Chapter 5 Process Costing

Copyright © 2015 Pearson Education, Inc.

5-1

Chapter 5

Process Costing

Quick Check

Answers:

QC-1. c

QC-3. c

QC-5. d

QC-7. d

QC-9. a

QC-2. c

QC-4. a

QC-6. d

QC-8. b

QC-10. b

(5-10 min.) S5-1

Job Costing System

• Direct materials, direct labor, and manufacturing overhead are assigned to each job.

• Direct materials, direct labor, and manufacturing overhead flow into a single Work in Process Inventory

Managerial Accounting 4e Solutions Manual

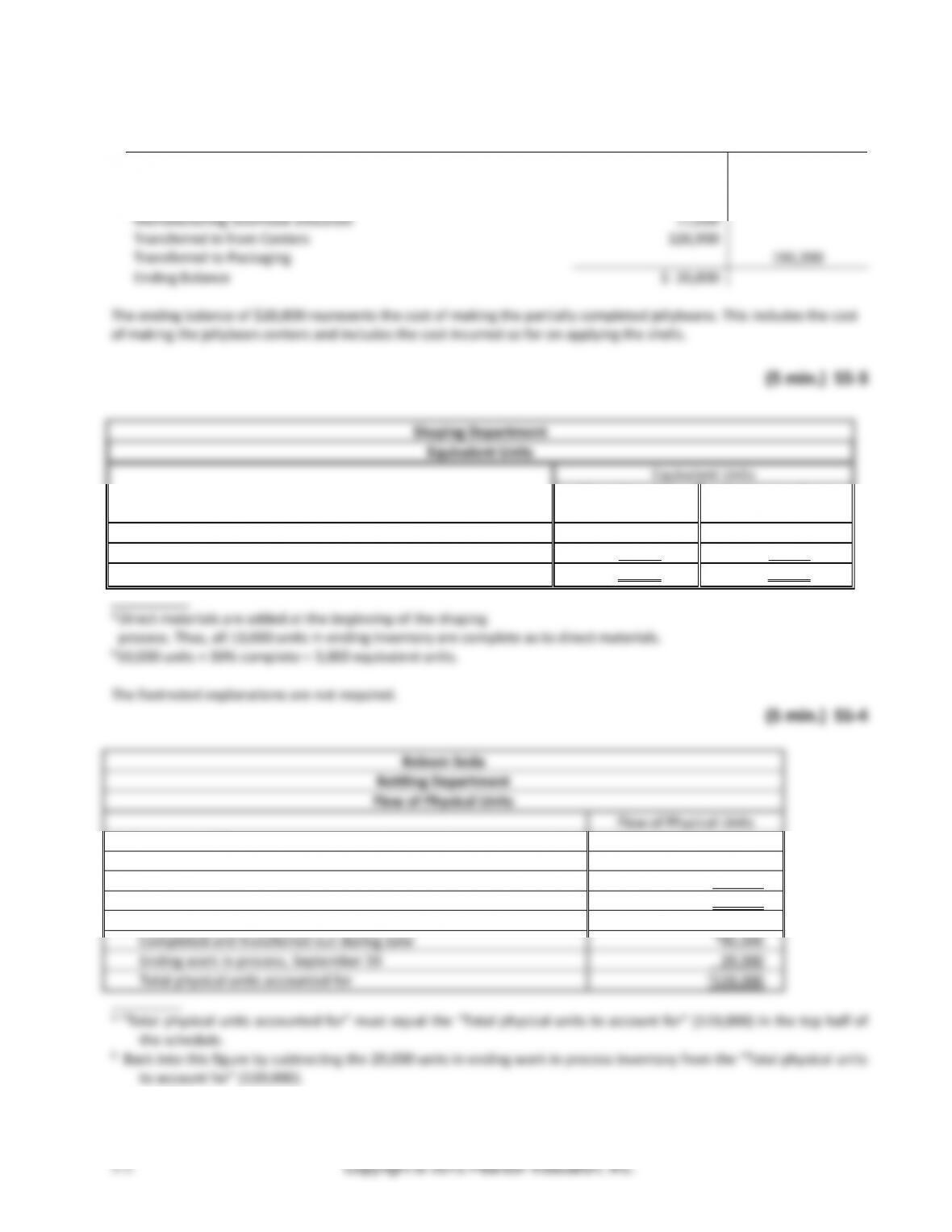

(5 min.) S5-2

Work in Process Inventory — Shells

Beginning Balance

$ 18,100

Direct materials used

42,500

Direct labor

12,500

Manufacturing overhead allocated

17,000

Transferred in from Centers

126,900

Transferred to Packaging

196,200

Ending Balance

$ 20,800

Chapter 5 Process Costing

(5 min.) S5–5

Equivalent Units

Physical Units

Direct Materials

Conversion Costs

Units accounted for:

Completed and transferred out

116,300

a116,300

a116,300

Ending work in process, July 31

9,300

b0

c3,348

Total physical units accounted for:

