Copyright © 2015 Pearson Education, Inc.

5-41

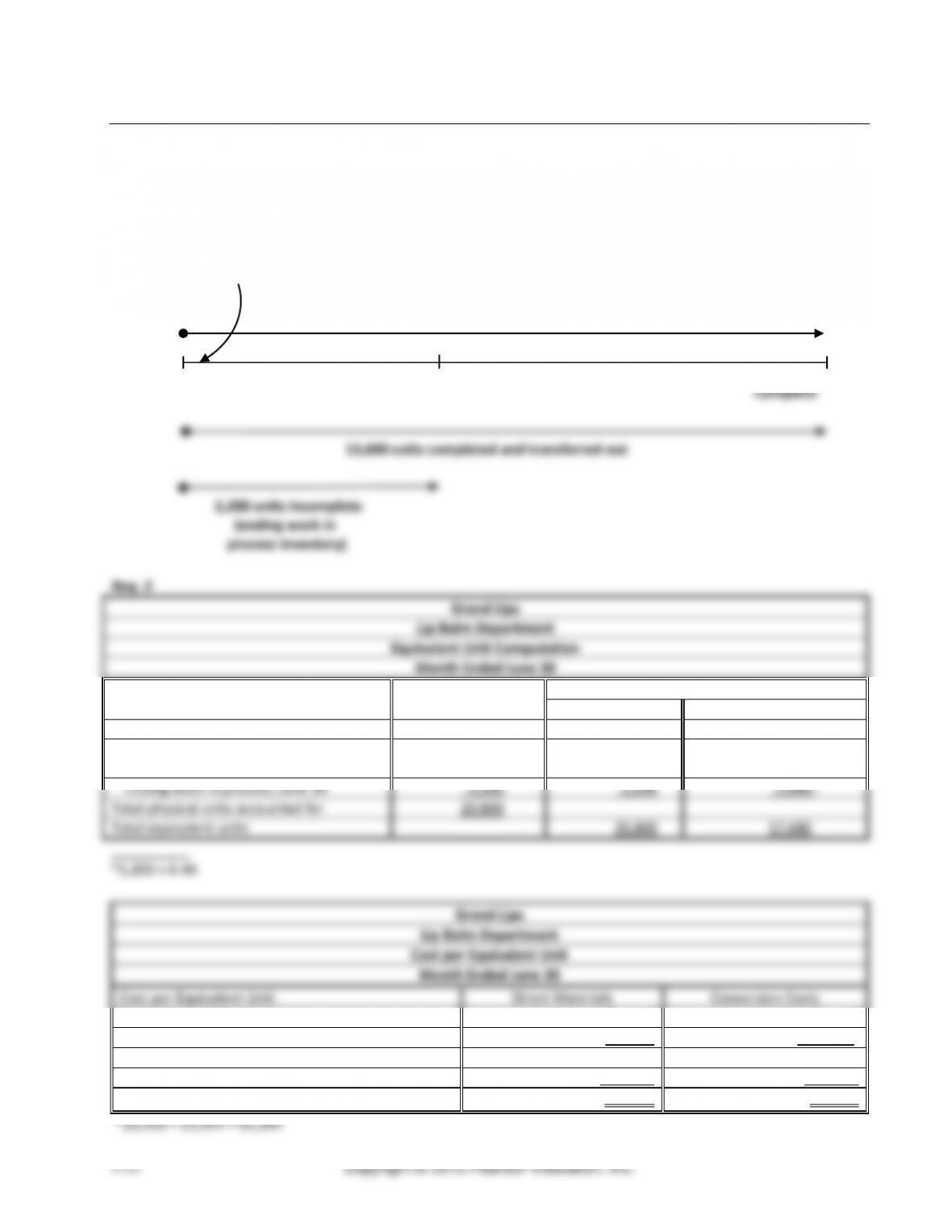

(30-45 min.) P5-48A

Req. 1

Direct

materials

added

Conversion costs added evenly throughout the process

Start 45% 100%

Managerial Accounting 4e Solutions Manual

(continued) P5-48A

Lopez Cosmetics

Lip Balm Department

Cost per Equivalent Unit

Month Ended June 30

Cost per Equivalent Unit:

