Chapter 5 Process Costing

(continued) E5-31A

Req. 2

Cambria Winery

Fermenting Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Physical Units

Equivalent Units

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work in process, March 1

2,900

Started in production during March

4,770

Total physical units to account for

7,670

Units accounted for:

Completed and transferred out

during March

6,420

6,420

6,420

Ending work in process, March 31

1,250

1,250a

1,000b

Total physical units accounted for

7,670

Total equivalent units

7,670

7,420

__________

Managerial Accounting 4e Solutions Manual

(continued) E5-31A

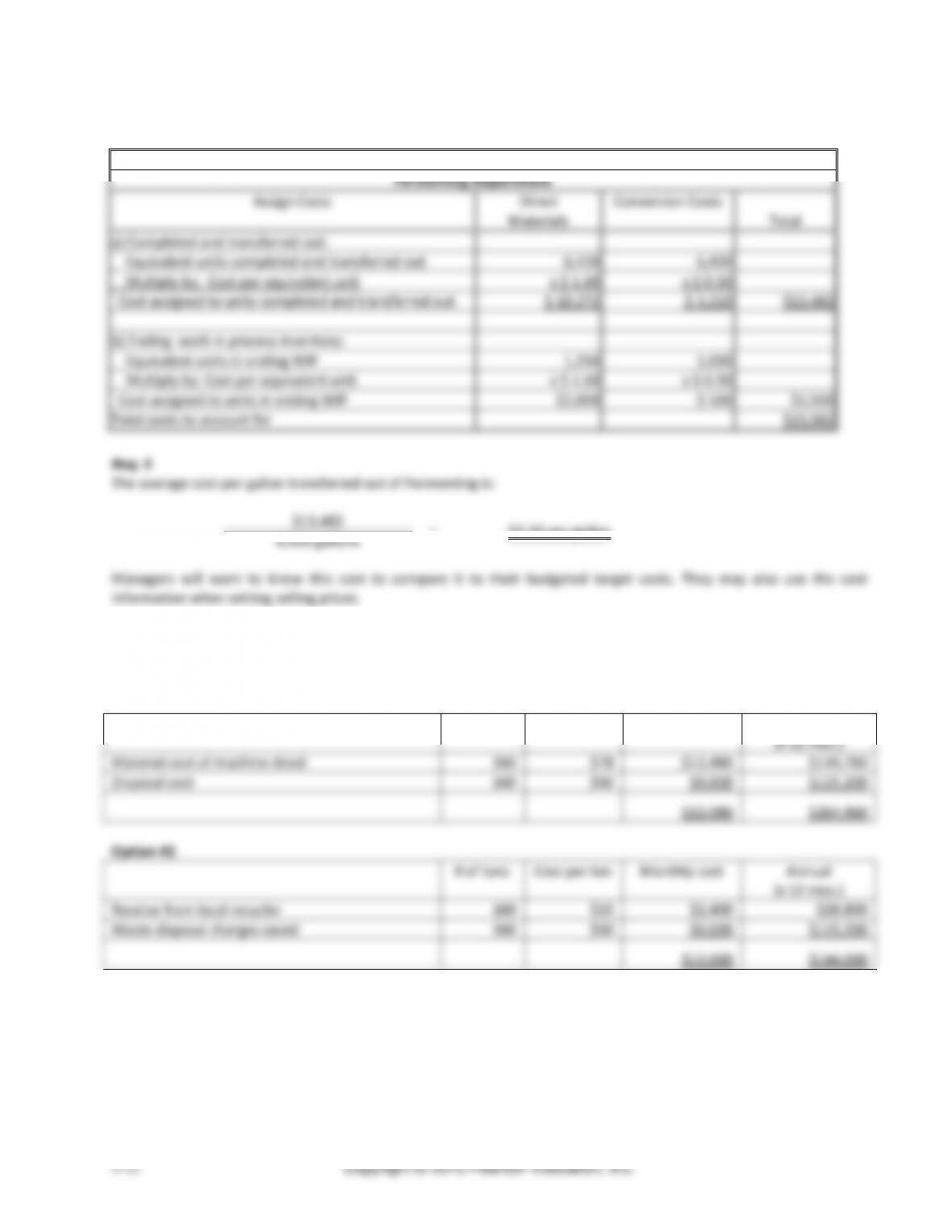

Req. 4

Cambria Winery

Fermenting Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

6,420

6,420

Multiply by: Cost per equivalent unit

x $ 1.60

x $ 0.50

Cost assigned to units completed and transferred out

$ 10,272

$ 3,210

$13,482

b) Ending work in process inventory:

Equivalent units in ending WIP

1,250

1,000

Multiply by: Cost per equivalent unit

x $ 1.60

x $ 0.50

Cost assigned to units in ending WIP

$2,000

$ 500

$2,500

Total costs to account for

$15,982

Req. 5

The average cost per gallon transferred out of Fermenting is:

$13,482

=

$2.10 per gallon

6,420 gallons

Managers will want to know this cost to compare it to their budgeted target costs. They may also use the cost

information when setting selling prices.