125,600

Total equivalent units

116,300

119,648

__________

a116,000 = 116,300 physical units × 100% complete

b 0 = 9,300 physical units × 0% complete (direct materials are

added at the end of the process)

c 3,348 = 9,300 physical units × 36% complete with respect to

conversion costs

(5 min.) S5–6

1. The “units completed and transferred out” are completely finished in the Frying Department, otherwise they

2. All of the direct materials have been added, so they are 100% complete with respect to direct materials:

3. The total equivalent units for the month are calculated as follows:

Equivalent Units

Direct Materials

Conversion Costs

Completed and transferred out during March

1,200,000

1,200,000

Ending work in process, March. 31

110,000

74,800

Total equivalent units

1,310,000

1,274,800

Managerial Accounting 4e Solutions Manual

(5 min.) S5-7

MacIntyre Company

Month Ended May 31

Direct

Materials

Conversion Costs

Total

Beginning Work in Process, May 1

$ 43,000

$ 25,000

$ 68,000

Costs added during May

103,000

a162,000

265,000

Total costs to account for

$146,000

$187,000

$333,000

__________

a Conversion costs ($162,000) = direct labor ($12,000) +

manufacturing overhead ($150,000)

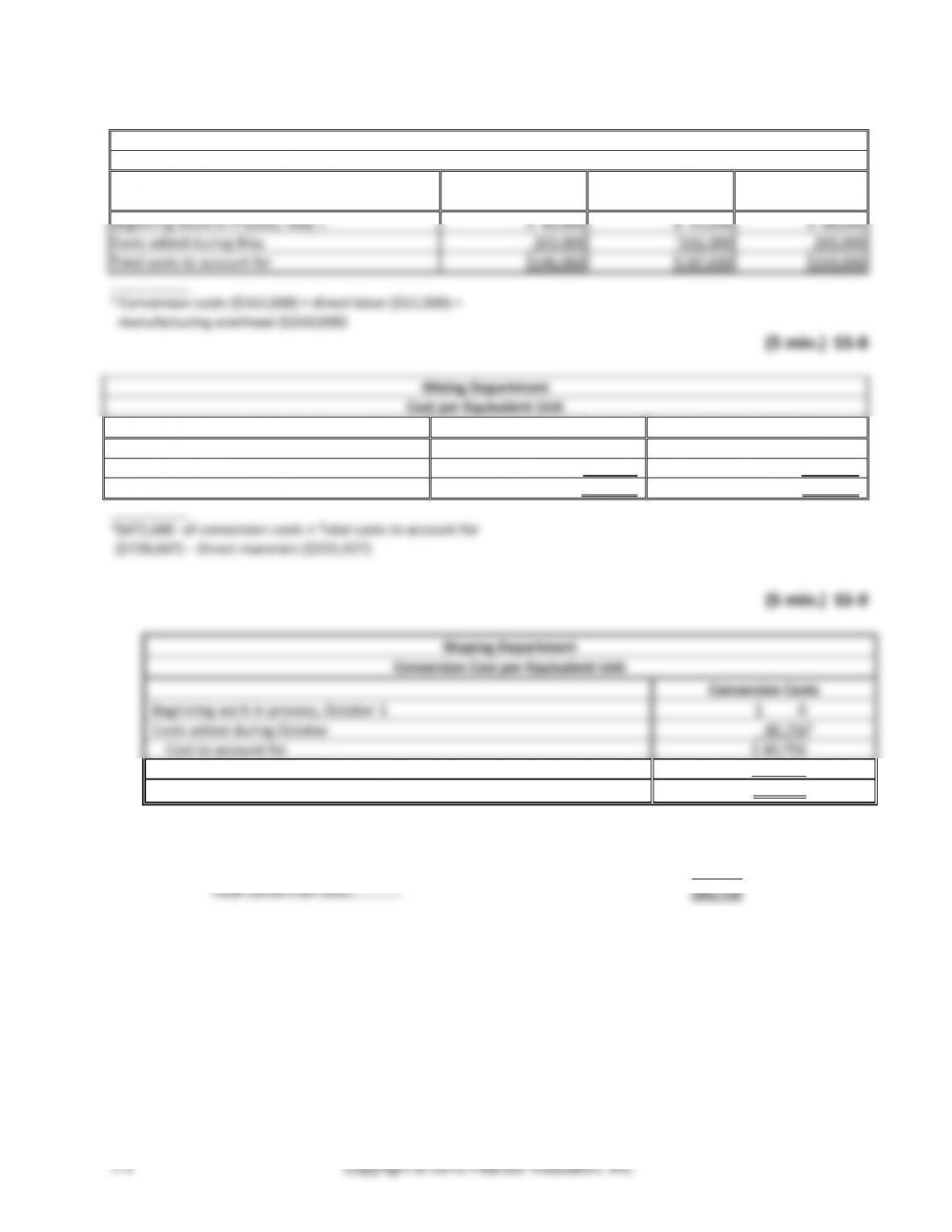

(5 min.) S5–8

Mixing Department

Cost per Equivalent Unit

Direct Materials

Conversion Costs

Total costs to account for

$255,927

a$472,680

÷ Total equivalent units

÷ 52,230

÷ 45,450

Cost per equivalent unit

$ 4.90

$ 10.40

Beginning work in process, October 1

Costs added during October

Divide by total equivalent units

Managerial Accounting 4e Solutions Manual

(5-10 min.) S5–12

1a.