Direct Materials

Conversion Costs

Beginning work in process June 1

$ 0

$ 0

Costs added during June

5,225

3,608d

Costs to account for

$ 5,225

$ 3,608

Divide by total equivalent units

÷ 20,900

÷ 18,040

Cost per equivalent unit

$ 0.25

$ 0.20

d$3,360 + $248 = $3,608

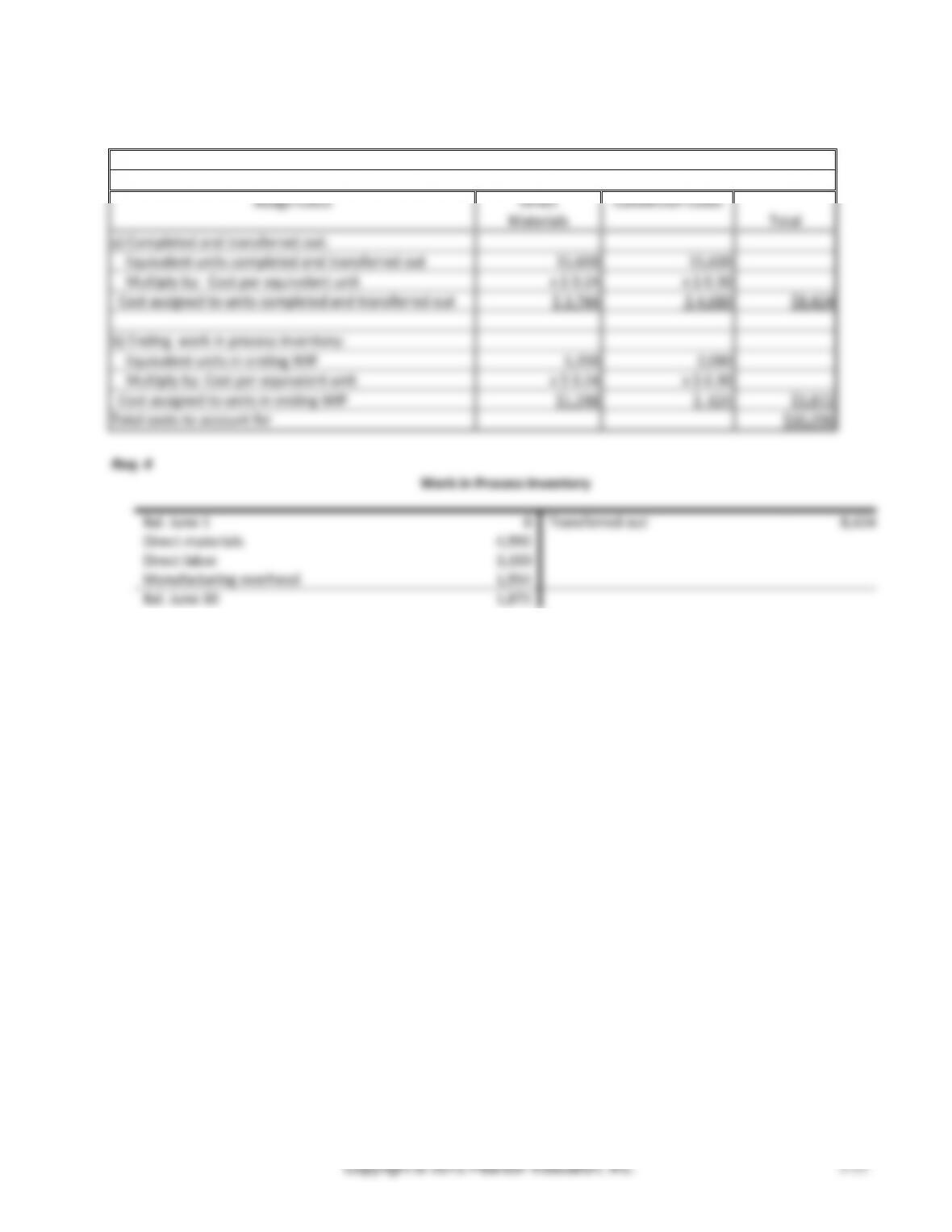

Req. 3

Lopez Cosmetics

Lip Balm Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

15,700

15,700

Multiply by: Cost per equivalent unit

x $ 0.25

x $ 0.20

Cost assigned to units completed and transferred out

$ 3,925

$ 3,140

$7,065

b) Ending work in process inventory:

Equivalent units in ending WIP

5,200

2,340

Multiply by: Cost per equivalent unit

x $ 0.25

x $ 0.20

Cost assigned to units in ending WIP

$1,300

$ 468

$1,768

Total costs to account for

$8,833

Req. 4

Work in Process Inventory

Bal. June 1

0

Transferred out

7,065

Direct materials

5,225

Direct labor

3,360

Manufacturing overhead

248

Bal. June 30

1,768

Chapter 5 Process Costing

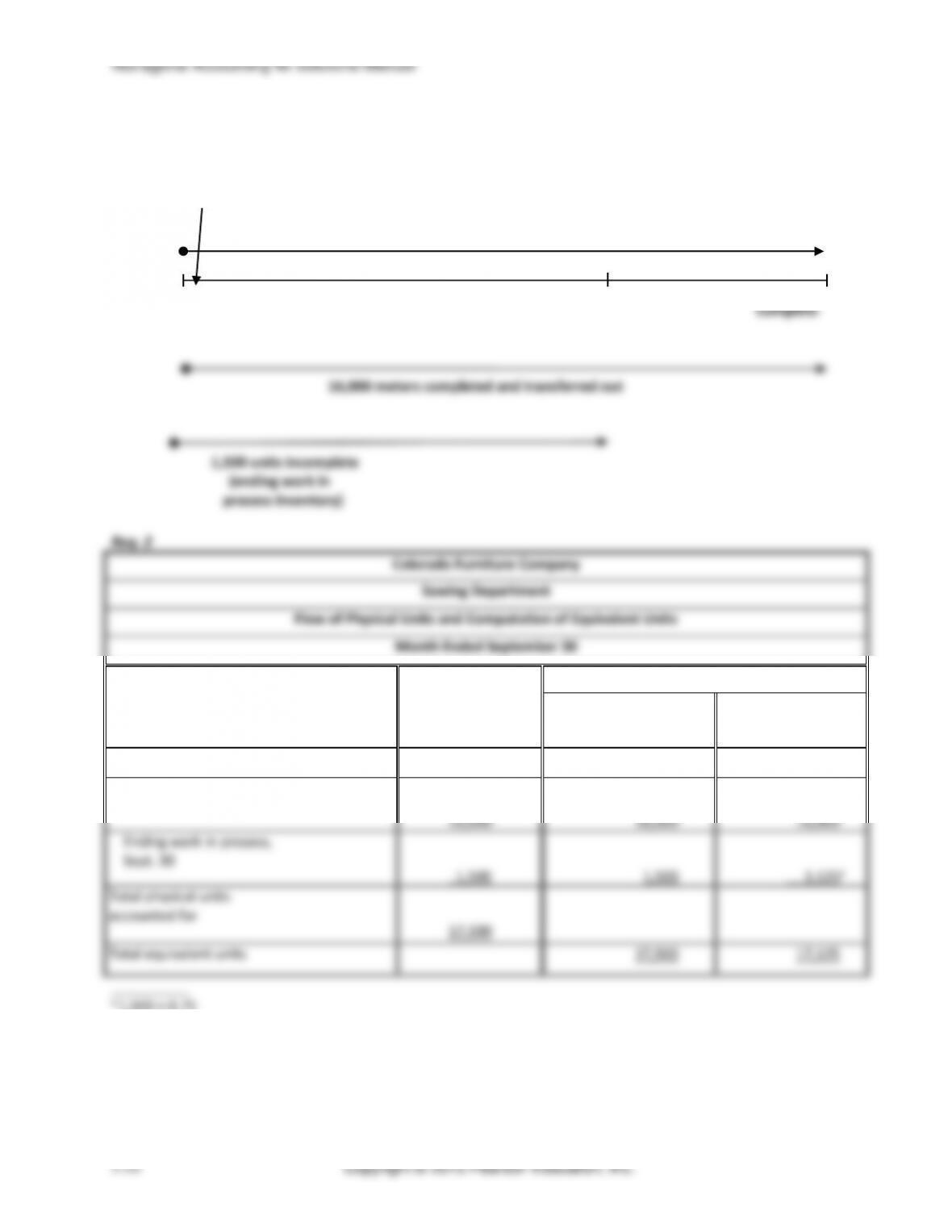

(30-45 min.) P5–49A

Req. 1

Direct

materials

added

Conversion costs added evenly throughout the process

Start 80% 100%

Managerial Accounting 4e Solutions Manual

(continued) P5–49A

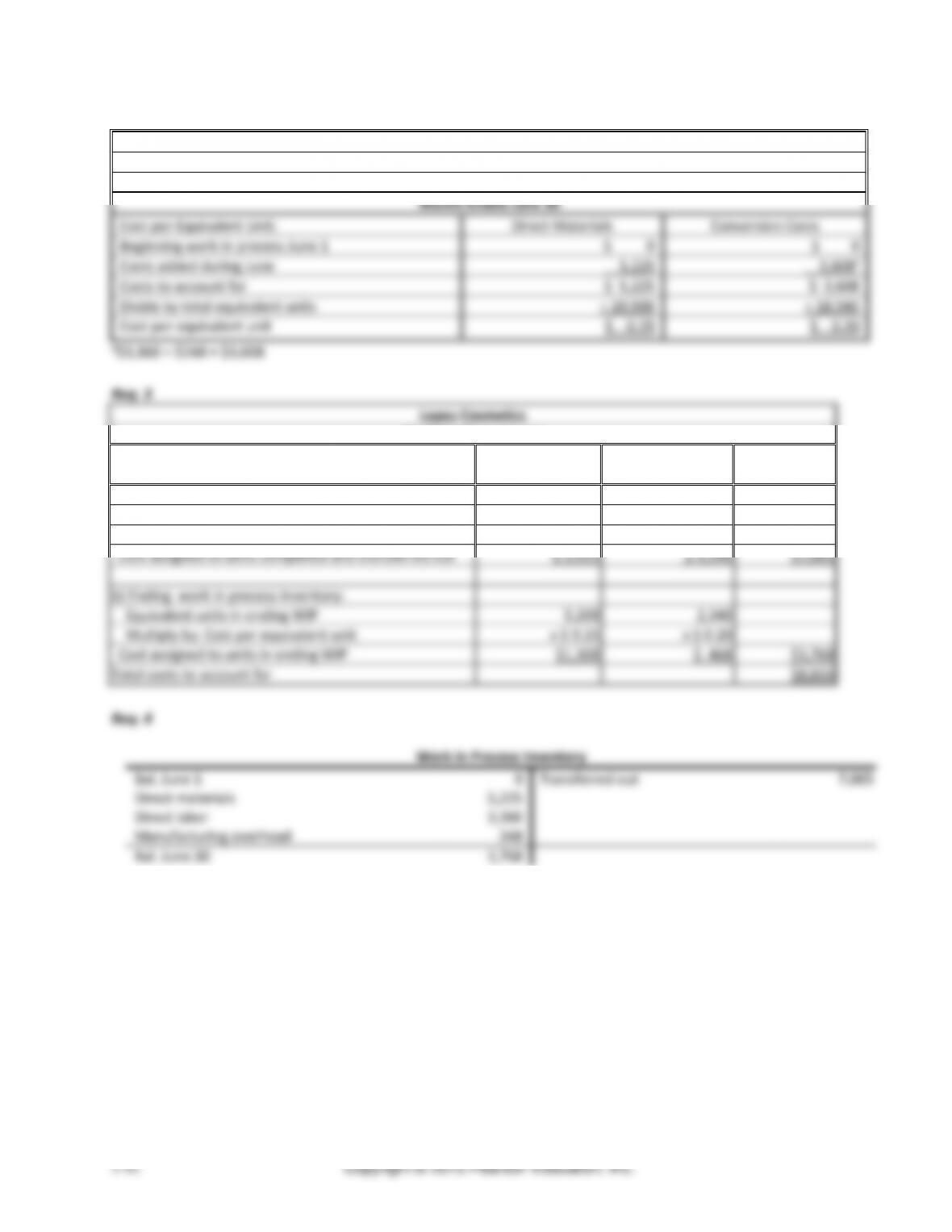

Northern Furniture Company

Sawing Department

Cost per Equivalent Unit

Month Ended September 30

Cost per Equivalent Unit:

Direct Materials

Conversion Costs

Total

Beginning work in process September 1

$ 0

$ 0

$ 0

Costs added during September

1,863,000

294,400

$2,157,400

Total costs to account for

$1,8463,000

$294,400

$2,157,400

Divide by total equivalent units

÷ 13,500

÷ 12,800

Cost per equivalent unit

$ 138

$ 23

__________ $137,000 + $157,400 = $294,400

Req. 3

Northern Furniture Company

Sawing Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

10,000

10,000

Multiply by: Cost per equivalent unit

x $ 138

x $ 23

Cost assigned to units completed and transferred out

$ 1,380,000

$ 230,000

$1,610,000

b) Ending work in process inventory:

Equivalent units in ending WIP

3,500

2,800

Multiply by: Cost per equivalent unit

x $ 138

x $ 23

Cost assigned to units in ending WIP

$483,000

$ 64,400

$547,400

Total costs to account for

$2,157,400

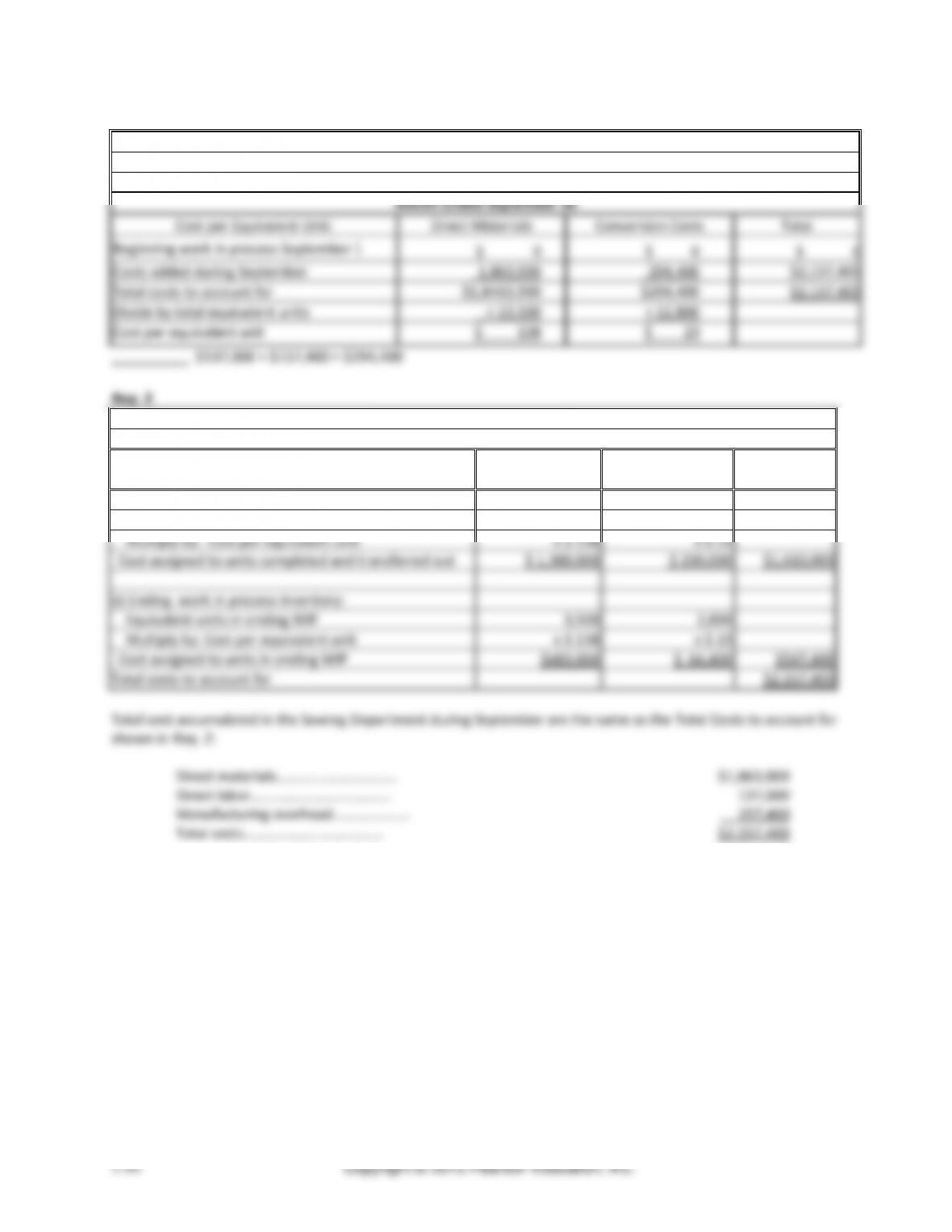

Total cost accumulated in the Sawing Department during September are the same as the Total Costs to account for

shown in Req. 2:

Direct materials……………………………

$1,863,000

Direct labor………………………………...

137,000

Manufacturing overhead…………………

157,400

Total costs…………………………………

$2,157,400

Chapter 5 Process Costing

(continued) P5–49A

Req. 4

Journal Entry

DATE

ACCOUNT TITLE AND EXPLANATION

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Sawing

2,157,400

Raw Materials Inventory

1,863,000

Wages Payable

137,000

Manufacturing Overhead

157,400

Work in Process Inventory—Assembly

1,610,000

Work in Process Inventory—Sawing

1,610,000

Note: Students may prepare three separate journal entry or the one summary journal entry (as shown above) to

record the three manufacturing costs.

(30-40 min.) P5-50A

Req. 1

Chicken and Green

cream peppers and

Managerial Accounting 4e Solutions Manual

(continued) P5-50A

Req. 2

Royce Chicken

Mixing Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Physical Units

Equivalent Units

Flow of Production

Chicken,

Cream

Green Peppers,

Mushrooms

Conversion

Costs

Units to account for:

Beginning work in process,

November 1

0

Started in production

14,200

Total physical units to account for

14,200

Units accounted for:

Completed and transferred out

13,200

13,200

13,200

13,200

Ending work in process,

November 30

1,000

1,000a

0a

600b

Total physical units accounted for

14,200

Total equivalent units

14,200

13,200

13,800

Beginning work in process

Costs added during Nov.

