

$30,800

$59,400

$ 123,200

Ending work in process inventory:

Equivalent units in ending WIP

1,400

0

700

Multiply by: Cost per equivalent unit

x $15

x $14

x $27

Cost assigned to units in ending WIP

$ 21,000

$0

$ 18,900

$39,900

Total costs accounted for

$163,100

Req. 3

Journal Entry

DATE

ACCOUNT TITLE AND EXPLANATION

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Plating

36,000

Work in Process Inventory—Shaping

36,000

To transfer in costs from Shaping

Department.

Work in Process Inventory—Plating

95,620

Raw Materials Inventory

30,800

Wages Payable

23,470

Manufacturing Overhead

41,350

To requisition materials and assign

conversion costs to the Plating

Department.

Finished Goods Inventory

123,200

Work in Process Inventory—Plating

123,200

To transfer cost of units completed to

finished goods.

Note: Students may have prepared three separate journal entries, rather than the one summary entry shown above, to

Managerial Accounting 4e Solutions Manual

(continued) P5-57B

Req. 5

The monthly operating income that would provide a 2% rate of return is:

Monthly return on investment

=

Monthly operating income

Investment

2%

=

Monthly operating income

$400,000

Monthly operating income

=

$400,000

×

2%

=

$8,000

To achieve a 2% rate of return, Jimmy’s Cricket Farm must charge a price that provides enough gross profit to cover

operating expenses of $2,000 and then provide $8,000 in operating income. This requires a gross profit of $10,000.

Gross profit

=

(Selling price per box – Cost per box)

×

Boxes sold

$10,000

=

(Selling price per box – $12.40)

×

19,000

$10,000

=

Selling price per box – $12.40

19,000

$0.5263*

=

Selling price per box – $12.40

$0.5263* + $12.40

=

Selling price per box

$12.93*

=

Selling price per box

*Rounded

Copyright © 2015 Pearson Education, Inc.

5-63

A5-58

1. What characteristics of the product or manufacturing process would lead a company to use a process costing

system?

A company that uses a series of steps or processes to make large quantities of identical units would use a process

costing system.

2. How are process costing and job costing similar? How are they different?

Process Costing and job costing are similar in these respects:

3. What are conversion costs? In a job costing system, at least some conversion costs are assigned directly to

4. Why not assign all costs of production during a period to only the completed units?

Some costs of production are included in the goods that were started but not completed.

What happens if a company does this?

Managerial Accounting 4e Solutions Manual

Copyright © 2015 Pearson Education, Inc.

5-64

If a company uses a just-in-time inventory system, they would not have any ending inventory. In that case, all the

costs of production would be assigned to the completed goods.

5. What information generated by a process costing system can be used by management? How can management

use this process costing information?

6. Why are the equivalent units for direct materials often different from the equivalent units for conversion costs

costs.

7. Describe the flow of costs in a process costing system. List each type of journal entry that would be made and

describe the purpose of that journal entry.

The flow of costs in a process costing system is similar to the flow of costs in a job order costing system. The main

difference is that direct materials, direct labor, and manufacturing overhead are assigned to processing

departments rather than jobs. In addition, a journal entry must be made at the end of the month to transfer costs

8. If a company has very little or no inventory, what effect does that lack of inventory have on its process costing

system?

The process costing system is easier to use because there is no need for determining equivalent units and

Managerial Accounting 4e Solutions Manual

Application & Analysis

A5–59

2. Summarize the production process.

Truckloads of russet potatoes arrive at the manufacturing plant where they are first scrubbed, then crinkle sliced

3. Justify why you think this production process would dictate the use of a process costing system.

4. List at least two separate processes that are performed in creating this product.

One process is scrubbing the potatoes and another is slicing the unpeeled potatoes.

5. Describe at least one department that would have ending work in process. What do the units look like as they

are “in process”?

Chapter 5 Process Costing

1. The ethical issues in this situation are:

a. Competence: “Perform professional duties in accordance with relevant laws, regulations, and technical

standards.” By changing the inventory records to show more inventory than actually exists, Quito is violating

2. Recording more units than are actually in inventory would impact the 2014 balance sheet and income statement

by having the starting inventory overreported.

3. He should bring up his concerns about the bonuses and losing employees to the supervisory staff members above

1. Which product(s) manufactured by Polly Products would use elements of a process costing system? Give a

detailed description of why you think that product (or those products) would require a process costing system.

2. Within the process costing portion of the hybrid system at Polly Products, what costs would be considered to be

direct materials? What costs are likely to be in conversion costs in the process costing system? (Use your

3. Which products manufactured by Polly Products would be likely to use elements of a job costing system? Again,

4. Within the job costing portion of the hybrid system at Polly Products, which are the direct materials? What

would be direct labor? What costs are likely to be in manufacturing overhead?