Donahue Corp.

Assignment of Costs

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

69,000

69,000

69,000

Multiply by: Cost per equivalent unit

x $2.84

x $0.75

x $1.56

Cost assigned to units completed and transferred out

$ 195,960

$ 51,750

$107,640

$355,350

1b.

Donahue Corp.

Assignment of Costs

Assign costs

Transferred-in

Costs

Direct Materials

Conversion

Costs

Total

Ending work in process inventory:

Equivalent units in ending WIP

9,000

8,400

4,400

Multiply by: Cost per equivalent unit

x $2.84

x $0.75

x $1.56

Cost assigned to units in ending WIP

$ 25,560

$ 6,300

$ 6,864

$ 38,724

2. The “Total costs accounted for” is $394,074 ($355,350 + $38,724).

The “Total costs accounted for” figure must match the “Total costs to account for” figure.

1. The company’s cost per square foot of making one unit is $4.50 ($2.44 + $0.40 + $1.66)

3.

Sales price per square foot

$13.00

Less: Cost per square foot

(4.50)

Gross profit per square foot

$ 8.50

4.

Square feet sold

165,000

Gross profit per square foot

× $8.50

Total gross profit

$1,402,500

Chapter 5 Process Costing

(10 min.) S5–14

Req. 1

Direct labor

+

Manufacturing overhead

=

Conversion costs

$21,780 ($10,280 +

$11,500)

+

$25,500

=

$47,280

Req. 2

Total filtration costs

÷

Total number of liters

=

Average filtration cost per liter

$166,180 ($10,280 +

$11,500 + $25,500 +

$118,900)

÷

205,000

=

$0.81 (rounded)

Req. 3

If only 165,000 liters were completely filtered and ozonated, the remaining 40,000 were incomplete, the cost of a

completely filtered and ozonated liter would be more the average filtration cost per liter calculated in Requirement 2.

This is because a decrease in the denominator of the formula will result in a greater cost per liter.