Costs to account for

Divide by total equivalent units

Chapter 5 Process Costing

(continued) P5-50A

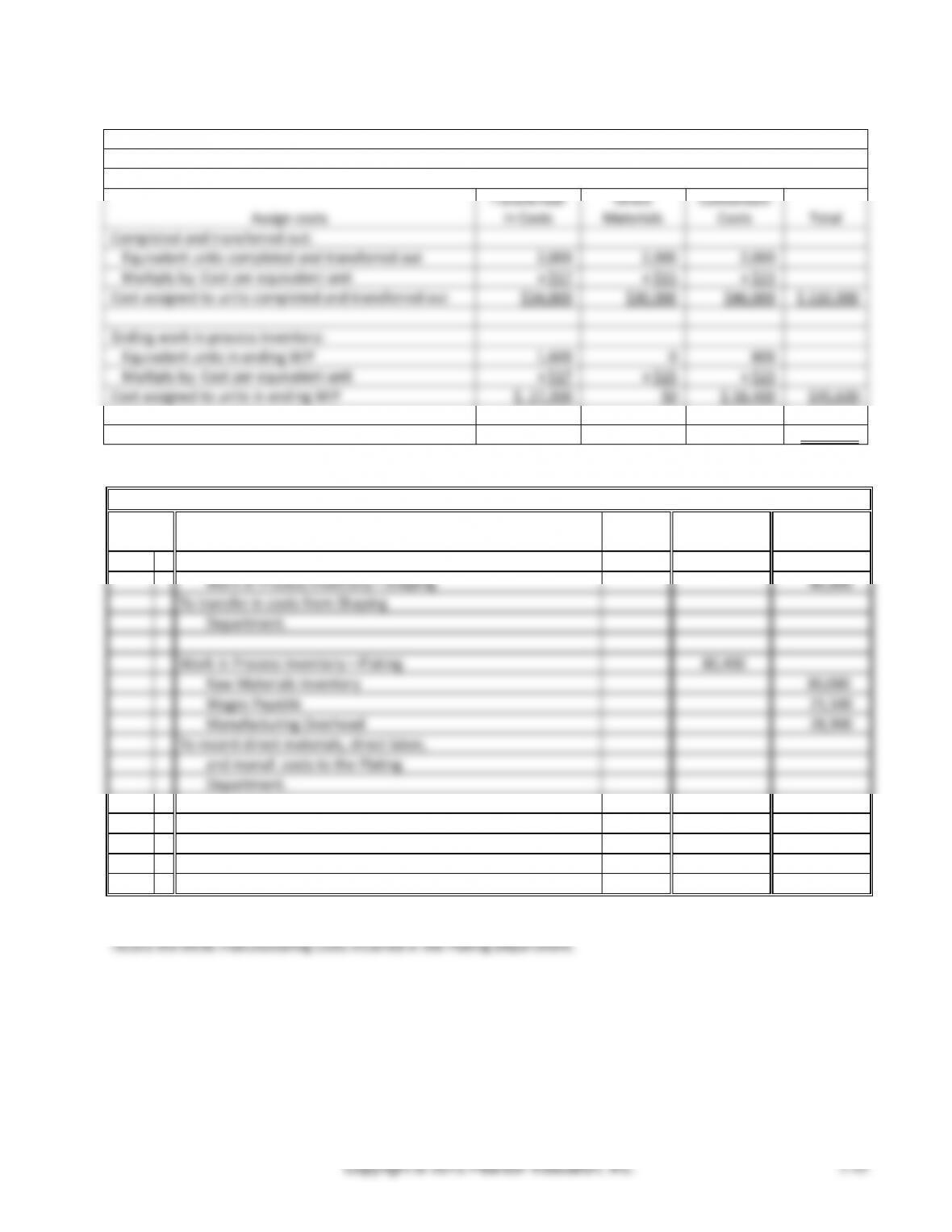

Req. 4

Royce Chicken

Mixing Department

Assignment of Costs

Assign costs

Chicken and

Cream

Green

Peppers &

Mushrooms

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

13,200

13,200

13,200

Multiply by: Cost per equivalent unit

x $1.40

x $0.60

x $1.04

Cost assigned to units completed and transferred out

18,480

$7,920

$13,728

$ 40,128

Ending work in process inventory:

Equivalent units in ending WIP

1,000

0

600

Multiply by: Cost per equivalent unit

x $1.40

x $0.60

x $1.04

Cost assigned to units in ending WIP

$ 1,400

$0

$624

$2,024

Total costs accounted for

$42,152

(45-60 min.) P5-51A

Req. 1

Transferred Direct

Managerial Accounting 4e Solutions Manual

(continued) P5-51A

Req. 2

Chrome Accessories

Plating Department

Equivalent Unit Computations (Weighted-Average)