(15 min.) E5-32A

Reqs. 1 – 3

Option #1

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

Material cost of machine drool

160

$78

$12,480

$149,760

Disposal cost

160

$60

$9,600

$115,200

$22,080

$264,960

Option #2

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

Receive from local recycler

160

$15

$2,400

$28,800

Waste disposal charges saved

160

$60

$9,600

$115,200

$12,000

$144,000

Chapter 5 Process Costing

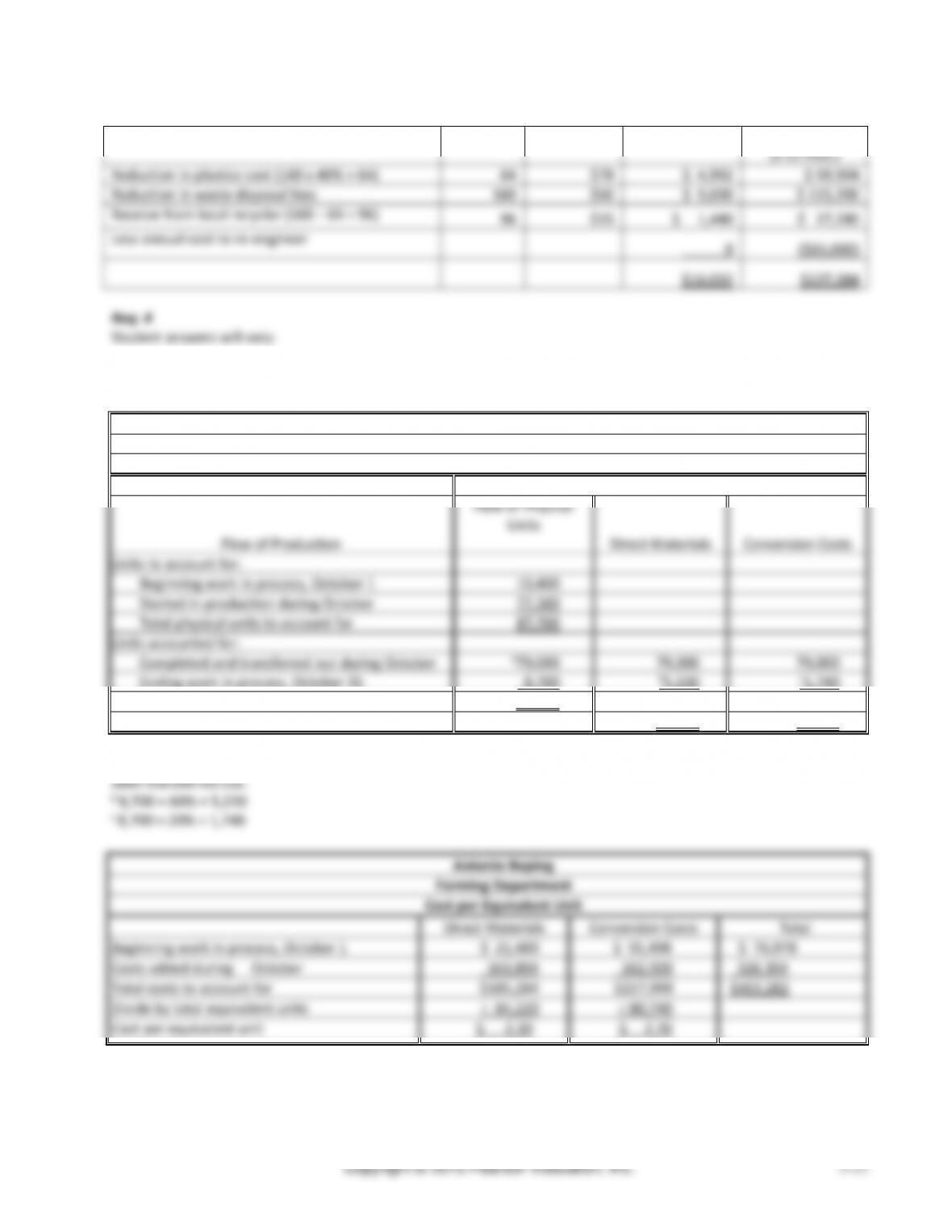

(continued) E5-32A

Option #3

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

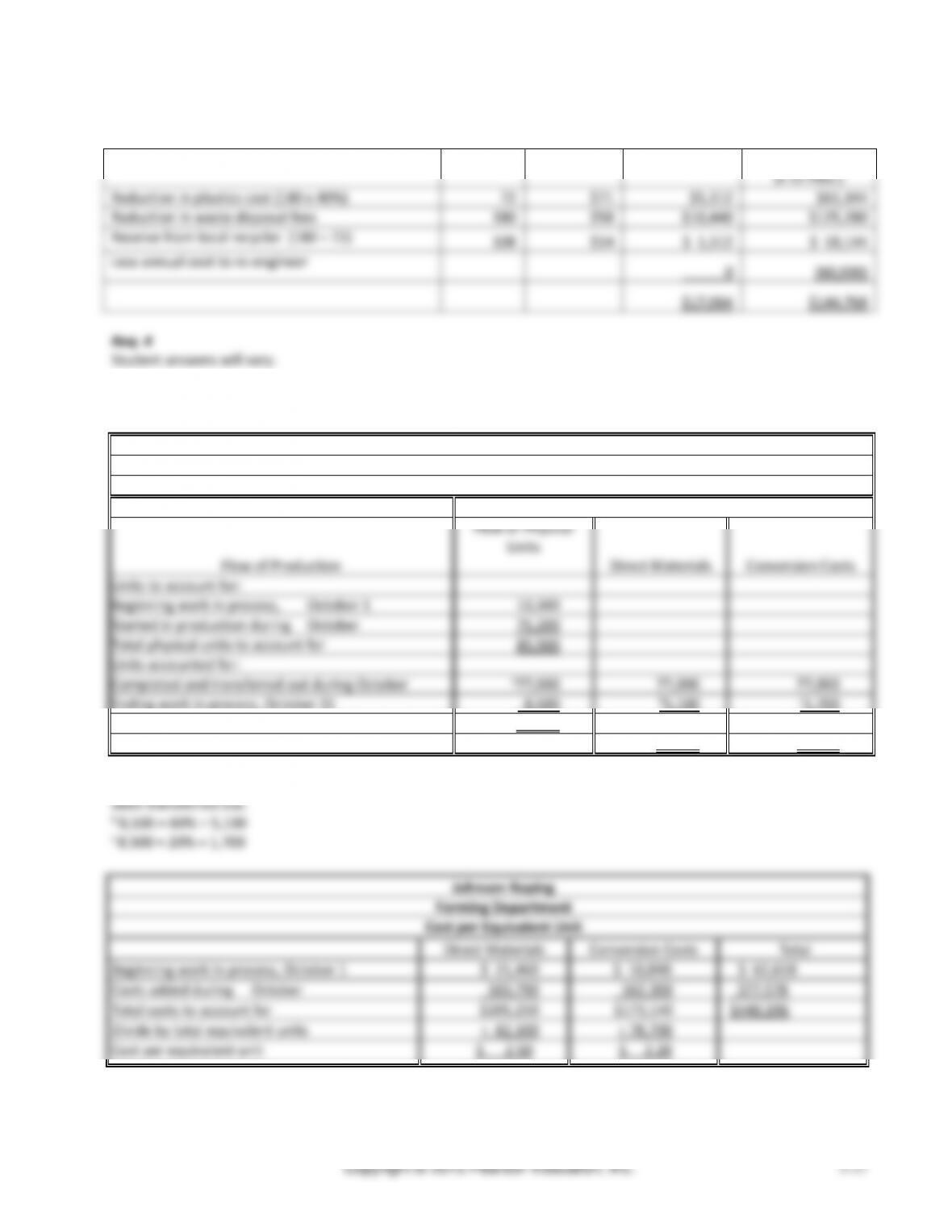

Reduction in plastics cost (160 x 40% = 64)

64

$78

$ 4,992

$ 59,904

Reduction in waste disposal fees

160

$60

$ 9,600

$ 115,200

Receive from local recycler (160 – 64 = 96)

96

$15

$ 1,440

$ 17,280

Less annual cost to re-engineer

0

($65,000)

$16.032

$127,384

Req. 4

Student answers will vary.

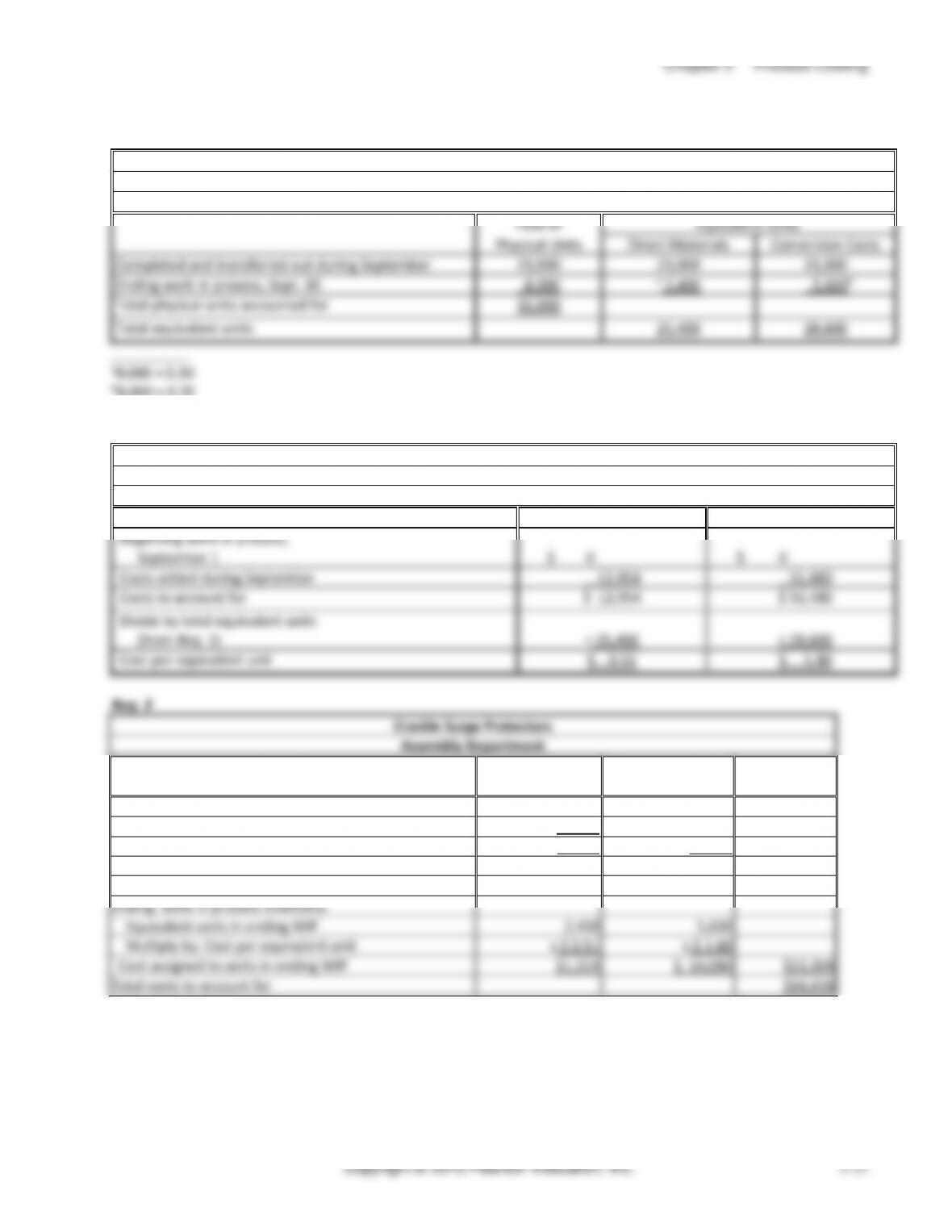

(15-20 min.) E5-33A

Antonio Roping

Forming Department

Physical Flow of Units and Equivalent Units

Equivalent Units

Flow of Production

Flow of Physical

Units

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, October 1

10,400

Started in production during October

77,300

Total physical units to account for

87,700

Units accounted for:

Completed and transferred out during October

a79,000

79,000

79,000

Ending work in process, October 31

8,700

b5,220

c1,740

Total physical units accounted for

87,700

Total Equivalent Units

84,220

80,740

__________

a 87,700 physical units to account for minus the 8,700 still in ending work in process inventory = 79,000 that must have

Forming Department

$185,284

Managerial Accounting 4e Solutions Manual

(continued) E5-33A

Antonio Roping

Forming Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

79,000

79,000

Multiply by: Cost per equivalent unit

x $ 2.20

x $ 2.70

Cost assigned to units completed and transferred out

$ 173,800

$ 213,300

$387,100

b) Ending work in process inventory:

Equivalent units in ending WIP

5,220

1,740

Multiply by: Cost per equivalent unit

x $ 2.20

x $ 2.70

Cost assigned to units in ending WIP

$11,484

$ 4,698

$16,182

Total costs to account for

$403,282

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Finishing

387,100

Work in Process Inventory—Forming

387,100

(15-20 mins.) E5-34A

Waterfall Fudge

Mixing Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred In

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, May 1

28,000

Transferred in during May

72,000

Total physical units to account for

100,000

Units accounted for:

Completed and transferred out

during May

85,000

85,000

85,000

85,000

Ending work in process, May 31

15,000

15,000

12,000a

3,000b

Total physical units accounted for

100,000

Total equivalent units

100,000

97,000

88,000

__________

a Direct materials: 15,000 units × 0.80 = 12,000

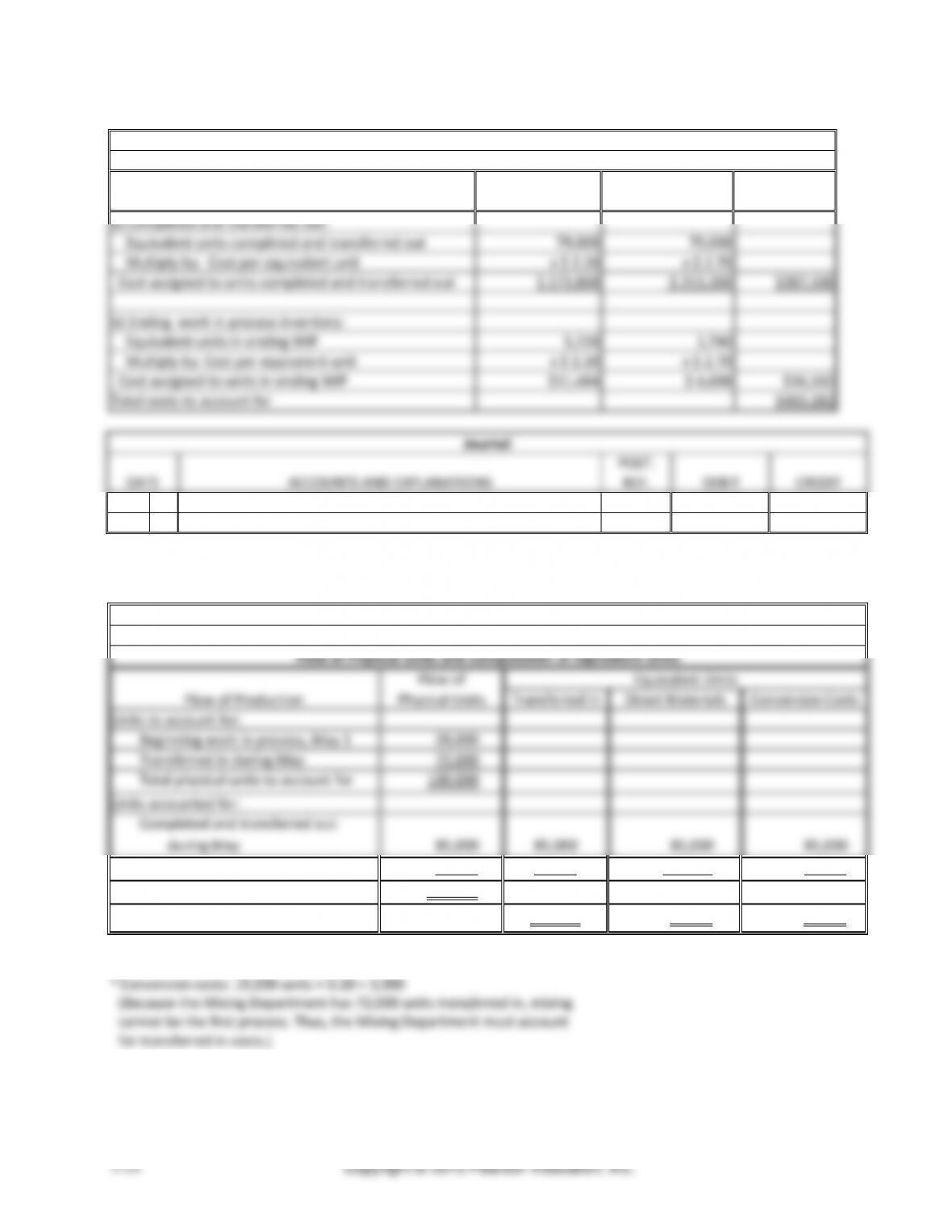

Chapter 5 Process Costing

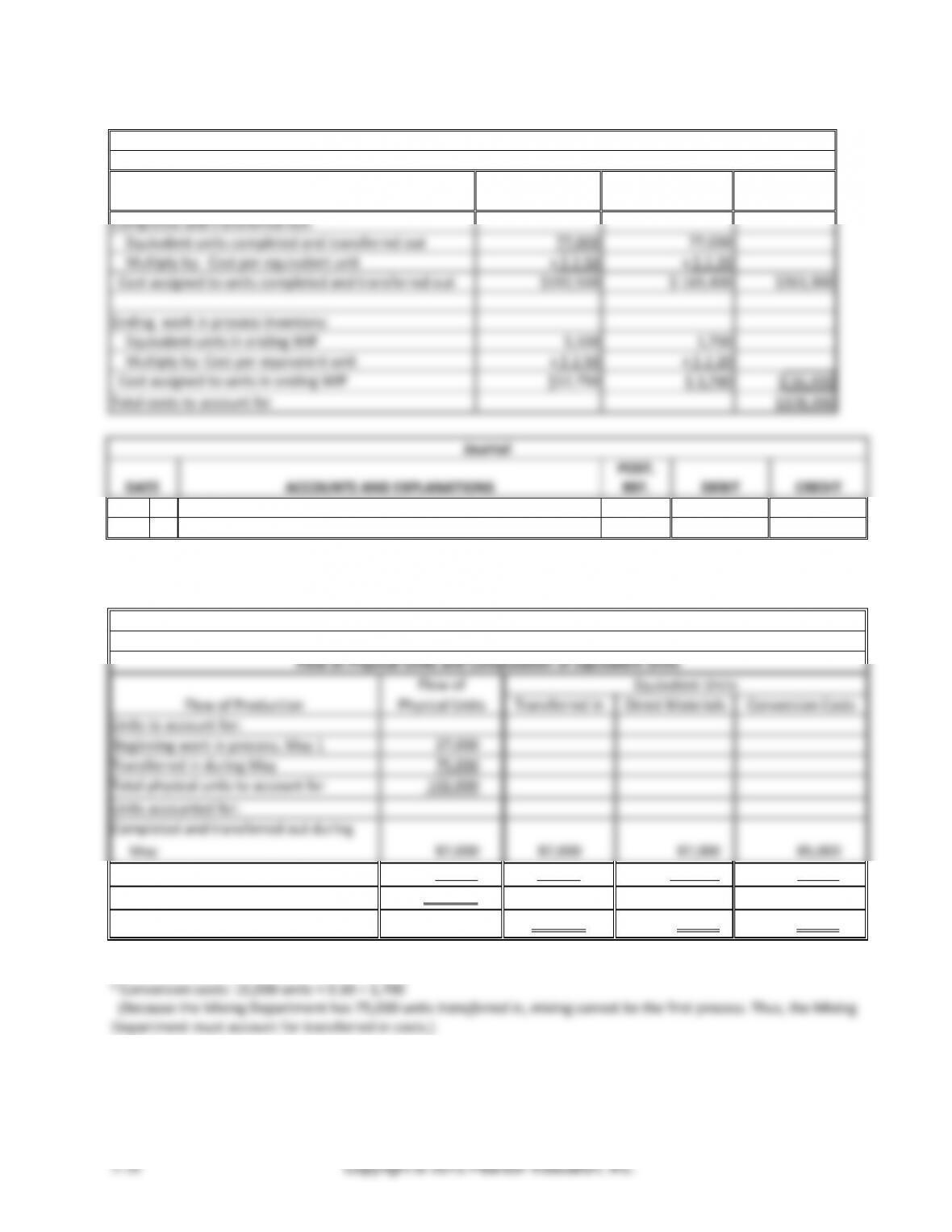

(continued) E5-34A

Waterfall Fudge

Heating Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred In

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, May 1

6,000

Transferred in during May

85,000

Total physical units to account for

91,000

Units accounted for:

Completed and

transferred out

during May:

79,000

79,000

79,000

79,000

Ending work in process, May 31

12,000

12,000

7,800a

6,600b

Total physical units accounted for

91,000

Total equivalent units

91,000

86,800

85,600

__________

a Direct materials: 12,000 units × 0.65 = 7,800

Flow of Physical Units and Computation of Equivalent Units

Units to account for:

9,000

Transferred in during December

23,000

Total physical units to account for

32,000

Units accounted for:

Completed and transferred out

during December

Ending work in process, December 31

32,000

Managerial Accounting 4e Solutions Manual

(continued) E5–35A

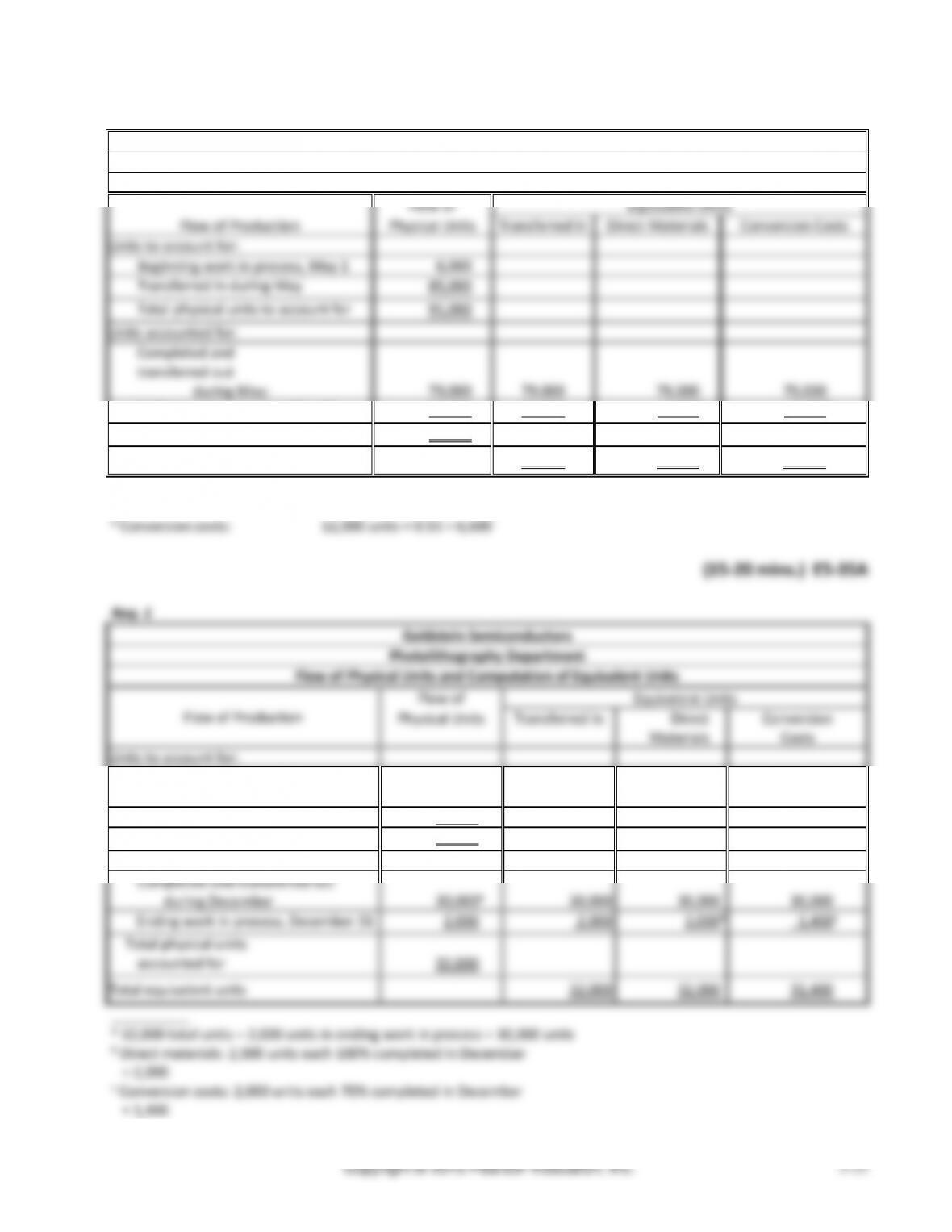

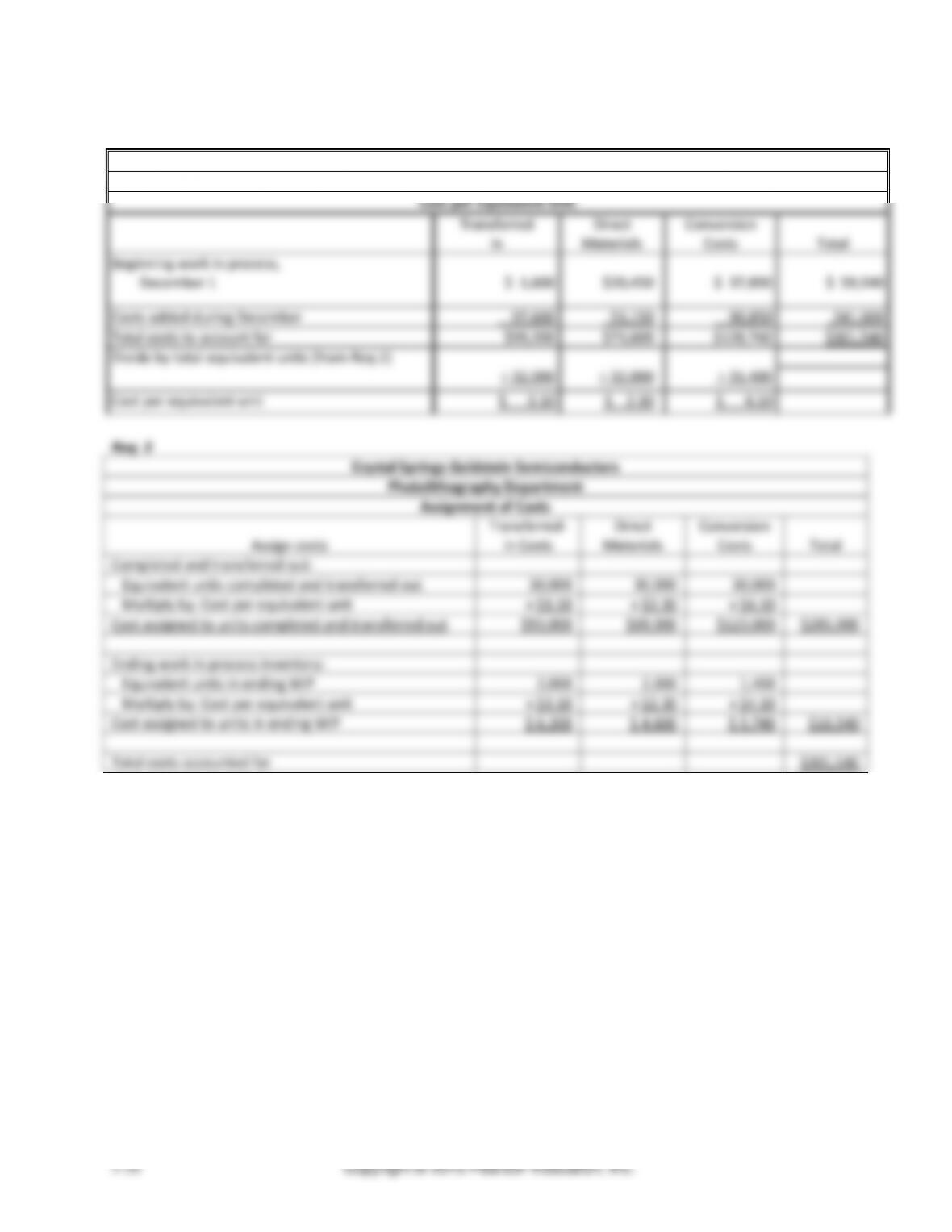

Req. 2

Goldstein Semiconductors

Photolithography Department

Cost per Equivalent Unit

Transferred

In

Direct

Materials

Conversion

Costs

Total

Beginning work in process,

December 1

$ 1,600

$20,450

$ 37,890

$ 59,940

Costs added during December

97,600

53,150

90,850

241,600

Total costs to account for

$99,200

$73,600

$128,740

$301,540

Divide by total equivalent units (from Req.1)

÷ 32,000

÷ 32,000

÷ 31,400

Cost per equivalent unit

$ 3.10

$ 2.30

$ 4.10

Req. 3

Crystal Springs Goldstein Semiconductors

Photolithography Department

Assignment of Costs

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

30,000

30,000

30,000

Multiply by: Cost per equivalent unit

x $3.10

x $2.30

x $4.10

Cost assigned to units completed and transferred out

$93,000

$69,000

$123,000

$285,000

Ending work in process inventory:

Equivalent units in ending WIP

2,000