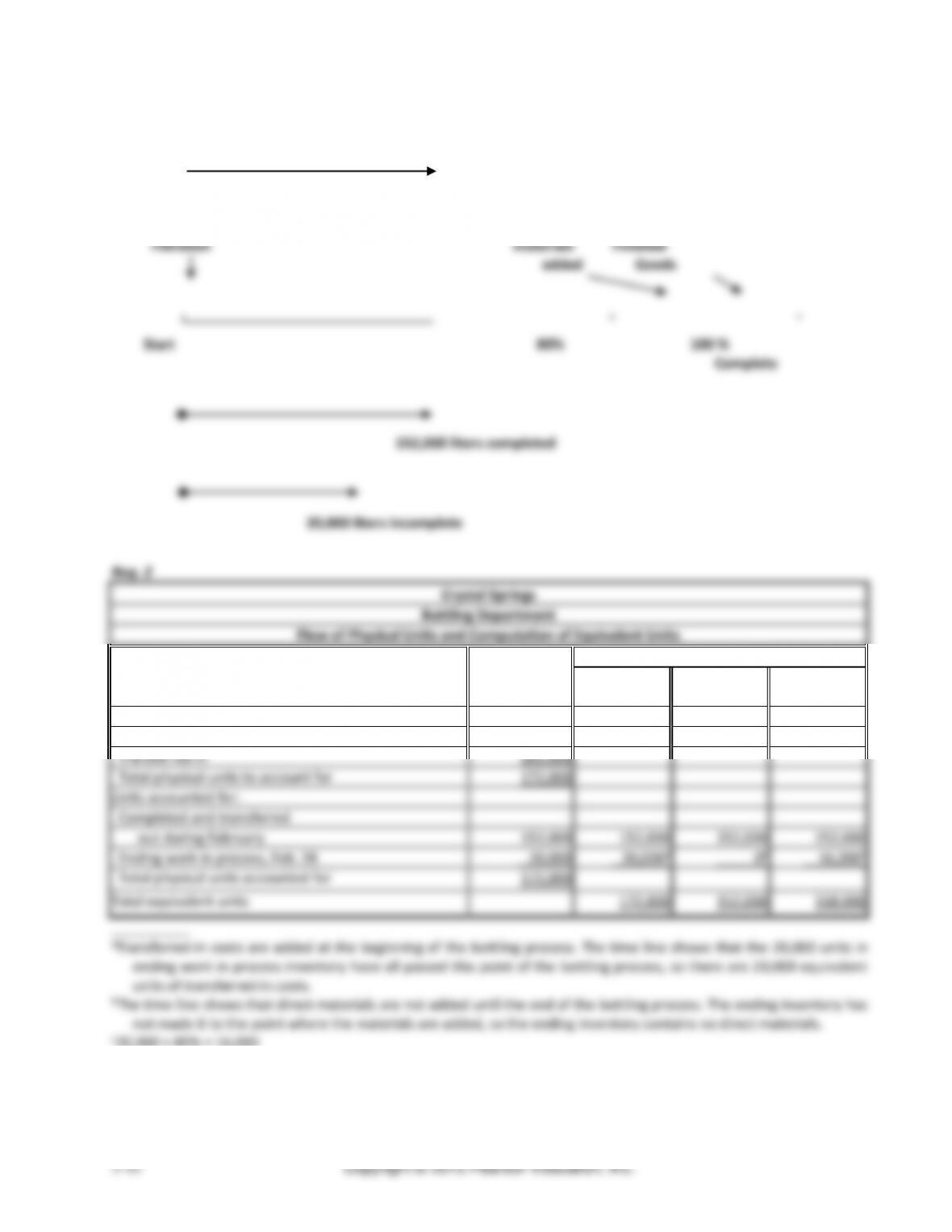

(10 min.) S5–15

Req. 1

Filtration Process

……………………… Conversion costs added evenly throughout process

Managerial Accounting 4e Solutions Manual

(continued) S5–15

Req. 2

Crystal Springs

Filtration Department

Flow of Physical Units and Computation of Equivalent Units

Equivalent Units

Flow of Production

Flow of Physical

Units

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, May 1

0

Started in production during May

205,000

Total physical units to account for

205,000

Units accounted for:

Completed and transferred out during May

165,000

165,000

165,000

Ending work in process, May 31

40,000

a40,000

b32,000

Total physical units accounted for

205,000

Equivalent Units

205,000

197,000

__________

a The ending inventory is 80% of the way through the filtration

process, so it has passed the point where water is added. The

ending inventory therefore has 40,000 equivalent units of

water (direct materials).

b40,000 units × 80% complete as to conversion work = 32,000

equivalent units.

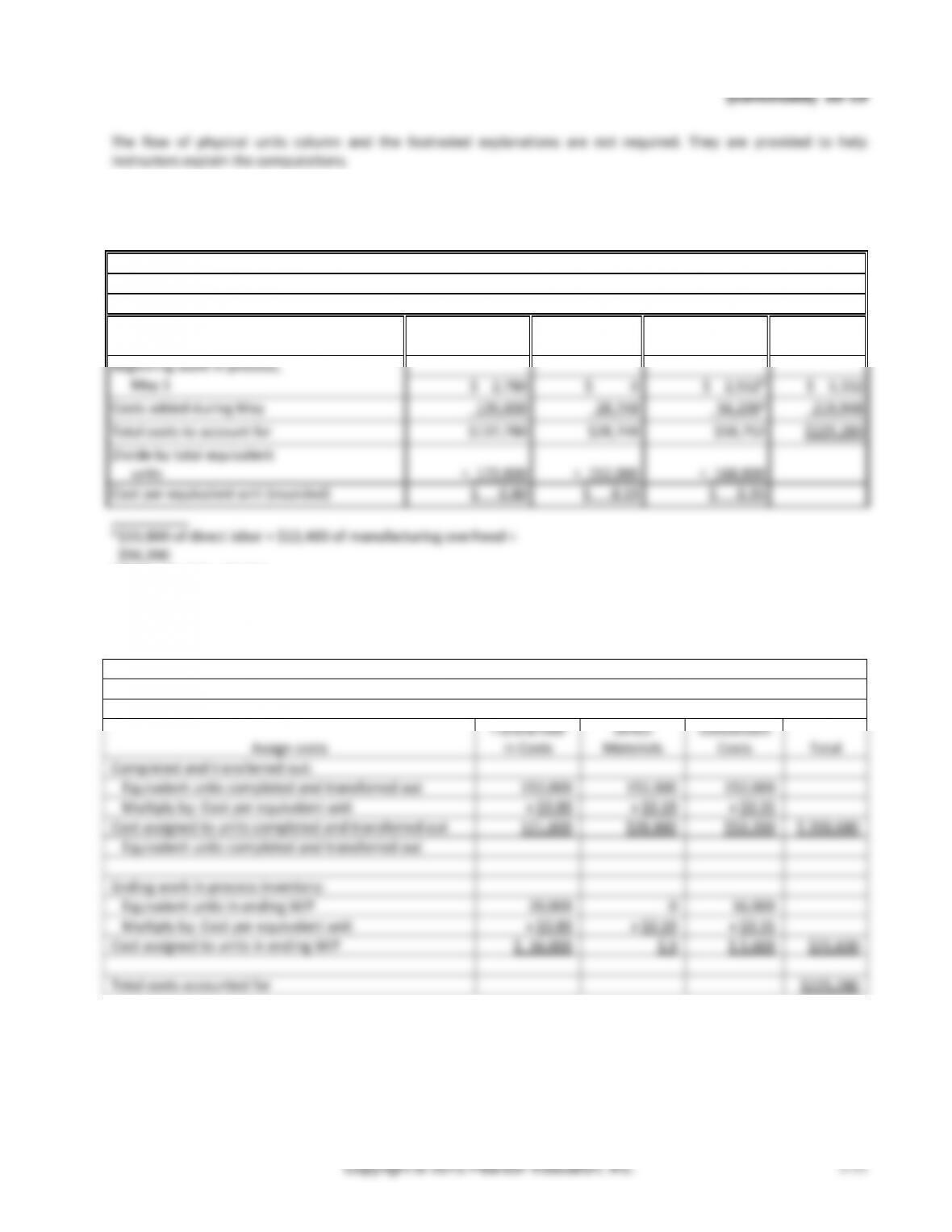

(5 min.) S5–16

Crystal Springs

Filtration Department

Cost per Equivalent Unit

Flow of Production

Direct Materials

Conversion Costs

Beginning work in process, February 1

$ 0

$ 0

Costs added during February

118,900

47,280

Total Costs to account for

$ 118,900

$ 47,280a

Divide by total equivalent units (from Req. 2)