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred

In

Direct Materials

Conversion

Costs

Units accounted for:

Completed and transferred out during March

2,000

2,000

2,000

2,000

Ending work in process, March 31

1,600

1,600a

0b

800c

Total physical units

accounted for

3,600

Total equivalent units

3,600

2,000

2,800

__________

a The time line shows that transferred-in costs are incurred at

the beginning of the plating process. Ending inventory was started this period, so it did pass the point where

transferred-in costs are added. The ending inventory is therefore complete with respect to transferred-in costs.

Beginning work in process, March 1

$14,000

Costs added during March

Total costs to account for

Divide by equivalent units

Cost per equivalent unit

Chapter 5 Process Costing

(continued) P5-51A

Chrome Accessories

Plating Department

Production Cost Report

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

2,000

2,000

2,000

Multiply by: Cost per equivalent unit

x $17

x $15

x $23

Cost assigned to units completed and transferred out

$34,000

$30,000

$46,000

$ 110,000

Ending work in process inventory:

Equivalent units in ending WIP

1,600

0

800

Multiply by: Cost per equivalent unit

x $17

x $15

x $23

Cost assigned to units in ending WIP

$ 27,200

$0

$ 18,400

$45,600

Total costs accounted for

$155,600

Req. 3

Journal Entry

DATE

ACCOUNT TITLE AND EXPLANATION

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Plating

40,800

Work in Process Inventory—Shaping

40,800

To transfer in costs from Shaping

Department.

Work in Process Inventory—Plating

80,400

Raw Materials Inventory

30,000

Wages Payable

21,500

Manufacturing Overhead

28,900

To record direct materials, direct labor,

and manuf. costs to the Plating

Department.

Finished Goods Inventory

110,000

Work in Process Inventory—Plating

110,000

To record cost of units completed and

transferred out.

Note: Students may have prepared three separate journal entries, rather than the one summary entry shown above, to

Chapter 5 Process Costing

(continued) P5-52A

Req. 5

In this requirement, we are proving that the current price of $12.60 per box does indeed provide the required 2.5%

return. The monthly operating income that would provide a 2.5% rate of return is:

Monthly return on investment

=

Monthly operating income

Investment

2.5%

=

Monthly operating income

$450,000

Monthly operating income

=

$450,000

×

2.5%

=

$11,250

To achieve a 2.5% rate of return, Charlie’s Cricket Farm must charge a price that provides enough gross profit to cover

operating expenses of $12,750 and then provide $11,250 in operating income. This requires a gross profit of $24,000.

Gross profit

=

(Selling price per box – Cost per box)

×

Boxes sold

$24,000

=

(Selling price per box – $11.40)

×

20,000

$24,000

=

Selling price per box – $11.40

20,000

$1.20

=

Selling price per box – $11.40

$1.20 + $11.40

=

Selling price per box

$12.60

=

Selling price per box

Managerial Accounting 4e Solutions Manual

Problems (Group B)

(30-45 min.) P5-53B

Req. 1

Direct

materials

added

Conversion costs added evenly throughout the process

Start 40% 100%

Chapter 5 Process Costing

(continued) P5-53B

Req. 3

Grand Lips

Lip Balm Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

15,600

15,600

Multiply by: Cost per equivalent unit

x $ 0.24

x $ 0.30

Cost assigned to units completed and transferred out

$ 3,744

$ 4,680

$8,424

b) Ending work in process inventory:

Equivalent units in ending WIP

5,200

2,080

Multiply by: Cost per equivalent unit

x $ 0.24

x $ 0.30

Cost assigned to units in ending WIP

$1,248

$ 624

$1,872

Total costs to account for

$10,296

Req. 4

Work in Process Inventory

Bal. June 1

0

Transferred out

8,424

Direct materials

4,992

Direct labor

3,350

Manufacturing overhead

1,954

Bal. June 30

1,872