2,000

1,400

Multiply by: Cost per equivalent unit

x $3.10

x $2.30

x $4.10

Cost assigned to units in ending WIP

$ 6,200

$ 4,600

$ 5,740

$16,540

Total costs accounted for

$301,540

Chapter 5 Process Costing

Exercises (Group B)

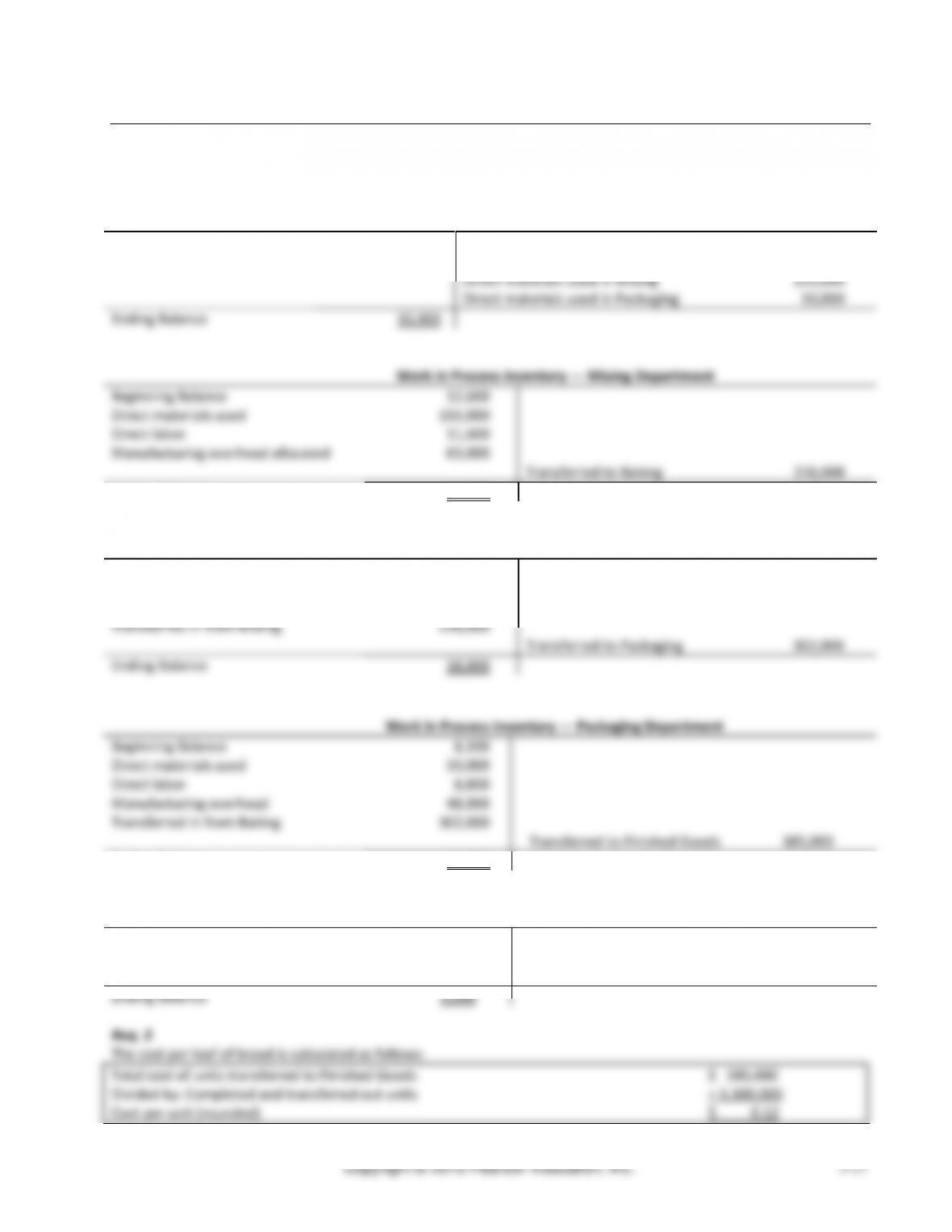

(15-20 min.) E5–36B

Reqs. 1 and 2

Raw Materials Inventory

Beginning Balance

23,300

Direct materials purchased

175,000

Direct materials used in Mixing

155,000

Direct materials used in Packaging

33,000

Ending Balance

10,300

Beginning Balance

12,600

Direct materials used

155,000

Direct labor

11,600

Manufacturing overhead allocated

63,000

Transferred to Baking

226,000

Ending Balance

16,200

Beginning Balance

15,200

Direct labor

Manufacturing overhead

74,000

Transferred in from Mixing

226,000

Transferred to Packaging

Ending Balance

18,000

Beginning Balance

Direct materials used

33,000

Direct labor

Manufacturing overhead

48,000

Transferred in from Baking

302,000

Ending Balance

14,900

Beginning Balance

Transferred in from Packaging

Ending Balance

The cost per loaf of bread is calculated as follows:

Chapter 5 Process Costing

(20 min.) E5–39B

Req. 1

Conversion costs added evenly throughout the process

Direct materials

Managerial Accounting 4e Solutions Manual

(continued) E5–39B

Req. 3

Shannon Paint Company

Blending Department

Cost per Equivalent Unit

Cost per Equivalent Unit:

Direct Materials

Conversion Costs

Total

Beginning work in process, May 1

$ 0

$ 0

$ 0

Costs added during May

5,166

2,429

$7,595

Total costs to account for

$5,166

$2,429

$7,595

Divide by total equivalent units (from Req. 2)

÷ 8,200

÷ 6,940

Cost per equivalent unit

$ 0.63

$ 0.35

__________

$600 + $1,829 = $2,429

Req. 4

Shannon Paint Company

Blending Department

Assign Costs

Direct

Materials

Conversion Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

6,100

6,100

Multiply by: Cost per equivalent unit

x $ 0.63

x $ 0.35

Cost assigned to units completed and transferred out

$ 3,843

$ 2,135

$5,978

Ending work in process inventory:

Equivalent units in ending WIP

2,100

840

Multiply by: Cost per equivalent unit

x $ 0.63

x $ 0.35

Cost assigned to units in ending WIP

$1,323

$ 294

$1,617

Total Costs to account for

$7,595

Req. 5

The average cost per gallon transferred out of blending is:

$5,978

=

$.98 per gallon

6,100 gallons

Managers will want to know this cost to compare it to their budgeted target costs. They may also use the cost

information when setting selling prices.

Chapter 5 Process Costing

(15 min.) E5-40B

Req. 1

Note: Students may prepare 3 separate journal entries or one summary entry (as shown below) to record the three

manufacturing costs.

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Blending

7,595

Raw Materials Inventory

5,166

Wages Payable

600

Manufacturing Overhead

1,829

Work in Process Inventory—Packaging

5,978

Work in Process Inventory—Blending

5,978

(from Req. 4 of E5-40B)

Req. 2

Work in Process Inventory—Blending

Bal. May 1

0

Transferred to Packaging

5,978

Direct materials

5,166

Direct labor

600

Manufacturing overhead

1,829

Bal. May 31

1,617

Managerial Accounting 4e Solutions Manual

(15-20 min.) E5-41B

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

a.

Raw Materials Inventory

9,900

Accounts Payable

9,900

b.

Work in Process Inventory—Assembly

4,400

Raw Materials Inventory

4,400

Work in Process Inventory—Finishing

2,800

Raw Materials Inventory

2,800

c.

Work in Process Inventory – Assembly

10,300

Cash

10,300

d.

Manufacturing Overhead

10,700

Property Taxes Payable—Plant

1,500

Utilities Payable

4,500

Prepaid Insurance—Plant

1,400

Accumulated Depreciation—Plant

3,300

e.

Work in Process Inventory—Assembly

7,700

Wages Payable

5,000

Manufacturing Overhead

2,700

f.

Work in Process Inventory—Finishing

10,300

Wages Payable

4,300

Manufacturing Overhead

6,000

g.

Work in Process Inventory—Finishing

10,200

Work in Process Inventory—Assembly

10,200

h.

Finished Goods Inventory

15,300

Work in Process Inventory—Finishing

15,300

Managerial Accounting 4e Solutions Manual

(continued) E5-42B

Req. 4

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Testing

53,130

Work in Process Inventory—Assembly

53,130

Chapter 5 Process Costing

(continued) E5-43B

Req. 2

Cove Point Winery

Fermenting Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Physical Units

Equivalent Units

Flow of Production

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work in process, March 1

2,000

Started in production during March

6,000

Total physical units to account for

8,000

Units accounted for:

Completed and transferred out

during March

6,550

6,550

6,550

Ending work in process, March 31

1,450

1,450a

1,160b

Total physical units accounted for

8,000

Total equivalent units

8,000

7,710

__________

Managerial Accounting 4e Solutions Manual

(continued) E5-43B

Req. 4

Cove Point Winery

Fermenting Department

Assign Costs

Direct

Materials

Conversion Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

6,550

6,550

Multiply by: Cost per equivalent unit

x $ 1.45

x $ 0.90

Cost assigned to units completed and transferred out

$ 9,497.50

$ 5,895

$15,392.50

Ending work in process inventory:

Equivalent units in ending WIP

1,450

1,160

Multiply by: Cost per equivalent unit

x $ 1.45

x $ 0.90

Cost assigned to units in ending WIP

$2,102.50

$ 1,044.00

$ 3,146.50

Total costs to account for

$18,539

Req. 5

The average cost per gallon transferred out of Fermenting is:

$15,392.50

=

$2.35 per gallon

6,550 gallons

Managers will want to know this cost to compare it to their budgeted target costs. They may also use the cost

information when setting selling prices.

(15 min.) E5-44B

Reqs. 1- 3

Option #1

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

Material cost of machine drool

180

$71

$12,780

$153,360

Disposal cost

180

$58

$10,440

$125,280

$23,220

$278,640

Option #2

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

Receive from local recycler

180

$14

$2,520

$30,240

Waste disposal charges saved

180

$58

$10,440

$125,280

$12,960

$155,520

Chapter 5 Process Costing

(continued) E5-44B

Option #3

# of tons

Cost per ton

Monthly cost

Annual

(x 12 mos.)

Reduction in plastics cost (180 x 40%)

72

$71

$5,112

$61,344

Reduction in waste disposal fees

180

$58

$10,440

$125,280

Receive from local recycler (180 – 72)

108

$14

$ 1,512

$ 18,144

Less annual cost to re-engineer

0

(60,000)

$17,064

$144,768

(15-20 min.) E5-45B

Johnson Roping

Forming Department

Physical Flow of Units and Equivalent Units

Equivalent Units

Flow of Production

Flow of Physical

Units

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, October 1

10,300

Started in production during October

75,200

Total physical units to account for

85,500

Units accounted for:

Completed and transferred out during October

a77,000

77,000

77,000

Ending work in process, October 31

8,500

b5,100

c1,700

Total physical units accounted for

85,500

Total Equivalent Units

82,100

78,700

__________

a 85,500 physical units to account for minus the 8,500 still in ending work in process inventory = 77,000 that must have

$205,250

Managerial Accounting 4e Solutions Manual

(continued) E5-45B

Johnson Roping

Forming Department

Assign Costs

Direct

Materials

Conversion Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

77,000

77,000

Multiply by: Cost per equivalent unit

x $ 2.50

x $ 2.20

Cost assigned to units completed and transferred out

$192,500

$ 169,400

$361,900

Ending work in process inventory:

Equivalent units in ending WIP

5,100

1,700

Multiply by: Cost per equivalent unit

x $ 2.50

x $ 2.20

Cost assigned to units in ending WIP

$12,750

$ 3,740

$ 16,490

Total costs to account for

$378,390

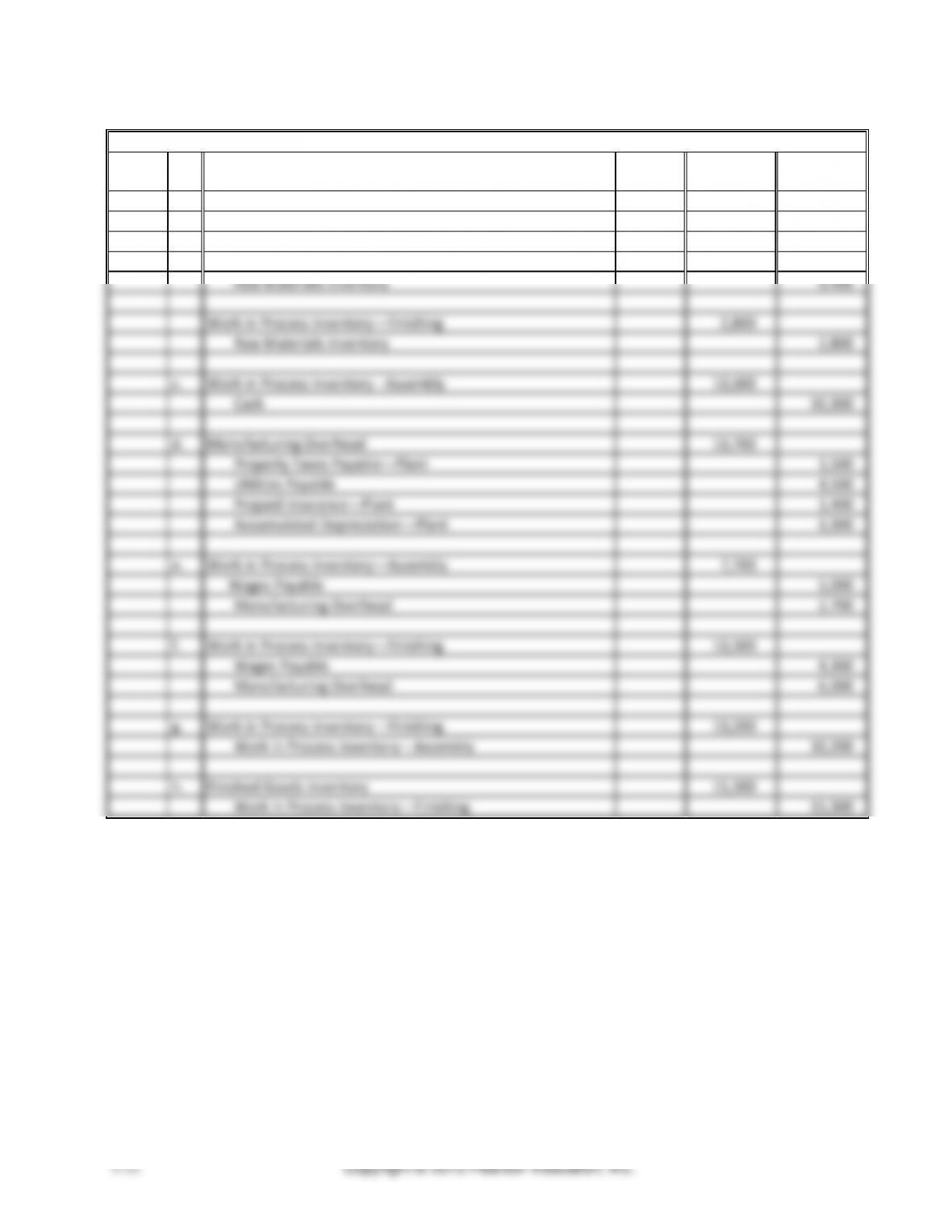

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Finishing

361,900

Work in Process Inventory—Forming

361,900

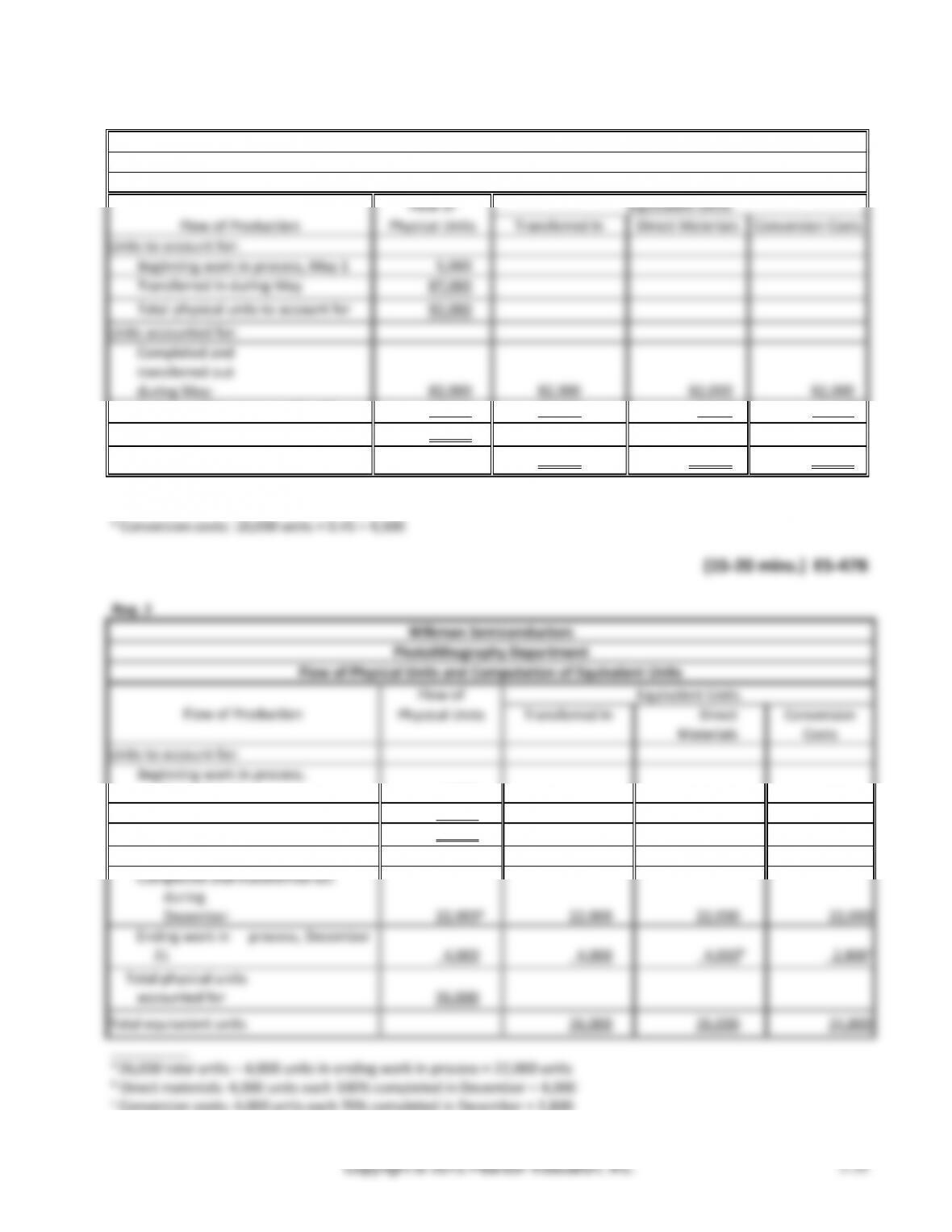

(15-20 mins.) E5-46B

Abby’s Fudge

Mixing Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred In

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, May 1

27,000

Transferred in during May

75,000

Total physical units to account for

102,000

Units accounted for:

Completed and transferred out during

May

87,000

87,000

87,000

85,000

Ending work in process, May 31

15,000

15,000

12,000a

1,500b

Total physical units accounted for

102,000

Total equivalent units

102,000

99,000

86,500

__________

a Direct materials: 15,000 units × 0.80 = 13,600

Chapter 5 Process Costing

(continued) E5-46B

Abby’s Fudge

Heating Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Flow of Production

Physical Units

Transferred In

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, May 1

5,000

Transferred in during May

87,000

Total physical units to account for

92,000

Units accounted for:

Completed and

transferred out

during May:

82,000

82,000

82,000

82,000

Ending work in process, May 31

10,000

10,000

5,500a

4,500b

Total physical units accounted for

92,000

Total equivalent units

92,000

87,500

86,500

__________

a Direct materials: 10,000 units × 0.55 = 5,500

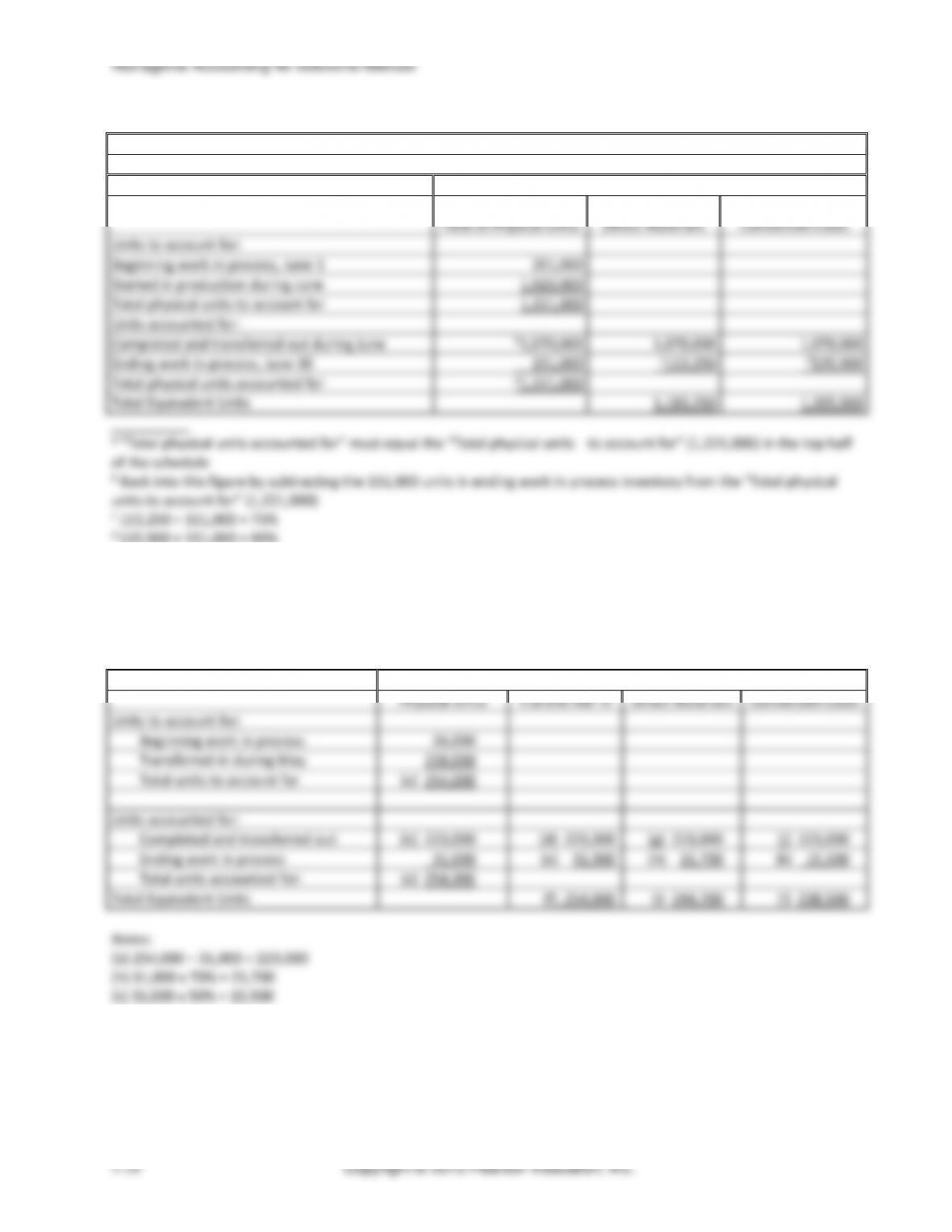

Equivalent Units

Units to account for:

2,000

Transferred in during December

Total physical units to account for

Units accounted for:

December

22,000

Managerial Accounting 4e Solutions Manual

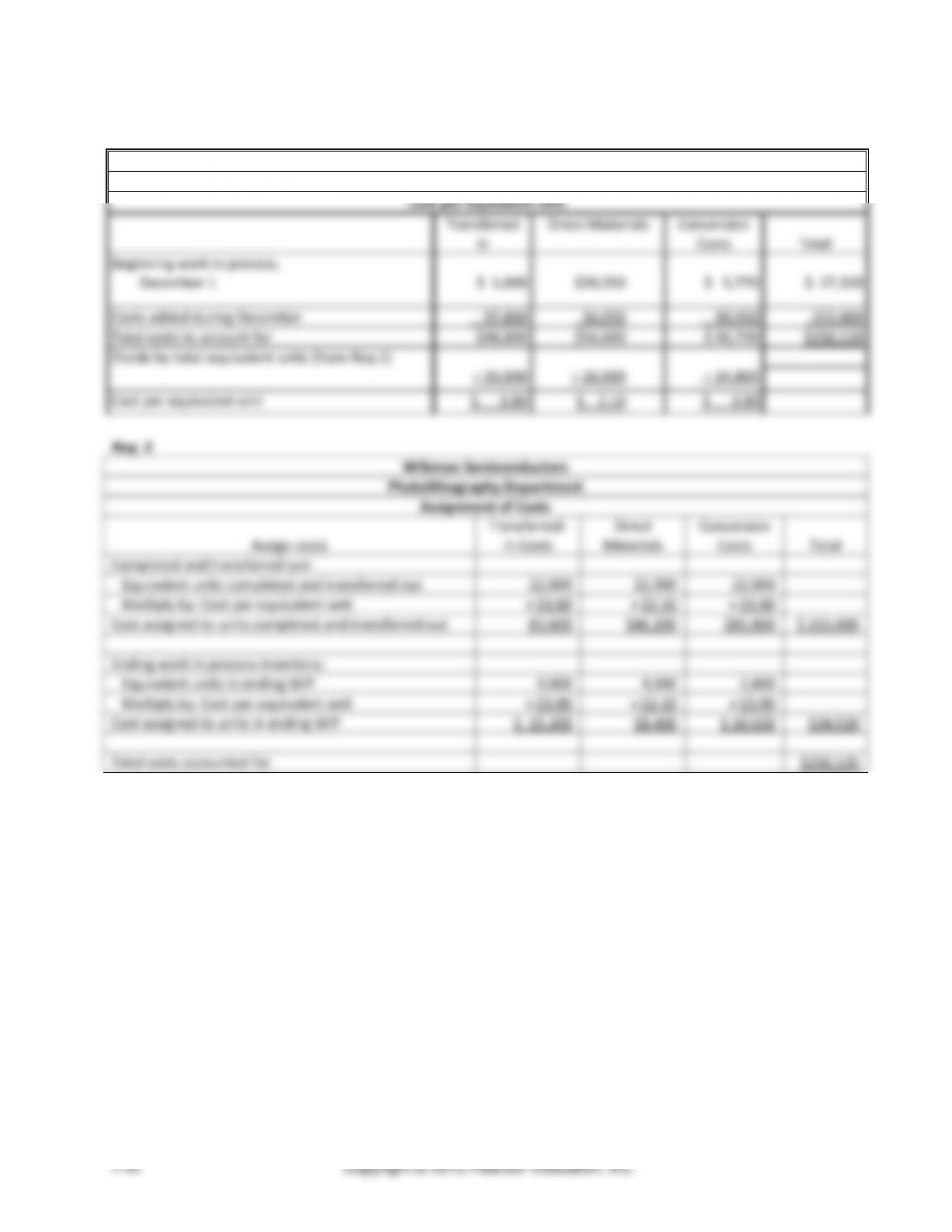

(continued) E5–47B

Req. 2

Wilkman Semiconductors

Photolithography Department

Cost per Equivalent Unit

Transferred

In

Direct Materials

Conversion

Costs

Total

Beginning work in process,

December 1

$ 1,000

$20,550

$ 5,770

$ 27,320

Costs added during December

97,800

34,050

90,950

222,800

Total costs to account for

$98,800

$54,600

$ 96,720

$250,120

Divide by total equivalent units (from Req.1)

÷ 26,000

÷ 26,000

÷ 24,800

Cost per equivalent unit

$ 3.80

$ 2.10

$ 3.90

Req. 3

Wilkman Semiconductors

Photolithography Department

Assignment of Costs

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

22,000

22,000

22,000

Multiply by: Cost per equivalent unit

x $3.80

x $2.10

x $3.90

Cost assigned to units completed and transferred out

83,600

$46,200

$85,800

$ 215,600

Ending work in process inventory:

Equivalent units in ending WIP

4,000

4,000

2,800

Multiply by: Cost per equivalent unit

x $3.80

x $2.10

x $3.90

Cost assigned to units in ending WIP

$ 15,200

$8,400

$ 10,920

$34,520

Total costs accounted for

$250,120