÷ 205,000

÷ 197,000

Cost per equivalent unit

$ 0.58

$ 0.24

__________

a $10,280 + $11,500 + 25,500 of wages and manufacturing

overhead

Chapter 5 Process Costing

(10 min.) S5–17

Reqs. 1 and 2

Crystal Springs

Filtration Department

Assign Costs

Direct

Materials

Conversion Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

165,000

165,000

Multiply by: Cost per equivalent unit

x $ 0.58

x $ 0.24

Cost assigned to units completed and transferred out

$ 95,700

$ 39,600

$135,300

Ending work in process inventory:

Equivalent units in ending WIP

40,000

32,000

Multiply by: Cost per equivalent unit

x $ 0.58

x $ 0.24

Cost assigned to units in ending WIP

$23,200

$ 7,680

$30,880

Total Costs to account for

$166,180

(5 min.) S5–18

(continues S5-17)

Req. 1

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Bottling

135,300

Work in Process Inventory—Filtration

135,300

Req. 2

Work in Process Inventory−Filtration

Bal. May 1

Direct materials

0

118,900

Transferred to Bottling

135,300

Direct labor

21,780

Manufacturing overhead

25,500

Bal., May 31

30,880

Managerial Accounting 4e Solutions Manual

(15 min.) S5–19

Req. 1

Conversion costs added evenly throughout the process

Transferred Transferred

in from Direct out to

Chapter 5 Process Costing

Copyright © 2015 Pearson Education, Inc.

5-11

(continued) S5–19

The flow of physical units column and the footnoted explanations are not required. They are provided to help

instructors explain the computations.

(5-10 min.) S5–20

Crystal Springs

Bottling Department

Cost per Equivalent Unit

Transferred

In

Direct Materials

Conversion Costs

Total

Beginning work in process,

May 1

$ 2,780

$ 0

$ 2,552b

$ 5,332

Costs added during May

135,000

28,748

56,200a

219,948

Total costs to account for

$137,780

$28,748

$58,752

$225,280

Divide by total equivalent

units

÷ 172,000

÷ 152,000

÷ 168,000

Cost per equivalent unit (rounded)

$ 0.80

$ 0.19

$ 0.35

__________

a $33,800 of direct labor + $22,400 of manufacturing overhead =

$56,200

b $560 + $1,992 = $2,552

(10 min.) S5–21

Crystal Springs

Bottling Department

Assignment of Costs

Assign costs

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Total

Completed and transferred out:

Equivalent units completed and transferred out

152,000

152,000

152,000

Multiply by: Cost per equivalent unit

x $0.80

x $0.19

x $0.35

Cost assigned to units completed and transferred out

121,600

$28,880

$53,200

$ 203,680

Equivalent units completed and transferred out

Ending work in process inventory:

Equivalent units in ending WIP

20,000

0

16,000

Multiply by: Cost per equivalent unit

x $0.80

x $0.19

x $0.35

Cost assigned to units in ending WIP

$ 16,000

$ 0

$ 5,600

$21,600

Total costs accounted for

$225,280

Chapter 5 Process Costing

(5 min.) S5–23

1.

Dawn works in Accounting at White Star Consulting.

She does not disclose that one of the companies

bidding on a contract to provide payroll services for

White Star employs her daughter.

Integrity – Mitigate actual conflicts of interest,

regularly communicate with business associates

to avoid apparent conflicts of interest. Advise all

parties of any potential conflicts.

2.

This quarter, the company switched from using the

FIFO method of process costing to the weighted–

average method of process costing. Clarke, the chief

accountant, did not disclose the change in methods in

the reports because he did not want to have to justify

the change.

Credibility – Disclose all relevant information

that could reasonably be expected to influence

an intended user’s understanding of the

reports, analyses, or recommendations.

3.

Darla Cortez is an accountant at Green Manufacturing,

Inc. This past month, she guessed at the percentage of

completion rather than asking the plant manager what

the actual percentage of completion was. She figured it

wouldn’t matter and would just be a hassle to talk to

the plant manager.

Competence – Provide decision support

information and recommendations that are

accurate, clear, concise, and timely.

4.

At a party, Kelvin gets carried away with bragging about

the production process that he has helped to develop

at his company. A party-goer who works for a

competitor overhears.

Confidentiality – Keep information confidential

except when disclosure is authorized or legally

required.

5.

Process costing has always confused Amber, an

accountant for Griffith Corporation. At the end of the

year she just accepts the bookkeeper’s numbers for

ending inventory and cost of goods sold even though

the bookkeeper does not have formal training in

process costing.

Competence – Maintain an appropriate level of

professional expertise by continually developing

knowledge and skills.

Managerial Accounting 4e Solutions Manual

Exercises (Group A)

(15-20 min) E5-24A

Reqs. 1 and 2

Raw Materials Inventory

Beginning Balance

23,000

Direct materials purchased

178,000

Direct materials used in mixing

150,000

Direct materials used in packaging

34,000

Ending Balance

17,000

Direct materials used

150,000

Direct labor

11,800

Manufacturing overhead allocated

65,000

Transferred to baking

229,000

Ending Balance

10,200

Beginning Balance

Direct labor

Transferred in from Mixing

Transferred to Packaging

Ending Balance

Work in Process Inventory — Packaging Department

Beginning Balance

Direct materials used

Direct labor

Manufacturing overhead allocated

42,000

Transferred in from Baking

306,000

Ending Balance

13,100

Beginning Balance

Transferred in from Packaging

Ending Balance

$ 385,000

÷ 3,375,000

$ 0.11

Chapter 5 Process Costing

(10-15 min.) E5-25A

Chelsea’s Chocolate Pies

Flow of Physical Units and Computation of Equivalent Units

Equivalent Units

Flow of Physical Units

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process, November 1

204,000

Started in production during November

1,015,000

Total physical units to account for

1,219,000

Units accounted for:

Completed and transferred out during November

b1,065,000

1,065,000

1,065,000

Ending work in process, November 30

154,000

c115,500

d123,200

Total physical units accounted for

a1,219,000

Total Equivalent Units

1,180,500

1,188,200

__________

a “Total physical units accounted for” must equal the “Total physical units to account for” (1,219,000) in the top half

of the schedule

b Back into this figure by subtracting the 154,000 units in ending work in

process inventory from the “Total physical units to account for” (1,219,000)

c 115,500 = 154,000 × 75%

d 123,200 = 154,000 × 80%

(10-15 min.) E5-26A

Note: Students may have filled out the chart, or they may have just given an answer for each lettered item.

Equivalent Units

Physical Units

Transferred–in

Direct Materials

Conversion Costs

Units to account for:

Beginning work in process

24,000

Transferred-in during May

232,000

Total units to account for

(a) 256,000

Units accounted for:

Completed and transferred out

(b) 227,000

(d) 227,000

(g) 227,000

(j) 227,000

Ending work in process

29,000

(e) 29,000

(h) 26,100

(k) 17,400

Total units accounted for:

(c) 256,000

Total Equivalent Units

(f) 256,000

(i) 253,100

(l) 244,400

Notes:

(b) 256,000 – 29,000 = 227,000

(h) 29,000 x 90% = 26,100

(k) 29,000 x 60% = 17,400

Managerial Accounting 4e Solutions Manual

(20 min.) E5-27A

Req. 1

Conversion costs added evenly throughout the process

Direct materials

Req. 2

The Lucy Paint Company

Blending Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Units to account for:

Beginning work in process, May 1

0

Started in production during May

8,400

Total physical units to account for

8,400

Units accounted for:

Completed and transferred out during May

6,200

6,200

6,200

Ending work in process, May 31

2,200

2,200a

880b

Total physical units accounted for

8,400

Total equivalent units

8,400

7,080

__________

a The time line shows that all direct materials are added at the

beginning of the blending process, so the ending work in

process inventory is complete as to materials.

Chapter 5 Process Costing

(continued) E5-27A

Req. 3

The Lucy Paint Company

Blending Department

Cost per Equivalent Unit

Cost per Equivalent Unit:

Direct Materials

Conversion Costs

Total

Beginning work in process, May 1

$ 0

$ 0

$ 0

Costs added during May

5,460

2,832c

8,292

Total costs to account for

$5,460

$2,832

$8,292

Divide by total equivalent units (from Req. 2)

÷ 8,400

÷ 7,080

Cost per equivalent unit

$ 0.65

$ 0.40

__________

c$920 + $1,912 = $2,832

Req. 4

The Lucy Paint Company

Blending Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

6,200

6,200

Multiply by: Cost per equivalent unit

x $ 0.65

x $ 0.40

Cost assigned to units completed and transferred out

$ 4,030

$ 2,480

$6,510

b) Ending work in process inventory:

Equivalent units in ending WIP

2,200

880

Multiply by: Cost per equivalent unit

x $ 0.65

x $ 0.40

Cost assigned to units in ending WIP

$1,400

$ 352

$1,782

Total costs to account for

$8,292

Req. 5

The average cost per gallon transferred out of blending is:

$6,510

=

$1.05 per gallon

6,200 gallons

Managers will want to know this cost to compare it to their budgeted target costs. They may also use the cost

information when setting selling prices.

Managerial Accounting 4e Solutions Manual

(15 min.) E5-28A

(continues E5-27A)

Req. 1

Note: Students may prepare 3 separate journal entries or one summary entry (as shown below) to record the three

Chapter 5 Process Costing

(continued) E5-29A

e.

Work in Process Inventory—Assembly

6,900

Wages Payable

4,800

Manufacturing Overhead

2,100

f.

Work in Process Inventory—Finishing

10,900

Wages Payable

4,500

Manufacturing Overhead

6,400

g.

Work in Process Inventory—Finishing

10,550

Work in Process Inventory—Assembly

10,550

h.

Finished Goods Inventory

15,700

Work in Process Inventory—Finishing

15,700

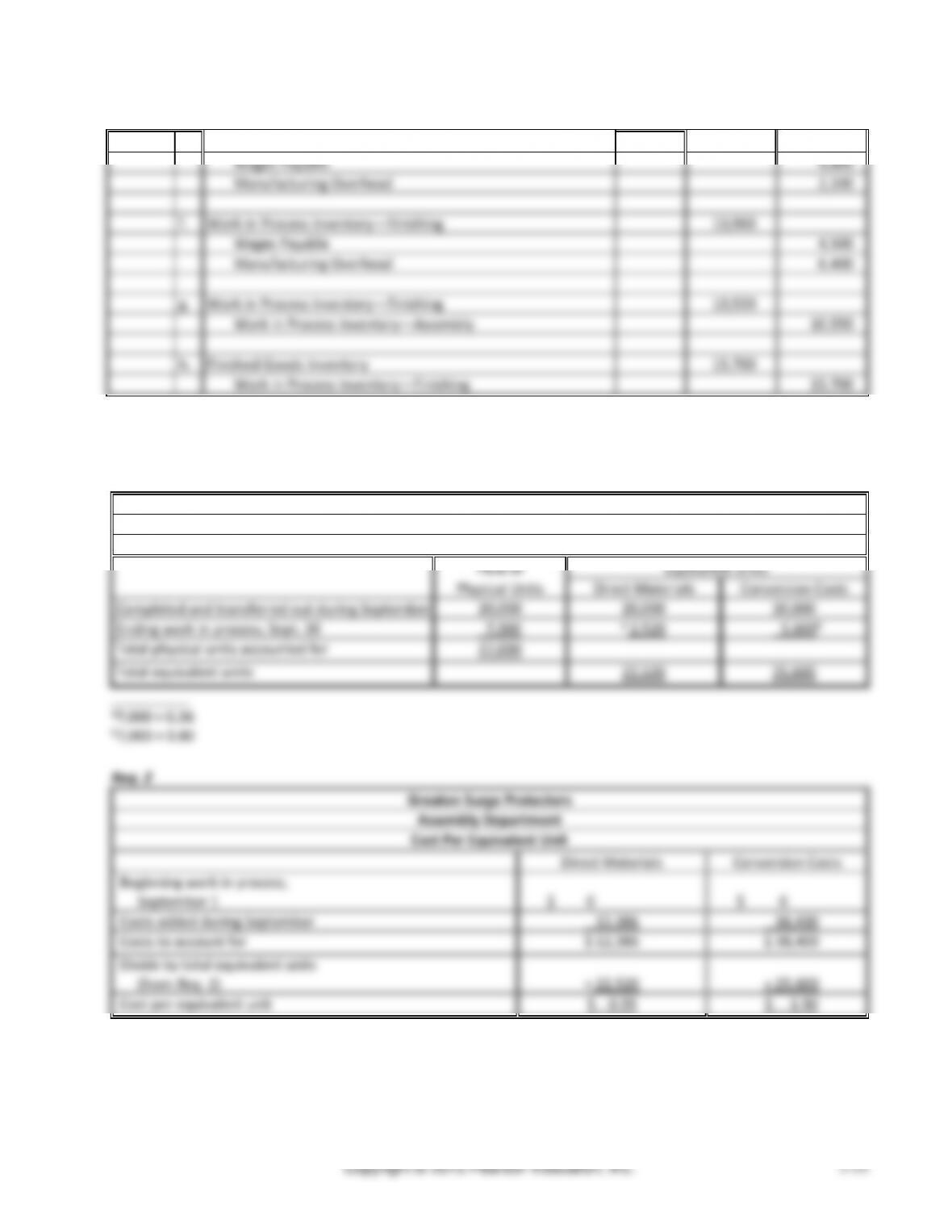

(25-30 min.) E5-30A

Req. 1

Greaton Surge Protectors

Assembly Department

Flow of Physical Units and Computation of Equivalent Units

Flow of

Equivalent Units

Physical Units

Direct Materials

Conversion Costs

Completed and transferred out during September

20,000

20,000

20,000

Ending work in process, Sept. 30

7,000

a 2,520

5,600b

Total physical units accounted for

27,000

Total equivalent units

22,520

25,600

__________

a7,000 × 0.36

b7,000 × 0.80

Req. 2

Greaton Surge Protectors

Assembly Department

Cost Per Equivalent Unit

Direct Materials

Conversion Costs

Beginning work in process,

September 1

$ 0

$ 0

Costs added during September

12,386

38,400

Costs to account for

$ 12,386

$ 38,400

Divide by total equivalent units

(from Req. 1)

÷ 22,520

÷ 25,600

Cost per equivalent unit

$ 0.55

$ 1.50

Managerial Accounting 4e Solutions Manual

(continued) E5-30A

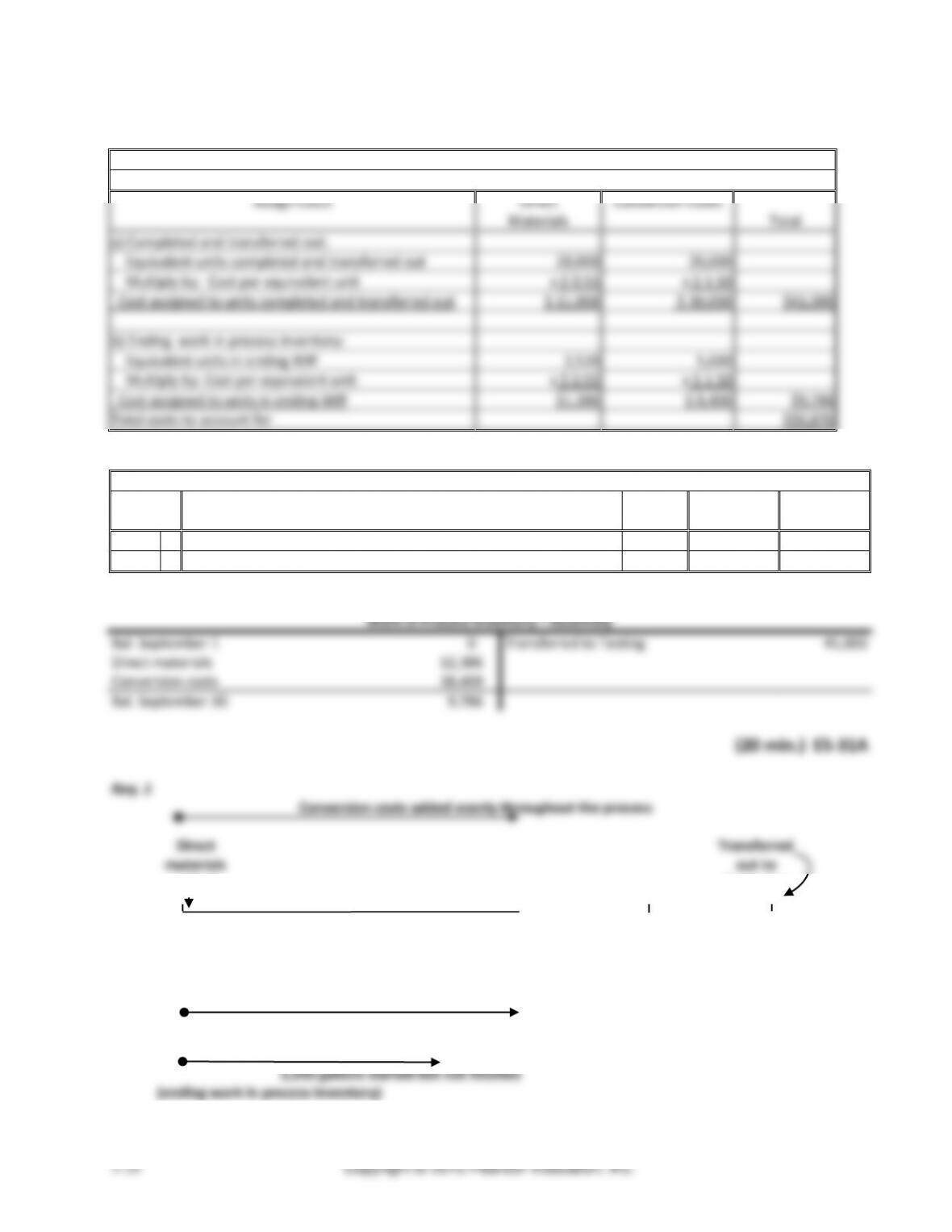

Req. 3

Great Surge Protectors

Assembly Department

Assign Costs

Direct

Materials

Conversion Costs

Total

a) Completed and transferred out:

Equivalent units completed and transferred out

20,000

20,000

Multiply by: Cost per equivalent unit

x $ 0.55

x $ 1.50

Cost assigned to units completed and transferred out

$ 11,000

$ 30,000

$41,000

b) Ending work in process inventory:

Equivalent units in ending WIP

2,520

5,600

Multiply by: Cost per equivalent unit

x $ 0.55

x $ 1.50

Cost assigned to units in ending WIP

$1,386

$ 8,400

$9,786

Total costs to account for

$50,876

Req. 4

Journal

DATE

ACCOUNTS AND EXPLANATIONS

POST.

REF.

DEBIT

CREDIT

Work in Process Inventory—Testing

41,000

Work in Process Inventory—Assembly

41,000

Req. 5

Work in Process Inventory—Assembly

Bal. September 1

0

Transferred to Testing

41,000

Direct materials

12,386

Conversion costs

38,400

Bal. September 30

9,786

(20 min.) E5-31A

Req. 1

Conversion costs added evenly throughout the process

Direct Transferred

materials out to

added Packaging

Start 80% 100%

Completion

6,420 gallons completed and transferred out